ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

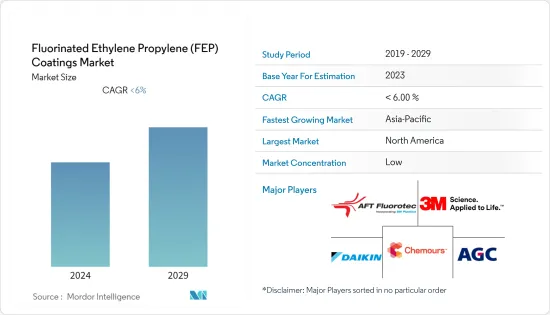

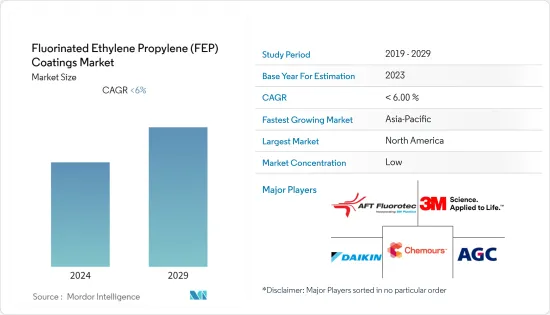

불소화 에틸렌 플로필렌 코팅 시장 규모는 2024년 4억 2,395만 달러로 추정되고, 2029년 5억 3,928만 달러에 이를 것으로 예측되며, 예측기간(2024-2029년)의 CAGR은 4.93%로 성장할 것으로 예상됩니다.

2020년에는 COVID-19의 팬데믹이 시장에 부정적인 영향을 미쳤습니다. 그러나 현재 시장은 팬데믹 이전 수준에 이르고 있으며 앞으로 몇 년동안 안정적인 성장이 예상됩니다.

주요 하이라이트

전자기기 및 식품가공 분야에 대한 수요 증가가 시장을 독점할 것으로 예상됩니다.

환경에 대한 우려가 증가하고 엄격한 환경보호청(EPA) 규정이 시장 성장을 방해할 수 있습니다.

앞으로 몇 년간 광섬유 산업의 새로운 용도로 시장 성장이 기대됩니다.

북미가 시장을 독점하고 미국과 캐나다 등 국가에서 소비가 가장 많습니다.

FEP 코팅 시장 동향

전기 및 전자 산업의 높은 수요

FEP 코팅은 전기 및 전자 산업에서 중요한 코팅 재료 중 하나입니다. FEP는 우수한 절연체이기 때문에 제조 공정에서 사용되는 가혹한 화학물질을 유지 및 운송하는 능력이 있어, 전선상에 수축시켰을 때 내약품성을 부여하면서 전기 절연을 실시하는데 이상적입니다.

반도체 집적 회로는 포토리소그래피, 에칭, 세정, 박막 증착, 연마 등의 공정을 거쳐 제조됩니다.

FEP 코팅은 반도체 산업에서 사용하기에 적합하며, 웨이퍼 캐리어, 튜브, 피팅, 펌프 부품 등의 제조 공정에서 사용되며, 반도체 제조에서 고순도 화학물질의 운송에 이상적입니다.

FEP 코팅의 특수 등급은 PC, 휴대폰, LCD, 플라즈마, LED 디스플레이 등의 전자 기기를 생산하는 반도체 산업의 높은 수요를 충족시키기 위해 개발되었습니다.

반도체산업협회(SIA)의 결론과 예측에 따르면 2023년 세계 반도체 산업 매출은 약 5,268억 달러로 2022년에 비해 8.2% 감소했습니다. 2023년 초 세계 반도체 매출은 낮은 수준이었으나 하반기에는 강력히 회복되었습니다. 또한 2024년 세계 반도체 매출은 2자리 전후 시장 성장이 관찰될 것으로 추정됩니다.

또한 전자정보기술산업협회(JEITA)에 따르면 평면 TV의 국내 출하 대수는 2023년 1월 36만 5,000대가 되어 시장 성장을 뒷받침하고 있습니다.

이러한 요인들은 예측 기간 동안 FEP 코팅 시장 수요가 증가할 것으로 예상됩니다.

시장을 독점하는 북미

FEP 코팅 수요가 높은 이유는 북미에서 식품 가공, 광섬유, 일렉트로닉스, 석유 및 가스, 화학 가공 산업이 증가하고 있기 때문입니다.

예를 들어, 캐나다 농업 농식품성(AAFC)에 따르면, 캐나다에서는 식음료 가공 산업이 생산액으로 가장 큰 제조업이며, 2022년의 상품 판매액은 1,565억 달러에 상당합니다.

게다가 VanillaPlus-the global voice for telecoms IT에 따르면 2022년 신규 케이블 수요는 약 9,130만f-km(화이버 킬로미터)이며, 2025년에는 1억2,700만fk-m에 달할 것으로 예측됩니다. 이러한 성장 동향은 FEP 코팅 시장을 촉진할 것으로 예상됩니다.

북미의 식품 가공 부문의 성장은 사람들의 포장 식품에 대한 과도한 의존과 식품 가공 기업의 강력한 비계에 의해 견조합니다. Tyson Foods, Nestle, PepsiCo는 이 지역에서 사업을 전개하는 중요한 식품 가공 기업입니다. 이 기업들은 시장 성장을 뒷받침하고 있습니다.

이와 같이, 다양한 용도로부터 수요 증가는 FEP 코팅 수요를 급증할 것으로 예상됩니다.

FEP 코팅 산업 개요

FEP 코팅 시장은 부분적으로 단편화됩니다. 시장의 주요 기업으로는 AGC Inc., 3M, DAIKIN INDUSTRIES Ltd., AFT Fluorotec Limited, The Chemours Company 등이 있습니다(순부동).

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

식품산업의 눌림 방지 용도에 있어서의 PTFE를 대신하는 비용 대비 효과

전자 기기의 반도체에 있어서의 FEP 코팅의 대두

억제요인

환경 문제의 고조와 엄격한 EPA 규제

기타 억제요인

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁도

제5장 시장 세분화(금액 베이스 시장 규모)

제품 유형별

분말 코팅

액체 코팅

용도별

조리기구 및 식품 가공

화학처리

석유 및 가스

전기 및 전자

광섬유

의료

기타

지역별

아시아태평양

중국

인도

일본

한국

태국

말레이시아

인도네시아

베트남

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

스페인

러시아

노르딕

터키

기타 유럽

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

나이지리아

카타르

아랍에미리트(UAE)

이집트

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴 및 협정

시장 점유율(%) 및 랭킹 분석

주요 기업의 전략

기업 프로파일

3M

AFT Fluorotec Limited

AGC Inc.

DAIKIN INDUSTRIES Ltd

Dongyue Chemical

GMM Pfaudler

Fluorocarbon Group

Hubei Everflon Polymer Co. Ltd

Impreglon UK Limited

INOFLON

Praxair ST Technology Inc.

Precision Coating Company Inc.

Rudolf Gutbrod GmbH

Shanghai 3F New Materials Co. Ltd

The Chemours Company

Toefco Engineered Coating Systems Inc.

Zeus Company Inc.

제7장 시장 기회 및 향후 동향

AJY

영문 목차

영문목차

The Fluorinated Ethylene Propylene Coatings Market size is estimated at USD 423.95 million in 2024, and is expected to reach USD 539.28 million by 2029, growing at a CAGR of 4.93% during the forecast period (2024-2029).

In 2020, the COVID-19 pandemic negatively impacted the market. However, the market has now reached pre-pandemic levels and is expected to grow steadily in the coming years.

Key Highlights

The increasing demand for electronic appliances and the food processing sector is expected to dominate the market.

Rising environmental concerns and stringent EPA regulations may hinder the growth of the market.

In the coming years, the market is expected to grow due to new applications in the optical fiber industry.

North America dominated the market, with the largest consumption in countries such as the United States and Canada.

High Demand from Electrical & Electronics Industry

FEP coatings are one of the important coatings materials in the electrical and electronics industry. They have the ability to hold and transport harsh chemicals that are used during manufacturing processes since FEP is an outstanding insulator and is ideal in providing electrical insulation while conferring chemical resistance when shrunk over wires.

Integrated circuits of semiconductors are produced using photolithography, etching, cleaning, thin film deposition, and polishing.

FEP coatings are well suited for applications in the semiconductor industry, where they are used in the process of manufacturing wafer carriers, tubing, fittings, and pump parts, which are ideal for transporting high-purity chemicals in semiconductor manufacturing.

Special grades of FEP coatings are being developed to meet the high demand of the semiconductor industry, which produces electronic equipment such as personal computers, cellular phones, LCDs, plasma, and LED displays.

As per the conclusions and estimations of the Semiconductor Industry Association (SIA), global semiconductor industry sales were around USD 526.8 billion in 2023, marking a decrease of 8.2% compared to 2022. It was observed that global semiconductor sales were low in early 2023 but rebounded strongly during the second half of the year. Furthermore, it was estimated that around double-digit market growth will be observed in the global semiconductor sales in 2024.

As per the Japan Electronics and Information Technology Industries Association (JEITA), Japan transported 365 thousand units of flat-panel-display TVs domestically in January 2023, thereby boosting market growth.

These aforementioned factors are expected to increase the demand in the FEP coatings market during the forecast period.

North America to Dominate the Market

The high demand for fluorinated ethylene propylene (FEP) coatings is due to the rising food processing, fiber optics, electronics, oil and gas, and chemical processing industries in North America.

For instance, according to Agriculture and Agri-Food Canada (AAFC), the food and beverage processing industry was the most significant manufacturing industry in Canada in terms of value of production, with sales of goods worth USD 156.5 billion in 2022.

Furthermore, the demand for new cabling was about 91.3 million f-km (fiber kilometers) in 2022, and it is projected to reach 127 million fk-m by 2025, according to VanillaPlus - the global voice for telecoms IT. Such growth trends are expected to propel the market for fluorinated ethylene propylene (FEP) coatings.

The growth of the food processing sector in North America is robust due to people's excessive dependence on packaged food products and the strong foothold of food processing companies. Tyson Foods, Nestle, and PepsiCo are important food processing companies operating in the region. These companies help boost market growth.

In March 2022, Nestle announced an investnment plan of USD 675 million in a new plant in Metro Phoenix, Arizona, United States, to produce beverages such as oat milk coffee creamers to meet the increasing consumer demand for plant-based products. The plant is expected to start operation in 2024, thus boosting market growth in the food processing sector.

Thus, the increasing demand from various applications is expected to surge the demand for fluorinated ethylene propylene (FEP) coatings in the near future.

Fluorinated Ethylene Propylene (FEP) Coatings Industry Overview

The fluorinated ethylene propylene (FEP) coatings market is partially fragmented. Some of the major players in the market include AGC Inc., 3M, DAIKIN INDUSTRIES Ltd, AFT Fluorotec Limited, and The Chemours Company (in no particular order).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Cost-effective Alternative to PTFE in Non-stick Applications of the Food Industry

4.1.2 Rising Prominence of FEP Coatings in the Semiconductors of Electronic Appliances

4.2 Restraints

4.2.1 Rising Environmental Concerns and Stringent EPA Regulations

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

5.1 By Product Type

5.1.1 Powder Coating

5.1.2 Liquid Coating

5.2 By Application

5.2.1 Cookware and Food Processing

5.2.2 Chemical Processing

5.2.3 Oil and Gas

5.2.4 Electrical & Electronics

5.2.5 Fiber Optics

5.2.6 Medical

5.2.7 Othe Applications

5.3 By Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Thailand

5.3.1.6 Malaysia

5.3.1.7 Indonesia

5.3.1.8 Vietnam

5.3.1.9 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 France

5.3.3.4 Italy

5.3.3.5 Spain

5.3.3.6 Russia

5.3.3.7 NORDIC

5.3.3.8 Turkey

5.3.3.9 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Colombia

5.3.4.4 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Nigeria

5.3.5.4 Qatar

5.3.5.5 United Arab Emirates

5.3.5.6 Egypt

5.3.5.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share(%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 3M

6.4.2 AFT Fluorotec Limited

6.4.3 AGC Inc.

6.4.4 DAIKIN INDUSTRIES Ltd

6.4.5 Dongyue Chemical

6.4.6 GMM Pfaudler

6.4.7 Fluorocarbon Group

6.4.8 Hubei Everflon Polymer Co. Ltd

6.4.9 Impreglon UK Limited

6.4.10 INOFLON

6.4.11 Praxair S.T. Technology Inc.

6.4.12 Precision Coating Company Inc.

6.4.13 Rudolf Gutbrod GmbH

6.4.14 Shanghai 3F New Materials Co. Ltd

6.4.15 The Chemours Company

6.4.16 Toefco Engineered Coating Systems Inc.

6.4.17 Zeus Company Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Emerging Applications in the Optical Fiber Industry