산업용 금속 포장 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)

Industrial Metal Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

상품코드:1521890

리서치사:Mordor Intelligence

발행일:2024년 07월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

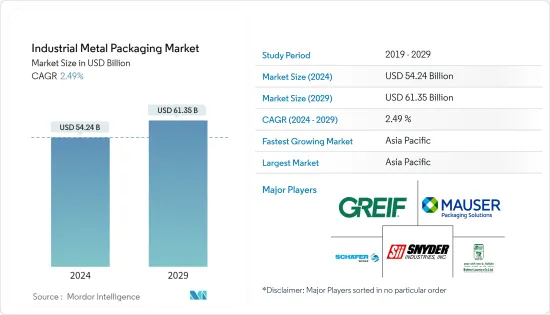

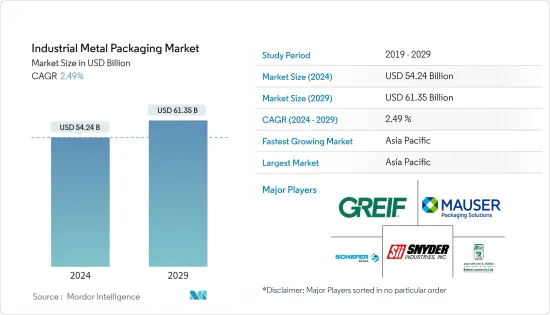

산업용 금속 포장 시장 규모는 2024년 542억 4,000만 달러로 추정되고, 2029년 613억 5,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2024-2029년) CAGR은 2.49%로 성장할 전망입니다.

주요 하이라이트

금속 벌크 컨테이너, 특히 강철과 알루미늄으로 구성된 컨테이너는 뛰어난 내구성과 보호를 제공하기 때문에 제품 무결성을 최우선으로 하는 산업에 선호되는 컨테이너가 되었습니다. 또한 신흥경제국가를 중심으로 한 세계 경기 확대와 산업화의 지속은 산업용 윤활유와 유체 수요를 자극할 것으로 예상됩니다. 그 결과 견고한 포장 솔루션에 대한 수요가 증가하고 금속 포장이 크게 성장할 것입니다.

제품 출하 중 포장은 정기적으로 토크력, 외압 및 내압, 극단적인 온도, 기타 악조건에 노출되는 것을 고려하는 것이 중요합니다. 강철의 기계적 성능은 높은 강도와 내고압성을 포함하며 쉽게 손상되지 않습니다. 그러므로 포장된 제품의 안전성을 확보하고 보관, 운송, 취급 및 사용이 용이합니다.

스틸 드럼은 석유 산업에서 사용되는 저점도 액체 및 기타 위험한 화학 물질을 보관하는 안전한 방법이며 플라스틱 드럼은 강철 드럼보다 열등합니다. 효율적인 소화 시스템과 함께 사용하는 경우, 회수형 스틸 드럼은 고온 화재에 대해 최고의 방어력을 발휘합니다. 이러한 독특한 특성은 석유 및 윤활유 분야의 산업용 드럼캔을 견인할 것으로 예상됩니다.

게다가 생산성 상승, 수입, 석유 수출은 국제 무역의 성장을 가져와 산업용 금속 포장 수요를 잠재적으로 증가시킵니다. 다양한 최종사용자 산업으로부터의 화학 및 석유 윤활유 시장의 상승과 공급망 능력의 강화에 큰 초점은 산업용 금속 포장의 요구를 촉진할 것으로 예상됩니다.

산업용 포장의 정세는 지속가능성에 대한 배려에 부응한 운송과 출하에 있어서 큰 변모를 이루고 있으며, 스틸제 중간 벌크 컨테이너(IBC)가 중요한 위치를 차지하고 있습니다. 스틸 IBC는 견고성과 재사용성과 같은 고유한 특성으로 인해 수명을 통해 환경에 미치는 영향을 크게 줄이기 위해 환경에 책임있는 포장을 보여줍니다.

산업용 금속 포장 시장 동향

액체 수송용 벌크 용기 포장 솔루션에 대한 수요 증가

IBC와 드럼 캔은 산업용 및 비산업용 제품의 대량 포장 솔루션 또는 운송 용기입니다. 이러한 솔루션은 위험물 및 비위험물의 액체 및 반액체 제품을 대량으로 보관 및 운반하도록 설계되었습니다. IBC와 같은 대량 포장 솔루션은 포장된 제품에 최적의 위생 환경을 제공하고 유출 가능성을 줄일 수 있기 때문에 널리 보급되고 있습니다.

화학, 제약, 식품 및 음료 기업은 제품 운송을 위해 고품질의 신뢰할 수 있는 벌크 용기를 요구하고 있으며, 드럼통과 IBC와 같은 산업용 금속 포장 솔루션에 새로운 기회가 탄생했습니다. 드럼통 제조업체와 IBC 제조업체는 국경을 넘는 운송이 지속가능성과 친환경 포장에 초점을 맞추고 벌크 용기에 대한 수요가 높아짐에 따라 변화하는 시장을 만나고 있습니다.

ITP 포장이 실시한 조사에 따르면, 강철 드럼은 다재다능하고 오래 지속되고 비용 효율적인 산업용 드럼 캔 형태로 많은 산업에서 여러 응용 분야에 사용됩니다. 스틸 드럼은 운송 및 물류 업계의 주력입니다. 또한 스틸 드럼에는 물류 업계의 연료가 되는 가솔린과 디젤이 보관되어 업계를 움직이고 있습니다.

중간 벌크 컨테이너(IBC)는 내구성, 다재다능성, 비용 효율성이 높기 때문에 산업용 화학물질의 포장 및 운송에 자주 사용됩니다. IBC는 운송 및 취급 시 발생하는 가혹한 조건에도 견딜 수 있도록 설계되었습니다. 미국 화학산업협회(American Chemistry Council)에 따르면 2021-2022년의 화학제품 출하액은 5조 655억 달러, 2022-2023년에는 5조 7,214억 달러에 이르렀고, 세계의 화학제품 출하액은 대폭으로 급증했습니다. 2023년이 0.6%였던 반면 2024년은 3.5%가 될 것으로 예상됩니다. 이러한 화학물질 출하 증가는 예측 기간 동안 드럼통과 IBC 시장을 견인할 것으로 예상됩니다.

성장하는 석유 화학 산업은 제품을 보호하기 위해 안전한 포장 솔루션이 필요합니다. 또한 신흥 시장에서의 페인트 및 윤활유 생산량 증가와 제품의 안전한 공급망 및 운송에 대한 수요 증가도 수요를 견인할 것으로 예상됩니다. 최종 사용자 산업의 생산에 대한 투자 증가는 산업용 강철 드럼 시장에 큰 성장 기회를 가져올 것으로 예상됩니다. 따라서, 금속 드럼 캔은 그 상대적인 재사용 가능성 및 위험물 수송의 안전성에 대한 평판에 의해 계속 널리 사용될 것입니다.

위험물의 국내 생산 증가와 원재료 가용성이 아시아태평양 시장 성장 뒷받침

금속 포장은 내구성과 외력에 대한 내성으로 인해 위험물 보관에 이상적인 솔루션입니다. 금속 드럼은 충격으로 인한 드릴링으로부터 뛰어난 보호를 제공하며 자외선(UV) 방사선에도 내성이 있어 야외 보관에 적합합니다. 자재관리은 주의 깊게 관리 및 취급하지 않으면 위협을 초래할 수 있습니다.

화학제품을 효과적으로 캡슐화하면 유출, 폭발, 부식 위험을 줄일 수 있습니다. 위험물 포장은 화학 및 제약 산업에서 널리 사용되는 화학 물질의 보호 솔루션을 설명합니다.

인도의 화학 산업은 수요 증가와 정부의 유리한 정책으로 번창하고 있습니다. 인도는 화학 생산국으로서 독자적인 지위를 자랑하고 있습니다. 인도 정부는 국내 제조 및 수출을 촉진하기 위해 화학제품 및 석유화학제품 부문에 생산 연동 장려금(PLI) 제도를 설립했습니다. 이 제도는 국내에서의 제품 판매 증가에 따라 기업에 인센티브를 부여하는 것입니다.

2023-2024년도 연방예산에서 중앙정부는 화학제품 및 석유화학제품성에 2,093만 달러를 할당했습니다. 이 배분은 화학 부문을 지원하고 더 발전시키는 정부의 헌신을 돋보이게 합니다. 화학 산업으로부터의 이러한 수요 증가는 예측 기간 동안 위험물의 산업용 금속 포장 시장을 견인하는 것으로 예상됩니다.

이 지역에서는 철강 등의 원재료를 입수할 수 있기 때문에 포장 제조업체에 장점이 있습니다. India Brand Equity Foundation에 따르면 인도의 철강 부문은 크게 성장하고 있습니다. 23년도의 조강 생산량은 125.32톤, 완성강 생산량은 121.29톤이었습니다.

위험물의 운송은 자산 손실을 최소화하고 모든 법적 컨테이너 준수 요건을 모니터링하기 위해 면밀히 관리해야 합니다. IBC의 전자 태깅은 산업용 물질의 추적성을 용이하게 할 것으로 예상되며, 제조업체는 IBC의 분실 및 파손으로 인한 비용을 절감해야 합니다. IBC는 드럼 캔에 비해 저장 비용이 낮고 대량으로 액체를 운반하는 데 사용됩니다. 드럼 캔의 둥근 형태는 충분한 미사용 공간을 형성하지만 IBC는 효율적인 공간 사용을 보장합니다. 또한 금속 포장의 편리함은 여러 번 사용할 수 있으므로 시장 성장을 가속합니다.

산업용 금속 포장 산업 개요

산업용 금속 포장 시장은 다양한 세계 기업과 현지 기업이 다양한 최종 사용자 산업을 위해 다양한 제품 포트폴리오를 제공하기 때문에 세분화되었습니다. 이 시장에서 사업을 전개하는 주요 기업으로는 Greif Inc., Mauser Packaging Solutions, Balmer Lawrie &, Snyder Industries Inc., SCHAFER Werke GmbH, Time Mauser Industries Pvt. Ltd. 등이 있습니다. 진출기업은 시장에서 발자국을 확대하고 능력을 강화하기 위해 전략적 인수에 진출하고 있습니다.

2024년 5월, Mauser Packaging Solutions는 스틸 페일 캔, 주석 강제 일반 라인, 위생 캔 및 에어로졸 캔을 제조하는 멕시코 회사 Taenza SA de CV의 인수를 발표했습니다. 이 인수를 통해 회사는 멕시코의 제조 능력과 존재를 강화할 것입니다.

2023년 5월 ENVASES OHRINGEN GMBH는 스페인과 네덜란드에서 식품 및 산업 제품의 금속 포장을 제조하는 Domiberia Group의 인수를 발표했습니다. 이를 통해 ENVASES OHRINGEN GMBH는 유럽의 지리적 범위를 확대합니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건 및 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

산업 밸류체인 분석

업계의 매력-Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁 기업간 경쟁 관계

지정학적 시나리오가 시장에 미치는 영향

제5장 시장 역학

시장 성장 촉진요인

액체 수송용 벌크 용기 포장 솔루션 수요 증가

위험물 저장용 금속 포장의 기술 혁신

시장 성장 억제요인

플라스틱 드럼과 같은 대체 포장 솔루션의 존재

제6장 시장 세분화

재료 유형별

알루미늄

스틸

제품 유형별

IBC류

수송용 배럴 및 드럼

벌크 용기(페일캔, 배럴 등)

최종 사용자 산업별

음식

화학 및 의약품

석유 및 석유화학

건축 및 건설

자동차

지역별

북미

미국

캐나다

유럽

영국

독일

프랑스

스페인

이탈리아

아시아

중국

인도

일본

태국

베트남

호주 및 뉴질랜드

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

사우디아라비아

남아프리카

이집트

아랍에미리트(UAE)

제7장 경쟁 구도

기업 프로파일

Greif Inc.

Mauser Packaging Solutions

Balmer Lawrie & Co. Ltd

ENVASES OHRINGEN GMBH

SCHAFER Werke GmbH

Sicagen India Limited

Time Mauser Industries Pvt. Ltd

THIELMANN PORTINOX SPAIN SA

Snyder Industries Inc.

American Keg Company(BLEFA BEVERAGE SYSTEMS)

Lancaster Container Inc.

P. Wilkinson Containers Ltd

Bison IBC Ltd

Colep Packaging(RAR Group Company)

Peninsula Drums

제8장 투자 분석

제9장 시장의 미래

AJY

영문 목차

영문목차

The Industrial Metal Packaging Market size is estimated at USD 54.24 billion in 2024, and is expected to reach USD 61.35 billion by 2029, growing at a CAGR of 2.49% during the forecast period (2024-2029).

Key Highlights

Metal bulk containers, particularly those composed of steel and aluminum, provide exceptional durability and protection, making them the preferred container for industries that prioritize product integrity. Also, the continued global expansion and industrialization, especially in developing economies, are expected to stimulate the demand for industrial lubricants and fluids. As a result, there will be an increased demand for sturdy packaging solutions, positioning metal packaging for substantial growth.

Throughout product shipment, it is important to consider that the package is regularly exposed to torque forces, external and internal pressure, extreme temperatures, and other unfavorable conditions. Steel's mechanical performance includes high strength and high-pressure resistance and cannot be damaged easily. This ensures the safety of packaged products and facilitates storage, transportation, handling, and use.

The steel drums are a safe way to store low-viscosity fluids and other hazardous chemicals used in the oil industry; plastic drums are inferior to steel drums. When employed with an efficient fire suppression system, steel drums of the retrieving type provide the best protection against high-temperature fires. Such unique properties are expected to drive industrial drums in the petroleum and lubricant sector.

In addition, the rising productivity, imports, and oil exports result in the growth of international trade, potentially increasing demand for industrial metal packaging. The rise in the market for chemicals and petroleum lubricants from varied end-user industries and a significant focus on strengthening the supply chain capability is expected to drive the need for industrial metal packaging.

The landscape of industrial packaging is undergoing a profound transformation in transportation and shipping fueled by sustainability considerations, and steel intermediate bulk containers (IBCs) occupy a prominent position. Steel IBCs illustrate environmentally responsible packaging due to their inherent characteristics, such as robustness and reusability, which significantly reduce environmental impact throughout their lifespan.

Industrial Metal Packaging Market Trends

Growing Demand for Bulk Container Packaging Solutions for Liquid Transportation

IBCs and drums are bulk-packaging solutions or shipping containers for industrial and non-industrial products. These solutions are designed to store and transport large quantities of hazardous and non-hazardous liquid and semi-liquid products. Bulk packaging solutions such as IBCs are gaining wider popularity due to their ability to provide an optimal hygienic environment for packed products and reduce the possibilities of spillage.

Chemical, pharmaceutical, food, and drink companies seek high-quality and reliable bulk containers for product transportation, creating new opportunities for industrial metal packaging solutions such as drums and IBCs. Drum and IBC manufacturers are encountering a changing market as the demand for bulk containers grows, with cross-border transportation focusing on sustainability and eco-friendly packaging.

According to a study conducted by ITP Packaging, steel drums are a versatile, long-lasting, cost-effective form of industrial drums with multiple uses across many industries. Steel drums are the mainstay of the transportation and logistics industry. Steel drums also store the petrol and diesel that fuel the logistics industry and keep the industry running in steel drums.

Intermediate bulk containers (IBCs) are often utilized for packaging and transporting industrial chemicals due to their durability, versatility, and cost-effectiveness. IBCs are designed to withstand harsh conditions encountered during shipping and handling. According to the American Chemistry Council, the value of chemical shipments in 2021-2022 was USD 5,065.5 billion and reached USD 5,721.4 billion in 2022-2023; global chemical shipments experienced a significant surge. The Y-o-Y growth of chemical output is projected to be 3.5% in 2024 compared to 2023, which was 0.6%. Such an increase in chemical shipments would drive the market for drums and IBCs during the forecast period.

The growing petrochemical industry requires safe packaging solutions to protect its products. Also, the rising production of paints and lubricants in emerging markets and the ever-increasing demand for a secure supply chain and transportation of products are anticipated to drive the demand. Increased investment in end-user industries' production will provide significant growth opportunities for the industrial steel drums market. Therefore, metal drums will remain widely used due to their relative reusability and reputation for safety in transporting hazardous materials.

Increasing Domestic Production of Hazardous Materials and Availability of Raw Materials Aids the Market Growth in the APAC Region

Metal packaging is an ideal solution for hazardous material storage due to its durability and resistance against external forces. Metal drums provide superior protection from impact puncture and are resistant to ultraviolet (UV) radiation, making them suitable for outdoor storage. Hazardous materials could pose a threat if not managed or handled carefully.

Effective encapsulation of chemical products reduces the risk of spillage, explosion, and corrosion. Hazardous material packaging offers a protective solution to chemicals extensively used in the chemical and pharmaceutical industries.

India's chemical industry thrives due to increasing demand and favorable government policies. India boasts a unique position as a chemical producer. The Government of India established a Production Linked Incentive (PLI) scheme for the chemical and petrochemical sector to boost domestic manufacturing and exports. This scheme incentivizes businesses based on increased product sales within the country.

In the Union Budget 2023-2024, the central government allotted USD 20.93 million to the Department of Chemicals and Petrochemicals. This allocation highlights the government's commitment to support and further develop the chemical sector. Such increased demand from the chemical industry would drive the industrial metal packaging of hazardous materials market during the forecast period.

The availability of raw materials such as steel in the region benefits the packaging manufacturers. According to the India Brand Equity Foundation, India's steel sector has grown significantly. In FY23, crude and finished steel production stood at 125.32 metric tons and 121.29 metric tons, respectively.

Shipping hazardous materials must be managed closely to minimize asset loss and monitor all legal container compliance requirements. Electronic tagging of IBCs is forecast to facilitate traceability of industrial substances, which manufacturers need to reduce the cost of lost or damaged IBCs. IBCs are used for the low storage cost and transportation of fluids in bulk quantity compared to drums. The round shape of drums forms ample unused space, while IBCs ensure efficient space utilization. Also, the usability of metal packaging can be used multiple times to drive market growth.

Industrial Metal Packaging Industry Overview

The industrial metal packaging market is fragmented due to various global and local players offering various product portfolios for different end-user industries. The key players operating in the market include Greif Inc., Mauser Packaging Solutions, Balmer Lawrie & Co. Ltd, Snyder Industries Inc., SCHAFER Werke GmbH, and Time Mauser Industries Pvt. Ltd. The players are entering into strategic acquisitions to expand their footprint in the market and strengthen their capabilities.

In May 2024, Mauser Packaging Solutions announced the acquisition of Taenza SA de CV, a company in Mexico that manufactures steel pails, tin-steel general line, sanitary, and aerosol cans. The acquisition would help the company strengthen its manufacturing capability and presence in Mexico.

In May 2023, ENVASES OHRINGEN GMBH announced the acquisition of Domiberia Group, a manufacturer of metal packaging for food and industrial products in Spain and the Netherlands. This will help the company broaden its geographical reach in Europe.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Value Chain Analysis

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Bargaining Power of Suppliers

4.3.2 Bargaining Power of Buyers

4.3.3 Threat of New Entrants

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

4.4 Impact of Geopolitical Scenario on the Market

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Growing Demand for Bulk Container Packaging Solutions for Liquid Transportation

5.1.2 Innovation in Metal Packaging for Storage of Hazardous Materials

5.2 Market Restraints

5.2.1 Presence of Alternate Packaging Solutions such as Plastic Drums and Others

6 MARKET SEGMENTATION

6.1 By Material Type

6.1.1 Aluminium

6.1.2 Steel

6.2 By Product Type

6.2.1 IBCs

6.2.2 Shipping Barrels and Drums

6.2.3 Bulk Containers (Pails, Kegs, etc.)

6.3 By End-user Industry

6.3.1 Food & Beverage

6.3.2 Chemicals and Pharmaceuticals

6.3.3 Oil and Petrochemicals

6.3.4 Building and Construction

6.3.5 Automotive

6.4 By Geography***

6.4.1 North America

6.4.1.1 United States

6.4.1.2 Canada

6.4.2 Europe

6.4.2.1 United Kingdom

6.4.2.2 Germany

6.4.2.3 France

6.4.2.4 Spain

6.4.2.5 Italy

6.4.3 Asia

6.4.3.1 China

6.4.3.2 India

6.4.3.3 Japan

6.4.3.4 Thailand

6.4.3.5 Vietnam

6.4.3.6 Australia and New Zealand

6.4.4 Latin America

6.4.4.1 Brazil

6.4.4.2 Mexico

6.4.4.3 Argentina

6.4.5 Middle East and Africa

6.4.5.1 Saudi Arabia

6.4.5.2 South Africa

6.4.5.3 Egypt

6.4.5.4 United Arab Emirates

7 COMPETITIVE LANDSCAPE

7.1 Company Profiles*

7.1.1 Greif Inc.

7.1.2 Mauser Packaging Solutions

7.1.3 Balmer Lawrie & Co. Ltd

7.1.4 ENVASES OHRINGEN GMBH

7.1.5 SCHAFER Werke GmbH

7.1.6 Sicagen India Limited

7.1.7 Time Mauser Industries Pvt. Ltd

7.1.8 THIELMANN PORTINOX SPAIN SA

7.1.9 Snyder Industries Inc.

7.1.10 American Keg Company (BLEFA BEVERAGE SYSTEMS)