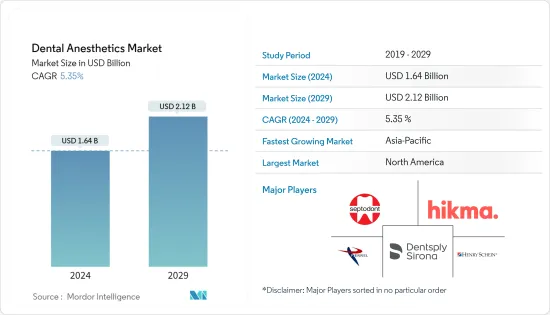

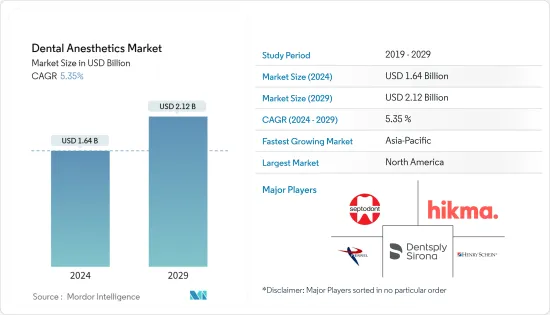

치과용 마취제 시장 규모는 2024년 16억 4,000만 달러로 추정 및 예측되며, 2029년에는 21억 2,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029) 동안 5.35%의 CAGR로 성장할 것으로 예상됩니다.

치과용 마취제 시장에는 치과 의사가 치과 시술 시 환자의 구강 감각을 마비시키기 위해 사용하는 다양한 제품이 포함됩니다. 이러한 치과용 마취제는 주사, 젤, 크림, 스프레이 등 다양한 형태로 제공됩니다. 치과 외상 및 충치 유병률 증가, 외과적 시술의 발전으로 인한 무통 치과 치료에 대한 수요 증가는 예측 기간 동안 시장 성장을 촉진할 것으로 예상되는 주요 요인으로 꼽힙니다.

충치의 높은 유병률은 치과 치료의 필요성과 치과용 마취제에 대한 수요를 증가시킬 것으로 예상됩니다. 예를 들어, Office for Health Improvement &Disparities가 2023년 10월에 발표한 데이터에 따르면, 2022년 영국에서는 5세 아동의 23.7%가 충치를 경험했습니다. 또한 충치 유병률은 지역별로 차이가 있어 영국 남서부의 19.1%에서 영국 북서부의 30.6%까지 다양했습니다. 따라서 높은 충치 유병률과 치과 치료는 치과용 마취제에 대한 수요를 증가시켜 예측 기간 동안 시장 성장에 기여할 것으로 예상됩니다.

최근 치과 국소 마취 투여의 발전은 치과 수술 중 쉽게 사용할 수 있어 치과용 마취제의 사용량을 증가시킬 것으로 예상됩니다. 예를 들어, 2024년 2월, Milestone Scientific Inc.는 Meridian Endo &Perio와 STA 단일 치아 마취 시스템(STA)을 직접 판매하기 시작했습니다. 또한, 2022년 8월에는 시냅스 덴탈(Synapse Dental)이 펜형 전자 치과 마취 도구인 'Dental Pain Eraser'라는 새로운 장치를 출시하였습니다. 이러한 첨단 마취제 공급 시스템은 불편함을 줄이고 치과용 마취제 채택을 증가시켜 시장 성장을 촉진할 수 있습니다.

이러한 충치 및 치과 외상 유병률 증가와 치과 수술의 기술적 발전은 예측 기간 동안 치과용 마취제 시장의 성장을 가속화할 것으로 보입니다. 그러나 마취제와 관련된 환자의 불편함, 위험 및 합병증은 예측 기간 동안 시장 성장을 억제할 가능성이 높습니다.

국소 마취는 전신마취보다 부작용과 합병증이 드물고 보통 경미하기 때문에 전신마취보다 선호되고 있습니다. 리도카인은 그 안전성과 효과로 인해 치과에서 가장 널리 사용되는 국소 마취제이자 치과에서 가장 널리 사용되는 표준입니다. 또한, 국소 마취는 전신 마취보다 비용이 저렴하고, 바이탈 및 중요한 신체 기능을 유지하기 위한 모니터링 장비가 덜 필요하기 때문에 선호됩니다. 따라서 국소 마취가 제공하는 이점으로 인해 이러한 제품에 대한 수요가 치과 의사들 사이에서 증가하고 궁극적으로 예측 기간 동안 부문 성장을 촉진 할 가능성이 높습니다.

더 많은 발치 에피소드는 적절한 국소 마취가 필요하기 때문에 예측 기간 동안 해당 부문의 성장을 촉진할 가능성이 높습니다. 예를 들어, Office for Health Improvement &Disparities가 2024년 2월에 발표한 데이터에 따르면, 2023년 런던에서 인구 10만 명당 333건의 충치 발치 에피소드가 보고되었는데, 이는 상당히 높은 수치입니다. 이로 인해 치료 중 국소 마취제 사용량이 증가하여 예측 기간 동안 이 분야의 성장을 촉진할 것으로 예상됩니다.

전신 마취로 인한 치아 손상의 위험이 높기 때문에 국소 마취제의 채택이 증가하여 이 분야의 성장을 촉진할 것으로 예상됩니다. 예를 들어, MedPress Dental Sciences가 2022년 1월에 발표한 보고서에 따르면, 치과 치료에서 전신 마취 중 가장 빈번하게 발생하는 문제 중 하나가 치아 손상이며, 이는 전신 마취의 채택을 감소시키고 국소 마취의 채택을 증가시킨 것으로 추정됩니다. 이러한 요인들은 예측 기간 동안 이 분야의 성장을 촉진할 것으로 예상됩니다.

북미는 구강 위생에 대한 높은 인식, 높은 치과 지출, 마취 전달 시스템 채택 증가로 인해 시장에서 큰 점유율을 차지할 것으로 예상됩니다. 또한, 미국에는 숙련된 치과 의사가 많고 노인 인구가 증가하고 있는 것도 예측 기간 동안 이 지역의 시장 성장을 촉진할 것으로 예상되는 주요 요인 중 하나입니다.

치과 치료 중 안전한 마취 치료에 대한 환자의 인식이 높아지면서 이 지역의 치과용 마취제 사용량이 증가할 것으로 예상됩니다. 예를 들어, 2024년 4월 미국간호마취학회(AANA)는 조기 발견이 구강 위생 문제를 가장 잘 예방할 수 있는 방법임을 국민들에게 환기시켰습니다. 또한 수술을 포함한 구강암 치료 중 안전한 치과 마취 치료를 받을 수 있도록 하는 것이 매우 중요하다는 것을 환자들에게 인식시켜야 한다고 밝혔습니다.

구강암과 구강인두암은 부담이 커서 수술 중 치과 마취의 필요성이 증가합니다. 예를 들어, 미국 암 협회에 따르면 2024년 미국에서 약 58,450건의 구강암 또는 구강인두암이 새로 발생할 것으로 예상되며, 이는 수술의 필요성과 수술 중 치과용 마취제에 대한 수요를 증가시켜 예측 기간 동안 시장 성장을 촉진할 것으로 예상됩니다.

치과용 마취제 시장은 전 세계적으로 사업을 영위하는 제한된 수의 기업이 존재하기 때문에 적당히 통합되어 있습니다. 경쟁 상황에는 Dentsply Sirona, Septodont, Pierrel SpA, Henry Schein Inc, Hikma Pharmaceuticals PLC, Cetylite Inc, Centrix Inc. Primex Pharmaceuticals 등 중요한 시장 점유율을 차지하고 있는 여러 국제 기업들에 대한 분석이 포함되어 있습니다.

The Dental Anesthetics Market size is estimated at USD 1.64 billion in 2024, and is expected to reach USD 2.12 billion by 2029, growing at a CAGR of 5.35% during the forecast period (2024-2029).

The dental anesthetics market encompasses a range of products dentists use to numb patient's mouths during dental procedures. These dental anesthetics come in various forms, such as injections, gels, creams, and sprays. The increasing prevalence of dental trauma and caries and the rising demand for painless dental treatments through advancements in surgical procedures are the major factors expected to drive the market growth over the forecast period.

The high prevalence of dental caries is expected to increase the need for dental treatment and the demand for dental anesthetics. For instance, according to the data published by the Office for Health Improvement & Disparities in October 2023, 23.7% of 5-year-old children experienced tooth decay in England in 2022. In addition, the prevalence of tooth decay varied across the regions, ranging from 19.1% in the South West to 30.6% in North West England. Hence, the high prevalence of tooth decay and dental treatment will likely boost the demand for dental anesthetics, contributing to the market growth over the forecast period.

The recent advancements in the delivery of dental local anesthesia are expected to increase the usage of dental anesthetics due to their easy usage during dental surgeries. For instance, in February 2024, Milestone Scientific Inc. started direct sales of its STA Single Tooth Anesthesia System (STA) with Meridian Endo & Perio. Additionally, in August 2022, Synapse Dental launched a new device, the Dental Pain Eraser, a pen-shaped, electronic dental anesthesia tool. Such advanced anesthetic delivery systems can decrease the discomfort produced and increase the adoption of dental anesthetics, driving market growth.

Thus, the increasing prevalence of dental caries and dental trauma and technological advancements in dental surgical procedures are poised to accelerate the growth of the dental anesthetics market over the forecast period. However, patient discomfort, risks, and complications associated with the anesthetics are likely to restrain market growth during the forecast period.

Local anesthesia is preferred over general anesthesia due to rare and usually minor side effects and complications. Lidocaine is the gold standard and most widely used local anesthetic in dentistry due to its safety and effectiveness. In addition, regional anesthesia is preferred owing to its lower cost than general anesthesia and the lower requirement for monitoring equipment to maintain vitals and essential body functions. Hence, owing to the advantages offered by local anesthesia, the demand for these products will likely increase among dentists, ultimately driving segmental growth over the forecast period.

More tooth extraction episodes need proper local anesthetics, which are likely to boost the segment's growth over the forecast period. For instance, according to data published by the Office for Health Improvement & Disparities in February 2024, in London, 333 decayed tooth extraction episodes per 100,000 population were reported in 2023, which was significantly high; this trend is estimated to continue. This, in turn, is expected to boost the usage of local anesthetics during treatment, driving the segment's growth over the forecast period.

The greater risk of dental injuries due to general anesthesia is expected to increase the adoption of local anesthetics, thereby boosting segmental growth. For instance, as per the report published by MedPress Dental Sciences in January 2022, orodental injuries were one of the most frequent problems seen during general anesthesia in dentistry, which likely decreased the adoption of general anesthetics and increased the adoption of local aesthetics. Such factors are expected to boost the segment's growth over the forecast period.

North America is expected to hold a significant share of the market owing to its high awareness of oral health, high dental spending, and increasing adoption of anesthesia delivery systems. In addition, the availability of skilled dentists and the increasing geriatric population in the United States are some of the key factors expected to boost the market's growth in the region over the forecast period.

The growing awareness among patients toward safe anesthesia care during dental procedures is expected to increase the usage of dental anesthetics in the region. For instance, in April 2024, the American Association of Nurse Anesthesiology (AANA) reminded the public that early detection was the best prevention of oral health issues. Additionally, it stated that patients needed to be aware of the critical importance of ensuring access to safe dental anesthesia care during oral cancer treatments, including surgery.

The high burden of oral or oropharyngeal cancer increases the need for dental anesthesia during surgery. For instance, according to the American Cancer Society, in the United States, around 58,450 new cases of oral or oropharyngeal cancer are expected to be recorded in 2024, which would increase the need for surgery and demand for dental anesthetics during procedures, thereby propelling the market's growth over the forecast period.

The dental anesthetics market is moderately consolidated due to the presence of limited companies operating globally. The competitive landscape includes an analysis of a few international companies that hold significant market shares, including Dentsply Sirona, Septodont, Pierrel SpA, Henry Schein Inc., Hikma Pharmaceuticals PLC, Cetylite Inc., Centrix Inc., HANSAmed Limited, Normon, and Primex Pharmaceuticals.