ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

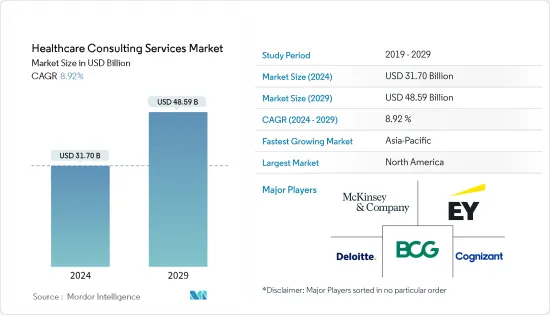

헬스케어 컨설팅 서비스 시장 규모는 2024년 317억 달러로 추정되며, 2029년에는 485억 9,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 8.92%의 CAGR을 기록할 것으로 예상됩니다.

시장 성장을 촉진하는 주요 요인으로는 헬스케어 제품에 대한 수요 증가, 의료의 질 향상과 의료비 절감에 대한 요구가 증가하고 있는 점을 들 수 있습니다.

헬스케어는 지난 몇 년 동안 증가하는 환자 인구에 대한 대응 측면에서 큰 변화를 목격했습니다. 헬스케어 컨설팅 서비스 시장은 전 세계적으로 디지털화가 빠르게 도입되면서 성장세를 보이고 있습니다. 애자일 방식을 통한 탄탄한 IT 지원은 의료 서비스 제공업체가 수익성 향상, 재고 관리 간소화, 품질 향상, 비용 절감을 통해 경쟁 우위를 확보할 수 있도록 돕습니다.

헬스케어 컨설팅 서비스를 의료와 통합하면 생활습관 개선 및 예방 의료가 효과적인 개인 식별, 환자 특성 분석, 광범위한 질병 프로파일링 분류를 통한 예측 사건 식별 및 예방 이니셔티브 지원, 비용 효율적인 치료법을 식별하기 위한 치료 비용 및 치료 비용 및 결과 분석 등의 이점을 제공할 것으로 기대됩니다. 예를 들어, 국제당뇨병연맹(International Diabetes Federation 2022)의 추산에 따르면, 2045년까지 전 세계 당뇨병 치료 비용은 기술 발전으로 인해 1조 5,400억 달러에 달할 것으로 예상되며, 이는 주로 무선 기기, 웨어러블 기기, 애플리케이션의 높은 보급에 기인하는 것으로 나타났습니다. 웨어러블 기기 및 애플리케이션의 높은 보급률에 기인합니다. 따라서 만성 질환에 대한 이러한 막대한 지출은 환자의 의료비 부담을 줄이기 위한 전략을 수립하는 헬스케어 컨설팅 서비스의 채택을 증가시킬 것으로 예상됩니다.

또한, 헬스케어 제공업체와 헬스케어 컨설팅 서비스 제공업체 간의 파트너십 증가는 예측 기간 동안 조사 대상 시장의 수요를 증가시켜 시장 성장을 촉진할 것으로 예상됩니다. 예를 들어, 2023년 6월, 데이터 분석 업체인 Vuitt, 자문 회사인 Develop Consulting, 헬스케어 개선 전문가인 Innovative Online Products, 교육 제공업체인 Click2Learn 등 4개 업체가 신디케이트를 구성하여 영국의 국가 보건 서비스(NHS)를 위한 통합 개선 파트너십을 출범시켰습니다. 이 파트너십은 NHS가 영국 의료 시스템 내에서 효율성을 실현하고, NHS 전체의 효율성 절감 및 역량 강화를 위한 전략을 수립할 수 있도록 지원합니다.

또한, 선진국과 개발도상국 정부의 우호적인 정책으로 인해 IT 헬스케어 컨설팅의 기회가 증가하고 있습니다. 다른 요인으로는 헬스케어 IT 솔루션에 대한 정부 지원의 증가와 예측 기간 동안 기술 환경의 변화 등이 있습니다. 그러나 높은 도입 비용은 시장 성장을 억제할 것으로 예상됩니다.

헬스케어 컨설팅 서비스 시장 동향

예측 기간 동안 병원 부문이 헬스케어 컨설팅 서비스 시장에서 큰 비중을 차지할 것으로 예상

병원은 IT 보안 서비스, 지원 서비스, 자원 계획, IT 인프라 관리, 모바일 컴퓨팅, 클라우드 기반 솔루션 등 업무의 디지털화가 진행되고 있습니다. 확장 가능한 운영으로 인해 의료 서비스 제공 업체는 의료 컨설팅 서비스 시장에서 수익 증가를 목격하고 있습니다.

병원의 IT 컨설팅은 디지털 헬스케어 인프라에서 보다 중요하고 지속적인 정보 흐름을 실현하는 데 도움이 됩니다. 아웃소싱 IT 컨설팅 서비스에는 분석 대시보드, 임상 플랫폼 개발 및 유지보수, 네트워크 최적화 서비스, IT 조달, 클라우드 서비스 등이 포함됩니다.

병원과 헬스케어 컨설팅 회사 간의 파트너십이 증가함에 따라 병원의 수익 성장을 유지하기 위해 IT 컨설팅 서비스에 대한 수요가 증가하여 부문의 성장을 촉진할 것으로 예상됩니다. 예를 들어, 2023년 10월 가상 의료 솔루션 제공 업체인 Cura는 사우디-독일 병원 그룹과 제휴하여 환자의 의료 서비스 접근에 혁명을 일으켰습니다. 이 제휴를 통해 환자들은 온라인 진료, 원격 모니터링, 사우디-독일 병원 그룹의 모든 지점에서 통합된 건강 정보 교환 등 다양한 의료 서비스를 이용할 수 있게 됐습니다.

또한, 병원은 수익주기 관리, 전사적 자원관리(ERP) 지원 서비스, 인구 건강 관리 등의 지원을 받고 있으며, 이 또한 시장 성장에 기여할 것으로 예상됩니다. 또한, 서비스당 지불(FFS)에서 가치 기반 진료로의 전환은 의료 서비스 제공자에 대한 압력을 증가시키고 있습니다. 따라서 예측 기간 동안 병원이 큰 시장 점유율을 차지할 것으로 예상됩니다.

북미가 시장에서 큰 비중을 차지하고 있으며, 이러한 추세는 예측 기간 동안 지속될 것으로 예상

북미 시장의 성장은 의료비 지불 및 규제 변경에 기인합니다. 그 결과, 의료 서비스 제공자들은 의료 IT 컨설팅 회사에 대한 의존도가 높아지고 있습니다.

또한, 미국의 규제 개혁으로 인해 비용 절감과 고객 만족을 위한 지불자 간의 경쟁이 치열해지고 있습니다. 헬스케어 지불자와 제공자들은 컨설팅 회사의 IT 지원을 필요로 하는 새로운 운영 모델을 적용하고 있으며, 이에 따라 기술 혁신이 진행되고 있습니다.

미국 보건복지부가 2024년 발표한 연례 실적 계획 및 보고서 데이터에 따르면, 2023년 주 및 관할 구역의 모자-영유아 가정방문(MIECHV) 프로그램 참여자 수는 164,470명이었으나 2024년에는 188,067명으로 증가하였습니다. 이처럼 산모-영유아 가정 방문의 증가는 산모-태아-영유아 케어에 대한 수요를 촉진하여 헬스케어 컨설팅 서비스 시장의 성장을 견인하고 있습니다.

또한 미국에서는 65세 이상 노인과 일부 장애인을 대상으로 주정부와 연계한 메디케어-메디케이드 서비스 센터와 같은 의료 서비스를 제공하는 정부 보조금 프로그램이 시장을 견인할 가능성이 높습니다.

재택 의료 분야에서 헬스케어 컨설팅 기업 간의 파트너십이 증가함에 따라 시장 성장을 촉진할 것으로 예상됩니다. 예를 들어, 2024년 3월 Brinster & Bergman은 재택 의료 컨설팅 회사인 Gary Carpenter and Associates와 파트너십을 체결하여 재택 의료 기관이 주정부 규제 및 세법을 탐색하는 전략으로 재택 의료 기관을 지원하고 있습니다.

또한, 크고 작은 의료 서비스 제공자는 의료 시스템의 복잡한 변화를 모두 처리할 수 없기 때문에 의료 컨설팅 서비스를 제3자 제공업체에 아웃소싱하고 있습니다. 데이터 보안 및 분석과 같은 혁신적인 접근 방식을 통해 의료 서비스 제공업체는 환자 경험을 개선하고, 그 결과 수익이 증가하면서 이익을 얻고 있습니다. 이는 북미 헬스케어 컨설팅 서비스 시장의 성장에 기여하고 있는 것으로 보입니다.

헬스케어 컨설팅 서비스 산업 개요

헬스케어 컨설팅 서비스 시장은 매우 세분화되어 있으며, 중소규모의 최종사용자들의 헬스케어 컨설팅 서비스 채택이 확대됨에 따라 건전한 성장세를 보이고 있습니다. 또한, 아시아태평양에서는 헬스케어 컨설팅 서비스의 시장 침투가 가속화될 것으로 예상되며, 신규 진입 기업들에게 성장 기회를 제공하고 있습니다. 시장 진출 기업으로는 액센츄어, 딜로이트 토즈, 보스턴 컨설팅 그룹, 코그니전트, 맥킨지 앤 컴퍼니 등이 있습니다.

기타 혜택:

엑셀 형식의 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 소개

조사 가정과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

시장 개요

시장 성장 촉진요인

헬스케어 제품에 대한 수요 증가

의료 질 향상과 헬스케어 비용 절감 요구 상승

시장 성장 억제요인

유사 기술의 존재

높은 도입 비용

Porter's Five Forces 분석

신규 참여업체의 위협

구매자/소비자의 협상력

공급 기업의 교섭력

대체품의 위협

경쟁 기업 간의 경쟁 강도

제5장 시장 세분화(금액 기준 시장 규모)

서비스 유형별

디지털 컨설팅

IT 컨설팅

컴포넌트별

서비스

솔루션

최종사용자별

병원

클리닉

생명과학 기업

용도별

재무

운영 관리

인구집단건강

지역별

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

스페인

기타 유럽

아시아태평양

중국

일본

인도

호주

한국

기타 아시아태평양

중동 및 아프리카

GCC

남아프리카공화국

기타 중동 및 아프리카

남미

브라질

아르헨티나

기타 남미

제6장 경쟁 상황

기업 개요

Deloitte Touche Tohmatsu Limited

McKinsey & Company

Accenture Consulting

Huron Consulting

PWC

Ernst & Young

The Boston Consulting Group

Bain & Company

KPMG

Cognizant

IQVIA

ZS

제7장 시장 기회와 향후 동향

ksm

영문 목차

영문목차

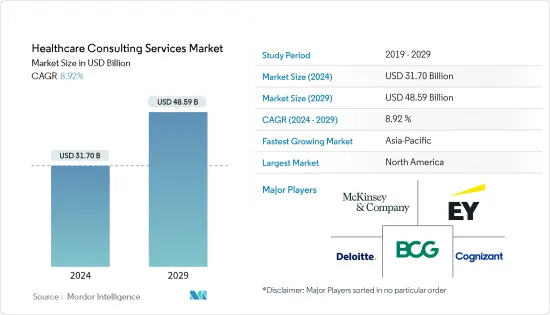

The Healthcare Consulting Services Market size is estimated at USD 31.70 billion in 2024, and is expected to reach USD 48.59 billion by 2029, growing at a CAGR of 8.92% during the forecast period (2024-2029).

The major factors driving the market growth include the rising demand for healthcare products and the rising need to improve the quality of care and reduce healthcare costs.

Healthcare has witnessed substantial changes in the past few years in terms of serving the growing patient population. The healthcare consulting services market is mainly driven by the rapid adoption of global digitalization. Robust IT support with agile methods is a competitive advantage for healthcare providers in achieving increased profitability, simplifying inventory management, improving quality, and controlling costs.

The integration of healthcare consulting services with medicine is expected to deliver benefits, like identifying individuals who may benefit from lifestyle changes or preventative care, analyzing patient characteristics, classifying broad-scale disease profiling to identify predictive events and support prevention initiatives, and analyzing the cost and outcomes of care to identify cost-effective treatments. For example, the International Diabetes Federation 2022 estimated that by 2045, the global expenditures for diabetes treatment are expected to grow to USD 1,054 billion due to technological advancements, which can primarily be attributed to the high adoption of wireless and wearable devices and applications. Therefore, such a huge expenditure on chronic diseases is anticipated to increase the adoption of healthcare consulting services to develop strategies for the reduction of the healthcare burden on patients.

Furthermore, the rising partnerships among the healthcare providers and the healthcare consulting service providers are also anticipated to increase the demand in the market studied during the forecast period, driving the market's growth. For instance, in June 2023, a syndicate of four businesses: data analyst Vuit, advisory firm Develop Consulting, healthcare improvement specialist Innovative Online Products, and training provider Click2 Learn launched an Integrated Improvement Partnership for National Health Service (NHS) in the United Kingdom. This will help the NHS realize efficiencies within the UK healthcare system and develop strategies for efficiency savings and capacity building across the NHS.

Furthermore, there has been a rise in IT healthcare consulting opportunities due to favorable government policies in developed and developing regions. Other factors include increasing government support for healthcare IT solutions and the changing technology landscape during the forecast period. However, the high cost of deployment is expected to restrain the growth of the market.

Healthcare Consulting Services Market Trends

Hospitals Segment Expected to Hold a Significant Share in the Healthcare Consulting Services Market During the Forecast Period

Hospitals are digitalizing their business practices in IT security services, support services, resource planning, IT infrastructure management, mobile computing, and cloud-based solutions. With scalable operations, healthcare providers have witnessed increased revenues in the healthcare consulting services market.

IT consulting in hospitals can help achieve a more significant and continuous flow of information within a digital healthcare infrastructure. Outsourced IT consulting services include analytics dashboards, development and maintenance of clinical platforms, network optimization services, IT procurement, and cloud services.

Rising partnerships among hospitals and healthcare consulting firms are anticipated to increase the demand for IT consulting services to sustain hospital revenue growth and thereby boost segment growth. For instance, in October 2023, Cura, a virtual healthcare solutions provider, partnered with the Saudi German Hospital Group to revolutionize patient access to healthcare services. This partnership allows patients to utilize various healthcare services, including online consultations, remote monitoring, and health information exchange integrated across all Saudi German Hospital Group locations.

Furthermore, the hospitals are also taking support for revenue cycle management, enterprise resource planning (ERP) support service, and population health, which are also anticipated to contribute to the market's growth. In addition, the transition from fee-for-service (FFS) to value-based care is increasing the pressure on healthcare providers. Thus, hospitals are anticipated to hold a significant market share during the forecast period.

North America Holds a Significant Share in the Market and is Expected to Continue the Same During the Forecast Period

The market's growth in North America is attributed to changes in medicare payments and regulations. As a result, healthcare providers are increasingly dependent on healthcare IT consulting companies.

Furthermore, with regulatory reforms in the United States, there is increased competition among payers for cost savings and customer satisfaction. Healthcare payers and providers are undergoing technological transformation as they are applying novel operating models that need IT support from consulting firms.

According to data published by the United States Department of Health and Human Services in 2024 in the form of an Annual Performance Plan and Report, the number of participants served by the state/jurisdiction maternal, infant, and early childhood home visiting (MIECHV) program in FY2023 was 164,470 compared to 188,067 in FY2024. Thus, the increase in maternal, infant, and early childhood visits fuels the demand for maternal, fetal, and infant care, boosting the growth of the healthcare consulting services market.

In addition, in the United States, government funding programs that provide healthcare services like the Centers for Medicare and Medicaid Services for people aged 65 years and older, as well as some people with disabilities working in partnership with the state governments, are likely to boost the market.

Rising partnerships among healthcare consulting firms in the home healthcare domain are anticipated to propel the market's growth. For instance, in March 2024, Brinster & Bergman entered a partnership with Gary Carpenter and Associates, a home healthcare consulting firm, to assist home healthcare agencies with strategies for exploring state regulatory and tax laws.

Moreover, small and big healthcare providers are outsourcing healthcare consulting services to third-party providers, as they cannot handle all the complex changes in the healthcare system. With innovative approaches, such as data security and analytics, healthcare providers benefit by improving the experience of patients and, therefore, gaining increased revenues. This is likely to contribute to the growth of the healthcare consulting services market in North America.

Healthcare Consulting Services Industry Overview

The healthcare consulting services market is highly fragmented and experiencing healthy growth owing to the greater adoption of healthcare consulting services by smaller and mid-sized end users. Moreover, healthcare consulting service market penetration is expected to increase in Asia-Pacific, offering growth opportunities for new entrants. Some of the players operating in the market are Accenture, Deloitte Touche Tohmatsu LLC, The Boston Consulting Group, Cognizant, and McKinsey and Company.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.2.1 Rising Demand for Healthcare Products

4.2.2 Rising Need to Improve the Quality of Care and Reduce Healthcare Costs

4.3 Market Restraints

4.3.1 Availability of Similar Technology

4.3.2 High Cost of Deployment

4.4 Porter's Five Forces Analysis

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Buyers/Consumers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)