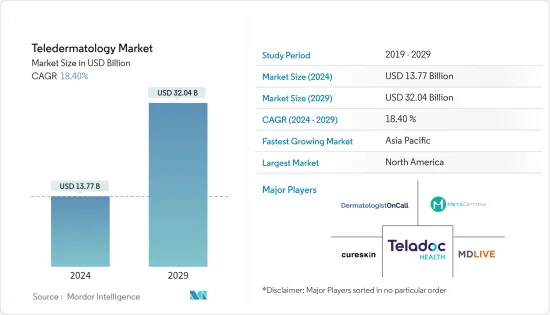

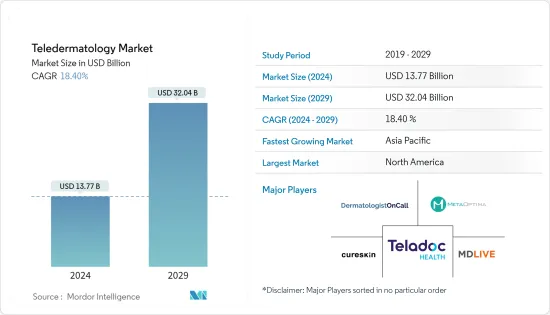

원격 피부과 시장 규모는 2024년 137억 7,000만 달러로 추정되며, 2029년에는 320억 4,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 18.40%의 CAGR로 성장할 것으로 예상됩니다.

원격 피부과는 원격의료의 한 분야로, 통신 기술을 활용해 원격지에서 피부과 의료를 제공하는 분야입니다. 평가와 진단을 위해 안전한 플랫폼을 통해 영상과 의료 정보 교환을 가능하게 하고, 피부에 문제가 있는 환자에게 원격으로 치료를 제공합니다. 원격 피부과에 대한 수요는 디지털 시대의 도래와 특히 원격지나 의료 서비스가 부족한 지역에서 피부과 의료에 대한 접근성이 향상됨에 따라 증가하고 있습니다. 피부과 의사 부족과 건선, 습진, 여드름과 같은 피부 질환의 증가로 인해 원격 피부과에 대한 수요가 급증하고 있습니다. 예를 들어, 영국 피부재단이 2023년 11월 발표한 기사에 따르면, 현재 약 2,000여 종의 피부질환이 있으며, 원격 피부과가 피부암을 포함한 약 90%에 대응할 수 있다고 합니다. 또한 환자와 의료진에게 제공되는 원격 피부과의 편의성, 접근성 및 비용 효율성은 시장 성장에 영향을 미치는 중요한 요인입니다.

또한, 중저소득 국가에서는 지리적 장벽, 긴 대기 시간, 이동의 어려움으로 인해 피부과 의사가 부족하고 피부과 의료에 대한 접근성이 제한되어 있어 원격 피부과 도입률이 급증하고 있으며, 이후 시장 성장에 박차를 가하고 있습니다. 예를 들어, 2023년 12월 Indian Journal of Dermatology, Venereology, and Leprology가 발표한 연구에 따르면, 2022년 사하라 사막 이남 아프리카의 인구 100만 명당 피부과 의사는 1명 이하로 나타났습니다. 반면 미국에서는 2022년 인구 100만 명당 34명의 피부과 의사가 있었습니다. 따라서 원격 피부과는 피부과 의사가 부족한 국가에서 피부 질환을 진단하고 관리하기 위한 강력한 교육 및 임상 지원 도구입니다. 피부과 의료에 대한 접근성을 개선하기 위해 이 기술을 도입하는 것이 향후 몇 년 동안 시장 성장의 원동력이 될 것으로 보입니다.

또한, 보다 정확한 진단 및 치료 제안을 제공하기 위해 시장 기업이 원격 피부과 시스템에 도입한 기술 발전은 고급 이미지 처리 및 데이터 분석 기능과 결합하여 시장 성장을 촉진할 것으로 예상됩니다. 예를 들어, 2022년 9월 헬스케어 기술 기업 MCI Onehealth Technologies Inc.와 인공지능 솔루션 제공업체인 Oro Health는 MCI Dermatology Connect 플랫폼을 공동 개발하여 출시했습니다. 이 플랫폼은 환자와 전문의 간의 고해상도 이미지의 안전한 전송을 포함하여 가상 피부과 치료를 위한 특별한 솔루션을 제공합니다. 전화 피부과 진료는 대면 진료의 긴 대기 시간에 비해 편안하고 장점이 있어 2024년부터 2029년까지 전화 피부과 진료에 대한 수요가 증가할 것으로 예상됩니다.

그러나 프라이버시 및 보안에 대한 우려, 규제 프레임워크 준수 부족, 신흥국에서의 상환 시설 부족 등이 2024-2029년 시장 성장을 억제할 것으로 예상됩니다.

원격 피부과는 원격진료, 원격 모니터링, 원격 교육 등 다양한 서비스를 제공합니다. 편리성, 전문적 치료 접근성, 의료 비용 절감, 건강 결과 개선, 환자 참여도 향상 등 다양한 이점을 제공합니다. 이러한 장점으로 인해 피부과 의료에 대한 수요 증가에 대응하기 위해 기존 대면 진료보다 원격 피부과 서비스 채택이 급증하고 있으며, 이는 2024년부터 2029년까지 이 분야의 성장에 유리하게 작용하고 있습니다. 예를 들어, News-Medical.Net이 2023년 10월에 발표한 보고서에 따르면 Consultant Connect의 PhotoSAF 기술은 영국에서 가장 널리 사용되는 원격 피부과 플랫폼 중 하나이며 잉글랜드, 스코틀랜드, 웨일스 NHS의 절반을 커버하고 있다고 합니다. Consultant Connect 플랫폼 출시 후 2023년 이용률은 이전 4년간 대비 2,400% 증가했으며, 이는 영국, 스코틀랜드, 웨일즈의 NHS의 절반 이상을 커버하고 있습니다. 따라서 이러한 사례는 원격 피부과 서비스가 환자 경험을 개선하고 건강 결과를 개선하며 2024년부터 2029년까지 부문 성장을 촉진할 것이라는 생각을 뒷받침합니다.

또한, 원격의료는 여드름, 모발 장애, 피부염 등 진단과 치료가 간단한 경우 필수적인 도구로 부상하고 있습니다. 예를 들어, Telemedicine and e-health Journal이 2023년 10월에 발표한 조사에 따르면, 독일에서 환자들이 원격 피부과를 이용하는 가장 큰 이유는 외래에서 피부과 치료를 받기 위해 대기하는 시간이 길기 때문인 것으로 나타났습니다. 또한, 등록 환자의 62.0%가 치료의 성공을 '좋음' 또는 '매우 좋음'으로 평가했으며, 86.1%가 원격의료의 질을 외래 진료와 동등하거나 그 이상으로 평가했다고 밝혔습니다. 또한, 2023년 4월 Life Journal지에 발표된 연구에 따르면, 원격의료 서비스를 통한 아토피피부염 진단 정확도는 84.4%로 나타났습니다. 이러한 연구는 더 많은 환자와 의료 서비스 제공자가 원격의료에 익숙해짐에 따라 원격 피부과 서비스가 향후 몇 년 동안 계속 확대될 가능성이 높다는 것을 강조합니다.

또한, 피부 질환에 대한 인식을 높이고 피부과 의료 서비스를 확대하기 위해 시장 진입 기업들이 적극적으로 투자하고 있는 것도 이 분야의 성장에 기여하고 있습니다. 예를 들어, 2024년 3월 조지워싱턴대학교 의과대학 피부과 건강과학부는 존슨앤드존슨 이노베이티브 메디슨(Johnson & Johnson Innovative Medicine)으로부터 무료 원격 피부과 프로그램인 'EACH one TEACH one'을 위해 50만 달러의 후원을 받았습니다. 이 프로그램은 미국 전역의 피부과 의료에 대한 접근성을 향상시키는 것을 목표로 합니다. 이러한 이니셔티브는 피부과 의료에 대한 접근성과 경제성을 향상시켜 원격 피부과에 대한 수요를 촉진하고 2024년부터 2029년까지 이 부문의 성장에 기여할 것으로 예상됩니다.

북미는 피부 질환에 대한 부담 증가, 의료 시설에서 원격의료의 급속한 수용과 보급으로 인해 조사 기간 동안 부문 성장에 기여할 것으로 예상되며, 북미가 시장에서 큰 비중을 차지할 것으로 예상됩니다. 또한, 다양한 솔루션을 제공하고 신흥국 시장의 의료 인프라를 활용할 수 있는 기존 기업의 존재감이 강하다는 점도 이 지역 전체 시장 성장을 촉진할 것으로 예상됩니다. 예를 들어, JMIR Dermatology가 2023년 8월에 발표한 조사에 따르면, 원격 피부과 진료는 의사의 지리적 분포가 부족한 다른 지역에 비해 북미에서 가장 널리 받아들여지고 있으며, 유럽이 그 뒤를 잇고 있는 것으로 나타났습니다. 여러 조사에 따르면 지난 2년 동안 이 지역 전체에서 원격 피부과 이용자들의 만족도가 높은 것으로 나타났습니다.

또한, 피부 질환에 대한 인식과 접근성을 높이기 위해 정부 및 비정부기구의 자금 지원이 증가하고 있는 것도 시장을 견인하고 있습니다. 예를 들어, 2023년 12월, Skin Investigation Network of Canada는 캐나다 보건연구기관(Canadian Institutes of Health Research)으로부터 5년간 200만 달러를 지원받아 국내의 광범위한 피부질환의 원인, 임상적 측면, 의료 시스템, 집단 위생에 관한 문제를 다루고 있습니다. 따라서 이러한 노력은 원격 피부과 채택을 증가시키고 시장 성장에 기여하고 있습니다.

또한, 이 시장의 주요 기업들이 지리적 입지를 확대하는 데 주력하고 있으며, 그 결과 이 시장에 많은 성장 기회가 창출되어 이 지역의 시장 성장에 영향을 미칠 것으로 예상됩니다. 예를 들어, 2023년 4월 원격 피부과 분야 선도기업인 MedX Health는 PharmaChoice Canada와 캐나다 전역에 MedX 원격 피부과 스크리닝 플랫폼을 출시하기로 합의했습니다. 이러한 주요 기업들의 전략적 이니셔티브는 시장 성장에 기여할 것입니다. 따라서 다양한 피부과 질환의 진단 및 치료를 위한 원격의료 플랫폼의 수용과 보급이 증가함에 따라 북미 지역 시장도 성장할 것으로 예상됩니다.

원격 피부과 시장은 세계 및 지역적으로 사업을 전개하는 여러 기업이 존재하기 때문에 시장이 세분화되어 있습니다. 경쟁사로는 Miiskin, Teladoc Health Inc, MDLIVE, DermatologistOnCall, First Derm, 3Derm, MetaOptima Technology Inc, Cureskin, Practo, MFine Pvt Ltd, American Well, Doctor On Demand 등 시장 점유율이 높고 인지도가 높은 국제 및 현지 기업들에 대한 분석이 포함됩니다.

The Teledermatology Market size is estimated at USD 13.77 billion in 2024, and is expected to reach USD 32.04 billion by 2029, growing at a CAGR of 18.40% during the forecast period (2024-2029).

Teledermatology is a subfield of telemedicine that uses telecommunication technology to provide dermatology care remotely. It enables the exchange of images and medical information through secure platforms for evaluation and diagnosis and remotely offers treatment to patients with skin problems. The demand for teledermatology is increasing with the rise of the digital age and improving access to dermatological care, particularly in remote and underserved areas. The lack of dermatologists and the increasing incidence of skin conditions such as psoriasis, eczema, and acne are surging the demand for teledermatology. For instance, according to an article published by the British Skin Foundation in November 2023, currently, there are around 2,000 different dermatological conditions, and teledermatology can address around 90% of them, including skin cancer. Moreover, the convenience, accessibility, and cost-effectiveness of teledermatology offered to patients and healthcare providers are significant factors influencing market growth.

Furthermore, the lack of dermatologists and limited access to dermatology care in low- and middle-income countries due to geographical barriers, long waiting times, and mobility issues are surging the adoption rate of teledermatology, subsequently fueling the market growth. For instance, in a study published by the Indian Journal of Dermatology, Venereology, and Leprology in December 2023, there was less than one dermatologist per million population in sub-Saharan Africa in 2022. In contrast, there were 34 dermatologists per million population in the United States in 2022. Hence, teledermatology is a powerful educational and clinical support tool for diagnosing and managing skin diseases in countries lacking dermatologists. Implementing this technology to improve access to dermatology care will drive market growth over the coming years.

In addition, technological advancements introduced by market players in the teledermatology systems to provide more accurate diagnosis and treatment recommendations, coupled with more advanced imaging and data analysis capabilities, are expected to fuel the market growth. For instance, in September 2022, MCI Onehealth Technologies Inc., a healthcare technology company, and Oro Health, an artificial intelligence solution provider, collaboratively developed and launched the MCI Dermatology Connect platform. The platform provides specific solutions for virtual dermatology care, including secure transfer of high-resolution imaging between patient and specialist. The comfort and benefits that teledermatology offers over long wait times for in-person visits are anticipated to drive the demand for teledermatology between 2024 and 2029.

However, privacy and security concerns, lack of adherence to the regulatory framework, and lack of reimbursement facilities in emerging countries are expected to restrain the market growth from 2024 to 2029.

Teledermatology offers various services, such as teleconsultation, telemonitoring, and tele-education. It provides numerous benefits such as convenience, access to specialized care, reduced healthcare costs, improved health outcomes, and increased patient engagement. These benefits are surging the adoption of teledermatology services over traditional in-person visits to cater to the increasing demand for dermatology care, which favors segment growth between 2024 and 2029. For instance, according to a report published by News-Medical.Net in October 2023, Consultant Connect's PhotoSAF technology is one of the United Kingdom's most widely used teledermatology platforms, covering over half of the NHS across England, Scotland, and Wales. After the launch of the Consultant Connect platform, its usage increased by 2,400% in 2023 compared to the previous four years. Hence, such instances support the idea that teledermatology services enhance patient experience and improve health outcomes, allowing them to drive segmental growth from 2024 to 2029.

Moreover, telemedicine has emerged as an essential tool in cases where diagnoses and treatment are straightforward, such as acne, hair disorders, and dermatitis. For instance, according to a study published by the Telemedicine and e-health Journal in October 2023, the most frequent reason for patients using teledermatology in Germany was high waiting time to avail dermatology care in the outpatient department. Furthermore, as per the same source, 62.0% of the enrolled patients rated the treatment success as good or very good, whereas 86.1% rated the quality of telemedical care as equivalent or better to that of an outpatient visit. Additionally, the study published by the Life Journal in April 2023 stated that the accuracy of atopic dermatitis diagnosis through telemedicine service was 84.4%. Such studies highlighted that as more patients and healthcare providers become familiar with telemedicine, it is likely that teledermatology services will continue to expand in the upcoming years.

Additionally, active investments made by market players to increase awareness about skin diseases and outreach to dermatology care are contributing to segmental growth. For instance, in March 2024, the Health Science Department of Dermatology of George Washington University School of Medicine received a USD 500,000 sponsorship from Johnson & Johnson Innovative Medicine for its free teledermatology program, EACH one TEACH one. The programs aim to enhance access to dermatology care across the country. Such initiatives increase the accessibility and affordability of dermatological care, driving the demand for teledermatology and contributing to segment growth from 2024 to 2029.

North America is expected to have a significant share in the market owing to factors such as the increasing burden of skin disease, with rapid acceptance and penetration of telehealth by healthcare facilities contributing to the segment growth over the study period. In addition, a strong presence of established players offering a wide range of solutions and access to developed healthcare infrastructure is anticipated to drive market growth across the region. For instance, according to a study published by JMIR Dermatology in August 2023, teledermatology was widely accepted in North America, followed by Europe, compared to other regions with poor geographical distributions of doctors, which appear to be underrepresented. Several studies reveal high levels of user satisfaction in teledermatology over the last two years across this region.

Furthermore, the market is driven by increased funding from government and non-government organizations to raise awareness and accessibility related to skin diseases. For instance, in December 2023, the Skin Investigation Network of Canada received USD 2 million from the Canadian Institutes of Health Research over five years to tackle the causes, clinical aspects, health systems, and population health questions for a broad range of skin conditions across the country. Hence, these initiatives increase the adoption of teledermatology, thus contributing to market growth.

Additionally, several prominent players in the market are focused on expanding their geographical presence, which in turn is projected to create numerous growth opportunities for the market, thereby influencing market growth in the region. For instance, in April 2023, MedX Health, a key player in teledermatology, agreed with PharmaChoice Canada to launch the MedX teledermatology screening platform across Canada. Such strategic initiatives by key players contribute to market growth. Therefore, the studied market is anticipated to grow in North America due to the growing acceptance and penetration of telehealth platforms for diagnosing and treating a wide range of dermatological conditions.

The teledermatology market is fragmented due to the presence of several companies operating globally and regionally. The competitive landscape includes an analysis of a few international and local companies that hold significant market share and are well known, including Miiskin, Teladoc Health Inc., MDLIVE, DermatologistOnCall, First Derm, 3Derm, MetaOptima Technology Inc., Cureskin, Practo, MFine Pvt Ltd, American Well, and Doctor On Demand.