ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

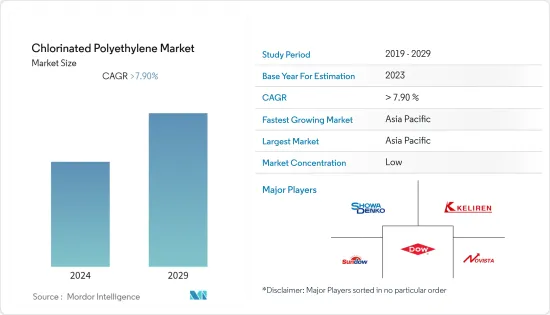

염소화 폴리에틸렌(Chlorinated Polyethylene) 시장 규모는 2024년에 577.28킬로톤으로 추정 되며, 2029년에는 815.35킬로톤에 이를 것으로 예측되며, 예측 기간 중(2024-2029년)의 CAGR은 7% 이상으로 성장할 것으로 예측됩니다.

염소화 폴리에틸렌 시장은 COVID-19 팬데믹시 수급면에서 몇 가지 장애와 중단을 목격했습니다. 물류와 공급망 문제에 정부 규제가 더해졌기 때문에 염소화 폴리에틸렌 공급업체는 생산 원료의 조달과 노동 문제로 문제에 직면했습니다. 그러나 세계 유행의 회복과 함께 백신 접종 증가와 정부 전략으로 시장 활동이 회복되기 시작하면 염소화 폴리에틸렌 시장은 이전 시장 상태로 돌아가기 시작했습니다.

고성능 폴리에틸렌 제품에 대한 수요 증가는 염소화 폴리에틸렌 시장 성장을 이끌 것으로 예상됩니다.

원유와 같은 원재료 가격 변동과 다양한 국가의 폴리에틸렌 사용에 대한 엄격한 규제 부설은 예측 기간 동안 시장 성장을 방해할 것으로 예상됩니다.

그럼에도 불구하고, 염소화 폴리에틸렌의 고도로 지속가능한 등급의 개발과 관련된 R&D는 시장에 유리한 기회를 제공할 것으로 예상됩니다.

아시아 태평양이 가장 높은 시장 점유율을 차지하고 있으며 예측 기간 동안에도 시장을 독점 할 가능성이 높습니다.

염소화 폴리에틸렌 시장 동향

충격 개량제가 시장을 독점

염소화 폴리에틸렌의 폭넓은 용도와 함께 세계의 건설·재건 활동이 증가하고 있기 때문에 염소화 폴리에틸렌 시장에서는 충격 개량제가 주요 용도 분야가 되고 있습니다.

PVC 사이딩, 파이프, 창문 프로파일, 문, 울타리에 대한 엄청난 수요는 건축 및 건설 업계에서 특히이 시장에서 충격 개량제의 성장을 이끌고 있습니다.

CPE 135A는 뛰어난 연성으로 인해 특수 폴리 염화 비닐 전선 튜브 및 고 충전 컴파운드에서 사용이 증가하고 있습니다. CPE 135A 세계 시장 개척은 충격 개량제 응용 분야에서 CPE 135A 카테고리의 사용 증가로 인한 것입니다.

이 내충격성 개질제는 포장 용도에서 접이식 백색성과 투명성의 이상적인 균형을 제공하는 능력으로 포장 용도에 널리 사용됩니다. 다양한 최종 용도 기업에서 플라스틱 포장 사용량의 급속한 증가가 충격 개량제 수요를 촉진할 것으로 예상됩니다. 예를 들어, 경제협력개발기구(OECD)에 따르면 세계의 포장용 플라스틱 사용량은 2029년까지 2022년 대비 20.1%까지 성장할 가능성이 있습니다.

경량화와 비용 절감의 요구로 인해 세계 산업에서 플라스틱의 사용이 증가하고 있는 것도 충격 개량제, 나아가서는 염소화 폴리에틸렌 수요를 촉진할 것으로 예상됩니다. 예를 들어, Our World in Data에 따르면 세계 플라스틱 생산량은 2022년 4억 7,539만 톤에 비해 2029년 5억 7,342만톤 가까이에 이를 것으로 예상됩니다.

위와 같은 모든 요인과 시장 성장 촉진요인은 예측 기간 동안 시장에서 충격 개량제 용도 부문의 우위를 높일 것으로 예상됩니다.

시장을 독점하는 아시아 태평양

건설 산업은 염소화 폴리에틸렌의 가장 큰 최종 사용자 산업입니다. 염소화 폴리에틸렌은 건설 및 건축자재에 널리 사용되며, 예를 들어 단열재, 방수막, 파이프 씰, 바닥재 등에 사용되며 내후성, 내약품성, 내열성을 제공합니다.

아시아 태평양은 세계에서 가장 바쁜 대규모 건축 및 건설 산업이 있기 때문에 염소화 폴리에틸렌 시장을 주로 지배하고 있습니다. 예를 들어 Seasia.co에 따르면 아시아 태평양에는 7,500개가 넘는 초고층 빌딩이 있으며, 이는 세계의 초고층 빌딩 총수의 80% 이상에 해당합니다.

중국, 인도, 일본, 인도네시아, 한국 등 국가들이 이 지역의 건축 및 건설 업계의 규모를 지지하고 있습니다.

또한 유엔무역개발회의(UNCTAD)에 따르면 아시아 태평양은 도시 인구가 가장 증가할 것으로 예측되고 있으며, 2022년에 비해 2050년까지 도시에 거주하는 인구가 10억 3,300만 명 증가할 것으로 예상 예상됩니다. 이 때문에 이 지역에서는 모든 유형의 건물 및 인프라의 건설량이 증가할 것으로 보입니다. 따라서 염소화 폴리에틸렌 시장에서 아시아 태평양의 이점은 예측 기간 동안에도 유지될 것으로 보입니다.

염소화 폴리에틸렌은 자동차 씰, 도어 트림, 보호 커버 등에 널리 사용되어 자동차 산업에서도 널리 사용되고 있습니다. 또한 아시아 태평양은 세계적으로 자동차 생산이 활발합니다.

따라서 위의 동향과 데이터로부터 아시아 태평양은 예측 기간 동안 염소화 폴리에틸렌 시장을 독점할 것으로 예측됩니다.

염소화 폴리에틸렌 산업 개요

세계의 염소화 폴리에틸렌 시장은 큰 시장 점유율이 없는 많은 플레이어들이 존재하기 때문에 본질적으로 단편화됩니다. 시장의 주요 기업으로는 SHOWA DENKO KK, Hangzhou Keli Chemical, Shandong Novista Chemical Ltd., Dow, Sundow Polymers 등이 있습니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 전제 조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

고성능 폴리에틸렌 제품에 대한 수요 증가

억제요인

원료 가격의 변동

폴리에틸렌의 사용에 관한 엄격한 규제

업계 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화 : 시장 규모(수량 기준)

제품

CPE 135A

CPE 135B

기타 제품

용도

충격 개량제

전선 및 케이블 피복

호스·튜브

접착제

적외선 흡수

기타 용도

지역

아시아 태평양

중국

인도

일본

한국

기타 아시아 태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

시장 점유율/랭킹 분석

주요 기업의 전략

기업 프로파일

Dow

Dycon Chemicals

Hangzhou Keli Chemical Co., Ltd.

Jiangsu Tianteng Chemical Industry Co., Ltd.

Aurora Plastics LLC

Shandong Gaoxin Chemical Co., Ltd.

Shandong Novista Chemicals Co.,Ltd(Novista Group)

Shandong Xiangsheng New Materials Technology Co.,Ltd.

Shandong Xuye New Materials Co., Ltd.

Resonac Holdings Corporation

Sundow Polymers Co., Ltd.

Weifang Yaxing Chemical Co., Ltd.

제7장 시장 기회 및 향후 동향

고급 등급 개발을 전제로 한 연구 개발

LYJ

영문 목차

영문목차

The Chlorinated Polyethylene Market size is estimated at 577.28 kilotons in 2024, and is expected to reach 815.35 kilotons by 2029, growing at a CAGR of greater than 7% during the forecast period (2024-2029).

The chlorinated polyethylene market witnessed several hurdles and interruptions in terms of supply and demand during the COVID-19 pandemic. Owing to the logistical and supply chain issues combined with government restrictions, chlorinated polyethylene suppliers faced challenges in procuring raw materials for production, as well as labor issues. However, as the market activities started to restore with the worldwide recovery from the pandemic because of an increase in vaccinations combined with government strategies, the chlorinated polyethylene market started to get back to the previous market states.

The increasing demand for high-performance polyethylene products is projected to drive the growth of the chlorinated polyethylene market.

Fluctuations in raw materials prices like crude oil and the laying down of strict regulations regarding the use of polyethylene from various countries are expected to hinder the market's growth during the forecast period.

Nevertheless, research and development pertaining to the development of advanced and sustainable grades of chlorinated polyethylene are expected to offer lucrative opportunities to the market.

Asia-Pacific accounted for the highest market share and is also likely to dominate the market during the forecast period.

Chlorinated Polyethylene Market Trends

Impact Modifier to Dominate the Market

Impact modifier stands to be the dominating application segment for the chlorinated polyethylene market owing to increasing global construction and reconstruction activities, coupled with the wide applicability of chlorinated polyethylene.

Huge demand for PVC siding, pipes, window profiles, doors, and fences is driving the growth of impact modifiers in this market, among others from the building & construction industry.

The growing use of CPE 135A in specialty polyvinyl chloride electrical conduits and highly filled compounds is witnessed owing to its superior ductility. Development in the global market segment of CPE 135A is majorly due to the increased use of the CPE 135A category in the application of impact modifiers.

The impact modifier is widely used in packaging applications owing to its ability to offer an ideal balance between crease-whitening resistance and clarity for packaging applications. A fast increment in the use of plastic packaging in different end-use enterprises is expected to drive the demand for impact modifiers. For instance, according to the Organisation for Economic Co-operation and Development (OECD), the global plastic use for packaging can grow up to 20.1% in volume by 2029 compared to 2022.

The growing incorporation of plastics across industries worldwide due to the requirement of improved weight and cost reductions is also expected to propel the demand for impact modifiers and, thus, ultimately, chlorinated polyethylene. For instance, according to Our World in Data, the global plastics production volume is expected to reach nearly 573.42 million tons in 2029 compared to 475.39 million tons in 2022.

All the factors above and drivers are expected to increase the impact modifier application segment's dominance in the market during the forecast period.

Asia-Pacific Region to Dominate the Market

Building and construction is the largest end-user industry for chlorinated polyethylene. Chlorinated polyethylene is extensively used in construction and building materials, such as thermal insulation materials, waterproofing membranes, pipe seals, flooring materials, etc., to provide them with weather resistance, chemical resistance, and heat resistance.

The Asia-Pacific region majorly dominates the chlorinated polyethylene market, as it has the world's busiest and largest building and construction industry. For instance, according to Seasia.co, Asia-Pacific has over 7,500 skyscrapers, which is more than 80% of the world's total number of skyscrapers.

Countries such as China, India, Japan, Indonesia, and South Korea, among others, are responsible for the large size of the region's building and construction industry.

Moreover, according to the United Nations Conference on Trade and Development (UNCTAD), the Asia-Pacific is projected to witness the highest growth in urban population, with an increase of 1,033 million more people residing in urban areas by 2050 compared to 2022. This will likely increase the construction volume of all kinds of buildings and infrastructure in the region. Hence, the dominance of the Asia-Pacific region over the chlorinated polyethylene market will be sustained during the forecast period.

Chlorinated polyethylene is also extensively used in the automotive industry due to its vast applications in automotive seals, door trims, protective covers, etc. Moreover, Asia-Pacific is the leading producer of automotives globally.

Hence, owing to the trends mentioned above and the data, the Asia-Pacific region is projected to dominate the chlorinated polyethylene market during the forecast period.

Chlorinated Polyethylene Industry Overview

The global chlorinated polyethylene market is fragmented in nature owing to the presence of numerous players with no significant market share. Some of the major players in the market (not in any particular order) include SHOWA DENKO K.K., Hangzhou Keli Chemical Co., Ltd., Shandong Novista Chemical Ltd., Dow, and Sundow Polymers Co., Ltd., amongst others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Growing Demand for High Performance Polyethylene Products

4.2 Restraints

4.2.1 Fluctuating Raw Material Prices

4.2.2 Strict Regulations Regarding the Use of Polyethylene

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

5.1 Product

5.1.1 CPE 135A

5.1.2 CPE 135B

5.1.3 Other Products

5.2 Application

5.2.1 Impact Modifier

5.2.2 Wire and Cable Jacketing

5.2.3 Hose and Tubing

5.2.4 Adhesives

5.2.5 Infrared Absorption

5.2.6 Other Applications

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 France

5.3.3.4 Italy

5.3.3.5 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle-East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share/Ranking Analysis**

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Dow

6.4.2 Dycon Chemicals

6.4.3 Hangzhou Keli Chemical Co., Ltd.

6.4.4 Jiangsu Tianteng Chemical Industry Co., Ltd.