배터리 원재료 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)

Battery Raw Material - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

상품코드:1519945

리서치사:Mordor Intelligence

발행일:2024년 07월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

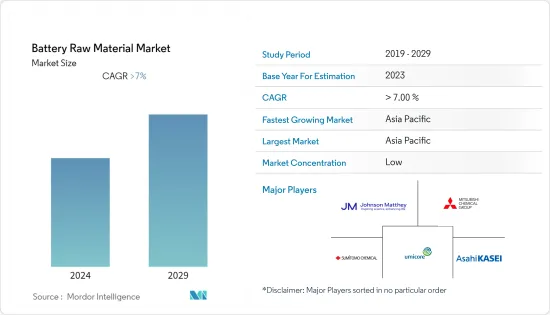

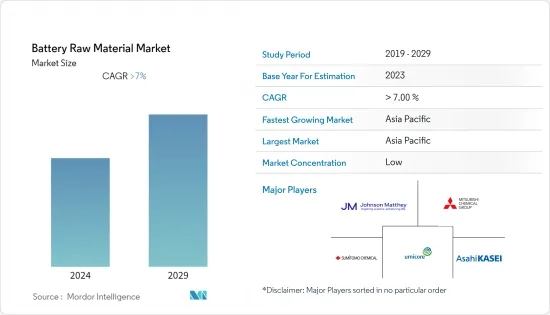

배터리 원재료 시장 규모는 2024년 587억 달러로 추정되고, 2029년 972억 3,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2024-2029년) CAGR은 10.62%로 성장할 전망입니다.

COVID-19 팬데믹은 배터리 원재료 시장을 혼란시켰습니다. 봉쇄 조치, 공장 폐쇄 및 이동 제한으로 인해 채광 작업, 광석 가공 시설 및 물류 네트워크가 혼란스럽고 원료 공급에 영향을 미쳤습니다. 자동차, 일렉트로닉스, 에너지 등 각 산업의 경제 활동의 재개가 배터리 원재료 시장의 회복에 기여했습니다.

주요 하이라이트

배터리 원재료 시장은 자동차 및 가전 분야에서의 사용 증가로 급속히 확대되고 있습니다.

그러나 배터리 원재료 시장의 성장은 배터리의 보관 및 운송에 대한 엄격한 안전 규정에 의해 저해될 것으로 예상됩니다.

바나듐 흐름 기술의 연구개발 활동 증가와 휴대용 전자기기 및 소비자용 기기 수요 증가는 앞으로 수년간 배터리 원재료 시장에 기회를 가져올 것으로 예상됩니다.

중국이나 인도 등 국가에서 자동차용 배터리와 가전용 배터리의 소비가 성장하고 있는 것이 아시아태평양이 세계 시장을 지배하는 요인이 되고 있습니다.

배터리 원재료 시장 동향

시장을 독점하는 자동차 부문

전기자동차의 급속한 보급에 따라 자동차 산업은 큰 변화를 맞이하고 있습니다. 중요한 에너지 저장인 리튬 이온 배터리에는 다양한 중요한 원료가 필요합니다. EV의 판매가 세계적으로 급증하고 있는 가운데, 이러한 배터리 원재료 수요가 급증하고, 배터리 원재료 시장의 자동차 분야의 성장을 견인하고 있습니다.

국제자동차공업회(OICA)가 발표한 추계에 의하면 2022년에는 세계 약 8,163만대의 자동차가 판매됩니다.

또한 연방 자동차 교통국(프렌스부르크)에 따르면 독일의 배터리 전기자동차 총 등록 대수는 2020년 136,617대에서 2023년 1,013,009대로 증가했습니다.

가전 및 자동차 분야에서는 중국, 일본, 한국, 인도 등 아시아태평양 국가들이 배터리 원재료의 사용량을 크게 늘리고 있으며, 예측 기간 중 시장의 견인역이 될 것으로 예상됩니다.

세계 EV 충전 인프라의 확대는 EV에 대한 소비자의 신뢰를 높이고 전기자동차의 보급에 박차를 가하고 있습니다. 정부, 전력 회사, 비공개 회사는 충전소, 급속 충전 네트워크, 스마트 그리드 기술 도입에 많은 투자를 하고 있습니다. 따라서 EV의 보유 대수 증가를 지원하고 있습니다. 이러한 인프라 정비는 차량용 리튬 이온 배터리 수요 증가에 대응하기 위해 배터리 원재료의 견조한 시장을 창출하고 있습니다.

연방 네트워크청이 발표한 데이터에 따르면 독일에는 2023년 10월 시점에서 EV용 평균 속도 충전이 가능한 공공 사이트가 8만 7,155개, 공공 급속 충전소이 2만 1,111개 있습니다.

전기차의 보급 확대는 청정 에너지 정책과 일치합니다. 중국 정부는 수요에 대한 공급 격차를 줄이기 위해 자동차 제조업체가 중국으로의 자동차 수입 규제를 완화하려는 의향입니다.

예측 기간 동안 배터리 원재료 시장은 위의 모든 요인에 의해 견인될 것으로 예상됩니다.

아시아태평양이 시장을 독점

아시아태평양은 자동차에서 전자, 신재생 에너지에 이르기까지 다양한 분야의 중요한 제조 기지입니다. 이 지역에는 수많은 배터리 제조업체, 배터리 셀 제조업체 및 배터리 원재료 공급업체가 있습니다. 이와 같이 제조시설이 집중되어 있는 것이 아시아태평양에서의 전지원료 수요를 견인하고 있습니다.

아시아태평양의 전기자동차 시장은 중국, 일본, 한국 등 국가에서 빠르게 성장하고 있습니다. 이들 국가는 세계 최대의 전기자동차 생산국이자 소비국이기도 합니다. 전기자동차용 리튬 이온 전지의 생산에는 리튬, 코발트, 니켈, 흑연 등의 배터리 원재료가 대량으로 필요하고, 이것이 배터리 원재료 시장에서의 아시아태평양의 우위성으로 이어지고 있습니다.

중국 기차공업협회(CAAM)가 발표한 데이터에 따르면 중국에서는 2022년에 약 540만대의 배터리 전기차가 판매되어 2021년 대비 83.5% 증가했습니다. 같은 해 중국에서 플러그인 하이브리드 자동차의 판매 대수는 전년 대비 151.91% 증가한 150만대 이상이 되었습니다.

일본의 자동차 검사 등록 정보 협회(AIRIA)가 발표한 데이터에 따르면, 2023년 일본에서 사용되는 전기 승용차의 대수는 약 16만 2,390대가 되어 10년 전보다 증가했습니다.

인도에서는 Vahan의 데이터에 따르면 2023년 3월의 EV 판매 대수는 139,789대로 2022년 3월의 77,128대에 비해 전년 동월 대비 82% 증가했습니다. 합계하면 2022년도의 4,58,746대에서 11,80,597대로 157%의 경이적인 성장을 보였습니다.

그러므로, 예측 기간 동안 이 지역의 배터리 원재료에 대한 수요는 이러한 모든 시장 개척에 의해 견인될 것으로 예상됩니다.

배터리 원재료 산업 개요

배터리 원재료 시장은 단편화되어 있으며 소수의 대기업과 수많은 소규모 기업이 있습니다. 주요 기업(순부동)에는 Umicore, Asahi Kasei Corporation, Johnson Matthey, Sumitomo Chemical, Mitsubishi Chemical Corporation 등이 있습니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

소비자 일렉트로닉스로부터 수요 증가

자동차 산업에서의 용도 증가

억제요인

전지의 보관 및 수송에 관한 엄격한 안전 규제

기타 억제요인

밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁도

제5장 시장 세분화(금액 베이스 시장 규모)

전지 유형별

납축전지

리튬 이온

기타 전지 유형(니켈 수소 전지, 고체 전지)

원료별

양극

음극

전해액

세퍼레이터

용도별

가전

자동차

산업용

통신용

기타(신재생 에너지 저장)

지역별

아시아태평양

중국

인도

일본

한국

태국

말레이시아

인도네시아

베트남

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

스페인

터키

러시아

노르딕

기타 유럽

세계 기타 지역

남미

중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴 및 협정

시장 점유율(%)** 및 랭킹 분석

주요 기업의 전략

기업 프로파일

Asahi Kasei Corporation

BASF SE

Celgard LLC

ENTEK

ITOCHU Corporation

Johnson Matthey

Mitsubishi Chemical Corporation.

NICHIA CORPORATION

Sumitomo Chemical Co. Ltd

Targray Technology International Inc.

Umicore

제7장 시장 기회 및 향후 동향

전지에 있어서의 바나듐 플로우 기술의 연구 개발

휴대용 전자기기 및 소비자용 기기 수요 증가

AJY

영문 목차

영문목차

The Battery Raw Material Market size is estimated at USD 58.70 billion in 2024, and is expected to reach USD 97.23 billion by 2029, growing at a CAGR of 10.62% during the forecast period (2024-2029).

The COVID-19 pandemic disrupted the battery materials market. Lockdown measures, factory closures, and restrictions on movement led to disruptions in mining operations, ore processing facilities, and logistics networks, impacting the supply of raw materials. The resumption of economic activities across industries, including automotive, electronics, and energy, contributed to the recovery of the battery raw materials market.

Key Highlights

The market for battery raw materials is proliferating due to the increasing use of these products in the automotive and consumer electronics sectors.

However, the growth of the battery raw materials market is expected to be hampered by strict safety regulations for batteries through storage and transport.

The rising research and development activities in vanadium flow technology and increasing demand for portable electronics and consumer devices are expected to provide opportunities for the battery raw material market in the coming years.

The growing consumption of automotive and consumer electronics batteries in countries such as China and India is driving Asia-Pacific to dominate the global market.

Battery Raw Material Market Trends

Automotive Segment to Dominate the Market

With the rapid rise in the adoption of electric vehicles, the car industry is undergoing a significant change. Various critical raw materials are required for the Lithium-ion battery, which is a crucial energy storage. As EV sales continue to surge globally, the demand for these battery raw materials has skyrocketed, driving growth in the automotive segment of the battery raw materials market.

According to the estimate released by the International Organization of Motor Vehicle Manufacturers (OICA), around 81.63 million vehicles were sold around the world in 2022.

Furthermore, according to the Federal Motor Transport Authority, Flensburg, the registration of the total number of battery electric cars in Germany increased from 136,617 units in 2020 to 1,013,009 units in 2023.

In the consumer electronics and automotive sectors, Asia-Pacific countries such as China, Japan, South Korea, and India are experiencing strong growth in the use of battery raw materials, which is expected to drive the market over the forecast period.

The expansion of EV charging infrastructure worldwide has bolstered consumer confidence in EVs and fueled the adoption of electric vehicles. Governments, utilities, and private companies are investing heavily in the deployment of charging stations, fast-charging networks, and smart grid technologies. Thus, this supports the growing fleet of EVs. This infrastructure development has created a robust market for battery raw materials to meet the increasing demand for lithium-ion batteries in automotive applications.

According to the data published by the Federal Network Agency, in Germany, there were 87,155 public sites with average speed recharging for EVs available in October 2023 and 21,111 public quick charge stations.

The increase in the adoption of electric vehicles aligns with the clean energy policy. The Chinese government intends to relax restrictions on the import of vehicles by automobile manufacturers into China in order to narrow the supply gap for demand.

The market for battery materials is expected to be driven by all of the above factors during the forecast period.

Asia-Pacific to Dominate the Market

Asia-Pacific is an important manufacturing hub for a wide range of sectors, from automotive to electronics and renewables. The region hosts a large number of battery manufacturers, cell producers, and suppliers of battery raw materials. This concentration of manufacturing facilities drives demand for battery raw materials in Asia-Pacific.

The Asia-Pacific market for electric vehicles is growing at a rapid rate in countries such as China, Japan, and South Korea. These countries are the biggest producers and consumers of electric vehicles in the world. The production of lithium-ion batteries for EVs requires significant quantities of battery raw materials such as lithium, cobalt, nickel, and graphite, contributing to the dominance of Asia-Pacific in the battery raw materials market.

According to the data published by the China Association of Automobile Manufacturers (CAAM), in China, approximately 5.4 million battery electric vehicles were sold in 2022, an increase of 83,5 % compared to 2021. In the same year, there was an increase of 151.91% in sales of plugin hybrids to over 1.5 million vehicles in China from a year earlier.

According to the data published by the Automobile Inspection & Registration Information Association, Japan (AIRIA), in 2023, the number of electric passenger cars in use in Japan increased to about 162.39 thousand vehicles, which was an increase from 10 years ago.

In India, according to Vahan's data, EV sales in March 2023 increased by 82 % Y-o-Y, with 1,39,789 units sold compared to 77,128 EVs sold in March 2022. In total, sales increased by a staggering 157% in the period, from 4,58,746 to 11,80,597 during fiscal year 2022.

Therefore, the demand for battery raw materials in the region during the forecast period is expected to be driven by all these market developments.

Battery Raw Material Industry Overview

The battery raw material market is fragmented, with the presence of a few large-sized players and a large number of small players operating. The major players (not in any particular order) include Umicore, Asahi Kasei Corporation, Johnson Matthey, Sumitomo Chemical Co. Ltd, and Mitsubishi Chemical Corporation.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Growing Demand from Consumer Electronics

4.1.2 Rising Application in Automotive Industry

4.2 Restraints

4.2.1 Stringent Safety Regulations for Batteries through Storage and Transportation

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

5.1 By Battery Type

5.1.1 Lead-acid

5.1.2 Lithium-ion

5.1.3 Other Battery Types (Nickel-metal Hydride (NiMH), and Solid-state Batteries)

5.2 By Material

5.2.1 Cathode

5.2.2 Anode

5.2.3 Electrolyte

5.2.4 Separator

5.3 By Application

5.3.1 Consumer Electronics

5.3.2 Automotive

5.3.3 Industrial

5.3.4 Telecommunication

5.3.5 Other Applications (Renewable Energy Storage)

5.4 By Geography

5.4.1 Asia-Pacific

5.4.1.1 China

5.4.1.2 India

5.4.1.3 Japan

5.4.1.4 South Korea

5.4.1.5 Thailand

5.4.1.6 Malaysia

5.4.1.7 Indonesia

5.4.1.8 Vietnam

5.4.1.9 Rest of Asia-Pacific

5.4.2 North America

5.4.2.1 United States

5.4.2.2 Canada

5.4.2.3 Mexico

5.4.3 Europe

5.4.3.1 Germany

5.4.3.2 United Kingdom

5.4.3.3 France

5.4.3.4 Italy

5.4.3.5 Spain

5.4.3.6 Turkey

5.4.3.7 Russia

5.4.3.8 NORDIC

5.4.3.9 Rest of Europe

5.4.4 Rest of the World

5.4.4.1 South America

5.4.4.2 Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%) **/ Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Asahi Kasei Corporation

6.4.2 BASF SE

6.4.3 Celgard LLC

6.4.4 ENTEK

6.4.5 ITOCHU Corporation

6.4.6 Johnson Matthey

6.4.7 Mitsubishi Chemical Corporation.

6.4.8 NICHIA CORPORATION

6.4.9 Sumitomo Chemical Co. Ltd

6.4.10 Targray Technology International Inc.

6.4.11 Umicore

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Research and Development in Vanadium Flow Technology in Batteries

7.2 Increasing Demand for Portable Electronics and Consumer Devices