ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

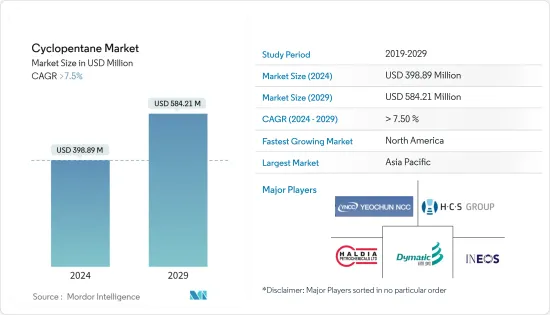

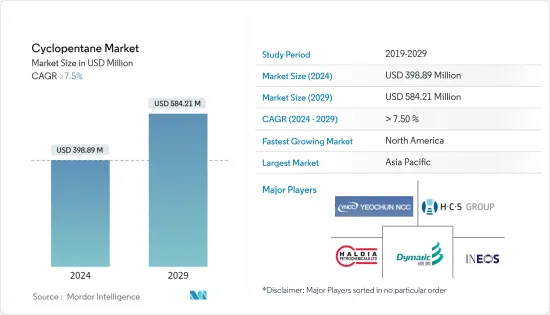

사이클로펜테인 시장 규모는 2024년 3억 9,889만 달러로 추정되고, 2029년 5억 8,421만 달러에 이를 것으로 예측되며, 예측 기간 중(2024-2029년) CAGR은 7.5% 이상으로 성장할 전망입니다.

COVID-19의 대유행은 사이클로펜테인 시장에 방해가 되었습니다. 여러 국가에서 전국적인 봉쇄, 엄격한 사회적 격리 조치, 세계 공급망 네트워크의 혼란으로 인해 냉매 산업은 생산 공장과 산업의 대부분이 폐쇄되어 심각한 타격을 입었습니다. 그러나 규제가 해제된 후 시장은 큰 성장률을 기록했습니다. 시장이 성장률을 기록한 이유는 냉동, 단열, 화학용제 등 다양한 용도로 사이클로펜테인의 사용량이 증가하고 있기 때문입니다.

주요 하이라이트

폴리우레탄 제조에 있어서 발포제 용도로의 사이클로펜테인 수요 증가와 냉동 용도에서의 사용량 증가가 사이클로펜테인 시장을 견인할 것으로 예상됩니다.

반면에, 더 나은 대체 제품의 가용성과 사이클로펜테인과 관련된 건강 관련 문제가 시장 성장을 방해할 것으로 예상됩니다.

건축 및 자동차 응용 분야에서 발포제 사용 증가는 예측 기간 동안 시장에 기회를 가져올 것으로 예상됩니다.

아시아태평양은 냉동, 단열, 화학 용제 분야에서 사이클로펜테인 수요가 증가함에 따라 시장을 독점할 것으로 예상됩니다.

사이클로펜탄 시장 동향

시장을 독점하는 냉동 응용 분야

사이클로펜테인은 알루미나의 존재 하에서 고온 고압에서 시클로헥산을 분해하여 생성됩니다. 사이클로펜테인은 주로 폴리우레탄의 제조에 있어서의 발포제로서 사용되고, 또한 냉장고나 냉동고 등의 제조에도 사용됩니다.

냉장고에 대한 수요는 식음료 분야에서 증가하고 있습니다. 식품을 안정된 온도에서 보존하는 수요 증가가 식품 분야에서 냉장고 및 냉동고 수요를 뒷받침하고 있습니다.

또한 제약 분야에서는 병원, 약국, 진료소, 진단센터에서 혈액과 혈액 유래 물질, 온도에 민감한 의약품을 안전하게 보관하는 수요 증가가 헬스케어 및 제약 업계에서의 냉동기 수요를 촉진하고 있습니다.

유럽에서는 냉장고 제조업체가 CFC(클로로플루오로카본) 및 HCFC(하이드로클로로플루오로카본) 대신 폴리우레탄 폼 단열재의 발포제로 사이클로펜테인을 사용합니다. HCFC 화합물의 사용에 대한 엄격한 규제로 인해 냉동 적용 시 사이클로펜탄의 사용이 증가하고 있습니다.

마찬가지로 아시아태평양, 중동, 아프리카, 라틴아메리카에서는 각국 정부가 냉장고 용도에서 HCFC(하이드로클로로플루오로카본)의 사용을 단계적으로 폐지하기 위한 다양한 정책을 도입하고 있습니다. 사이클로펜테인 수요는 이 지역의 인구 증가, 주택용 냉장고 및 건축 용도 수요 증가로 인한 것입니다.

2022년 LG전자에 의한 냉장고 생산량은 약 977만대에 달했습니다. LG전자 냉장고는 한국, 인도, 멕시코, 중국에서 생산됩니다. LG전자의 냉장고 생산량은 전년 대비 15.19% 감소했습니다. 그러나 냉장고의 생산량은 예측 기간 동안 더욱 증가할 것으로 예상되며 사이클로펜테인 시장을 견인합니다.

따라서 예측 기간 동안 냉동 응용 분야가 시장을 독점하게 됩니다.

시장을 독점하는 아시아태평양

예측 기간 동안 아시아태평양은 사이클로펜테인 시장을 독점할 것으로 예상됩니다. 중국과 인도와 같은 국가에서는 가정용 및 상업용 냉장고에서의 사용이 증가하고 있기 때문에 사이클로펜테인 수요가 증가하고 있습니다.

중국은 하이드로클로로플루오로카본(HFC)의 최대 생산 및 소비국입니다. HCFC와 관련된 환경 문제로 인해 HCFC는 단계적으로 폐지될 전망입니다. 이것은 사이클로펜테인을 포함하는 비 HCFC 발포제에 충분한 기회를 가져올 것으로 보입니다.

중국국가통계국에 따르면 중국의 가정용 냉장고 생산량은 8,664만대입니다. 전년도의 생산 대수 8,992만대와 비교하면 약간 감소하고 있습니다. 그러나 중국 전역의 급속한 도시화에 따라 생산량이 증가할 것으로 예상되어 현재의 연구시장을 견인하고 있습니다.

마찬가지로 일본에서는 가정용 냉장고의 생산 대수는 전년도의 126만대에서 2022년에는 128만대로 1.59%의 성장률로 증가하였습니다. 그러므로 냉장고의 생산량 증가는 이 나라의 사이클로펜테인 시장을 견인하게 됩니다.

또한 화학시장의 확대에 따라 화학용제로서 사이클로펜테인 수요도 증가하고 있습니다. 예를 들어, 인도의 화학 부문은 2000년 4월부터 2022년 12월 사이에 209억 6,000만 달러에 이르는 FDI 유입으로 입증된 수년간 건전한 투자를 해왔습니다. 또한 정부는 2023년부터 2024년까지 연방예산으로 화학석유화학부에 2,093만 달러를 할당하여 국내 화학제품 제조를 추진하고 있습니다.

전반적으로 냉장고 및 화학 산업에서 사이클로펜테인 수요가 증가하면 예측 기간 동안이 지역 시장을 견인할 것으로 보입니다.

사이클로펜탄 산업 개요

사이클로펜탄 시장은 통합됩니다. 시장의 주요 기업(순부동)에는 Dymatic Chemicals, Inc, Haldia Petrochemicals Limited, HCS Group GmbH, INEOS, YEOCHUN NCC 등이 있습니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

폴리우레탄을 제조하는 발포제 용도에서 수요 증가

냉동용도에서 수요 증가

기타 촉진요인

억제요인

보다 우수한 대체 제품의 가용성

사이클로펜테인과 관련된 건강 문제

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 진입업자의 위협

대체품의 위협

경쟁도

제5장 시장 세분화 : 시장 규모(금액 기준)

기능별

발포제 및 냉매

용제 및 시약

기타 기능(고무 접착제, 수지 등)

용도별

냉동

단열재

화학용제

기타 용도(퍼스널케어, 연료 첨가제 등)

지역별

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴 및 협정

시장 점유율(%)** 및 랭킹 분석

주요 기업의 전략

기업 프로파일

Dymatic Chemicals, Inc

Haldia Petrochemicals Limited

HCS Group GmbH

INEOS

Liaoning Yufeng Chemical Co., Ltd.

Meilong Cyclopentane Chemical Co.,Ltd.

Merck KGaA

PURECHEM.CO.KR

SINTECO SRL

TRECORA RESOURCES

YEOCHUN NCC CO., LTD

제7장 시장 기회 및 향후 동향

건설 및 자동차 용도에서의 발포제 사용 증가

기타 기회

AJY

영문 목차

영문목차

The Cyclopentane Market size is estimated at USD 398.89 million in 2024, and is expected to reach USD 584.21 million by 2029, growing at a CAGR of greater than 7.5% during the forecast period (2024-2029).

The COVID-19 pandemic hampered the cyclopentane market. Due to nationwide lockdowns in several countries, strict social distancing measures, and disruption in global supply chain networks, the refrigerant industry was severely hit as most of the production plants and industries were shut down. However, the market registered a significant growth rate well after the restrictions were lifted. The market registered a growth rate due to the rising usage of cyclopentane in various applications, such as refrigeration, insulation, and chemical solvents.

Key Highlights

The growing demand for cyclopentane in blowing agent applications to manufacturing polyurethane and the increasing usage in refrigeration applications are expected to drive the market for cyclopentane.

On the flip side, the availability of better substitute products and health-related issues associated with cyclopentane is expected to hinder the growth of the market.

The increasing use of blowing agents in construction and automotive applications is expected to create opportunities for the market during the forecast period.

The Asia-Pacific region is expected to dominate the market owing to the rising demand for cyclopentane from refrigeration, insulation, and chemical solvent applications.

Cyclopentane Market Trends

Refrigeration Application Segment to Dominate the Market

The cyclopentane is formed by cracking cyclohexane in the presence of alumina at high pressure and temperature. Cyclopentane is majorly used as a foam-blowing agent in the production of polyurethane, which is further used in the manufacture of refrigerators, freezers, etc.

The demand for refrigerators is increasing in the food and beverage sectors. The rising demand for storing food products at stable temperatures is fueling the demand for refrigerators and freezers in the food and beverage sector.

Furthermore, in the pharmaceutical sector, the increase in the demand for safe storage of blood and blood derivatives and temperature-sensitive medicines from hospitals, pharmacies, clinics, and diagnostic centers is also propelling the demand for refrigeration in the healthcare and pharmaceutical industry.

In the European region, refrigerator manufacturers are using cyclopentane as a blowing agent in polyurethane foam insulation in place of CFC (Chlorofluorocarbon) and HCFC (hydrochlorofluorocarbon). Due to the stringent regulations on the usage of HCFC compounds, the usage of cyclopentane is increasing in refrigeration applications.

Similarly, in Asia Pacific, Middle-East and Africa, and Latin America regions, the governments introduced various policies to phase out the usage of HCFC (hydrochlorofluorocarbon) in refrigerator applications. The demand for cyclopentane is being driven by a growth in population and an increase in demand for residential refrigerators and building applications in these regions.

In 2022, the production volume of refrigerators by LG Electronics amounted to around 9.77 million. LG Electronics' refrigerators were manufactured in South Korea, India, Mexico and China. The production volume of refrigerators by LG Electronics decreased by 15.19% as compared to the previous year. However, the production volume of refrigerators is further expected to increase over the forecast period, thereby driving the market for cyclopentane.

Thus, the refrigeration application segment will dominate the market during the forecast period.

Asia-Pacific Region to Dominate the Market

Asia-Pacific region is expected to dominate the market for cyclopentane during the forecast period. In countries like China and India, owing to increasing use in residential and commercial refrigerators, the demand for cyclopentane is increasing in the region.

China is the largest producer & consumer of hydrochlorofluorocarbons (HFCs). It is expected to phase out HCFCs due to the environmental concerns associated with them. It will create ample opportunities for the non-HCFC foaming agents, including cyclopentane.

According to the National Bureau of Statistics of China, the production volume of household refrigerators in China is registered at 86.64 million units. It is slightly declined as compared to 89.92 million units manufactured in the previous year. However, the production volume is expected to increase with the rapid urbanization across China, thereby driving the current studied market.

Similarly, in Japan, the production volume of residential refrigerators increased at a growth rate of 1.59% to 1.28 million units in 2022, as compared to 1.26 million units manufactured in the previous year. Thus, the increasing production volume of refrigerators will drive the market for cyclopentane in the country.

Furthermore, the demand for cyclopentane as a chemical solvent is increasing in the region, with an increasing chemical market. For instance, the Indian chemical sector witnessed healthy investments over the years, as evidenced by the FDI inflows that reached USD 20.96 billion between April 2000 and December 2022. Further, the government allocated USD 20.93 million to the Department of Chemicals and Petrochemicals under the Union Budget 2023-24, thereby boosting chemical manufacturing in the country.

Overall, the increasing demand for cyclopentane from refrigerators and chemical industries is likely to drive the market in the region during the forecast period.

Cyclopentane Industry Overview

The Cyclopentane market is consolidated. Some of the major players (not in any particular order) in the market include Dymatic Chemicals, Inc., Haldia Petrochemicals Limited, HCS Group GmbH, INEOS, and YEOCHUN NCC CO., LTD, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Growing Demand in Blowing Agent Application to Manufacture Polyurethane

4.1.2 Increasing Demand in Refrigeration Application

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Availability of Better Substitute Products

4.2.2 Health Related Issues Associated with Cyclopentane

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

5.1 Function

5.1.1 Blowing Agent & Refrigerant

5.1.2 Solvent & Reagent

5.1.3 Other Functions (Rubber Adhesives, Resins, etc.)

5.2 Application

5.2.1 Refrigeration

5.2.2 Insulation

5.2.3 Chemical Solvent

5.2.4 Other Applications (Personal Care, Fuel Additives, etc.)

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Dymatic Chemicals, Inc

6.4.2 Haldia Petrochemicals Limited

6.4.3 HCS Group GmbH

6.4.4 INEOS

6.4.5 Liaoning Yufeng Chemical Co., Ltd.

6.4.6 Meilong Cyclopentane Chemical Co.,Ltd.

6.4.7 Merck KGaA

6.4.8 PURECHEM.CO.KR

6.4.9 SINTECO S.R.L

6.4.10 TRECORA RESOURCES

6.4.11 YEOCHUN NCC CO., LTD

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Increasing Use of Blowing Agents in Construction and Automotive Applications