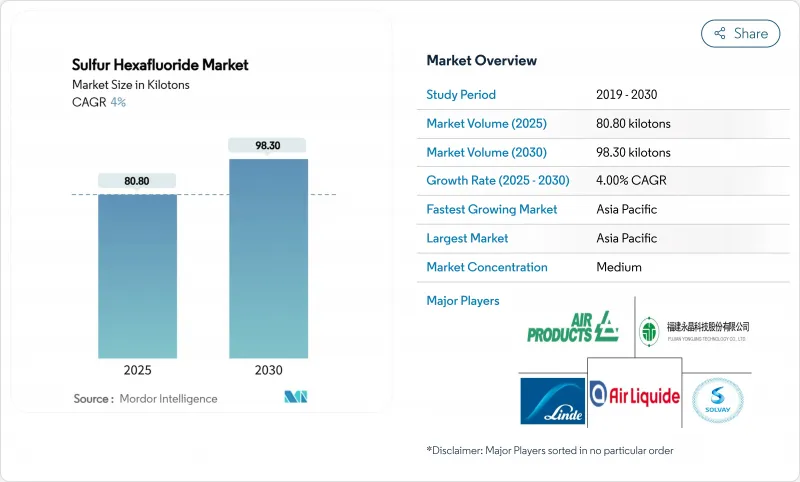

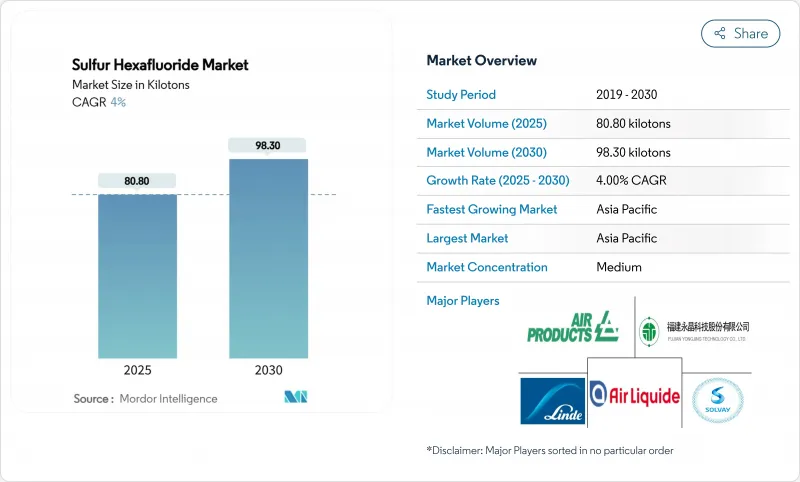

육불화황 시장 규모는 2025년에 80.80킬로톤으로 평가되었고, 예측기간 중(2025-2030년)의 CAGR은 4%를 나타낼 것으로 예측되며, 2030년에 98.30킬로톤에 이를 전망입니다.

신흥국에서의 강력한 전력망 확장 프로그램, 급증하는 반도체 생산 능력, 해상 풍력 송전 프로젝트는 환경 규제가 강화되는 상황에서도 수요를 유지하고 있습니다. 전력 회사들은 가스 절연 개폐기(GIS)에 SF6를 계속해서 지정하고 있는데, 이는 타의 추종을 불허하는 절연 강도, 소형 설치 공간, 신속한 가동이라는 장점을 제공하기 때문입니다. 기존 대체재들은 아직도 이러한 장점을 따라잡지 못하고 있습니다. 반도체 제조업체들은 빠르고 깨끗한 플라즈마 에칭을 위해 초고순도 SF6를 필요로 하며, 이 요구는 특징 크기가 축소됨에 따라 더욱 심화됩니다. 한편, 의료 및 마그네슘 다이캐스팅 용도는 점진적인 성장을 제공하여 규제 충격 완화에 도움이 되는 다양한 최종 시장을 창출합니다.

중국의 SF6 배출량은 2011년 2.6Gg에서 2021년에 5.1Gg로 증가하지만, 이는 송전망의 기록적인 확장에 맞추어 송전사업자가 콤팩트한 가스 절연 변전소를 설치했기 때문입니다. 인도에서는 급속한 도시화 속에서 전압의 안정성을 확보하기 위해 SF6 스위치기어를 지정한 네트워크의 현대화에 2,000캐롤 루피를 계상하고 있습니다. 일반적인 변전설비는 25년부터 50년간 사용되기 때문에 설치결정마다 장래의 육불화황 시장 수요가 확정될 것입니다. 가스절연변전소는 공기절연변전소보다 45% 빨리 통전할 수 있으므로 혼잡완화를 서두르는 전력회사에게는 시간을 절약할 수 있습니다. 그 결과, 환경정책에 대한 논의가 격화되고 있음에도 불구하고, 육불화황시장은 아시아태평양 전역에서 존재감을 계속 늘리고 있습니다.

유럽연합(EU)은 2026년부터 중전압 개폐기, 2032년부터 고전압 장비에서 SF6 사용을 금지하여 전력 회사들이 개조 계획을 가속화하도록 강제하고 있습니다. 캘리포니아주는 2033년까지 완전한 단계적 폐지를 의무화하고 연간 누출률을 1%로 제한하여 자산 소유자들이 고가의 모니터링 시스템에 투자하도록 하고 있습니다. 뉴욕과 매사추세츠에서도 유사한 추세가 나타나 SF6 의존 자산에 대한 투자 기간이 단축되면서 선진 지역의 구매량이 위축되고 있습니다. 이러한 중첩된 정책들은 육불화황 시장 성장 전망에서 1.8% 포인트를 감소시킵니다.

유럽 연합(EU)은 2026년부터 중전압 개폐기, 2032년부터 고압 개폐기에 SF6의 사용을 금지하고 있으며, 전력회사는 리노베이션 계획을 앞당겨야 합니다. 캘리포니아는 2033년까지 완전한 단계적 폐지를 의무화하여 연간 누설률을 1%로 제한하고 있습니다. 뉴욕주와 매사추세츠주에서도 비슷한 방침으로 SF6 의존 자산의 투자기간이 단축되어 선진지역의 조달량이 감소합니다. 이러한 중복 정책은 육불화황 시장의 성장 전망을 1.8포인트 낮춥니다.

2024년 육불화황 시장 점유율의 61.18%를 전자/기술 등급 부문이 차지했습니다. 이는 전력사들이 개폐기, 차단기, 가스 절연 선로에 검증된 절연 성능을 우선시하기 때문입니다. 기술 등급 SF6는 상품 가격 동향을 따르며, 변전소 현장까지 대량 탱커 운송이 가능한 확립된 글로벌 유통 채널의 혜택을 받습니다. 개조 프로젝트가 예측 기간 내 지속됨에 따라 해당 부문은 전체 SF6 시장을 지탱하는 상당한 기본 부하 물량을 유지합니다.

초고순도 SF6은 절대 톤수 기준 규모는 작지만, 첨단 반도체 및 LCD 제조 수요에 힘입어 제품 유형 중 가장 빠른 연평균 성장률(CAGR) 4.90%로 확대될 전망입니다. 오염 물질 농도를 10억분의 1 이하로 유지하려면 다단계 정제 공정, 특수 용기, 전용 공급망이 필요합니다. 이러한 생산 프로토콜을 숙달한 공급업체는 낮은 물량을 상쇄하는 높은 마진을 확보하며, 환경 정책으로 인해 기존 전력 수요가 위축되는 상황에서 전략적 헤지 수단을 제공합니다. 두 등급의 제품이 함께 작용하여 육불화황 시장은 일반 상품과 특수 니치 시장 간 균형 잡힌 포트폴리오를 유지합니다.

육불화황 시장 보고서는 제품 유형(전자 및 기술 등급, 초고순도 등급), 용도(전력 및 에너지, 전자, 금속 제조, 의료, 기타 용도), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)으로 구분하고 있습니다. 시장 예측은 수량(톤)으로 제공됩니다.

아시아태평양 지역은 2024년 47.65% 점유율로 육불화황 시장을 주도했으며, 2030년까지 연평균 4.75% 성장률을 기록할 것으로 전망됩니다. 중국의 전력망 운영사들은 초고압 송전 회랑에 소형 550kV 가스절연변전소를 설치하여 기록적인 재생에너지 용량을 수용하고 있으며, 이는 수십 년간 지속될 SF6 수요를 확고히 하는 전략입니다. 인도의 주간 송전망 강화 프로그램은 급속히 도시화되는 부하 중심지의 신뢰성 향상을 위해 SF6 링 메인 유닛을 활용합니다. 한국의 반도체 확장은 지역 초고순도 수요를 증폭시키는 반면, 일본은 SF6 무사용 솔루션의 기술 시범국으로 자리매김하며 기존 기술과 신기술이 공존하는 이중 구조를 형성합니다.

북미는 노후 자산 교체와 규제 준수를 균형 있게 추진하는 가운데 중간 단일자리 수치(5%대)의 소비 증가세를 보입니다. 캘리포니아주의 2033년 단계적 폐지 및 누출 제한 규정은 모니터링 및 포집 시스템의 조기 도입을 촉진하지만, 현장 적용 가능한 대체재가 부족한 고전압 등급에서는 타 주 전력망 운영사들이 여전히 SF6 사용을 요구합니다. 연방 인프라 복원력 강화 자금 지원으로 전체 수요는 안정적이지만, 재활용률 상승이 신규 공급 수요를 완화하는 데 기여합니다. 캐나다는 캘리포니아 배출권 거래제와의 연계로 국경 간 정책 조정이 이루어지며, 기존 장비용 예비품 확보와 동시에 SF6 무사용 시범 운영을 모색 중입니다.

유럽은 가장 엄격한 정책 환경에 직면 : 개정된 F-가스 규정은 2026년부터 중전압 SF6 스위치기어 신규 설치를, 2032년부터는 고전압 설치를 금지합니다. 독일 및 북유럽 기업을 중심으로 한 송전 시스템 운영사들은 진공 차단기 및 청정 공기 기술을 시범 운영 중이지만, 기존 설비 확장에선 여전히 SF6에 의존하고 있습니다. 영국은 EU 규제를 동일하게 적용하며, 개조 프로그램에 약 1억-2억 8천만 파운드의 추가 준수 비용이 발생할 것으로 추정됩니다. 교체 주기가 느린 남부 및 동부 유럽 유틸리티 기업들은 비용 압박에 직면해, 제한된 SF6 조달이 2020년대 중반 이후로 연장될 가능성이 있습니다. 라틴 아메리카, 중동, 아프리카는 기초 전기화 및 산업 역량 확장으로 여전히 규모는 작지만 고성장 지역으로 남아 있어 육불화황(SF6) 시장의 미래 성장 가능성을 제시합니다.

The Sulfur Hexafluoride Market size is estimated at 80.80 kilotons in 2025, and is expected to reach 98.30 kilotons by 2030, at a CAGR of 4% during the forecast period (2025-2030).

Robust grid-upgrade programs in emerging economies, surging semiconductor fabrication capacity, and offshore wind transmission projects are sustaining demand even as environmental regulations tighten. Electrical utilities continue to specify SF6 for gas-insulated switchgear because it delivers unrivalled dielectric strength, compact footprints, and rapid energization, advantages that existing alternatives still struggle to match. Semiconductor manufacturers require ultra-high-purity SF6 to achieve fast, clean plasma etching, and this requirement deepens as feature sizes shrink. Meanwhile, medical and magnesium die-casting uses provide incremental growth, creating diversified end-markets that help buffer regulatory shocks.

China's SF6 emissions climbed from 2.6 Gg in 2011 to 5.1 Gg in 2021 as transmission developers installed compact gas-insulated substations to keep pace with record-setting grid expansions. India has earmarked INR 2,000 crore for network modernization that specifies SF6 switchgear to secure voltage stability during rapid urbanization. Because typical substation assets remain in service for 25 to 50 years, every installation decision effectively locks in future sulfur hexafluoride market demand. Gas-insulated stations can be energized 45% faster than air-insulated yards, a time saving valued by utilities racing to alleviate congestion. As a result, the sulfur hexafluoride market continues to deepen its presence across Asia-Pacific despite intensifying environmental policy debates.

Korea's USD 471 billion semiconductor cluster, slated to add 16 fabs by 2047, exemplifies capital flows that elevate consumption of ultra-high-purity SF6. In deep-trench silicon etching, SF6 generates fluorine radicals that remove material up to 100 times faster than rival gases, ensuring throughput targets for 3 nm and below nodes. Although abatement systems curb direct emissions, a portion of feedstock still reaches the atmosphere, prompting regulatory scrutiny as fabrication capacity scales. Even so, process engineers continue to specify SF6 until drop-in alternatives can replicate its etching precision, keeping the sulfur hexafluoride market firmly embedded in advanced manufacturing value chains.

The European Union has banned SF6 in medium-voltage switchgear from 2026 and in high-voltage gear from 2032, forcing utilities to accelerate retrofit plans. California mandates complete phase-out by 2033 and restricts annual leak rates to 1%, compelling asset owners to fund costly monitoring systems. Similar trajectories in New York and Massachusetts compress investment horizons for SF6-dependent assets, dampening procurement volumes in developed regions. These overlapping policies subtract 1.8 percentage points from the sulfur hexafluoride market growth outlook.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The electronic/technical-grade segment accounted for 61.18% of sulfur hexafluoride market share in 2024 as utilities prioritize proven insulation performance for switchgear, breakers, and gas-insulated lines. Technical-grade SF6 follows commodity price dynamics and benefits from established global distribution channels that permit bulk tanker deliveries to substation sites. Because retrofit projects continue through the forecast period, the segment maintains a sizable base-load volume that anchors the overall sulfur hexafluoride market.

Ultra-high-purity SF6, while representing a smaller absolute tonnage, is forecast to expand at 4.90% CAGR, the fastest among product types, propelled by advanced semiconductor and LCD fabrication. Maintaining contaminant thresholds below parts-per-billion requires multiple purification stages, specialised cylinders, and dedicated supply chains. Suppliers that master these production protocols secure higher margins, offsetting lower volumes and providing a strategic hedge as environmental policy squeezes traditional utility demand. Collectively, the two grade tiers ensure that the sulfur hexafluoride market retains a balanced portfolio across commodity and specialty niches.

The Sulfur Hexafluoride Market Report is Segmented by Product Type (Electronic/Technical Grade, Ultra-High Purity Grade), Application (Power and Energy, Electronics, Metal Manufacturing, Medical, Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (tons).

Asia-Pacific dominated the sulfur hexafluoride market with 47.65% share in 2024 and is projected to log a 4.75% CAGR through 2030. China's grid operators are installing compact 550 kV gas-insulated substations across ultrahigh-voltage corridors to accommodate record renewable capacity, a strategy that cements multi-decade SF6 demand. India's program to reinforce inter-state transmission uses SF6 ring-main units to improve reliability in rapidly urbanizing load centers. South Korea's semiconductor expansion amplifies regional ultra-high-purity volumes, while Japan positions itself as a technology demonstrator for SF6-free solutions, creating a dual-track landscape that blends incumbent and emerging technologies.

North America shows mid-single-digit consumption growth as utilities balance ageing-asset replacements with regulatory compliance. California's 2033 phase-out and leak caps compel early adoption of monitoring and capture systems, but grid operators in other states continue to specify SF6 in high-voltage classes where field-ready alternatives remain scarce. Federal infrastructure funding for resilience upgrades keeps overall demand stable, although rising recycling rates help temper fresh supply needs. Canada's linkages to California's cap-and-trade system drive cross-border policy alignment, nudging Canadian utilities to explore SF6-free pilots while maintaining critical spares for legacy equipment.

Europe faces the most stringent policy environment: the revised F-gas regulation bans new medium-voltage SF6 switchgear from 2026 and high-voltage installations from 2032. Transmission system operators, led by entities in Germany and the Nordics, are piloting vacuum-interrupter and clean-air technologies but still rely on SF6 for brownfield extensions. The United Kingdom mirrors EU limits, adding compliance costs estimated at GBP 100-280 million for retrofit programs. Southern and Eastern European utilities with slower replacement cycles face cost pressures, potentially extending limited SF6 procurement beyond mid-decade. Latin America, the Middle East, and Africa collectively remain smaller yet high-growth territories as they expand base-line electrification and industrial capacity, offering future upside for the sulfur hexafluoride market.