ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

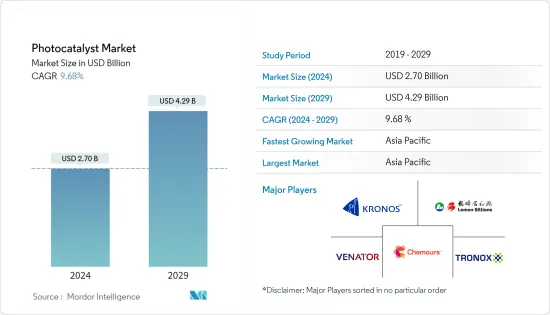

광촉매 시장 규모는 2024년 27억 달러로 추정되며, 2029년까지 42억 9,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 9.68%의 CAGR로 성장할 것으로 예상됩니다.

COVID-19 전염병은 광촉매 시장에 부정적인 영향을 미쳤습니다. 현재 시장은 전염병에서 회복되어 큰 폭으로 성장하고 있습니다.

주요 하이라이트

단기적으로 이산화티타늄에 대한 높은 수요와 수처리 및 공기 정화 응용 분야의 증가로 인해 광촉매 시장 수요가 증가할 수 있습니다.

그러나 막대한 설비투자는 시장 성장을 저해할 것으로 예상됩니다.

그럼에도 불구하고, 소독제로서의 연구 개발의 증가는 매력적인 시장 성장을 창출하고 예측 기간 동안 큰 잠재력을 가져올 것으로 예상됩니다.

아시아태평양은 세계 시장을 독점할 것으로 예상되며, 소비의 대부분은 중국과 인도에서 발생합니다.

광촉매 시장 동향

셀프 클리닝 애플리케이션에 대한 수요 증가

광촉매에 의한 셀프 클리닝은 아마도 건축 건설에서 가장 널리 사용되는 나노 기능일 것입니다. 전 세계의 많은 건물이이 기능을 사용하고 있습니다. 그 주요 효과는 표면에 먼지가 부착되는 정도를 크게 줄이는 것입니다. 또 다른 장점은 표면의 얼룩과 불분명한 얼룩의 햇빛이 줄어들어 유리와 반투명 필름의 광 투과율이 향상되어 조명 에너지 비용을 절감할 수 있다는 것입니다.

최근 건물 외부와 내부를 코팅하는 광촉매 페인트와 코팅이 개발되고 있습니다. 광촉매 코팅은 먼지를 씻어낼 뿐만 아니라 공기 중의 오염물질과 건물 외부의 스모그와 같은 오염물질과 먼지를 분해합니다. 또한 광촉매 코팅은 건물의 실내 가구에서 냄새를 제거하고 VOC, 부유 바이러스, 박테리아를 분해합니다. 또한 광촉매 코팅은 건물 내부의 목재 표면을 보호하기 위해 선호되는 주요 옵션 중 하나입니다.

광촉매 재료의 응용은 대형 건물에만 국한되지 않습니다. 예를 들어, 온실이나 겨울 정원에도 똑같이 적합합니다. 도로 건설에서는 투명 코팅을 방음벽 등에 사용할 수도 있습니다. 내구성이 뛰어난 코팅이 적용된 타일은 실내와 실외 모두에서 사용할 수 있습니다. 마찬가지로 외관의 또 다른 일반적인 건축 자재인 콘크리트도 자동 세척 표면을 장착 할 수 있습니다. 따라서 건설 부문은 예측 기간 동안 자체 세척 광촉매 재료에 대한 수요에 크게 기여할 것으로 예상됩니다.

세계 건설 산업은 꾸준히 성장하고 있습니다. 아시아태평양에서는 중동 및 아프리카과 마찬가지로 수많은 시장 기회로 인해 건설 부문에 대한 막대한 투자가 이루어지고 있습니다.

중국 국가통계국에 따르면 중국의 건설 생산액은 2020년 26조 3,900억 위안(3조 7,900억 달러), 2021년에는 약 29조 3,000억 위안(4조 2,000억 달러)으로 정점을 찍을 것으로 예상했습니다.

일본 국토교통성(일본)에 따르면 2021년도 일본의 총 건설투자액은 66조 6,000억 엔(약 4억 9,810만 달러)을 넘어섰으며, 이 중 절반 이상을 건축 공사가 차지할 것으로 예상했습니다. 총 건설 지출은 2022년에 약 67조 엔(약 5억 1,090만 달러)에 달할 것으로 예상됩니다.

유럽에서는 독일이 건설 분야의 발전을 주도하고 있습니다. 알렉산더 베를린의 캐피탈 타워와 에스트렐 타워는 현재 독일이 개발 중인 주요 고층 빌딩 중 일부입니다. 독일은 인프라 부문에 대한 막대한 투자와 주택 수요 증가로 인해 건설 부문이 더욱 성장하고 있습니다.

세계은행에 따르면, 건설 산업은 2021년에 12조 9,000억 달러 규모로 성장하여 연간 3%의 성장률을 기록할 것으로 예상됩니다. 여기에는 주거 및 상업용 부동산 개발, 인프라 및 산업 건설이 모두 포함됩니다. 건설 지출 데이터에는 인건비 및 재료비, 건축 및 토목 공사, 세금 등이 포함됩니다.

자가 세척 광촉매 코팅은 자동차 앞 유리, 창 유리, 고층 건물, 현미경, 안경, 태양전지판 커버, 주방 가전 제품, 많은 전자 장비의 화면과 같은 많은 응용 분야에서 사용되는 광학적으로 투명한 유리 재료의 코팅에 사용됩니다. 광학 기기.

저비용, 경량, 유연한 PC 기판의 자동 세척 광촉매 코팅은 다기능 자동 세척 장치의 유용성을 위해 필수적입니다. 따라서 자동차, 전자, 의료, 태양 에너지 생산과 같은 다른 최종사용자 산업도 예측 기간 동안 자체 세척 가능한 광촉매 재료의 수요에 크게 기여할 것으로 예상됩니다.

앞서 언급한 모든 요인은 예측 기간 동안 산업 성장에 기여할 것입니다.

아시아태평양이 시장을 독점

아시아태평양은 시장 점유율과 시장 수익 측면에서 광촉매 시장을 지배하고 있습니다. 이 지역은 예측 기간 동안 계속 우위를 유지할 것으로 예상됩니다.

광촉매의 초친수성으로 인해 자체 세정 작용을 얻을 수 있습니다. 예를 들어, 이산화티타늄은 광촉매 보호막을 형성하고 초산화 및 친수성을 통해 자체 세정하는 특성을 가지고 있습니다. 이러한 광촉매의 특성은 페인트 및 코팅의 자체 세정 보조제로서 수요가 많은 응용 분야에 적합합니다. 또한 광촉매로서 고유한 세정 및 항균 특성을 전달합니다. 따라서 건설 활동이 증가함에 따라 페인트 및 코팅에 대한 수요가 증가할 것으로 예상되며, 이는 광촉매의 시장 수요를 주도하고 있습니다.

건설, 자동차 및 포장 분야의 수요 증가로 인한 페인트 및 코팅에 대한 수요 증가는 예측 기간 동안 광촉매 시장을 견인할 것으로 예상됩니다. 중국은 전 세계 총 페인트 및 코팅의 약 30%를 생산하고 있으며, 페인트 및 코팅에 유도된 광촉매의 자체 세척 특성으로 인해 광촉매 소비의 주요 공급원이 되고 있습니다.

PPG Industries는 2022년까지 6억 2,000만 위안(8,903만 달러)을 투자하여 중국 남부에 연구개발 및 생산기지를 건설할 계획입니다. Asia Cuanon은 또한 후난성 창사에 총 6억 위안(8,616만 달러)을 투자하여 20만 톤의 고품질 건축용 페인트 및 기타 건축 자재를 생산할 수 있는 새로운 생산기지를 건설하는 계약을 체결하였습니다.

BASF Coatings(Guangdong)는 아시아에서 유일한 BASF의 자동차 수리용 도료 생산 기지입니다. 이 회사는 2022년 상반기에 생산을 시작할 자동차 수리 코팅을 위한 새로운 시설을 건설하고 있습니다.

중국 국가통계국에 따르면 중국은 세계 최대 건설 시장으로 성장했습니다. 2021년 중국 건설 산업의 가치는 1조 1,174억 2,000만 달러에 달합니다. 중국 정부는 중소도시의 인프라 건설에 집중할 계획으로 건설 산업은 연간 5%의 성장률을 기록할 것으로 예상됩니다.

일본의 페인트 및 코팅 산업은 페인트 및 코팅 산업의 가장 큰 소비자인 자동차, 화학, 가전 및 전자 산업에 확고한 제조 기반을 가지고 있으며, 아시아태평양에서 두 번째로 큰 규모입니다.

일본의 페인트 및 코팅 생산은 주로 건설 및 기타 산업 부문의 수요 증가에 의해 주도되고 있습니다. 국토 교통성에 따르면 2021년 일본의 총 건설 투자액은 66 조 6,000억 엔(4억 9,903만 달러)이며이 지출의 절반 이상을 건축 공사가 차지할 것으로 예상됩니다. 2022년 건설 투자 총액은 약 67조엔(5억203만 달러)에 달할 것으로 예상됩니다.

국내 수요 증가에 따른 이러한 페인트 생산 확대는 예측 기간 동안 광촉매에 대한 시장 수요를 더욱 촉진할 것으로 예상됩니다.

광촉매 산업 개요

광촉매 시장은 본질적으로 통합되어 있으며, 상위 5개 기업이 주요 생산 능력을 보유하고 있습니다. 주요 기업으로는 The Chemours Company, Tronox Holdings PLC, Venator Materials PLC, Lomon Billions, Kronos Worldwide Inc. 등이 있습니다.

기타 혜택

엑셀 형식의 시장 예측(ME) 시트

3개월간 애널리스트 지원

목차

제1장 서론

조사 가정

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

빠르게 높아지는 이산화티타늄 수요

수처리와 공기 정화의 용도 증가

성장 억제요인

거액의 설비 투자

기타 성장 억제요인

업계의 밸류체인 분석

Porter's Five Forces 분석

신규 참여업체의 위협

구매자의 교섭력

공급 기업의 교섭력

대체 제품의 위협

경쟁 정도

제5장 시장 세분화

유형

이산화티타늄

산화 아연

기타 유형

용도

셀프 클리닝

공기 정화

수처리

김서림 방지

기타 용도

지역

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카공화국

기타 중동 및 아프리카

제6장 경쟁 상황

인수합병, 합작투자, 협업 및 계약

시장 점유율(%)**/순위 분석

유력 기업이 채용한 전략

기업 개요

Daicel Miraizu Ltd

Green Millennium

Hangzhou Harmony Chemical Co. Ltd

ISHIHARA SANGYO KAISHA Ltd

KRONOS Worldwide Inc.

Lomon Billions

Nanoptek Corp.

SHOWA DENKO KK

TAYCA

The Chemours Company

TitanPE Technologies Inc.

Tronox Holdings PLC

Venator Materials PLC

제7장 시장 기회와 향후 동향

소독제로서 연구개발이 진행된다

ksm

영문 목차

영문목차

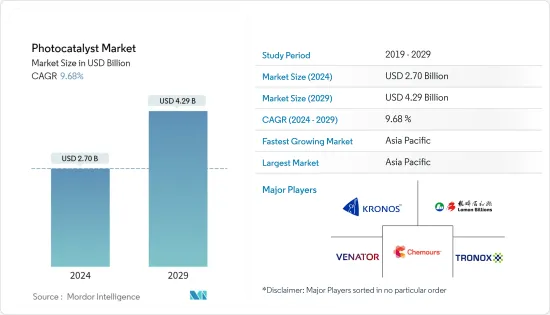

The Photocatalyst Market size is estimated at USD 2.70 billion in 2024, and is expected to reach USD 4.29 billion by 2029, growing at a CAGR of 9.68% during the forecast period (2024-2029).

The COVID-19 pandemic had a negative impact on the market for photocatalysts. Currently, the market has recovered from the pandemic and growing at a significant rate.

Key Highlights

Over the short term, high demand for titanium dioxide and increasing water treatment and air purification applications are likely to drive the demand for the photocatalyst market.

However, high capital investments are expected to hinder the growth of the market.

Nevertheless, increasing research and development as a disinfectant is expected to generate attractive market growth and give substantial potential in the forecast period.

The Asia-Pacific region is expected to dominate the global market, with the majority of the consumption coming from China and India.

Photocatalyst Market Trends

Increasing Demand from Self Cleaning Application

Photocatalytic self-cleaning is probably the most widely used nano-function in building construction. Numerous buildings around the world make use of this function. Its primary effect is that it greatly reduces the extent of dirt adhesion on surfaces. Another advantage is that light transmission for glazing and translucent membranes is improved since surface dirt and obscure grime sunshine are less, which can reduce lighting energy costs.

Photocatalytic paints and coatings have been developed in recent years to coat the outer surface and interiors of the building. Photocatalytic coatings not only wash off dirt but also break down contaminants and stains: airborne pollutants, and smog from the exterior surfaces of the building. Furthermore, photocatalyst coatings remove odors and break down VOC, airborne viruses, and bacteria from the interior furniture of the building. Moreover, photocatalyst coating is one of the major options preferred to protect wooden surfaces in the interior of the building.

The application of photocatalytic material is not limited exclusively to large buildings. It can be equally appropriate, for example, for conservatories and winter gardens. In road building, the transparent coating can also be used, for example, for noise barriers. Tiles with baked-on durable coatings are available for use both indoors and outdoors. Likewise, concrete, another common building material for facades, can also be equipped with a self-cleaning surface. Hence the construction sector will contribute majorly to the demand for self-cleaning photocatalytic materials in the forecast period.

The global construction industry is growing at a healthy rate. Asia-Pacific, along with the Middle East and African regions, is witnessing huge investments in the construction sector due to numerous market opportunities available in these markets.

According to the National Bureau of Statistics of China, China's construction output value peaked in 2021 at roughly CNY 29.3 trillion (USD 4.2 trillion), compared to CNY 26.39 trillion (USD 3.79 trillion) in 2020.

According to The Ministry of Land, Infrastructure, Transport, and Tourism (Japan), total construction investment in Japan was over JPY 66.6 trillion (~USD 498.10 million) in the fiscal year 2021, with building construction accounting for more than half of this expenditure. Total construction spending is expected to reach almost JPY 67 trillion (~USD 501.09 million) in the fiscal year 2022.

In Europe, Germany has taken the lead in developments in the construction sector. Alexander Berlin's Capital Tower and Estrel Tower are some of the major high-rise buildings the country is developing at present. The construction sector is further rising in the country owing to significant investments in its infrastructural sector and further due to the rising demand for residential units.

According to World Bank, the construction industry grew to a spending value of USD 12.9 trillion in 2021 and is expected to grow by three percent per annum. This comprises real estate developments, both residential and commercial, as well as infrastructural and industrial constructions. Data on construction spending cover labor and material costs, architectural and engineering work, and taxes.

The self-cleaning photocatalytic coating is used to coat optically transparent glass materials, which are used in many applications, including automobile windshields, window glass, skyscrapers, microscopes, eyeglasses, solar cell panel covers, kitchen appliances, screens of many electronic devices, and optical instruments.

The self-cleaning photocatalytic coating on low-cost, lightweight, and flexible PC substrates is crucial for multifunctional self-cleaning devices to be useful. Therefore, other end-user industries, such as automobile, electronics, medical, and solar energy generation, will also contribute significantly to the demand for self-cleaning photocatalytic material in the forecast period.

All the aforementioned factors will contribute towards industry growth during the forecast period.

Asia-Pacific Region to Dominate the Market

Asia-Pacific dominates the photocatalyst market in terms of market share and market revenue. The region is set to continue its dominance over the forecast period.

The super-hydrophilic nature of photocatalysts imparts the self-cleaning nature. For instance, titanium dioxide provides a photocatalytic protective film, which possesses the property of self-cleaning by becoming super-oxidative and hydrophilic. This property of photocatalyst caters to its high-demand application as self-cleaning aid in paints and coatings. Moreover, as a photocatalyst, it transmits unique cleaning and anti-microbial properties. Hence, with the increasing construction activity, the demand for paint and coatings is expected to increase, which is driving the market demand for photocatalysts.

The growing demand for paint and coatings due to the growing demand from construction, automotive, and packaging is expected to drive the market for photocatalysts during the forecast period. China produces around 30% of the total global paints and coatings, which is acting as a major source in the consumption of photocatalysts, owing to their self-cleaning properties when induced in paints and coatings.

PPG Industries plans to construct its South Chinese R&D and production base by 2022, with an investment of CNY 620 million (USD 89.03 million). Asia Cuanon also signed an agreement to construct a new production base in Changsha, Hunan province, with a total investment of CNY 600 million (USD 86.16 million), which will include 200 thousand metric tons of high-quality architecture coatings and other construction materials.

BASF Coatings (Guangdong) Co. Ltd has the only automotive refinish coatings production site for BASF in Asia. The company is constructing a new facility for automotive refinish coatings that have started production in the first half of 2022.

According to the National Bureau of Statistics of China, China has grown to become the world's largest construction market. The value of China's construction industry was USD 1,117.42 billion in 2021. Since the government intends to focus on upgrading infrastructure in small and medium-sized communities, the construction industry is expected to increase at a five percent yearly rate.

The paints and coatings industry in Japan was the second largest in Asia-Pacific, as it has well-established manufacturing bases in the automotive, chemicals, appliance, and electronic industries, which are the largest consumers of the paints and coatings industry.

The production of paints and coatings in Japan is mainly driven by the growing demand from the construction and other industrial sectors. According to The Ministry of Land, Infrastructure, Transport, and Tourism (MLIT Japan), total construction investment in Japan was YPY 66.6 trillion (USD 499.03 million) in the fiscal year 2021, with building construction accounting for more than half of this expenditure. Total construction investment is expected to reach almost YPY 67 trillion (USD 502.03 million) in the fiscal year 2022.

All such expansions in paint production with the growing demand in the country are further expected to drive the market demand for photocatalysts during the forecast period.

Photocatalyst Industry Overview

The photocatalyst market is consolidated in nature, with the top five players having major production capacities. Some of the key players are The Chemours Company, Tronox Holdings PLC, Venator Materials PLC, Lomon Billions, KRONOS Worldwide Inc., and others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Rapidly Growing Demand for Titanium dioxide

4.1.2 Increasing Applications in Water Treatment and Air Purification

4.2 Restraints

4.2.1 High Capital Investment

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter Five Forces

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Buyers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Degree of Competition

5 MARKET SEGMENTATION

5.1 Type

5.1.1 Titanium dioxide

5.1.2 Zinc Oxide

5.1.3 Other Types

5.2 Application

5.2.1 Self-Cleaning

5.2.2 Air Purification

5.2.3 Water Treatment

5.2.4 Anti-Fogging

5.2.5 Other Applications

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 France

5.3.3.4 Italy

5.3.3.5 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle-East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%) **/ Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Daicel Miraizu Ltd

6.4.2 Green Millennium

6.4.3 Hangzhou Harmony Chemical Co. Ltd

6.4.4 ISHIHARA SANGYO KAISHA Ltd

6.4.5 KRONOS Worldwide Inc.

6.4.6 Lomon Billions

6.4.7 Nanoptek Corp.

6.4.8 SHOWA DENKO KK

6.4.9 TAYCA

6.4.10 The Chemours Company

6.4.11 TitanPE Technologies Inc.

6.4.12 Tronox Holdings PLC

6.4.13 Venator Materials PLC

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Increasing Research and Development as a Disinfectant