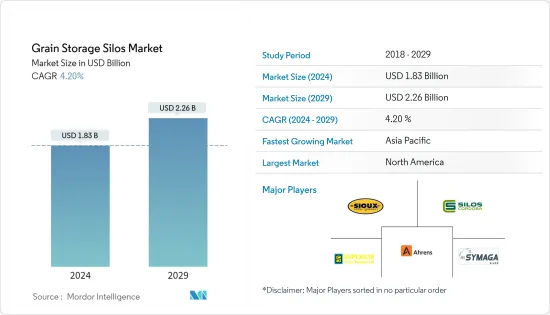

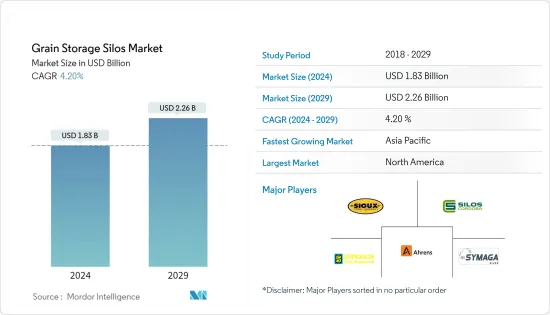

세계의 곡물 저장 사일로(Grain Storage Silos) 시장 규모는 2024년에 18억 3,000만 달러로 추정되며, 2029년에는 22억 6,000만 달러에 달할 것으로 예상되며, 예측기간 중(2024-2029년) CAGR 4.20%로 추이하며 성장할 것으로 예상됩니다.

미국, 러시아, 인도, 브라질 등 세계 주요 곡물 생산국의 곡물 저장 수요 증가가 연구 기간 동안 곡물 저장 사일로 산업을 주도했습니다. 또한 곡물 저장에 필요한 투입 비용과 막대한 투자가 증가하면서 모든 지역에서 사일로에 대한 수요가 증가했습니다. 국제곡물위원회(IGC)에 따르면 전 세계 밀 재고량은 2020년 2억 7,600만 톤에서 2021년 2억 7,800만 톤으로 증가했으며, 2021년에는 2억 7,800만 톤에 달할 것으로 예상됩니다. 이러한 곡물 생산량 증가는 예측 기간 동안 시장의 성장으로 이어졌습니다.

또한 이집트는 곡물, 특히 밀을 수입에 의존하고 있습니다. 우크라이나와 러시아 간의 분쟁으로 인해 밀 공급에 문제가 발생했습니다. 밀 공급을 다변화하기 위한 추가 조치에도 불구하고 국제 가격 상승은 이집트가 국제 공급처에서 대량의 밀을 구매하는 데 방해가 될 것입니다. 따라서 이집트는 계속해서 새로운 사일로를 건설하고 저장 용량을 확장하여 가격 급등을 견디기 위해 수입을 제한할 수 있었습니다.

이와 함께 사일로는 곡물 운송의 자동화로 인해 비용 효율적인 곡물 저장 수단으로 장기적으로 운영 비용을 절감할 수 있습니다. 사일로의 적재 및 하역 비용도 곡물 창고보다 낮은데, 이는 자동화가 SCADA(감독 제어 및 데이터 수집) 시스템에 의해 운영되기 때문입니다. 비용 효율성과 사일로의 큰 저장 용량이라는 이점이 전 세계적으로 곡물 저장 사일로 시장을 주도하고 있습니다.

2020년 곡물 저장 사일로 사용에서 가장 큰 비중을 차지한 지역은 북미 지역입니다. 미국 농무부(USDA)에 따르면 지난 10년 동안 농장 내 저장량은 16억 부셸, 농장 밖 저장량은 22억 부셸 증가하여 각각 14%와 24%의 성장률을 기록했습니다. 국내 생산자들은 대부분 장기 저장이 가능한 평바닥형 또는 호퍼바닥형 사일로를 선호합니다. 이로 인해 미국 내 평바닥 사일로 또는 호퍼 바닥 사일로 시장이 증가했습니다.

또한 미국의 곡물 저장 능력은 지난 20년 동안 크게 향상되었습니다. USDA에 따르면 2020년 미국의 곡물 저장 용량은 약 253억 부셸입니다. 옥수수, 대두, 밀 및 기타 작물의 저장량은 절대적인 양, 수확 시기 및 생산지에 따라 다릅니다. 전국적으로 옥수수가 곡물 재고를 가장 많이 차지합니다. 수확 후 옥수수는 미국 곡물 재고의 4분의 3 이상을 차지하며, 옥수수 재고의 대부분은 농장에 보관되어 있습니다. 2021년 전체 옥수수 재고량 중 72억 3천만 부셸이 농장에 저장되어 있으며, 이는 2020년 대비 3% 증가한 수치입니다. 이러한 주요 곡물 작물의 재고량 증가는 예측 기간 동안 시장 성장으로 이어집니다.

이와 함께 USDA에 따르면 최근 미국과 중국이 주요 원자재에 관세를 부과하면서 미국 농가의 곡물 잉여가 누적되어 전체 저장 가능량의 20%가 대두, 옥수수, 밀로 채워진 것으로 나타났습니다. 기존 저장고가 최대 용량에 도달함에 따라 예측 기간 동안 미국 전역에 더 많은 대형 저장 사일로의 필요성이 더욱 높아질 것으로 예상됩니다.

곡물 저장 사일로 시장은 세분화되어 있으며 대기업이 차지하는 시장 점유율은 낮아지고 있습니다. Ahrens Agri, Buhler Group, Sioux Steel Company, Symaga, Silos Cordoba가 조사 대상 시장의 주요 기업입니다. 신제품 출시, 제휴 및 인수는 세계 시장의 선도 기업들이 채택하는 주요 전략입니다.

The Grain Storage Silos Market size is estimated at USD 1.83 billion in 2024, and is expected to reach USD 2.26 billion by 2029, growing at a CAGR of 4.20% during the forecast period (2024-2029).

The growing demand for grain storage from the leading grain-producing countries in the world, namely, the United States, Russia, India, Brazil, and others, have driven the grain storage silos industry during the study period. Further, rising input costs and heavy investments required in grain storage led to a rise in demand for silos across all regions. According to the International Grains Council (IGC), the global wheat stock increased from 276 million metric tons in 2020, and the stock accounted for 278.0 million tons in 2021. This increase in the production of grains led to the market's growth in the forecast period.

Further, Egypt relies on imports for grains, especially wheat. The conflict between Ukraine and Russia caused wheat supply challenges. Even with additional measures to diversify its wheat supply, rising global prices would impede Egypt's ability to purchase large volumes of wheat from international sources. Therefore, Egypt continued to build new silos and expand its storage capacity, which may allow Egypt to limit imports to withstand price spikes.

Along with this, silos are cost-effective modes of grain storage due to the automation of grain transport, resulting in low operational costs in the long run. The loading and unloading costs of silos are also low than grain warehouses, as automation is operated by the Supervisory Control and Data Acquisition (SCADA) system. The benefits of cost-effectiveness and the large holding capacity of silos are driving the grain storage silos market globally.

North America held the largest share in using silos for grain storage in 2020. As per the United States Department of Agriculture (USDA), in the last ten years, the on-farm storage increased by 1.6 billion bushels and off-farm storage by 2.2 billion bushels, registering a growth of 14% and 24%, respectively. The producers in the country mostly prefer flat-bottom or hopper-bottom silos as they can be used for long-term storage. It increased the market for flat-bottom silos or hopper-bottom silos in the United States.

Moreover, the US grain storage capacity improved substantially in the last 20 years. According to USDA, in 2020, the national grain storage capacity was approximately 25.3 billion bushels. Corn, soybeans, wheat, and other crop storage differ concerning the absolute quantity, harvest timing, and production location. Nationally, corn dominates grain inventories. Post-harvest corn makes up more than three-quarters of US grain inventories, with the majority of corn inventory held on-farm. Of the total corn stocks, 7.23 billion bushels were stored on farms in 2021, an increase of 3% from 2020. This increase in the stocks of major grain crops leads to market growth during the forecast period.

Along with this, as per USDA, the recent imposition of tariffs by both the United States and China on primary commodities led to the accumulation of grain surplus for the US farmers, resulting in 20% of the total available storage filled with soybean, corn, and wheat. It is anticipated to further boost the need for more large storage silos across the country during the forecast period, as the existing ones are reaching full capacity.

The grain storage silos market is fragmented, in which major players account for less market share. Ahrens Agri, Buhler Group, Sioux Steel Company, Symaga, and Silos Cordoba are the major players in the market studied. New product launches, partnerships, and acquisitions are the major strategies adopted by the leading companies in the market globally.