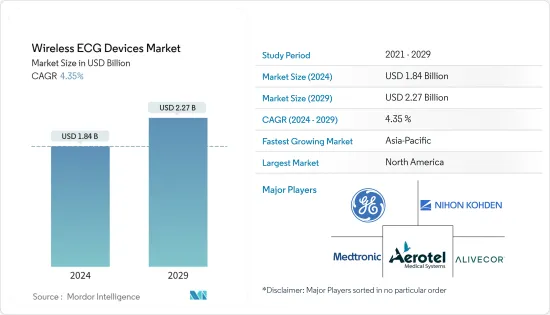

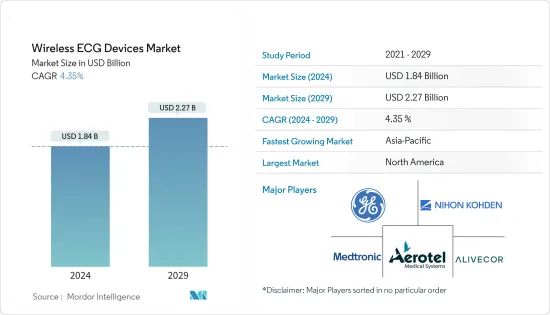

무선 심전도 기기(Wireless ECG Devices) 시장 규모는 2024년에 18억 4,000만 달러로 추정되며, 2029년까지 22억 7,000만 달러에 이를 것으로 예측되며, 예측 기간(2024-2029년) 동안 4.35%의 CAGR로 성장할 전망입니다.

팬데믹 기간 동안 COVID-19는 무선 심전도 기기 산업에 큰 영향을 미쳤습니다. 2021년 1월 유럽 심장 저널에 발표된 논문에 따르면, 입원하지 않은 COVID-19 환자를 대상으로 스마트폰으로 가정에서 ECG를 모니터링한 결과 질병 관련 심장 합병증과 ECG 변화의 존재를 파악할 수 있었습니다. 또한 COVID-19 팬데믹 초기에는 엄격한 봉쇄 규정으로 인해 원격 의료 및 가상 솔루션에 대한 수요가 증가했습니다. 팬데믹 기간 동안 심장 치료 시설에 대한 환자의 접근이 제한되었기 때문에 이러한 원격 모니터링 시스템은 전 세계적으로 큰 인기를 끌었습니다. 따라서 COVID-19는 무선 심전도 기기 시장에 큰 영향을 미쳤습니다. 또한 팬데믹 이후에도 무선 심전도 기기에 대한 수요는 그대로 유지될 것으로 예상됩니다.

무선 심전도 기기 시장의 성장을 이끄는 주요 요인으로는 노인 인구 증가, 심혈관 질환 발병률 증가, 원격 모니터링 기술의 발전 등이 있습니다. 예를 들어, 2022년 1월에 발표된 영국 심장 재단(BHF) 데이터에 따르면 2021년에 전 세계적으로 가장 흔한 심장 질환은 관상동맥(허혈성) 심장 질환(전 세계 유병률 2억 명 추정), 말초 동맥(혈관) 질환(1억 1천만 명), 뇌졸중(1억 명), 심방세동(6천만 명)이었다고 보고했습니다. 이 보고서는 또한 북미의 심장 및 순환기 질환 유병률은 4,600만 명, 유럽은 9,900만 명, 아프리카는 5,800만 명, 남아메리카는 3,200만 명, 아시아와 호주는 3억 1,000만 명이라고 언급했습니다. 따라서 전 세계 인구의 심혈관 질환자 수가 많을수록 더 정확하고 사용하기 쉬운 무선 심전도 기기에 대한 수요가 늘어날 것으로 보입니다. 이는 시장 성장에 도움이 될 것입니다.

또한, 2022년 UN에서 발표한 보고서에 따르면 전 세계 65세 이상 인구의 비중이 2022년 10%에서 2050년 16%로 증가할 것으로 예상됩니다. 향후 몇 년 동안 심장 질환에 걸릴 가능성이 높은 노년층의 증가도 시장 성장에 도움이 될 것으로 예상됩니다.

또한 주요 업체들이 시장에서의 입지를 확대하기 위해 다양한 전략을 채택하고 있어 시장 성장을 더욱 촉진할 수 있습니다. 예를 들어, 2022년 1월 Philips는 분산형 임상시험에 사용할 수 있는 12-리드 심전도 솔루션을 출시했습니다. 이 임상 등급 솔루션은 Philips의 심장 모니터링 제품 라인 중 가장 진보된 환자 중심 심전도입니다. 이 솔루션의 데이터 판독값은 임상 환경에서 사용되는 심전도와 유사합니다. 따라서 고령 인구의 증가, 심혈관 질환자 수 증가, 주요 시장 플레이어의 정기적인 신제품 출시가 시장의 성장에 도움이 될 것으로 보입니다.

그러나 심혈관 질환에 대한 복잡한 환급 정책과 정밀 보고의 오류로 인해 시장 성장이 둔화될 가능성이 높습니다.

심혈관 질환의 발생률이 증가하고 노인 인구가 증가함에 따라 지속적인 심혈관 모니터링 ECG 시스템 부문은 예측 기간 동안 성장할 것으로 예상되며, 일상 생활에서 환자의 심장의 지속적인 심혈관 모니터링의 필요성이 높아질 수 있습니다. 예를 들어 2021년 9월 발행된 MDPI 저널의 조사 논문에서는 말초동맥질환(PAD) 세계의 유병률은 3-12%로 추정되고 있으며 미국과 유럽의 약 2,700만명이 이환 하고 있다고 보고되었습니다. 이 정보통은 또한 유럽에서는 PAD의 유병률이 45세와 55세 사이에서 약 17.8%로 추정되고 있다고 보고하고 있습니다. 이러한 심혈관 질환의 유병률의 높이는 지속적인 심혈관 모니터링 ECG 시스템에 대한 수요 증가에 기여할 것으로 예상됨에 따라 이 부문의 성장을 가속합니다.

심혈관 질환의 조기 발견과 관리에 대한 인식이 높아짐에 따라 지속적인 심혈관 심전도 모니터링 장치에 대한 수요가 증가하고 있습니다. 예를 들어, 세계 심장 연맹(WHF)은 매년 9월 29일 세계 심장의 날을 축하합니다. WHF는 2022년 9월 심장 건강에 대한 인식을 높이는 캠페인을 계획하고 있습니다. 매년 90개 이상의 국가가 이 국제 행사에 참여합니다. 그 결과 세계 심장의 날은 심혈관 질환에 대한 정보를 전파하는 효과적인 수단임이 입증되었습니다.

지속적인 심혈관 모니터링 ECG 시스템에 대한 수요 증가에 부응하는 데 필요한 혁신적인 제품 출시도 이 분야의 성장을 가속할 것으로 예상됩니다. 예를 들어, Biotricity는 2022년 4월 미국 FDA의 승인을 받은 무선 웨어러블 심장 모니터링 장치 Biotres를 출시했습니다. 이 제품은 2022년 2월 하순부터 의사, 클리닉, 병원 및 개인 사용자를 위한 선주문을 시작했습니다.

북미는 무선 심전도 기기 시장에서 큰 점유율을 차지하고 있으며 예측 기간 동안 비슷한 경향을 보일 것으로 예상됩니다. 노인 인구 증가와 심혈관 질환의 발생률 증가 등 요인이 조사 대상 지역 시장 성장을 가속하고 있습니다. 예를 들어, 2022년 심장병 및 뇌졸중 통계 최신 사실 시트에 따르면 미국에서는 약 40초마다 한 명이 심근 경색을 일으킬 것으로 예상됩니다. 마찬가지로 2021년 9월에 업데이트된 CDC는 미국의 40세 이상 약 650만 명이 말초 동맥 질환을 앓고 있다고 보고했습니다. 또한 캐나다 심장뇌졸중재단의 2022년 2월 보고서에 따르면 국내에서는 75만명이 심부전을 갖고 있으며 매년 10만명이 심부전으로 진단되고 있습니다.

또한 주요 기업의 존재와 빈번한 제품 승인, 출시 및 개발이 이 지역 시장 성장에 기여할 것으로 예상됩니다. 예를 들어, 2022년 10월에 QT Medical은 소아 환자에게 사용되는 12유도 심전도 PCA 500에 대한 FDA 인가를 취득했습니다. 이 승인은 신생아, 유아, 소아, 청소년을 포함한 모든 소아 집단에 대한 사용 적응을 확대했습니다.

따라서 노인 인구 증가와 심혈관 질환의 발생률 증가 등 위의 요인, 주요 제품의 출시가이 지역 시장 성장에 기여할 것으로 예상됩니다.

무선 심전도 기기 시장은 시장에 소수의 대기업과 소규모 기업이 있기 때문에 적당히 통합된 시장입니다. 시장 관계자는 시장을 위해 기술적으로 첨단 제품을 개발하기 위한 연구 개발에 주력하고 있습니다. 주요 시장 기업은 Nihon Kohden Corporation, Medtronic, General Electric Company (GE Healthcare), Aerotel Medical Systems, AliveCor Inc., 등입니다.

The Wireless ECG Devices Market size is estimated at USD 1.84 billion in 2024, and is expected to reach USD 2.27 billion by 2029, growing at a CAGR of 4.35% during the forecast period (2024-2029).

Over the pandemic period, COVID-19 had a significant impact on the wireless ECG device industry. As per the article published by the European Heart Journal in January 2021, home ECG monitoring with the help of smartphones in non-hospitalized COVID-19 patients was able to identify disease-related cardiac complications and the presence of ECG alterations. Moreover, the COVID-19 pandemic increased the demand for telehealth and virtual solutions due to the strict lockdown regulations imposed at the initial stages of the pandemic. Since there was limited patient access to cardiac care facilities during the pandemic, these remote monitoring systems were immensely popular across the world. Hence, COVID-19 had a significant impact on the wireless ECG device market. In addition, the demand for wireless ECG devices is expected to remain intact during the post-pandemic period.

The major factors driving the growth of the wireless ECG devices market include the growing geriatric population, the increasing incidence of cardiovascular diseases, and technological advancements in remote monitoring technologies. For instance, the British Heart Foundation (BHF) data published in January 2022 reported that in 2021, the most common heart conditions affected globally were coronary (ischemic) heart disease (global prevalence estimated at 200 million), peripheral arterial (vascular) disease (110 million), stroke (100 million), and atrial fibrillation (60 million). The report also mentioned that the prevalence of heart and circulatory diseases in North America was 46 million, in Europe it was 99 million, in Africa it was 58 million, in South America it was 32 million, and in Asia and Australia it was 310 million. Thus, the high number of cardiovascular diseases in the world's population is likely to increase the demand for wireless ECG devices because they are more accurate and easier to use. This will help the market grow.

Additionally, the report published by the UN in 2022 mentioned that the share of the global population aged 65 years or older is projected to rise from 10% in 2022 to 16% in 2050. Over the next few years, the growth of the market is also expected to be helped by the growing number of older people who are more likely to get heart diseases.

Furthermore, major players are adopting various strategies to grow their presence in the market, which may further fuel market growth. For instance, in January 2022, Philips launched the 12-lead electrocardiogram solution for use in decentralized clinical trials. The clinical-grade solution is the most advanced patient-centered ECG in the company's line of cardiac monitoring products. Its data readings are similar to those of ECGs used in clinical settings. Thus, the growth of the market is likely to be helped by the growing number of older people, the high number of people with cardiovascular diseases, and the regular release of new products by key market players.

But the growth of the market is likely to be slowed by complicated reimbursement policies for cardiovascular diseases and errors in precision reporting.

The continuous cardiovascular monitoring ECG systems segment is expected to grow over the forecast period, due to the increasing incidence of cardiovascular diseases and a growing geriatric population, which is likely to increase the need for continuous cardiovascular monitoring of patients' hearts during their daily routines. For instance, the MDPI Journal research article published in September 2021 reported that the worldwide prevalence of peripheral arterial disease (PAD) is estimated to be 3-12%, affecting nearly 27 million people in America and Europe. The same source also reported that in Europe, the prevalence of PAD is estimated at around 17.8% between the ages of 45 and 55. Such a high prevalence of cardiovascular diseases is expected to contribute to the growing demand for continuous cardiovascular monitoring ECG systems, thereby fueling segment growth.

Increasing awareness regarding the early detection and management of cardiovascular diseases is augmenting the demand for continuous cardiovascular ECG monitoring devices. For instance, the World Heart Federation (WHF) celebrates World Heart Day on September 29 every year. WHF has planned a campaign to raise awareness of heart health in September 2022.Over 90 countries take part in this international observance every year. As a result, World Heart Day has proven to be an effective means for disseminating information about cardiovascular disorders.

The innovative product launches necessary to meet the growing demand for continuous cardiovascular monitoring ECG systems are also expected to boost segment growth. For instance, in April 2022, Biotricity launched its US FDA-cleared, wireless wearable cardiac monitoring device, Biotres. The product was available for pre-order to physicians, medical offices, hospitals, and individual users as of late February 2022.

North America holds a major share of the wireless ECG devices market, and it is expected to show a similar trend over the forecast period. Factors such as the growing geriatric population and increasing incidence of cardiovascular diseases fuel the market growth in the studied region. For instance, as per the 2022 Heart Disease and Stroke Statistics Update Fact Sheet, approximately every 40 seconds, a person in the United States is anticipated to have a myocardial infarction. Likewise, the CDC updated in September 2021 reported that approximately 6.5 million people aged 40 and older in the United States have peripheral arterial disease. Also, as per the February 2022 report from the Heart and Stroke Foundation of Canada, 750,000 people are living with heart failure, and 100,000 people are diagnosed with heart failure each year in the country.

Furthermore, the presence of key players and frequent product approvals, launches, and developments are expected to contribute to the growth of the market in this region. For instance, in October 2022, QT Medical received FDA clearance for PCA 500, aresting 12-lead electrocardiogram for use in pediatric patients. This clearance expanded its indication for use to all pediatric populations, including newborns, infants, children and adolescents.

Therefore, the above mentioned factors such as growing geriatric population and increasing incidence of cardiovascular diseases, key product launches are expected to contribute to the growth of the market in this region.

The wireless ECG devices market is a moderately consolidated market, owing to the presence of a few major players and smaller players in the market. The market players are focusing on R&D to develop technologically advanced products for the market. The major market players are Nihon Kohden Corporation, Medtronic, General Electric Company (GE Healthcare), Aerotel Medical Systems, and AliveCor Inc., among others.