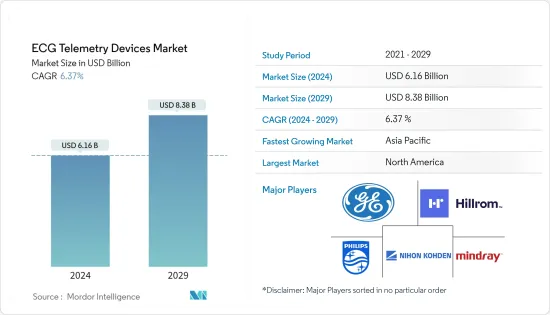

심전도(ECG) 원격 측정 장치(ECG Telemetry Devices) 시장 규모는 2024년에 61억 6,000만 달러로 추정되고, 2029년까지 83억 8,000만 달러에 이를 것으로 예측되고 있으며, 예측 기간(2024-2029년) 중 6.37%의 CAGR로 성장할 전망입니다.

COVID-19 팬데믹은 시장 성장에 큰 영향을 미쳤습니다. COVID-19 팬데믹이 시작되면서 전국적으로 봉쇄령이 내려지고 긴급하지 않은 방문과 입원이 중단되면서 심장 질환 환자의 진단이 지연되는 결과를 초래했습니다. 예를 들어, 2022년 2월 Nature Medicine에 발표된 논문에 따르면 COVID-19 환자는 심부전, 혈전색전성 질환, 부정맥, 심낭염, 심근염, 허혈성 및 비허혈성 심장 질환과 같은 심혈관 질환에 걸릴 가능성이 더 높다는 사실이 관찰된 바 있습니다. 따라서 CVD 관련 질병의 높은 부담으로 인해 팬데믹 기간 동안 ECG 원격 측정, 웨어러블 및 환자 모니터링 기기에 대한 수요가 증가했습니다. 또한 2021년 8월 PLOS One에 발표된 논문에 따르면 심혈관 질환의 조정된 발생률 비율이 COVID-19 이전 기간에 비해 COVID-19 이후 노출 기간에 훨씬 더 높은 것으로 나타났습니다. 이로 인해 심장마비 위험을 줄이기 위해 심장 상태를 정기적으로 모니터링하는 기기에 대한 수요가 증가하고 있습니다. 또한 COVID-19 제한 완화, 심장 서비스 재개, 환자 방문 증가로 인해 연구 대상 시장은 예측 기간 동안 성장할 것으로 예상됩니다.

심혈관 질환의 유병률 증가, 노인 인구 증가, 원격 모니터링 기술의 기술 발전과 같은 요인이 시장 성장을 촉진하고 있습니다. 예를 들어, BHF의 2022년 보고서에 따르면 2021년 영국에서는 760만 명 이상의 사람들이 심혈관 질환을 앓고 있었습니다. 따라서 심혈관 질환과 그 높은 유병률은 심장 상태를 정기적으로 모니터링하려는 수요를 증가시켜 시장 성장을 촉진할 것으로 예상됩니다.

또한 호주 통계청의 2022년 3월 업데이트에 따르면 호주의 심장병 유병률은 2020-2021년 4.0%로 약 100만 명에 달합니다. 또한 같은 자료에 따르면 호주에서 심장병은 45-54세 인구의 2.3%에서 75세 이상 인구의 23.2%로 연령이 높아질수록 증가했으며, 남성이 호주에서 가장 많은 영향을 받고 있는 것으로 나타났습니다. 따라서 노인 인구의 증가와 함께 CVD의 부담 증가는 예측 기간 동안 시장 성장의 주요 원동력이 될 것으로 예상됩니다.

또한 인구 중 비만, 당뇨병, 고혈압, 고콜레스테롤혈증의 유병률이 증가하는 것도 시장 성장에 기여하고 있습니다. 예를 들어, OECD가 발표한 2021년 데이터에 따르면 2030년까지 미국 인구의 약 47%, 멕시코의 39%, 캐나다의 35%가 비만을 겪을 것으로 예상됩니다. 또한 IDF가 발표한 2022년 통계에 따르면 전 세계적으로 20-79세 성인 약 5억 3700만 명이 당뇨병을 앓고 있으며, 2030년과 2045년에는 각각 6억 4300만 명, 7억 8300만 명으로 늘어날 것으로 예상됩니다. 당뇨병으로 인한 고혈당은 심장과 혈관을 조절하는 신경을 손상시켜 동맥이 좁아지는 관상동맥질환, 뇌졸중 등 다양한 심혈관 질환을 유발할 수 있습니다. 이는 심장 이벤트 모니터링 및 기타 원격 측정 기기에 대한 수요를 증가시켜 시장 성장을 촉진할 것으로 예상됩니다.

또한 원격 모니터링 기술의 기술 발전으로 인해 원격 측정 및 원격 환자 모니터링 장치를 제조하는 기업에게 기회가 창출되고 있습니다. 이는 시장에서의 제품 가용성을 증가시켜 시장 성장을 촉진할 것으로 예상됩니다. 예를 들어, 2022년 1월 로열 필립스는 분산형 임상시험에 사용할 수 있는 최초의 가정용 12-리드 심전도(ECG) 솔루션을 출시했습니다. 또한 2021년 7월, 애보트는 미국에서 이식형 심장 모니터(ICM)인 Jot Dx를 출시했습니다. 이 기술을 통해 환자의 심장 부정맥을 원격으로 감지하고 진단 정확도를 개선할 수 있습니다.

따라서 위에서 언급 한 요인으로 인해 연구 된 시장은 예측 기간 동안 성장할 것으로 예상됩니다. 그러나 장치의 높은 비용과 여러 국가의 복잡한 환급 정책은 예측 기간 동안 시장의 성장을 방해 할 것으로 예상됩니다.

이식형 루프 레코더 부문은 심장 질환의 유병률 증가, 심장 모니터링 장치의 최근 기술 진보, 원격 환자 모니터링 수요 증가 등 요인으로 인해 예측 기간 동안 심전도(ECG) 원격 측정 장치 시장에서 큰 성장이 예상될 것으로 예상됩니다. 이식형 루프 레코더(ILP)는 심장 이벤트 레코더라고도 하며, 심장 리듬을 최장 3년 동안 지속적으로 기록하는 심장 감시 장치의 일종입니다. 또한 의사가 원격에서 심박수를 모니터링 할 수 있습니다. 2021년 12월 Cardiovascular Diagnosis and Therapy(CDT)에 게재된 논문에 따르면, ILP는 생명을 위협하는 심장병의 위험이 있는 증후성 CHD 환자의 양성 및 악성 부정맥의 확인 및 분류에 중요한 보조 진단 가치를 제공하는 것이 관찰되었습니다. 이벤트. 또한, 동일한 출처에 따르면, 특히 단기 홀터 모니터링은 충분한 진단 확실성을 얻지 못하는 경우 중기 또는 장기 부정맥 모니터링이 필요한 어떤 복잡한 CHD 환자에서 ILR 이식을 고려해야합니다. 입니다. 이는 광범위한 심혈관 질환으로 고통받는 환자에게 이식 가능한 루프 레코더의 채택을 증가시키고 이 부문의 성장을 가속할 것으로 예상됩니다.

게다가 새로운 상환정책 도입으로 인한 환자간의 원격환자 모니터링(RPM) 채택 증가와 제휴, 인수 등 다양한 비즈니스 전략 채택 증가도 ILP 수요를 증가시킬 것으로 예상됩니다. 예를 들어 2021년 1월 CMS는 2021년 의사 요금표를 수정하여 원격 환자 모니터링(RPM)의 상환 기준을 인상했습니다. 이는 심장 모니터링에 RPM이 널리 채택되어 이식형 루프 레코더에 대한 수요가 증가하고 있음을 보여줍니다. 또한 AHA에 따르면 최근 임상 지침은 뇌졸중 환자와 비 뇌졸중 환자 모두에서 심방 세동 검출을 위한 원격 환자 모니터링을 사용하는 것이 좋습니다. 증가하고 시장 성장을 가속하고 있습니다. 또한 2021년 1월 Boston Scientific은 Preventice Solutions를 9억 2,500만 달러로 인수했습니다. 이 인수로 보스턴은 핵심 심장 리듬 관리 및 전기 생리학 사업 부문을 확대했습니다. 따라서 위의 요인으로 인해 조사 대상 부문이 예측 기간 동안 성장할 것으로 예상됩니다.

예측 기간 동안 북미가 시장을 독점할 것으로 예상됩니다. 시장 성장의 요인으로는 국민의 심장혈관 부담 증가, 상환정책에 따른 고액의 의료비, 이 지역의 심전도(ECG) 원격 측정 장치 수요와 채택 증가 등이 있습니다.

심혈관 질환의 유병률 증가는 이 지역의 ECG 원격 측정 장치 수요를 촉진하는 주요 요인입니다. 예를 들어 AHA가 2021년 6월에 발표한 통계에 따르면 2021년 캐나다 심부전 유병률은 1.5%에서 1.9%였습니다. 같은 출처에 따르면, 추정에서 캐나다 성인은 1억 3,000만 명 이상입니다. 미국에서는 2035년까지 어떤 심장병이 발생할 것으로 예상됩니다. 또한 CDC가 발표한 2022년 데이터에 따르면 심장병은 미국의 주요 사망 원인이며 미국에서는 매년 약 805,000명이 사망하고 있습니다. 심장 발작을 일으키고 있습니다. 따라서 인구의 심부전 사례 수가 많으면 심방 세동이나 부정맥의 위험이 높아지므로 심장에 대한 추가 위험을 방지하기 위해 심박수와 산소 포화도를 정기적으로 모니터링해야하므로 ECG 원격 측정 장비 수요가 증가하고 있습니다. 게다가 2021년 7월에 International Journal of Stroke에 게재된 조사 결과에 따르면, 미국에서는 2050년까지 약 600만명에서 1,200만명이, 2060년까지 1,790만명이 심방세동에 시달리면 예상됩니다., 심혈관 관련 건강 문제로 인한 국민 부담 증가가 예상되고 있어 환자 파라미터 감시 장치 뿐만 아니라 정기적인 심장 감시 수요도 높아질 것으로 예상됩니다. 이것은 예측 기간 동안 시장의 성장을 가속할 것으로 예상됩니다.

게다가 환자감시장치의 기술진보와 심혈관질환 환자를 지원하는 제품을 개발·발매하고 있는 지역의 주요 기업의 존재에 의해 예측기간 중 시장의 성장이 확대될 것으로 예상됩니다. 예를 들어, 2021년 7월, 애봇은 삽입 가능한 심장 모니터(ICM)인 Jot Dx를 미국에서 출시했습니다. 이것은 환자의 부정맥의 원격 검출과 진단 정확도를 향상시킬 수 있습니다. 또한 Jot Dx는 환자가 ICM에 연결하고 연결을 유지할 수 있도록 일대일 교육 및 안내를 제공하는 개인화된 서비스인 SyncUP에서 지원합니다. 마찬가지로 2021년 7월 미국 식품의약국은 메드트로닉의 2개의 AccuRhythm 인공지능(AI) 알고리즘을 LINQ II 이식형 심장 모니터(ICM)에 사용하도록 승인했습니다. 따라서 위의 요인으로 인해 조사 대상 시장은 예측 기간 동안 성장할 것으로 예상됩니다.

심전도(ECG) 원격 측정 장치 시장은 본질적으로 세분화되어 있으며 여러 기업이 시장에서 좋은 성적을 거두고 있습니다. 그러나 일부 기업은 이 시장에 가장 기여하며 특정 지역을 지배하고 있습니다. 제품 개발에 대한 관심 증가와 건강 관리에서 기술 활용 증가로 인해 향후 더 많은 중소기업이 시장에 진입할 것으로 예상됩니다.

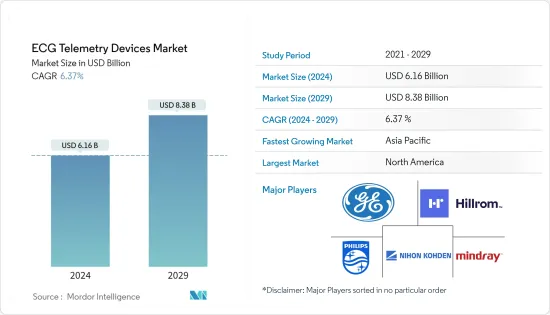

The ECG Telemetry Devices Market size is estimated at USD 6.16 billion in 2024, and is expected to reach USD 8.38 billion by 2029, growing at a CAGR of 6.37% during the forecast period (2024-2029).

The COVID-19 pandemic has significantly impacted market growth. The onset of the COVID-19 pandemic caused a nationwide lockdown with the suspension of non-urgent scheduled visits and hospitalizations, which resulted in the delayed diagnosis of patients with cardiac disorders. For instance, from an article published in Nature Medicine in February 2022, it has been observed that people with COVID-19 are more likely to have cardiovascular diseases such as heart failure, thromboembolic diseases, dysrhythmias, pericarditis, myocarditis, and ischemic and non-ischemic heart disease. Thus, the high burden of CVD-related diseases raised the demand for ECG telemetry, wearables, and patient monitoring devices during the pandemic. Moreover, an article published in PLOS One in August 2021 showed that the adjusted incident rate ratios for cardiovascular outcomes were considerably greater in the post-COVID-19 exposure period as compared to the pre-COVID-19 period. This raises the demand for devices that regularly monitors heart conditions to reduce the risk of a heart attack. Also, with the relaxed COVID-19 restrictions, resumed cardiac services, and increased patient visits, the studied market is expected to grow over the forecast period.

Factors such as the increasing prevalence of cardiovascular diseases, the growing geriatric population, and technological advancements in remote monitoring technologies are boosting market growth. For instance, as per BHF's 2022 report, more than 7.6 million people were living with cardiovascular diseases in the United Kingdom in 2021. Hence, cardiovascular diseases and their high prevalence is expected to increase the demand for regular monitoring of heart condition, propelling market growth.

Additionally, according to the March 2022 update of the Australian Bureau of Statistics, the prevalence of heart disease in Australia was 4.0% in 2020-2021, which equates to about 1 million people. Also, as per the same source, in Australia, heart disease increased with age, from 2.3% of people aged 45-54 years through to 23.2% of people aged 75 years and over, with males being the most affected by it in the country. Hence, the rising burden of CVDs, coupled with the increasing geriatric population, is expected to be the major driving factor for the growth of the market over the forecast period.

Furthermore, the increasing prevalence of obesity, diabetes, hypertension, and high cholesterol among the population is contributing to market growth. For instance, according to the 2021 data published by the OECD, about 47% of the population in the United States, 39% in Mexico, and 35% in Canada are expected to suffer from obesity by 2030. Also, according to the 2022 statistics published by IDF, about 537 million adults aged between 20-79 years were living with diabetes globally, and this number is projected to increase to 643 million and 783 million by 2030 and 2045, respectively. Therefore, high blood sugar caused by diabetes can damage the nerves that control the heart and blood vessels, leading to a variety of cardiovascular diseases like coronary artery disease and stroke, which can narrow the arteries. This is further expected to increase the demand for cardiac event monitoring and other telemetry devices, hence boosting market growth.

Moreover, the growing technological advancements in remote monitoring technologies are creating opportunities for companies to manufacture telemetry and remote patient monitoring devices. This increases the availability of products in the market, which is anticipated to fuel market growth. For instance, in January 2022, Royal Phillips introduced the first at-home 12-lead electrocardiogram (ECG) solution for use in decentralized clinical trials. Also, in July 2021, Abbott launched Jot Dx, an insertable cardiac monitor (ICM), in the United States. This technology allows for remote detection and improved diagnostic accuracy of cardiac arrhythmia in patients.

Therefore, owing to the above-mentioned factors, the studied market is expected to grow over the forecast period. However, the high cost of the devices and complex reimbursement policies in various countries are expected to impede the growth of the market over the forecast period.

The implantable loop recorder segment is expected to witness significant growth in the ECG telemetry devices market over the forecast period owing to factors such as the growing prevalence of cardiac disorders, recent technological advancements in cardiac monitoring devices, and increasing demand for remote patient monitoring. An implantable loop recorder (ILP), also called a cardiac event recorder, is a type of heart-monitoring device that constantly records the heart rhythm for up to three years. It also allows doctors to remotely monitor the heartbeat. According to an article published in Cardiovascular Diagnosis and Therapy (CDT) in December 2021, it has been observed that ILP offers a significant supplemental diagnostic value for the identification and classification of benign and malignant arrhythmias in symptomatic CHD patients at risk of life-threatening cardiac events. Also, as per the same source, ILR implantation should be considered in patients with CHD of any complexity who need medium or long-term arrhythmia monitoring, especially if short-term Holter monitoring is unable to provide adequate diagnostic certainty. This is anticipated to increase the adoption of implantable loop recorders in patients suffering from a wide range of cardiovascular diseases, hence bolstering the segment's growth.

Furthermore, the increasing adoption of remote patient monitoring (RPM) among patients due to the introduction of new reimbursement policies and the rising adoption of various business strategies such as collaborations, acquisitions, and others are also expected to increase the demand for ILP, hence boosting market growth. For instance, in January 2021, the CMS amended the 2021 Physician Fee Schedule to increase the reimbursement criteria for remote patient monitoring (RPM). This indicates wider adoption of RPM for cardiac monitoring, thereby increasing the demand for implantable loop recorders. Also, as per the AHA, recent clinical guidelines strongly recommend the use of remote patient monitoring for atrial fibrillation detection in both stroke and non-stroke patients, thereby further increasing the demand for implantable loop recorders, hence boosting the market growth. Moreover, in January 2021, Boston Scientific acquired Preventice Solutions for USD 925 million. With this acquisition, Boston expanded its business segment of core cardiac rhythm management and electrophysiology. Therefore, owing to the abovementioned factors, the studied segment is expected to grow over the forecast period.

North America is expected to dominate the market over the forecast period. The factors attributed to the market's growth are the rising cardiovascular burden among the population, high healthcare expenditure along with reimbursement policies, and rising demand and adoption for ECG telemetry devices in the region.

The increasing prevalence of cardiovascular diseases is the key factor driving the demand for ECG telemetry devices in the region. For instance, according to the statistics published by the AHA in June 2021, the prevalence rate of heart failure in Canada was between 1.5% to 1.9% in 2021. As per the same source, in an estimate, more than 130 million adults in the United States are expected to have some type of heart disease by 2035. Also, according to the 2022 data published by the CDC, heart disease is the leading cause of death in the United States, and every year, about 805,000 people in the United States have a heart attack. Thus, the high number of heart failure cases among the population increases the risk of atrial fibrillation and cardiac arrhythmias, which requires regular monitoring of the heart rate and oxygen saturation to prevent further risk to the heart, hence propelling the demand for ECG telemetry devices. Additionally, as per a research study published in the International Journal of Stroke in July 2021, it has been observed that about 6-12 million people in the United States are expected to suffer from atrial fibrillation by 2050 and 17.9 million people by 2060. Thus, the expected increase in the burden of cardiovascular-related health problems among the population is anticipated to fuel the demand for regular heart monitoring as well as a patient-parameters monitoring device. This is expected to propel the market's growth over the forecast period.

Furthermore, the technological advancements in patient monitoring devices, as well as the presence of key players in the region that are developing and launching products for helping patients with cardiovascular diseases, are expected to augment the market's growth over the forecast period. For instance, in July 2021, Abbott launched Jot Dx, an insertable cardiac monitor (ICM), in the United States. It allows remote detection and improved diagnostic accuracy of cardiac arrhythmia in patients. Also, Jot Dx is supported by SyncUP, a personalized service that offers one-on-one training and instruction to help patients become connected and stay connected to their ICM. Similarly, in July 2021, the US Food and Drug Administration approved Medtronic's two AccuRhythm artificial intelligence (AI) algorithms for use with the LINQ II insertable cardiac monitor (ICM). Therefore, owing to the abovementioned factors, the studied market is expected to grow over the forecast period.

The ECG telemetry devices market is fragmented in nature, and multiple companies are performing well in the market. However, some of the companies are contributing the most to this market and dominating certain geographies. With the rising focus on product development and the increasing usage of technology in healthcare, more small and mid-sized companies are expected to enter the market in the future. Some of the companies that are currently dominating the market are Aerotel Medical Systems Ltd, BioTelemetry Inc., GE Healthcare (GE Company), Medtronic Inc., iRhythm Technologies Inc., Nihon Kohden Corporation, Philips Healthcare, Medicalgorithmics SA, Preventice Solutions Inc., and Hill-Rom Services Inc. (Welch Allyn).