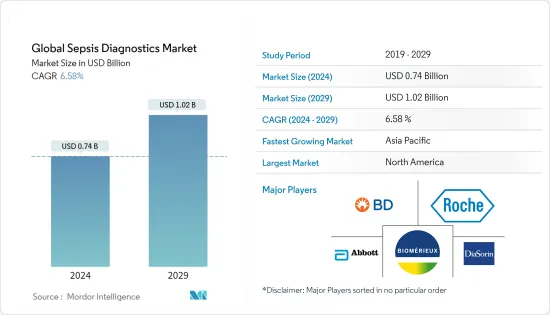

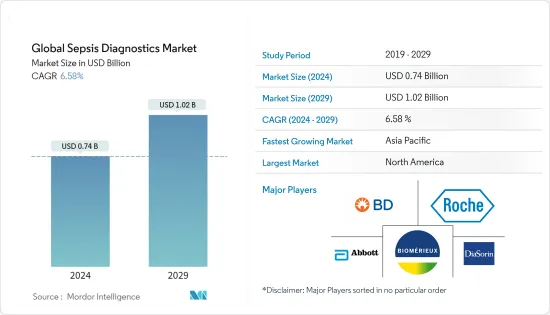

세계의 패혈증 진단 시장 규모는 2024년에 7억 4,000만 달러로 추정되며, 2029년까지 10억 2,000만 달러에 달할 것으로 예측되고 있으며, 예측 기간(2024-2029년) 중 6.58%의 CAGR로 성장합니다.

COVID-19 감염 환자의 패혈증 발생률 증가는 조사 대상 시장에 긍정적인 영향을 미칠 것으로 예상됩니다. 예를 들어 질병통제예방센터(CDC)가 2021년 발표한 '2020년 국가 및 주 의료 관련 감염 진행 보고서'에 따르면 2020년 급성기 병원의 표준화된 감염률을 분석한 결과 급성기 병원의 감염률이 크게 증가한 것으로 나타났습니다. 중심정맥관 관련 혈류감염, 카테터 관련 요로감염, 인공호흡기 관련 사건, 메티실린 내성 황색포도상구균 혈증이 2019년에 비해 증가하였습니다. 가장 큰 증가는 2020년 4분기에 발생했습니다. 또한 PLOS가 2019년8월에 발표 한 연구에 따르면 2021년8월"면역 대사 시그니처는 COVID-19 감염에서 패혈증으로의 진행 위험을 예측한다"는 연구에 따르면 COVID-19 환자는 패혈증 발병 위험이 가장 높습니다. 따라서 이는 조사 대상 시장에서 새로운 진단을 위한 새로운 기회를 창출할 것으로 기대됩니다.

패혈증 진단 시장 성장의 주요 요인으로는 패혈증 부담 증가, 병원내 감염 부담 증가, 폐렴 환자 수 증가, 패혈증 치료 건수 증가, 패혈증에 대한 자금 증가 등이 있습니다. 관련 연구 활동. 병원내 감염(HAI)은 입원 환자들 사이에서 가장 흔한 합병증입니다. 예를 들어 질병 통제 예방 센터(CDC)가 2021년에 발표 한 보고서 "2020년국가 및 주 의료 관련 감염 진행 보고서"에 따르면 중심선은 약 24%, 35%, 15% 증가했습니다. 2019 -2020년까지 미국의 혈류 감염, 인공호흡기 관련 사건, 메티 실린 내성 황색 포도상 구균(MRSA) 균혈증. 혈류 감염 증가는 패혈증 진단 제품의 채택을 증가시킬 것입니다. 또한 2021년 6월, 리버풀 대학이 주도하는 공동 연구는 모성 패혈증을 적극적으로 예방, 치료 및 평가하기 위한 새로운 개입을 위해 300만 파운드 이상의 자금을 지원받았습니다.

따라서 패혈증 유병률 증가와 패혈증 진단을 위한 연구 활동에 대한 자금 지원 증가는 예측 기간 중 전체 패혈증 진단 시장의 성장을 가속할 것으로 예상됩니다.

패혈증은 병원의 많은 환자들에게 영향을 미치며, 6번째로 많은 입원 원인으로 꼽힙니다. 감염을 일으키는 병원균을 신속하고 정확하게 프로파일링하는 것은 현대 의료에서 여전히 큰 도전 과제입니다. 또한 원인 병원체의 식별은 치료의 일환으로 적절한 항생제 요법을 선택하는 데 필수적입니다. 이러한 요구사항으로 인해 분자진단(MDx)은 패혈증 진단에 있으며, 매력적인 접근법이 되고 있습니다.

분자진단은 쉬운 실현 가능성과 검출 방법의 정확성으로 인해 여러 다국적 기업과 기관을 매료시키고 있습니다. 감염성 질환의 신속하고 정확한 프로파일링을 위한 혈액 배양 분석은 분자진단 방법의 황금 표준입니다. 그러나 분자진단의 비용은 여전히 기존 방법에 비해 매우 높기 때문에 시장 성장을 제한하고 있습니다. 일부 기업은 세균 및 바이러스성 병원균의 조기 진단과 환자 관리를 개선하기 위해 현장 분자진단에 투자하고 있습니다. 예를 들어 2020년 10월 Immunexpress는 유럽에서 Biocartis의 Idylla 플랫폼에서 패혈증에 대한 1시간 분자진단 테스트인 Rapid SeptiCyte를 출시했습니다. 이는 임상의의 패혈증 진단을 지원하기 위해 면역 반응에 기반한 최초의 완전 통합형 신속 검사 중 하나입니다.

연구진은 또한 COVID-19와 패혈증을 감지하고 구별할 수 있는 분자진단법을 개발하기 위해 노력하고 있습니다. 2020년 11월, 그리스 패혈증 연구소와 Sanmina Corporation의 일부가 연구 자금을 지원하여 패혈증과 중증 COVID-19의 조기 진단을 위한 새로운 광학 바이오센서를 개발했습니다. 이러한 발전은이 부문의 성장에 긍정적인 영향을 미칠 것으로 예상됩니다.

북미는 패혈증 진단 시장에서 큰 비중을 차지하는 것으로 나타났으며, 예측 기간 중 큰 변동 없이 비슷한 추세를 보일 것으로 예상됩니다. 미국 질병예방통제센터(CDC)에 따르면 2021년 8월 기준 미국 성인 약 170만 명이 패혈증에 걸렸으며, 약 27만 명의 미국인이 패혈증으로 사망했습니다. 또한 병원에서 사망하는 환자 3명 중 1명은 패혈증으로 사망하는 것으로 나타났습니다. 따라서 미국내 이 질병의 높은 발병률은 진단을 증가시키고 시장을 촉진할 것입니다.

또한 패혈증 진단을 위한 연구개발 분야에 대한 투자 증가도 시장을 촉진할 것으로 보입니다. 예를 들어 2020년 4월 Cytovale Inc.는 COVID-19를 포함한 잠재적 호흡기 감염 환자의 패혈증 진단을 위해 생물 의학 첨단 연구 및 개발 개발국(BARDA)과 COVID-19를 확대했습니다. 이 연구에는 590만 달러의 비용이 소요될 것으로 추정되며, 그 중 약 3.83 달러는 생물 의학 첨단 연구개발 개발국(BARDA)에서 기부하여 시장을 주도하고 있습니다.

따라서 패혈증 유병률 증가와 패혈증 진단 연구개발에 대한 투자 증가는 미국 시장의 성장을 가속할 수 있습니다.

패혈증 진단 시장은 소수의 주요 기업이 존재하여 어느 정도 통합되어 있습니다. 시장의 주요 기업이 출시한 제품과 주요 기업의 패혈증 진단에 대한 연구 구상이 증가함에 따라 시장이 성장할 것으로 예상됩니다. 시장 진출기업으로는 Abbott, Becton, Dickinson and Company, bioMerieux SA, Bruker Corporation, F. Hoffmann-LA Roche Ltd, Immunexpress Inc. 등이 있습니다.

The Global Sepsis Diagnostics Market size is estimated at USD 0.74 billion in 2024, and is expected to reach USD 1.02 billion by 2029, growing at a CAGR of 6.58% during the forecast period (2024-2029).

Increasing incidences of sepsis in COVID-19 patients is anticipated to have a positive impact on the market studied. For instance, according to a report published by the Centers for Disease Control and Prevention (CDC) in 2021, '2020 National and State Healthcare-Associated Infections Progress Report', the analysis of the 2020 acute care hospitals standardized infection ratios found significant increases in central line-associated bloodstream infections, catheter-associated urinary tract infections, ventilator-associated events, and methicillin-resistant Staphylococcus aureus bacteremia compared to 2019. The largest increases occurred during quarter 4 of 2020. Furthermore, according to a study published by PLOS in August 2021, 'Immunometabolic signatures predict the risk of progression to sepsis in COVID-19,' COVID-19 patients are at the highest risk of developing sepsis. Hence, this is expected to create new opportunities for novel diagnosis in the market studied.

The major factors for the growth of the sepsis diagnostics market include the increasing burden of sepsis, the growing burden of hospital-acquired infections, the increasing number of pneumonia cases, the rise in the number of sepsis procedures, and an increase in funding for sepsis-related research activities. Hospital-acquired infections (HAIs) are the most common complications among hospitalized patients. For instance, according to a report published by the Centers for Disease Control and Prevention (CDC) in 2021, '2020 National and State Healthcare-Associated Infections Progress Report', about 24%, 35%, and 15% increase in central line-associated bloodstream infections, ventilator-associated events, and Methicillin-resistant Staphylococcus Aureus (MRSA) bacteremia between 2019 and 2020 in the United States. The rising bloodstream infections will lead to increased adoption of sepsis diagnostic products. Additionally, in June 2021, the collaboration led by the University of Liverpool has received more than GBP 3 million in funding for a new intervention that will actively prevent, treat and evaluate maternal sepsis.

Thus, the rise in the prevalence of sepsis and increase in funding for research activities for sepsis diagnosis are expected to drive the overall growth of the sepsis diagnosis market over the forecast period.

Sepsis affects significant patient populations in hospitals and is the sixth most common reason for hospitalization. Rapid and accurate profiling of infection-causing pathogens remains a significant challenge in modern healthcare. Moreover, identification of the causative pathogen is essential in selecting appropriate antibiotic therapy as part of the treatment. These requirements make molecular diagnostics (MDx) an attractive approach to consider for sepsis diagnostics.

Molecular diagnostics have attracted several multinational companies and institutions, owing to their easy feasibility and accuracy in detection methods. The blood culture analysis for rapid and accurate profiling of infections has been the gold standard for the molecular diagnostic method. However, the cost of molecular diagnostics has remained very high, as compared to conventional procedures, which restricts its market growth. Several companies are investing in point-of-care molecular diagnostics for the early diagnosis of bacterial and viral pathogens and better patient management. For instance, in October 2020, Immunexpress launched a rapid SeptiCyte, a one-hour molecular diagnostic test for sepsis in Europe on Biocartis' Idylla platform. This is one of the first rapid, fully-integrated, and immune response-based tests to aid clinicians with a sepsis diagnosis.

Furthermore, researchers are attempting to develop a molecular diagnostic that can detect the COVID-19 and sepsis, as well as discriminate between the two. In November 2020, the Hellenic Institute for the Study of Sepsis and, in part by Sanmina Corporation, funded a study and developed a novel optical biosensor for the early diagnosis of sepsis and severe COVID-19. These developments are expected to have a positive impact on the growth of this segment.

North America is found to hold a major share of the sepsis diagnostics market and is expected to show a similar trend over the forecast period, without significant fluctuations. According to the Centers for Disease Control and Prevention, in August 2021, approximately 1.7 million adults in America develop sepsis, and nearly 270,000 Americans die due to sepsis. It was also found that 1 in 3 patients who die in a hospital has sepsis. Thus, the high incidence rate of the disease in the country will boost its diagnosis, thus, boosting the market.

Moreover, rising investments in the fields of research and development for the diagnosis of sepsis will also boost the market. For instance, in April 2020, Cytovale Inc. expanded its partnership with the Biomedical Advanced Research and Development Authority (BARDA) for diagnosing sepsis in patients with potential respiratory infections, including COVID-19. The research is estimated to stand at the cost of USD 5.9 million, with approximately USD 3.83 contributed by the Biomedical Advanced Research and Development Authority (BARDA), thus, driving the market.

Therefore, the rising prevalence of sepsis and increasing investments in the research and development of sepsis diagnosis may augment the growth of the market in the United States.

The sepsis diagnostics market is moderately consolidated owing to the presence of a few key players. The market is expected to drive due to the products launched by the key players in the market and the rise in research initiatives on sepsis diagnostics by the key players. Some of the market players are Abbott, Becton, Dickinson, and Company, bioMerieux SA, Bruker Corporation, F. Hoffmann-LA Roche Ltd, and Immunexpress Inc., among others.