ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

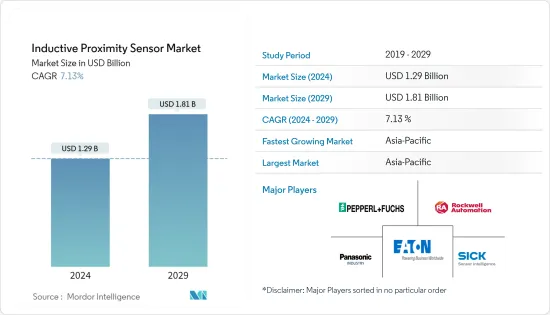

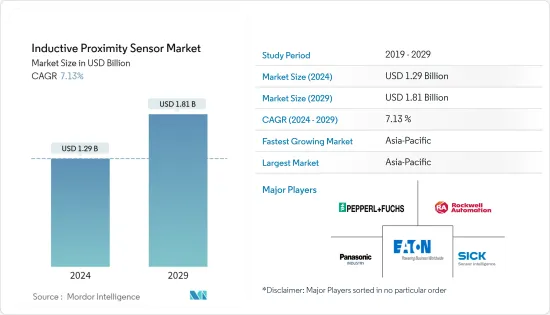

유도형 근접 센서의 시장 규모는 2024년 12억 9,000만 달러로 추정되며, 2029년까지 18억 1,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 7.13%의 CAGR로 성장할 것으로 예상됩니다.

유도형 근접 센서는 코일과 발진기를 사용하여 무선 주파수 필드를 설정하는 비접촉식 장치입니다. 물체의 존재에 따라 이 필드가 변경될 수 있으며, 센서는 이러한 변화를 감지할 수 있습니다. 유도형 근접 센서는 물체를 만지지 않고도 물체를 감지할 수 있기 때문에 물체에 손상을 입히거나 마모되지 않습니다.

주요 하이라이트

근접 센서는 일반적으로 많은 자동화 애플리케이션에 사용됩니다. 물체를 감지하는 데 사용되며 감지되는 대상 또는 물체와의 물리적 접촉이 필요하지 않습니다. 따라서 비접촉식 센서라고 합니다. 일반적인 근접 센서 유형에는 광전 센서, 정전 용량 센서, 유도 센서 등이 있습니다.

유도형 근접 센서는 금속 물체의 비접촉식 감지에 활용됩니다. 이 센서의 작동 원리는 감지 표면 주변에 전자기장을 생성하는 코일과 발진기를 기반으로 합니다. 근접 센서는 소비자 기기에도 탑재되어 있습니다. 스마트폰에서 근접 센서는 사용자가 휴대폰을 얼굴에 가까이 대고 있는지 여부를 감지합니다.

ASIC 기술을 채택한 SICK 센서는 정확도와 신뢰성을 향상시킵니다. SICK는 단일, 이중 또는 삼중 작동 거리를 가진 직사각형 및 원통형 표준 센서부터 폭발성 및 독성 분위기 또는 열악한 환경에서 사용하는 특수 센서에 이르기까지 고객의 요구 사항을 충족하는 적절한 솔루션을 항상 제공할 수 있습니다. 이 회사의 유도형 근접 센서는 산업별 자동화를 수반하는 모든 작업에 맞춤형으로 구현할 수 있는 지능적이고 신뢰할 수 있는 수단입니다.

기존 유도형 근접센서의 경우, 제진소자까지의 거리가 멀어질수록 감지 대상에 대한 센서의 감도가 높아지며, 설치 주변의 금속이 스위칭 거리에 영향을 미칩니다.

이 문제를 해결하기 위해 Pepperl Fuchs는 설치 조건에 관계없이 긴 스위칭 거리를 허용하는 액티브 차폐 기술을 도입했습니다. 회사는 이를 VariKont 시리즈에 처음으로 통합했습니다. 플러시 장착의 경우 30mm, 비 플러시 장착의 경우 50mm의 긴 스위칭 거리를 가진 버전이 제공됩니다.

유도형 근접 센서는 안전 및 재고 관리 애플리케이션과 같은 여러 산업 및 제조 애플리케이션에 사용됩니다. 예를 들어, 자동 생산 라인은 위치 결정, 물체 감지, 계수 및 검사에 사용됩니다. 근접 센서는 일부 산업용 컨베이어 시스템의 부품 감지에도 사용됩니다.

식품 및 음료 산업은 강력한 세정제, 혹독한 온도 및 고압 세척 환경을 견뎌야 하기 때문에 근접 센서를 채택할 수밖에 없습니다. 식품 및 음료 분야에서는 식품 제조 및 강력한 화학제품과 같은 응용 분야가 세척 중에 사용되어 표준 센서가 부식되어 조기에 고장날 수 있습니다. 유도식 근접 센서는 고온 및 고압 세척 공정에 대한 우수한 내성을 갖춘 견고한 설계를 보여줍니다.

유도형 근접 18억 1,000만센서 시장 동향

산업 부문이 큰 시장 점유율을 차지

산업 응용 분야는 점점 더 추적, 모니터링, 측정 및 통신에 의존하고 있습니다. 현대 산업은 효과적인 스마트 제조 환경을 구현하기 위해 다양한 센서 장치가 제어 시스템에 공급하는 정보와 데이터에 크게 의존하고 있으며, 이상적으로는 몇 분의 1의 비용으로 제어 시스템에 공급합니다. 모든 산업용 애플리케이션은 비용 효율적인 센서 구현과 함께 견고성, 높은 IP 보호 등급, 높은 EMC 및 전압 내성, 광범위한 온도 안정성이 요구됩니다.

유도식 근접 센서는 주로 물이나 먼지가 많이 묻을 수 있는 환경과 같이 기존 스위치를 사용할 경우 문제가 발생하거나 사용이 불가능할 수 있는 곳에서 주로 사용됩니다. 대표적인 예로는 식음료 환경의 첨단 CNC 기계와 컨베이어 라인, 그리고 산업 환경의 여러 응용 분야가 있습니다.

대규모 산업에서 유도형 근접 센서 기술의 사용은 수년 동안 대규모 산업에서 사용되어 왔으며, 기술의 향상으로 인해 모든 계층의 기업에서 업무 간소화, 산업 자동화 강화 및 일부 기업의 제조 환경 변화를 위해 모든 계층의 기업에서 널리 채택되고 있습니다. 기업에서 널리 채택되었습니다. 또 다른 성장 요인은 산업 자동화를 가능하게 하는 공급업체의 증가와 산업용 사물인터넷(IIoT) 수요의 성장입니다.

시중에 판매되는 많은 WFI 센서는 동일한 감지 범위에서 여러 금속을 감지합니다. 이러한 센서는 알루미늄과 같은 비철 재료에 대한 감지 거리 감소 계수가 없기 때문에 일반적으로 요인 1 또는 F1 모델이라고합니다. 또한 감지 거리 감소 계수는 1.0입니다(감지 거리 감소 없음).

아시아태평양은 큰 성장을 이룰 것

아시아태평양은 중국, 인도 등 신흥국 덕분에 다른 지역에 비해 상당한 성장률을 보일 것으로 예상됩니다. 또한 오므론(Omron Corporation), 파나소닉(Panasonic Corporation), 오토닉스(Autonics Corporation)와 같은 저명한 업체들이 이 지역에 본사를 두고 있습니다.

자동차 업계 제조업체들은 경량 차량을 생산하고 철보다 알루미늄을 우선시하여 전기자동차(EV) 및 저연비 수요를 충족시키기 위해 노력하고 있습니다. 알루미늄과 철을 모두 포함하는 혼합 생산 라인의 보급이 증가함에 따라 적절한 감지 범위를 가진 동일한 감지 거리의 근접 센서에 대한 수요도 증가하고 있습니다.

자동차 및 자동차 부품 산업을 위한 생산 연동 인센티브(PLI) 제도는 첨단 자동차 기술(AAT) 제품의 국내 제조를 촉진하고 자동차 제조 밸류체인에 대한 투자를 유치하기 위해 금전적 인센티브를 제안하고 있습니다. 이 제도의 주요 목적은 비용 장애물 극복, 규모의 경제 창출, AAT 제품 분야의 견고한 공급망 구축 등을 포함합니다.

아시아태평양은 최근 몇 년 동안 석유 및 가스 산업의 생산 능력이 증가한 유일한 지역입니다. 또한, 석유 및 가스 산업에 대한 투자 증가는 기회를 창출할 것입니다. 예를 들어, IBEF에 따르면 인도의 석유 및 가스 탐사 및 생산 활동에 대한 투자는 2022년까지 2,500만 달러에 달할 것으로 예상됩니다. 또한, 에너지 수요를 충족시키고 새로운 프로젝트를 시작하기 위한 정부의 정책 및 이니셔티브의 확대도 기여할 것입니다. 적극적으로 시장에 진입할 것입니다.

유도형 근접 센서 산업 개요

유도형 근접 센서 시장은 본질적으로 경쟁이 치열합니다. 시장은 크고 작은 기업의 존재로 인해 집중되어 있습니다. 시장의 주요 업체로는 Panasonic Corporation, Sick AG Pepperl Fuchs, Rockwell Automation Inc. 등이 있습니다.

2022년 8월: 유도형 근접 센서는 차량, 즉 모바일 기기에서 회전 암, 그립 암, 덤프 본체의 위치 모니터링 및 종료 위치 모니터링과 같은 작업에 자주 사용됩니다. 로크웰 오토메이션(Rockwell Automation Inc.)은 브라보 모터 컴퍼니(Bravo Motor Company)와 협력하여 배터리, 차량 및 에너지 저장 시스템 생산에 주력하고 있습니다. 이번 제휴를 통해 로크웰 오토메이션은 순환 경제 개념에 기반한 브라질 시장에서 배터리 및 전기자동차 제조를 위한 최첨단 솔루션을 제공하는 데 기여할 것입니다.

기타 혜택

엑셀 형식의 시장 예측(ME) 시트

3개월간 애널리스트 지원

목차

제1장 서론

조사 가정과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

업계의 매력 - Porter's Five Forces 분석

공급 기업의 교섭력

소비자의 협상력

신규 참여업체의 위협

대체품의 위협

경쟁 기업간 경쟁 강도

COVID-19가 유도형 근접 센서 시장에 미치는 영향

제5장 시장 역학

시장 성장 촉진요인

산업 자동화 성장

비접촉 센싱 기술에 대한 수요 상승

시장 과제

센싱 기능 제한

제6장 시장 세분화

최종사용자 용도별

산업용

자동차

항공우주와 방위

포장

기타 최종사용자 용도

지역별

북미

미국

캐나다

유럽

영국

독일

프랑스

기타 유럽

아시아태평양

중국

일본

인도

기타 아시아태평양

라틴아메리카

중동 및 아프리카

제7장 경쟁 상황

기업 개요

Pepperl+Fuchs

Rockwell Automation Inc.

Panasonic Industry Co. Ltd

Eaton Corporation PLC

Sick AG

Omron Corporation

Delta Electronics Inc.

Autonics Corporation

Datalogic SpA

Riko Opto-electronics Technology Co. Ltd

Fargo Controls Inc.

Hans Turck GmbH and Co. Kg

Keyence Corporation

Honeywell International

Balluff GmbH

KA Schmersal GmbH &Co.

EUCHNER USA Inc.

Baumer Holding AG

제8장 투자 분석

제9장 시장 전망

ksm

영문 목차

영문목차

The Inductive Proximity Sensor Market size is estimated at USD 1.29 billion in 2024, and is expected to reach USD 1.81 billion by 2029, growing at a CAGR of 7.13% during the forecast period (2024-2029).

Inductive proximity sensors are non-contact devices that set up a radio frequency field with a coil and an oscillator. The presence of an object can alter this field, and the sensor can detect this alteration. The inductive proximity sensors can detect an object without touching it and therefore do not cause damage or abrasion to the object.

Key Highlights

Proximity sensors are generally used in many automation applications. They are used to sense objects and do not require physical contact with the target or object being sensed. Thus, they are referred to as non-contact sensors. The common proximity sensor types include photoelectric, capacitive, and inductive sensors.

Inductive proximity sensors are utilized for the non-contact detection of metallic objects. The operating principle of these sensors is based on the coil and oscillator, which creates an electromagnetic field in the near surroundings of the sensing surface. Proximity sensors are also found in consumer devices. In smartphones, proximity sensors detect if a user is holding the mobile near their face.

With ASIC technology, SICK sensors provide enhanced precision and reliability. The company can offer the right solution to meet the customer's requirements every time, from cuboid standard sensors or cylindrical, with single, double, or triple operating distances, to special sensors for use in explosive and toxic atmospheres or harsh environments. The company's inductive proximity sensors are the intelligent, reliable route to implementing industry-specific and customized to any task involving automation.

In the case of conventional inductive proximity sensors, if the distance to the damping element increases, the sensor becomes more sensitive to the detection object, and the metal surrounding the installation affects the switching distance.

To tackle this issue, Pepperl+Fuchs has introduced active shielding technology, which enables high switching distances regardless of the installation conditions. The company has integrated it into the VariKont series for the first time. They are available in versions with high switching distances of 30 mm for flush mounting and 50 mm for non-flush mounting.

The inductive proximity sensors are used in several industrial and manufacturing applications for safety and inventory management applications. An automated production line, for example, is used for positioning, object detection, counting, and inspection. The proximity sensors are also used for part detection in several industrial conveyor systems.

The need to withstand harsh cleaning agents, severe temperatures, and high-pressure wash-down environments is compelling the food and beverage industry to adopt proximity sensors. In the food and beverage sector, applications like food production and harsh chemicals are used during cleaning, where a standard sensor will corrode and fail prematurely. The inductive proximity sensor exhibits a robust design with superior resistance to high temperature and high-pressure cleaning processes.

Inductive Proximity Sensors Market Trends

Industrial Segment to Hold Significant Market Share

Industrial applications are becoming dependent on tracking, monitoring, measuring, and communication. Modern industries depend heavily on the information and data that various sensory devices supply to the control system, ideally in fractions of a second, to be an effective smart manufacturing environment. All industrial applications require robustness, high IP protection classes, advanced EMC and voltage immunity, and wide-range temperature stability parallel to cost-efficient sensor implementation.

Inductive proximity sensors are majorly used where a more traditional switch might prove problematic or impossible to use, like in an application where lots of water and dirt might be present. Typical examples would be an advanced CNC machine or a conveyor line in a food and beverage environment and multiple uses in the industrial landscape.

Although large industries practiced the use of inductive proximity sensor technology over a few years, improved technology has led to its widespread adoption by all-tier companies to streamline operations, enhance industrial automation, and change the manufacturing landscape of several companies. Another growth factor is the increase in the number of vendors that enable industrial automation and growth in the Industrial Internet of Things (IIoT) demand.

Many WFI sensors on the market also provide multi-metal detection at the same sensing range. These sensors are commonly referred to as Factor 1 or F1 models since they have no sensing range reduction factor for non-ferrous materials like aluminum. Moreover, their sensing range reduction factor would be equal to 1.0 (no reduction in sensing distance).

Asia-Pacific to Witness Significant Growth

Asia-Pacific is anticipated to witness a considerable growth rate compared to other regions because of developing countries like China and India. Additionally, prominent vendors, such as Omron Corporation, Panasonic Corporation, and Autonics Corporation, are headquartered in the region.

Manufacturers in the automotive industry strive to meet the demand for electric vehicles (EVs) and low fuel consumption by building lighter-weight vehicles and favoring aluminum over iron. As the prevalence of mixed production lines containing both aluminum and iron increases, the need for the same sensing distance proximity sensors with suitably long sensing ranges is also rising.

The Production Linked Incentive (PLI) Scheme for the automobile and auto component industry proposes financial incentives for boosting domestic manufacturing of advanced automotive technology (AAT) products and gaining investments in the automotive manufacturing value chain. The prime objectives of the schemes include overcoming cost disabilities, creating economies of scale, and building a robust supply chain in areas of AAT products.

Asia-Pacific is the only region to witness capacity growth in the oil and gas industry in recent years. Moreover, growing investment in the oil and gas industry would create opportunities. For instance, according to IBEF, the investment in oil and gas exploration and production activities in India is anticipated to reach USD 25 million by 2022. Additionally, the growing government policies and initiatives toward the fulfillment of energy demands and initiation of new projects will contribute positively to the market.

Inductive Proximity Sensors Industry Overview

The inductive proximity sensors market is very competitive in nature. The market is concentrated due to the presence of various small and large players. Some of the significant players in the market are Panasonic Corporation, Sick AG Pepperl+Fuchs, Rockwell Automation Inc., Eaton Corporation PLC, Omron Corporation, Delta Electronics Inc., and many more.

August 2022: Inductive proximity sensors are often used in vehicles, i.e., in mobile equipment, for tasks such as position monitoring or end position monitoring of swivel arms, gripping arms, and dump bodies. Rockwell Automation Inc. partnered with Bravo Motor Company, focusing on producing batteries, vehicles, and energy-storage systems. With the new alliance, Rockwell Automation will contribute to providing cutting-edge solutions for manufacturing batteries and electric vehicles in the Brazilian market based on the circular economy concept.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Consumers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitutes

4.2.5 Intensity of Competitive Rivalry

4.3 Impact of COVID-19 on the Inductive Proximity Sensor Market

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Growth in Industrial Automation

5.1.2 Increase in the Demand for Non-contact Sensing Technology