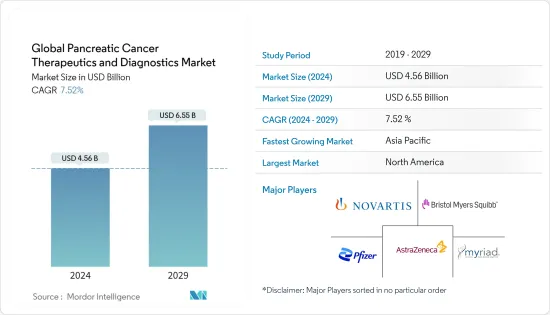

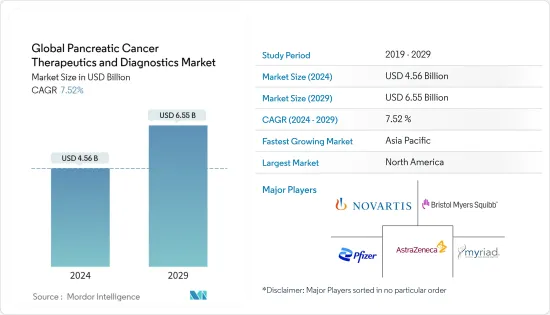

세계 췌장암 치료 및 진단 시장 규모는 2024년 45억 6,000만 달러로 추정되며, 2029년까지 65억 5,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 7.52%의 CAGR로 성장할 것으로 예상됩니다.

COVID-19의 발생으로 병원과 의료 서비스가 크게 감소하여 췌장암 치료 및 진단 시장에 영향을 미쳤습니다. 또한 COVID-19는 세계 경제에 영향을 미쳤고, 병원 내 신종 코로나바이러스 감염증 환자 외의 일반 환자들을 위한 병원 의료 기능에 큰 영향을 미쳤습니다. 2020년 6월, 국립생명공학정보센터(National Biotechnology Information Center)에 게재된 기사는 COVID-19가 전 세계 내시경 장비 사용에 미치는 영향에 대해 연구했습니다. 이 연구는 2020년 4월 23일부터 5월 12일까지 6개 대륙 55개국을 대상으로 조사했습니다. 연구 결과, COVID-19 팬데믹 기간 동안 시행된 내시경 검사의 수가 감소했으며, 기준치 대비 83% 감소한 것으로 나타났습니다. 같은 기간 동안 상부 내시경 검사는 82%, 하부 내시경 검사는 85% 감소한 것으로 나타났습니다. 2020년 8월, COVID-19가 암 환자의 췌장 수술에 미치는 영향에 대한 연구 결과가 PubMed에 발표되었습니다. 이 조사는 37개국 267개 센터의 337명의 응답자를 대상으로 실시됐습니다. 조사에 따르면, COVID-19 사태로 인해 대부분의 센터에서 췌장 수술 건수가 감소하여 주당 췌장 절제술 건수가 3건에서 1건으로 감소했습니다. 따라서 COVID-19 팬데믹은 조사 대상 시장의 성장에 큰 영향을 미칠 것으로 예상됩니다.

췌장암 치료 및 진단에는 췌장암 진단 및 후속 치료에 사용되는 의료 절차가 포함됩니다. 췌장암의 유병률과 발생률 증가, 분자 생물학, 의약품 개발, 진단 기술의 발전과 같은 요인이 시장 성장에 큰 역할을 하고 있습니다. 연구 개발 노력의 증가, 유리한 상환 시나리오, 신제품 출시로 인해 시장은 예측 기간 동안 크게 성장할 것으로 예상됩니다. 2021년 1월, Myriad Genetics Inc.는 일본 후생노동성으로부터 췌장암 검진에 사용되는 BRACAnalysis 진단 시스템에 대한 상환을 받을 것이라고 발표했습니다. 이를 통해 일본 내 췌장암 유전자 검사 환자 수가 늘어날 것으로 기대됩니다. 또한, 시장에서는 많은 협업이 이루어지고 있어 시장 발전에 긍정적인 영향을 미칠 것으로 예상됩니다. 2020년 10월, Oncolytics Biotech Inc.는 전이성 췌장암 치료에서 페라올렙과 아테졸리주맙의 효능을 시험하는 1/2상 임상시험을 위해 Roche 및 AIO와 협력한다고 발표했습니다. 따라서 이러한 발전은 예측 기간 동안 조사 대상 시장의 성장에 긍정적인 영향을 미칠 것으로 예상됩니다.

화학요법은 췌장암 세포의 증식과 분열을 막아 췌장암 세포를 죽이는 주요 암 치료법 중 하나입니다. 이 약들은 전신 치료입니다. 약물이 혈류를 통해 이동하여 몸 전체의 암세포에 손상을 입힙니다. 불행히도 화학 요법은 일부 건강한 세포를 손상시키고 심각한 부작용을 일으킬 수 있습니다. 화학요법은 췌장 종양을 축소하거나 증식을 방지할 수 있습니다. 미국암협회에 따르면, 췌장암 치료에 사용되는 화학요법 약물에는 젬시타빈(젬잘), 5-플루오로라실(5-FU), 일리노테칸(캄토살), 옥살리플라틴(엘록사틴), 알부민 결합 파클리탁셀(아브락산), 카페시타빈(젤로다), 시스플라틴(시스플라틴), 알부민 결합 파클리탁셀(아브라산), 카세티바틴(젤로다), 카세티닙(젤로다), 시스플라틴(젤라틴), 카세티바틴(젤라틴)이 있습니다. 젤로다), 시스플라틴, 파클리탁셀(탁솔), 도세탁셀(탁소텔), 일리노테칸 리포솜(오니바이드)이 있습니다.

1990년대부터 화학요법제 젬시타빈(젬자르)은 수술로 절제할 수 있는(절제 가능한) 췌장암 환자 치료의 핵심이 되어왔습니다. 전통적으로 젬시타빈은 환자가 수술에서 회복된 후 보조 화학요법으로 투여되어 왔지만, 이 수술은 많은 환자들에게 채찍질 수술로 알려진 가혹한 수술입니다. 최근에는 젬시타빈을 화학요법제인 카페시타빈(젤로다)과 병용하기도 합니다. 화학요법은 단독으로 또는 수술, 표적치료, 면역치료 및/또는 방사선 치료와 함께 시행될 수 있습니다. 화학요법과 방사선을 병용하는 경우, 일반적으로 저용량의 화학요법이 사용됩니다. 방사선 치료와 함께 가장 일반적으로 사용되는 화학요법은 플루오로우라실(5-FU)과 젬시타빈(젬자르)입니다. 5-FU는 방사선과 함께 사용한 경험이 많고 부작용이 적기 때문에 가장 자주 사용됩니다.

2020년 3월, 루스트가르텐 재단과 Stand Up to Cancer(SU2C)의 전략적 파트너십인 췌장암 집단은 다나 파버 암 연구소의 팀을 포함한 4명의 최고 연구팀에게 최대 1,600만 달러의 연구비를 수여했습니다. New Therapies Challenge Grants, American Association for Cancer Research(AACR) 및 SU2C의 과학 파트너 중 일부입니다. 화학요법과 결합된 DNA 복구 억제제를 시험하는 3건의 췌장암 임상시험을 지원하기 위해 약 400만 달러의 자금이 지원됩니다. 따라서 췌장암에 대한 효과적인 치료 옵션에 대한 수요가 급증함에 따라 연구 대상 부문은 예측 기간 동안 상당한 성장을 이룰 것으로 예상됩니다.

미국은 췌장암 발생률 증가, 보조금 지급 정책, 높은 의료비 지출로 인해 중요한 시장 점유율을 유지할 것으로 예상됩니다.

MedCrave Gastroenterology and Hepatology 저널의 2018년 발표에 따르면, 췌장암은 중간 정도의 발병률에도 불구하고 9번째로 흔한 암으로 나타났습니다. 2030년까지 췌장암은 암 사망 원인 중 두 번째로 많은 암이 될 것으로 예상됩니다. 또한, GLOBOCAN 2020 보고서에 따르면 2020년에는 약 56,654명의 췌장암 환자가 새로 보고되었습니다. 또한 2020년 췌장암으로 인한 사망자 수는 약 47,683명으로 보고됐습니다. 미국. USFDA는 또한 임상 단계에서 의약품을 승인하여 임상 개발을 가속화함으로써 췌장암 치료제 및 진단 시장의 성장을 촉진하기위한 조치를 취하고 있습니다. 기업과 연구 기관은 연구 개발에 투자하고 있습니다. 따라서 시장은 빠르게 성장하고 있습니다. 예를 들어, 2020년 엘리텍의 주요 제품 후보인 엘리아스파제는 국내 2차 치료 전이성 췌장암 환자를 위한 새로운 치료 옵션이 절실히 필요한 상황에서 FDA로부터 패스트트랙 지정을 받았습니다. FDA의 이러한 제품 승인은 전체 시장을 끌어올릴 것으로 예상됩니다.

2020년, 나노바이오틱스는 미국 FDA에 따라 췌장암을 대상으로 NBXR3를 이용한 첫 번째 임상 1상 시험을 발표했는데, 이는 미국 FDA에 따라 안전하게 실시할 수 있는 시험입니다. 이 임상시험은 Nanobiotix와 공동 개발되었으며, MD Anderson이 임상시험의 스폰서이자 수행자입니다. 이러한 임상시험의 좋은 결과는 새로운 치료법을 가져오고 지역 시장 성장에 긍정적인 영향을 미칠 것입니다. 따라서 위의 요인으로 인해 조사 대상 시장은 예측 기간 동안 이 지역에서 상당한 성장을 기록할 것으로 예상됩니다.

췌장암 치료 및 진단 시장은 경쟁이 치열하며 많은 주요 기업들이 시장을 독점하고 있습니다. Novartis AG, Pfizer Inc., Bristol-Myers Squibb Company, AstraZeneca PLC, Myriad Genetics Inc. 및 Viatris Inc.와 같은 주요 시장 기업의 존재로 인해 경쟁이 심화되고 있습니다. 시장 기업들은 치열해지는 시장 경쟁을 유지하기 위해 R&D 투자 증가, 합병, 인수, 제품 혁신 등의 전략을 채택하고 있습니다.

The Global Pancreatic Cancer Therapeutics and Diagnostics Market size is estimated at USD 4.56 billion in 2024, and is expected to reach USD 6.55 billion by 2029, growing at a CAGR of 7.52% during the forecast period (2024-2029).

The outbreak of COVID-19 significantly reduced hospital and healthcare services, impacting the pancreatic cancer therapeutics and diagnostics market. Moreover, the COVID-19 pandemic affected the global economy and showed a huge impact on the functioning of general hospital care for non-COVID-19 patients in hospitals. In June 2020, an article appearing in the National Center for Biotechnology Information studied the impact of the COVID-19 pandemic on the use of endoscopy units globally. The study looked into 55 countries across 6 continents from April 23 to May 12, 2020. The study found that the number of endoscopy procedures performed during the COVID-19 pandemic decreased, constituting an 83% reduction compared to the baseline figures. The study also found out that there was an 82% reduction in upper endoscopy procedures and an 85% reduction in lower endoscopy procedures during the same time. In August 2020, a survey was published in PubMed on the impact of COVID-19 on pancreatic surgery for cancer patients. The survey was conducted amongst 337 respondents from 267 centers from 37 countries. According to the survey, most centers performed fewer pancreatic surgeries due to the COVID-19 pandemic, which reduced the weekly pancreatic resection rate from 3 to 1. Thus, the COVID-19 pandemic is expected to impact the studied market's growth significantly.

Pancreatic cancer therapeutics and diagnostics involve medical procedures used to diagnose pancreatic cancer and subsequent treatment. Factors such as the increasing prevalence and incidence of pancreatic cancer and advancements in molecular biology, development of drugs, and diagnostic technology play a major part in market growth. With the increase in R&D initiatives, favorable reimbursement scenarios, and the launch of novel products, the market is expected to grow significantly during the forecast period. In January 2019, scientists from the Van Andel Research Institute (VARI) developed a novel blood test (CA19-9 test) that, when combined with an existing test, can detect nearly 70% of pancreatic cancers with a less than 5% of false-positive rate. Moreover, in January 2021, Myriad Genetics Inc. announced that it would receive reimbursement for its BRACAnalysis Diagnostic System, which is also used for pancreatic cancer screening from Japan's Ministry of Health, Labour, and Welfare. The initiative is expected to increase the patient pool for genetic testing for pancreatic cancer in Japan. Also, many collaborations are taking place in the market, which is expected to affect market development positively. In October 2020, Oncolytics Biotech Inc. announced a collaboration with Roche and AIO for a phase 1/2 trial of testing the efficacy of pelareorep and atezolizumab in the treatment of metastatic pancreatic cancer. Thus, these developments are expected to impact the studied market growth over the forecast period positively.

Chemotherapy is one of the main cancer treatments that kill pancreatic cancer cells by preventing them from growing and dividing. These drugs are systemic treatments; the drugs travel through the bloodstream and damage cancer cells throughout the body. Unfortunately, chemotherapy can damage some healthy cells and cause major side effects. Chemotherapy may shrink and/or prevent the growth of pancreatic tumors. According to the American Cancer Society, the chemotherapy drugs used to treat pancreatic cancer include Gemcitabine (Gemzar), 5-fluorouracil (5-FU), Irinotecan (Camptosar), Oxaliplatin (Eloxatin), Albumin-bound paclitaxel (Abraxane), Capecitabine (Xeloda), Cisplatin, Paclitaxel (Taxol), Docetaxel (Taxotere), and Irinotecan liposome (Onivyde).

Since the 1990s, the chemotherapy drug gemcitabine (Gemzar) has been the backbone of treating people with pancreatic cancer that can be removed with surgery (resectable). Traditionally, gemcitabine has been given as adjuvant chemotherapy after the patient has recovered from the surgery, which, for many patients, is a grueling procedure known as the Whipple procedure. More recently, gemcitabine is sometimes combined with the chemotherapy drug capecitabine (Xeloda). Chemotherapy may also be given alone or combined with surgery, targeted therapy, immunotherapy, and/or radiation. When chemotherapy is given in combination with radiation, a low dose of chemotherapy is typically used. The chemotherapy drugs most commonly used in conjunction with radiation therapy are fluorouracil (5-FU) and gemcitabine (Gemzar). 5-FU is used most often since there is more experience using this drug in combination with radiation, and there are fewer side effects.

In March 2020, the Pancreatic Cancer Collective, the strategic partnership of the Lustgarten Foundation and Stand Up To Cancer (SU2C), was awarded up to USD 16 million to four teams of top researchers, including a team at Dana-Farber Cancer Institute, as part of its New Therapies Challenge Grants, the American Association for Cancer Research (AACR), and Scientific Partner of SU2C. Nearly USD 4 million in funding is available to help support three pancreatic cancer clinical trials testing DNA repair inhibitors combined with chemotherapy. Thus, due to the surging demand for effective treatment options for pancreatic cancers, the studied segment is expected to witness significant growth over the forecast period.

The United States is expected to retain its significant market share due to the rising incidence of pancreatic cancers, supportive reimbursement policies, and high healthcare spending.

As per a 2018 publication in the MedCrave Gastroenterology and Hepatology journal, pancreatic cancer was the ninth most frequent cancer, despite its moderate incidence. It was expected to be among the second-deadliest cause of cancer by 2030. Also, according to the GLOBOCAN 2020 report, about 56,654 new cases of pancreatic cancer were reported in 2020. Moreover, approximately 47,683 deaths due to pancreatic cancer were reported in the United States. The USFDA is also taking steps to enhance the growth of the pancreatic cancer therapeutics and diagnostic market by approving drugs in the clinical phase, thereby accelerating clinical developments. Companies and research organizations are investing in R&D. Thus, the market is expanding quickly. For instance, in 2020, ERYTECH's lead product candidate, eryaspase, received the fast track designation by the FDA due to the urgent need for potential new treatment options for patients with second-line metastatic pancreatic cancer in the country. Such product approvals by the FDA are expected to lift the overall market.

In 2020, NANOBIOTIX announced its first phase I trial with NBTXR3 in Pancreatic Cancer, which is safe to proceed as per the US FDA. The trial was co-developed with Nanobiotix, and MD Anderson is the sponsor and executor of the trial. These clinical trials' positive outcomes will result in a new treatment, positively influencing the regional market growth. Thus, owing to the factors mentioned above, the studied market is anticipated to register significant growth over the forecast period in the region.

The Pancreatic Cancer Therapeutics and Diagnostics market is highly competitive, with many key players dominating the market. The presence of major market players like Novartis AG, Pfizer Inc., Bristol-Myers Squibb Company, AstraZeneca PLC, Myriad Genetics Inc., and Viatris Inc. is intensifying the competition. The market players are adopting strategies, such as rising R&D investments, mergers, acquisitions, and product innovations, to sustain the increasing market rivalry. For instance, in January 2021, Myriad Genetics Inc. entered into a strategic partnership with Illumina Inc. for the latter to create a kit-based version of the myChoice companion diagnostic (CDx) test for international markets, which can be used to detect pancreatic cancer.