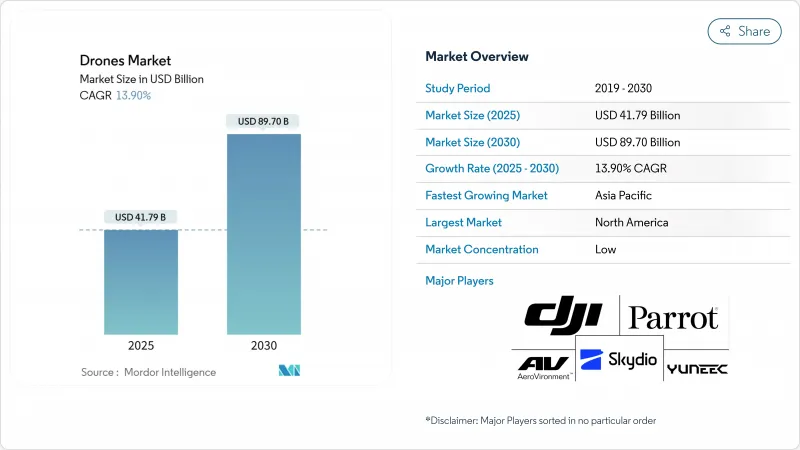

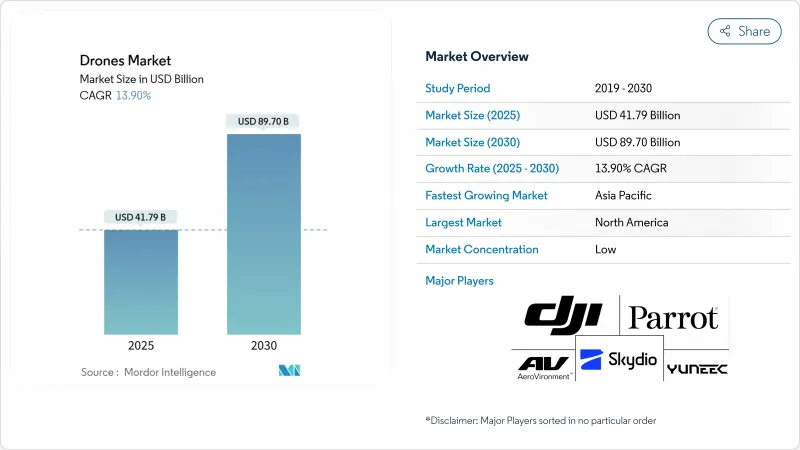

드론 시장 규모는 2025년에 417억 9,000만 달러에 이르고, 2030년에는 897억 달러에 달할 전망입니다.

탑재된 에지 AI가 10W 이하의 칩셋으로 복잡한 지각 알고리즘을 실행해, 건설, 에너지, 농업에서 자율형 미션이 실행 가능하게 됨에 따라, 채용이 가속합니다. 멀티 액세스 엣지 컴퓨팅(MEC)을 갖춘 5G의 급속한 배치는 신뢰할 수 있는 Beyond Visual Line-of-Sight(BVLOS) 제어를 지원하는 10ms 이하의 대기 시간을 제공하는 반면, 센서의 급격한 가격 저하로 인해 고급 페이로드가 소규모 사업자에게도 개방됩니다. 특히 FAA의 BVLOS 규칙안이나 ICAO의 새로운 기준·권장 관행(SARPs) 등 규제의 움직임은 공역 액세스의 확대를 시사하고 있습니다. 그러나 리튬 이온 배터리 부족과 희토류 재료의 수출 억제 등 공급망의 변형은 계속해서 재료비 상승을 초래하여 재량 수요를 줄일 수 있습니다. 전반적으로 경쟁은 하드웨어, AI 소프트웨어 및 규제 준수를 엔드 투 엔드 가치 제안에 번들 수있는 기업으로 전환하고 있으며 드론 시장 전체의 통합이 가속화되고 있습니다.

에지 추론 엔진은 7-10W 경량 프로세서로 물체 검출, 경로 계획, 비측정 로직을 실행하며, 드론은 복잡한 환경에서도 백홀의 대기 시간 없이 적응할 수 있게 되었습니다. 유틸리티자는 AI를 탑재한 선박이 이상을 감지하고 상세한 이미지 처리를 위해 자율적으로 재배치함으로써 다운타임이 최대 35% 삭감되고 ROI가 높아졌습니다고 보고하고 있습니다. 대규모 언어 모델이 안전 스택에 통합되어 충돌 회피의 판단 품질이 향상되었습니다.

반송파 에지 노드와 결합된 독립형 5G 네트워크는 10ms 이하의 왕복 지연을 실현하여 지상 기반 무선 릴레이의 필요성을 제거합니다. Valmont가 T-Mobile의 5G 그리드에서 수행한 77마일의 BVLOS 검사는 지속적인 명령 링크와 실시간 비디오 백홀을 확인했습니다. FCC 파트 88 규칙은 무인 항공기 명령 채널에 대해 보호되는 5030-5091MHz 코리도를 더욱 강화합니다.

배터리 셀은 일반적인 소형 드론 비용의 1/4을 차지하며, 2024년 이후 30-40%의 인상으로 OEM은 마진 압축을 흡수하거나 판매 가격을 인상해야 합니다. 지정학적 긴장과 EV 수요 증가는 부족을 악화시키고 중국의 주요 배터리 광물 수출 억제는 장기적인 생산 능력을 위협하고 있습니다.

2024년 드론 시장의 39.45%는 건설업이 차지하고 공중 촬영에 의한 진행 추적, 3D 모델링, 현장 보안이 주류가 되었습니다. 고해상도 사진 측량은 수작업에 비해 측량 시간을 70% 이상 단축하고, 자동화된 수량 계산은 지불 사이클을 앞당깁니다. 에너지 산업은 규모가 작고 CAGR은 19.05%로 2030년까지 그 차이를 줄일 수 있습니다. 유틸리티 회사는 현재 헬리콥터를 AI 유도 로터 공예로 전환하고, 한 번의 출격으로 절연체의 균열과 열 핫스팟을 발견하여 연간 약 60%의 비용 절감을 달성하고 있습니다. 농업은 FAA(연방항공국)가 승인한 군산포 덕분에 바로 뒤를 이었습니다. 하이리오와 같은 기업에 따르면 현재 고객의 절반 이상이 광대 한 토지를 커버하기 위해 여러 드론스 웜을 도입하고 있습니다.

공공 안전과 엔터테인먼트 분야에서도 기세가 증가하고 있습니다. 트라이얼에서는 드론에 의한 초동 대응(DFR) 프로그램에 의해 출동 시간이 8분에서 3분 반으로 단축되어 지역 경찰 활동의 효율이 향상되었습니다. 시네마토그래피는 페이로드의 혁신을 추진하고 보다 광범위한 센서 통합을 촉진합니다. 이러한 추세는 드론 시장이 점차 다양해지고 각 틈새 시장이 특정 항공기, 센서 및 자율성 요구 사항을 최적화하고 있음을 보여줍니다.

고정익기는 2024년 매출의 45.07%를 차지하고 파이프라인과 같은 긴 직선 통로에서의 에너지 소비가 적은 것으로 평가되었습니다. 그러나 하이브리드 VTOL 항공기는 도시 지역의 에어 모빌리티 사업자가 공간에 제약이 있는 옥상에 맞추어 수직 이륙해야 하기 때문에 CAGR 20.10%를 나타낼 전망입니다. 통신 타워 점검이나 수색 구조와 같은 호버링 작업에는 회전익 유닛이 필수적인 것에 변함이 없습니다. EHang의 EH216-S는 세계 최초를 달성했습니다. 복합재료의 채용도 차별화 요인의 하나입니다. 탄소섬유 강화 폴리머의 기체는 강성을 유지하면서 중량을 최대 15% 줄이고 항속 거리를 직접 늘립니다. 한편, 바이오 수지는 2024년에 파일럿리스 여객기 eVTOL의 드론 형식 증명을 취득해 하이브리드의 실현 가능성을 강조하는 가운데 환경에 대한 감시가 높아지고 있음을 반영하여 사용 후 재활용성에 기대가 있었습니다.

복합재료의 채용도 차별화 요인의 하나입니다. 탄소섬유 강화 폴리머의 기체는 강성을 유지하면서 중량을 최대 15% 줄이고 항속 거리를 직접 늘립니다. 한편, 바이오 수지는 드론 산업 전반에 걸쳐 환경에 대한 감시의 눈이 높아지고 있음을 반영하여 사용 후 재활용성으로 유망시되고 있습니다.

북미는 FAA의 테스트 사이트 프로그램과 커맨드 링크용 5030-5091MHz의 전용 주파수 대역에 힘입어 2024년 세계 매출의 37.97%를 벌어들였습니다. Wing과 Walmart는 완전히 통합된 UTM 서비스를 사용하여 15만 건의 소포 납품을 달성했으며 대규모 상업적 준비 태세를 입증했습니다. 그러나 미국 안보 드론법(American Security Drone Act)은 연방 정부가 보유한 중국제 기체를 대체하는 국산 기체의 생산을 장려하고 있으며, 데이터 보안에 관한 정책은 강화되고 있습니다.

아시아태평양은 CAGR 15.27%에서 가장 빠르게 성장하는 지역입니다. 중국의 '저고도 경제' 전략은 2035년까지 3조 5,000억 위안(4,870억 달러) 시장을 목표로 하고 있으며, 시험 코리도와 구매 보조금으로 현지 챔피언을 지원하고 있습니다. 인도의 수입 금지 조치는 외국 OEM의 진입을 막지 만 PLI 계획 하에서 신흥 제조 클러스터를 활성화시킵니다. 일본과 한국은 높은 재해대책 예산을 반영하여 드론을 인프라 점검과 쓰나미 대응 미션으로 돌려보냅니다.

유럽은 160만 명 이상의 등록 사업자를 관리하는 EASA의 통합된 U-공간 청사진에 의해 지원되며 여전히 매우 중요합니다. 엄격한 프라이버시 바이 디자인의 의무화로 인해 배치 사이클은 장기화되지만, 드론에 의한 해상 풍력 발전의 유지보수와 같은 지속가능성을 중시한 프로젝트는 수요 증가를 유지하고 있습니다. 이 대륙은 또한 eVTOL 시험을 위한 특정 통로를 승인하고 있으며, 제조업체는 2020년대 후반까지 에어택시 인증 획득을 위한 명확한 길을 걷게 됩니다.

The drones market size reached USD 41.79 billion in 2025 and is on course to climb to USD 89.70 billion by 2030, reflecting a robust 13.9% CAGR.

Adoption accelerates as on-board edge-AI runs complex perception algorithms on sub-10 W chipsets, making autonomous missions viable in construction, energy, and agriculture. Rapid 5G roll-outs with Multi-access Edge Computing (MEC) provide sub-10 ms latency that supports dependable Beyond Visual Line-of-Sight (BVLOS) control, while steep sensor-price declines open sophisticated payloads to smaller operators. Regulatory momentum-most notably the FAA's draft BVLOS rules and ICAO's new Standards and Recommended Practices (SARPs)-signals greater airspace access. Yet supply chain strains, notably lithium-ion cell shortages and export curbs on rare-earth materials, continue to inflate bill-of-materials costs and could dampen discretionary demand. Overall, competition is shifting toward firms that are able to bundle hardware, AI software, and regulatory compliance into an end-to-end value proposition, accelerating consolidation across the drones market.

Edge inference engines now execute object detection, path planning, and contingency logic on lightweight 7-10 W processors, letting drones adapt in complex environments without back-haul latency. Utility operators report downtime cuts of up to 35% when AI-equipped craft flag anomalies and autonomously re-position for detailed imaging, driving strong ROI. Large language models are integrated into safety stacks to boost collision-avoidance decision quality.

Standalone 5G networks paired with carrier-edge nodes deliver sub-10 ms round-trip latency, removing the need for ground-based radio relays. Valmont's 77-mile BVLOS inspection over T-Mobile's 5G grid validated persistent command links and real-time video backhaul. The FCC's Part 88 rules further cement a protected 5030-5091 MHz corridor for drone command channels.

Battery cells comprise up to one-quarter of typical small-drone costs, and 30-40% price hikes since 2024 have forced OEMs either to absorb margin compression or lift selling prices. Geopolitical tensions and rising EV demand exacerbate the shortage, while China's export curbs on key battery minerals threaten longer-term capacity.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Construction held 39.45% of the drones market in 2024 as aerial progress tracking, 3-D modeling, and site security became mainstream. High-resolution photogrammetry slashes survey time by over 70% compared with manual methods, while automated volume calculations speed payment cycles. The energy industry, though smaller, exhibits a 19.05% CAGR that could narrow the gap by 2030. Utilities now swap helicopters for AI-guided rotorcraft that spot insulator cracks or thermal hotspots in a single sortie, achieving around 60% annual cost savings. Agriculture follows closely, thanks to FAA-approved swarm spraying; firms such as Hylio report that over half of clients now deploy multi-drone swarms to cover large acreages.

Momentum is also building in public safety and entertainment. In trials, drone-as-first-responder (DFR) programs cut dispatch times from eight to 3.5 minutes, augmenting community policing efficiency. Cinematography continues to push payload innovation, encouraging wider sensor integration. These trends point to a progressively diversified drone market, each niche optimizing specific airframe, sensor, and autonomy requirements.

Fixed-wing craft commanded 45.07% of 2024 revenue, prized for low energy consumption over long linear corridors such as pipelines. Yet, hybrid VTOL aircraft are scaling at 20.10% CAGR as urban air-mobility operators need vertical take-off to fit space-constrained rooftops. Rotary-wing units remain essential for hovering jobs like telecom-tower inspection or search-and-rescue. EHang's EH216-S achieved the world's first. Adoption of composite materials is another differentiator. Carbon-fiber-reinforced polymer airframes trim weight by up to 15% while preserving stiffness, directly extending range. Meanwhile, bio-based resins show promise for end-of-life recyclability, reflecting rising environmental scrutiny across the drone type certificate for a pilotless passenger eVTOL in 2024, underscoring hybrid viability.

Adoption of composite materials is another differentiator. Carbon-fiber-reinforced polymer airframes trim weight by up to 15% while preserving stiffness, directly extending range. Meanwhile, bio-based resins show promise for end-of-life recyclability, reflecting rising environmental scrutiny across the drone industry.

The Drones Market Report is Segmented by Application (Construction, Agriculture and More), Type (Fixed-Wing Drones, Rotary-Wing Drones, and More), Weight Class (Nano/Micro, Small, and More), Mode of Operation (Remotely Piloted, Optionally Piloted, and More), End-User (Commercial and Consumer, and More) and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America produced 37.97% of global 2024 revenue, buoyed by FAA test-site programs and dedicated 5030-5091 MHz spectrum for command links. Wing and Walmart surpassed 150,000 parcel deliveries using fully integrated UTM services, demonstrating commercial readiness at scale. Policy, however, is tightening around data security, with the American Security Drone Act encouraging domestic production to replace Chinese airframes in federal fleets.

Asia-Pacific is the fastest-expanding region, with a 15.27% CAGR. China's "low-altitude economy" strategy targets a CHY 3.5 trillion yuan (USD 487 billion) market by 2035 and supports local champions with testing corridors and purchase subsidies. India's import embargo stifles foreign OEMs but fuels nascent manufacturing clusters under the PLI scheme. Japan and South Korea channel drones into infrastructure inspection and tsunami-response missions, reflecting high disaster-preparedness budgets.

Europe remains pivotal, anchored by EASA's unified U-space blueprint that governs more than 1.6 million registered operators. Stringent privacy-by-design mandates prolong deployment cycles, yet sustainability-oriented projects-like drone-assisted offshore-wind maintenance-keep demand rising. The continent has also approved specific corridors for eVTOL trials, putting manufacturers on a clear path toward air-taxi certification by the late 2020s.