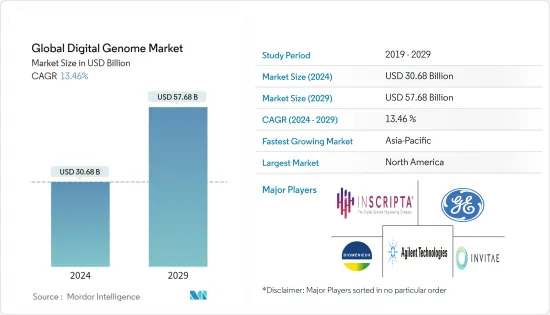

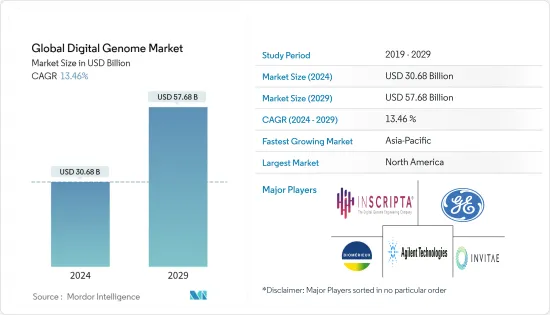

세계의 디지털 게놈 시장 규모는 2024년에 306억 8,000만 달러로 추정되며, 2029년까지 576억 8,000만 달러에 달할 것으로 예측되고 있으며, 예측 기간(2024-2029년) 중 13.46%의 CAGR로 성장합니다.

신종 코로나바이러스 감염증(COVID-19) 팬데믹은 전례 없는 건강 문제이며, 전 세계 디지털 게놈 시장에 큰 영향을 미치고 있습니다. 팬데믹은 디지털 게놈 소프트웨어 및 제품 수요에 긍정적인 영향을 미치고 있습니다. 예를 들어 2022년 2월에 발표된 'COVID-19와 인공지능: 게놈 시퀀싱, 의약품 개발, 백신 발견'이라는 제목의 기사에 따르면 AI의 도움으로 SARS-CoV-2의 염기서열을 확인하고, 델타 균주 및 오믹론으로 우려되는 변종(VOC)을 신속하게 식별할 수 있다고 합니다. 신속하게 식별합니다. 또한 범미보건기구(PAHO)의 2022년 5월 업데이트에 따르면 2020년 COVID-19 감염병 유전체 감시 지역 네트워크가 설립되어 참여 연구소의 시퀀싱 능력을 강화할 뿐만 아니라 루틴을 확립했습니다. SARS-CoV-2 게놈 시퀀싱은 국제 사회가 이용할 수 있는 유전자 염기서열 데이터의 양을 늘리는 전략으로 진단 프로토콜 개발, 백신 개발을 위한 정보 지원, 진화 및 분자 역학을 더 깊이 이해하기 위해 중요합니다. SARS-CoV-2의. 또한 백신의 도입과 봉쇄 제한이 강화됨에 따라 시장에서 디지털 게놈 제품에 대한 수요가 증가하여 시장 성장에 기여할 것으로 예상됩니다.

시장 성장을 가속하는 주요 요인은 디지털 게놈 관련 기술의 발전, 맞춤형 의료의 채택 증가, 끊임없이 진화하는 질병 패턴, 디지털 게놈에 대한 연구개발 활동 증가입니다.

디지털 게놈 관련 기술의 발전으로 시장은 빠르게 성장하고 있습니다. 예를 들어 2021년 7월 GE헬스케어와 세계 헬스케어 데이터 공유 네트워크인 SOPHiA GENETICS는 게놈 기반 AI를 개발하여 암 치료의 발전을 위해 협력했습니다. 유전체학 기반 인공지능을 종양학 워크플로우 솔루션에 통합하는 것은 새로운 치료법에 반응할 가능성이 가장 높은 환자를 선택하는 능력에 점점 더 의존하고 있는 통합 암 치료와 미래 임상 연구에 획기적인 발전이 될 것입니다.

또한 2021년 4월, 유전학 및 유전체학을 일상 진료에 도입하는 디지털 헬스 기업 게놈 메디컬(Genome Medical)은 전국 규모의 유전학 전문가 팀이 제공하는 임상 서비스를 강화하기 위해 기술을 확장했습니다. Genome Medical은 Health Heritage, 가족력 및 유전체 의사결정 지원 용도의 독점 라이선싱을 통해 환자의 종합적인 가족력 수집을 자동화하고, 그 결과를 정확하고 시기적절한 유전적 위험 평가에 통합합니다.

그러나 고가의 설비 투자와 숙련된 노동력 부족이 시장 성장을 저해하는 요인으로 작용하고 있습니다.

제품별로는 세분화된 시퀀싱 및 분석 소프트웨어가 주요 시장 점유율을 차지할 것으로 예상됩니다. 염기서열 분석은 DNA, RNA 또는 펩티드 서열을 다양한 분석 방법을 적용하여 그 특성, 기능, 구조 또는 진화를 이해하는 과정이며, 사용되는 방법론에는 서열 정렬 및 생물학적 데이터베이스에 대한 검색 등이 포함됩니다. 시장 성장을 가속하는 주요 요인은 시퀀싱 분석에 대한 연구 증가와 기술 발전입니다.

일부 시장 기업도 시장 성장에 기여하고 있습니다. 예를 들어 2020년 7월, Illumina, Inc.는 TruSight 소프트웨어 제품군을 출시하여 전체 게놈 시퀀싱 도입을 가속화하고 촉진하는 턴키 데이터 분석 솔루션을 도입했습니다.

또한 NanoString Technologies, Inc.는 2022년 5월, Illumina NextSeq 1000 및 NextSeq 2000 시퀀싱 시스템과 GeoMx 디지털 공간 프로파일러를 사용하는 고객의 공간 데이터 분석 경험을 향상시키기 위해 클라우드 기반의 원활한 워크플로우를 출시하였다고 밝혔습니다.

따라서 위의 발전으로 인해 시장은 예측 기간 중 상당한 성장을 이룰 것으로 예상됩니다.

북미는 암과 같은 만성질환의 발생률 증가, 정부 기관의 연구 투자 증가, 환자 인식 개선, 고급 의료 인프라의 가용성 등으로 인해 예측 기간 중 전체 유전체학 시장을 지배할 것으로 예상됩니다. 이 지역의 생명공학 관행에 대한 수요 증가는 이 지역의 성장을 가속할 것으로 예상됩니다. 일부 주요 기업이 이 지역에 기반을 두고 있는 것도 이 지역의 우위를 확보하는 데 도움이 되고 있습니다.

현재 세계 팬데믹은 이 분야에서 사업을 운영하는 국내 시장 기업에게 큰 기회를 가져다주었습니다. 예를 들어 2021년 3월 Applied DNA Sciences Inc.는 미국에서 SARS-CoV-2 변종을 추적하기 위해 제한된 차세대 염기서열 분석(NGS) 리소스의 유용성을 높이기 위해 Linea COVID-19 선택적 게놈 모니터링 변이 패널을 출시했습니다. 시작했습니다. 지역, 주 및 연방 차원의 우려(VOC)가 개선되었습니다.

2021년 4월, 디지털 게놈 엔지니어링 회사 인스크립타(Inscripta)는 Onyx 플랫폼의 첫 상업적 출하를 발표했습니다. 이 플랫폼은 게놈 규모의 엔지니어링을 위한 세계 최초의 완전 자동화된 벤치탑 장비입니다. Inscripta는 또한 1억 5 ,000만 달러의 시리즈 E 자금 조달을 발표했습니다.

따라서 위의 발전으로 인해 시장은 예측 기간 중 상당한 성장을 보일 것으로 예상됩니다.

디지털 게놈 시장은 여러 세계 및 국제 시장 기업이 존재하기 때문에 경쟁이 치열합니다. 주요 기업은 파트너십, 계약, 협업, 신제품 출시, 지역적 확장, 합병, 인수합병 등 다양한 성장 전략을 채택하여 시장 입지를 강화하기 위해 노력하고 있습니다. 시장의 주요 기업에는 bioMerieux, Agilent Technologies, Inscripta, Inc., GE Healthcare, Invitae Corporation 등이 있습니다.

The Global Digital Genome Market size is estimated at USD 30.68 billion in 2024, and is expected to reach USD 57.68 billion by 2029, growing at a CAGR of 13.46% during the forecast period (2024-2029).

The COVID-19 pandemic is an unprecedented health concern and has significantly impacted the digital genome market worldwide. The pandemic has positively impacted the demand for digital genome software and products. For instance, as per a February 2022 published article titled, "Covid-19 and Artificial Intelligence: Genome sequencing, drug development, and vaccine discovery", the sequence of SARS- CoV-2 was identified with the help of AI and also aids in the prompt identification of variants of concern (VOC) as delta strains and Omicron. In addition, as per a May 2022 update by the Pan American Health Organization (PAHO), the COVID-19 Genomic Surveillance Regional Network was created in 2020 not only to strengthen the sequencing capacity in the participating laboratories but also for them to establish a routine SARS-CoV-2 genomic sequencing, as a strategy to increase the amount of genetic sequence data available to the global community, which is critical to support the development of diagnostic protocols, the information for vaccine development and to better understand the evolution and molecular epidemiology of the SARS-CoV-2. Moreover, with the introduction of vaccines and the upliftment of lockdown restrictions, the market is expected to increase the demand for digital genome products, thereby contributing to market growth.

The major factors fueling the market growth are the increasing technological advancements pertaining to the digital genome, growing adoption of personalized medicine, constantly evolving disease patterns as well as rising research and development activities about the digital genome.

The increasing technological advancement pertaining to the digital genome is proliferating market growth. For instance, in July 2021, GE Healthcare and SOPHiA GENETICS, a global healthcare data-sharing network, collaborated on advancing cancer care by developing genomic-based AI. The integration of genomics-based artificial intelligence into oncology workflow solutions would be a breakthrough for integrated cancer medicine and for future clinical research, which increasingly depends on the ability to select those patients most likely to respond to new therapies.

In addition, in April 2021, Genome Medical, a digital health company bringing genetics and genomics into everyday care, expanded its technology offering to augment the clinical services provided by its nationwide team of genetics specialists. Genome Medical will automate the collection of a patient's comprehensive family health history and incorporate the findings into an accurate and timely genetic risk assessment rough an exclusive licensing of Health Heritage, a family medical history, and genomic decision support application.

However, high capital expenditure and a lack of a skilled workforce are the factors hindering the market growth.

By product, sequencing and analysis software segmented is expected to hold a major market share. Sequence analysis is the process of subjecting a DNA, RNA, or peptide sequence to any of a wide range of analytical methods to understand its features, function, structure, or evolution, and methodologies used include sequence alignment and searches against biological databases and others. The major factors fueling the market growth are the increasing research in sequence analysis as well as growing technological advancements.

Several market players are also contributing to the market growth. For instance, in July 2020, Illumina, Inc. introduced turn-key data analysis solutions to accelerate and facilitate the adoption of whole-genome sequencing with the launch of the TruSight Software Suite.

Also, in May 2022, NanoString Technologies, Inc. launched a seamless, cloud-based workflow that improves the spatial data analysis experience of customers using Illumina NextSeq 1000 and NextSeq 2000 sequencing systems and the GeoMx Digital Spatial Profiler.

Thus, due to the above-mentioned developments, the market is expected to witness significant growth over the forecast period.

North America is expected to dominate the overall genomics market throughout the forecast period due to the rising incidence of chronic diseases, such as cancer, increasing government entities' investment in research, raising awareness of patients, and the availability of advanced healthcare infrastructure, contributing to the growing technological advances in this sector and rising demand for biotechnological practices in the region, is anticipated to drive the growth in the region. The domicile presence of some of the major players in the region also ensures the dominance of the region.

The current global pandemic created considerable opportunities for the domestic market players operating in the space. For instance, in March 2021, Applied DNA Sciences Inc. launched the Linea COVID-19 Selective Genomic Surveillance Mutation Panel to enhance the utility of limited Next Generation Sequencing (NGS) resources in the United States to track the SARS-CoV-2 Variants of Concern (VOCs) better at local, state, and federal levels.

In April 2021, Inscripta, a digital genome engineering company, announced the first commercial shipment of its Onyx platform. The platform is the world's first fully automated benchtop instrument for genome-scale engineering. Inscripta also announced its Series E funding of USD 150 million.

Thus, due to the above-mentioned developments, the market is expected to witness significant growth over the forecast period.

The digital genome market is competitive with the presence of several global and international market players. The key players are adopting different growth strategies to enhance their market presence, such as partnerships, agreements, collaborations, new product launches, geographical expansions, mergers, and acquisitions. Some of the key players in the market are bioMerieux, Agilent Technologies, Inscripta, Inc., GE Healthcare, and Invitae Corporation.