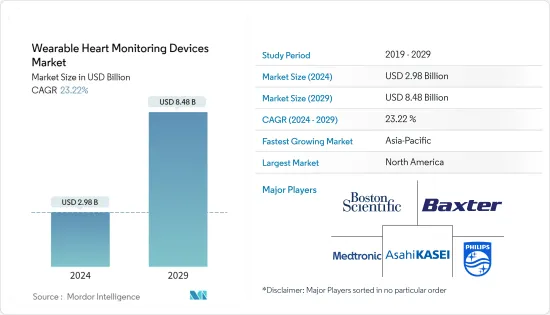

웨어러블 심장 모니터링 디바이스 시장 규모는 2024년에 29억 8,000만 달러로 추정되고, 2029년까지 84억 8,000만 달러에 이를 것으로 예측되며, 예측 기간(2024-2029년) 동안 23.22%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다.

COVID-19 감염의 팬데믹 중에 코로나 바이러스에 감염된 환자는 심장 질환을 일으킬 가능성이 높았으며, 반대로 마찬가지로 위험이 증가했습니다. 이는 심혈관 질환의 실시간 모니터링으로 COVID-19 감염으로 인한 사망률이 효과적으로 저하되었기 때문에 웨어러블 심장 모니터링 디바이스에 대한 수요가 높아제게 되었습니다. 예를 들어, 2021년 2월에 JMIR 출판물에 게시된 기사에 따르면, 웨어러블 디바이스는 기존 진단 방법보다 빨리 신형 COVID-19를 확인할 수 있어 질병 관리를 추적하고 개선하는 데 도움이 되었슷ㅂ니다. 비강 PCR에 의한 COVID-19의 동정 전에 심박수 변동(HRV)의 유의한 변화가 관찰되었으며, 이는 비강 PCR이 COVID-19 감염을 진단할 예측 능력이 있음을 시사했습니다. 그러나 일부 환자에서는 COVID-19 감염의 영향 후에도 심장 문제가 오래 지속되었습니다. 예를 들어, 2022년 2월에 Nature 저널에 게재된 논문에 따르면 COVID-19증에서 회복된 사람들은 감염 후 1년 동안 심혈관계 문제가 현저하게 증가한 것으로 나타났습니다. 따라서 심장병 환자들 사이에서 웨어러블 기술에 대한 의식이 지속적으로 증가하고 있으며, 웨어러블 심장 모니터링 디바이스 시장은 가까운 미래에 빠르게 확대될 것으로 예상됩니다.

시장 성장을 가속하는 특정 요인으로는 심부전율 증가, 웨어러블 기반 심장 모니터링에 대한 의식 증가, 웨어러블 디바이스 기술 발전 등이 있습니다. 2022년 10월에 발표된 CDC의 최신 정보에서 관상 동맥 성 심장 질환은 가장 흔한 유형의 심장 질환이며 20세 이상 성인 약 2,010만 명(약 7.2%)이 관상 동맥 질환을 앓고 있다고 말합니다. 따라서 관상 동맥 질환의 높은 부담이 시장 성장을 가속하고 있습니다. 또한 '2022 Spotlight on Heart Failure' 보고서에 따르면 매년 10만 명 이상의 캐나다인이 심부전으로 진단됩니다. 같은 출처에 따르면, 심부전으로 인한 캐나다 손실은 연간 28억 달러를 초과할 수 있습니다. 따라서, 심부전 증가 및 건강 관리비 증가는 비용을 절감하고 심장 모니터링을 개선하는 웨어러블 기술에 기초한 심장 모니터링 장치가 요구되고 있습니다.

또한 2021년 1월 보스턴 사이언티픽은 Preventice Solutions를 9억 2,500만 달러로 인수했습니다. Preventice Solutions는 원격 환자 모니터링에 사용되는 여러 웨어러블 심장 센서(BodyGuardian) 제조업체입니다. 이 장비는 성인 환자뿐만 아니라 소아 환자를 위해 개발되었습니다. 따라서 이 인수를 통해 보스턴 사이언티픽은 핵심 심조율 관리 및 전기 생리학 사업 부문을 확대하여 이 매력적인 시장에서의 입지를 강화하였습니다.

또한 리듬 메딕스는 2021년 2월 'RhythmStar'라는 최신 세대의 웨어러블 심전도 모니터를 출시했습니다. 이 기기에는 휴대전화 연결이 내장되어 있어 자체적으로 ECG 기록을 수집하고 전화를 사용하지 않고 의사에게 데이터를 무선으로 전송할 수 있습니다. 이 간소화되고 시간이 절약된 접근 방식은 더 많은 고객을 매료시켜 시장 잠재력을 높일 수 있습니다. 따라서, 웨어러블 디바이스에서의 첨단 기술 채용 증가는 환자와 의사가 더 나은 방식으로 심장 문제를 관리하는 데 도움이 되는 이점을 포함하여 시장 성장에 기여합니다.

따라서 심장 합병증 증가와 심장 모니터링 웨어러블 제품의 출시 증가로 웨어러블 심장 모니터링 디바이스 시장은 예측 기간 동안 성장할 것으로 예상됩니다. 그러나, 웨어러블 디바이스의 프라이버시 및 보안 문제, 엄격한 규칙 및 규제 정책은 웨어러블 심장 모니터링 디바이스 시장의 성장을 방해하는 주요 요인입니다.

광학기술 기반 제품 부문은 심혈관 질환(CVD) 유병률 증가, 노인 인구 증가, 제품 승인 증가 등과 같은 요인으로 인해 예측 기간 동안 상당한 성장률을 나타낼 것으로 예상됩니다. 기반 제품은 포토플리티스모그래피(PPG)라는 방법을 기반으로 합니다. 피부에 빛을 비추고 혈류에 의해 산란되는 빛의 양을 측정하여 심박수를 측정합니다. 최근에는 심박수를 지속적으로 모니터링하기 위해 광학 기술을 기반으로 한 웨어러블 장치가 널리 관심을 끌고 있습니다. 기능이 간단하기 때문에 소비자에게 직접 사용할 수 있으며 의료진과의 직접적인 접촉이 줄어들고 전기 펄스 기반 제품에 비해 저렴합니다.

또한 영국 정부의 건강개선 및 격차국에 따르면 2020-21년 NHS 버킹과 다게남 CCG의 만성 심질환에 의한 입원률은 인구 10만명당 427.9명(입원수 580명)이었습니다. 이는 영국의 비율(10만명당 368명)보다 훨씬 높았습니다. 따라서 심혈관 합병증 증가는 심장 모니터링에 대한 수요를 증가시켜 예측 기간 동안 부문의 성장을 가속시킵니다. 대부분의 CVD는 심박수를 실시간으로 모니터링하여 억제할 수 있으며, 이는 사망률과 치료비 절감에 중요한 역할을 합니다. 예를 들어, 2021년 11월 미국 심장협회(AHA)가 발표한 데이터에 따르면, ECG 패치 모니터에서 확인된 바와 같이 Fitbit PPG 검출은 98%의 확률로 심방세동(AF) 이벤트를 확인했습니다. 따라서 PPG 알고리즘의 효율성 향상으로 향후 수년간 광학 기술 기반 제품 수요가 증가하여 시장 성장에 기여할 것으로 예상됩니다.

게다가 많은 시장 기업들이 전략적 노력의 실행에 초점을 맞추어 웨어러블 심장 모니터링 디바이스 시장의 성장에 기여하고 있습니다. 예를 들어, 2022년 4월에 Google 소유 Fitbit은 AF를 식별하기 위한 'AFib'라는 새로운 광전맥파계(PPG) 알고리즘의 제품 승인을 FDA에서 받았습니다. 이 알고리즘은 Fitbit 기기의 새로운 불규칙한 심박 리듬 알림 기능을 향상시킬 수 있습니다. 따라서 웨어러블 심장 모니터링 디바이스를 위한 광학 기술 기반 제품의 주요 기업이 제공하는 발전으로 이 시장 부문은 예측 기간 동안 상당한 성장을 이룰 것으로 예상됩니다.

따라서 심장병 증가 및 광학기술 기반 심장 모니터링 웨어러블 제품의 출시가 급증함에 따라 시장 조사 대상 부문은 예측 기간 동안 성장할 것으로 예상됩니다.

북미는 웨어러블 심장 모니터링 디바이스 시장에서 큰 점유율을 차지하고 있는 것으로 보입니다. 이는 CVD 발생률 증가, 주요 시장 기업의 존재 및 전략적 노력 등의 요인 때문입니다. 예를 들어 CARES 2021 연례 보고서에 따르면 미국에서는 남성의 62.5%가 원외심정지(OHCA)를 일으켰다고 보고되었습니다. 같은 출처에 따르면 2021년 미국에서 성인의 97.6%와 어린이의 2.4%가 OHCA를 경험했습니다. 따라서 심장 합병증의 수가 증가함에 따라 웨어러블 심장 모니터링 디바이스에 대한 수요가 증가하고 예측 기간 동안 시장 성장을 가속합니다.

정부의 이니셔티브와 웨어러블 심장 모니터링 장비 시장의 성장으로 인해 대기업은 이 업계에 초점을 맞추고 전략적 이니셔티브를 이행하기 위해 노력하고 있습니다. 예를 들어, 의료 진단 및 소비자 헬스케어 기술 회사인 Biotricity Inc.는 2022년 3월에 FDA의 승인을 받은 무선 웨어러블 심장 모니터링 디바이스 Biotres를 출시했습니다. 이 제품은 2022년 2월 하순부터 의사, 진료소, 병원, 개인용으로 제공을 개시했습니다.

또한 2022년 8월 삼성캐나다는 디지털 헬스의 다음 시대를 추진하는 삼성의 독자적인 BioActive Sensor 기술을 탑재한 Galaxy Watch5 및 Galaxy Watch5 Pro를 출시했습니다. Samsung BioActive 센서(광학 심박수 전기 심장 신호 생체 전기 임피던스 분석), 온도 센서, 가속도계, 기압계, 자이로 센서, 지자기 센서, 광 센서가 포함되어 있습니다.

따라서 심장병 증가 및 심장 모니터링 웨어러블 제품의 출시가 급증함에 따라 북미는 예측 기간 동안 크게 성장할 것으로 예상됩니다.

웨어러블 심장 모니터링 디바이스 시장은 매우 세분화되어 있으며 여러 주요 기업으로 구성되어 있습니다. 시장 점유율의 점에서 현재, 몇몇 대기업은 시장을 독점하고 있습니다. 현재 시장을 장악하고 있는 회사로는 Medtronic plc, iRhythm Technologies, Inc., Baxter, Vital Connect, Inc., Asahi Kasei Corporation (ZOLL Medical Corporation), Koninklijke Philips N.V. (BioTelemetry, Inc.), Hemodynamics Company LLC, ACS Diagnostics, Inc., General Electric Company (GE Healthcare, Inc.), Boston Scientific (Preventice Solutions, Inc.), Qardio, Inc., Heartbit Holdings Plc. 등이 있습니다.

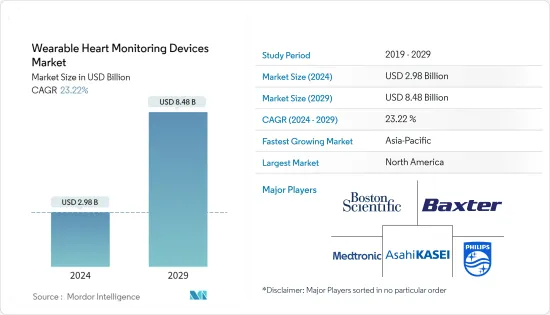

The Wearable Heart Monitoring Devices Market size is estimated at USD 2.98 billion in 2024, and is expected to reach USD 8.48 billion by 2029, growing at a CAGR of 23.22% during the forecast period (2024-2029).

During the COVID-19 pandemic, coronavirus-infected patients were more likely to develop heart problems and vice-versa, which increased the risk. This was attributed to the rising demand for wearable heart monitoring devices, as the real-time monitoring of cardiovascular disease effectively reduced COVID-19 mortality rates. For instance, as per the article published in February 2021 in JMIR publications, wearable devices can identify COVID-19 cases earlier than traditional diagnostic methods and can help track and improve the management of the disease. Significant changes in heart rate variability (HRV) were seen before the identification of COVID-19 by nasal PCR, suggesting its predictive capacity to diagnose COVID-19 infection. However, for some patients, heart problems persisted long after the impact of COVID-19 infection. For instance, as per the article published in February 2022 in Nature journal, people who had recovered from COVID-19 showed stark increases in cardiovascular problems over the year after infection. Therefore, the awareness of wearable technology among cardiac patients is constantly rising, and the wearable heart monitoring devices market will see rapid expansion in the near future.

Certain factors that are driving the market growth include the increasing rate of heart failure, rising awareness of wearables-based cardiac monitoring, and technological advancements in wearable devices. The CDC update published in October 2022 stated that coronary heart disease is the most common type of heart disease, and around 20.1 million adults aged 20 and older have coronary artery disease (approximately 7.2%). Thus, the high burden of coronary artery disease is driving the growth of the market. Further, as per the 2022 Spotlight on Heart Failure report, more than 100,000 Canadians are diagnosed with heart failure each year. As per the same source, Heart failure is likely to cost Canada more than USD 2.8 billion a year. Therefore, the rising cases of heart failure and increasing healthcare cost demands heart monitoring devices based on wearable technology to reduce the cost and improves heart monitoring.

In addition, in January 2021, Boston Scientific acquired Preventice Solutions for USD 925 million. Preventice Solutions is a manufacturer of several wearable cardiac sensors (BodyGuardian) used for remote patient monitoring. These devices are developed for adult as well as pediatric patients. Therefore, from this acquisition, Boston Scientific expanded its business segment of core cardiac rhythm management and electrophysiology which in turn strengthened its position in this attractive market.

Moreover, in February 2021, RhythMedix launched the newest-generation wearable ECG monitor named 'RhythmStar'. This device has built-in cellular connectivity which can collect ECG recordings by itself and send data wirelessly to physicians without the use of a phone. This simplified and time-saving approach may entice more customers and raise their market potential. Thus, the rise in the adoption of advanced technology in wearable devices comprises benefits that help patients and physicians to manage heart problems in a better way, thereby contributing to market growth.

Thus, due to the rise in cardiac complications, and the increase in heart-monitoring wearable product launches, the wearable heart-monitoring devices market is anticipated to witness growth over the forecast period. However, privacy & security issues of wearable devices and stringent rules and regulatory policies are major factors hindering the wearable heart monitoring devices market's growth.

The optical technology-based product segment is anticipated to register a significant growth rate during the forecast period owing to the factors such as the rise in the prevalence of cardiovascular diseases (CVDs), the growing geriatric population, and the rising product approvals This optical technology-based product is based on a method called photoplethysmography (PPG). It measures heart rate by shining light into the skin and measuring the amount of light that is scattered by blood flow. These days, wearable devices based on optical technology are gaining wide interest for continuous monitoring of the heart rate. Attributable to its uncomplicated features, available direct-to-consumer, reduce direct contact with clinical staff, and is inexpensive as compared to electric pulse-based products.

Further, according to the Government of the UK, Office of Health Improvement & Disparities, in 2020-21 the admission rate for chronic heart disease in NHS Barking and Dagenham CCG was 427.9 for every 100,000 people in the population (580 admissions). This was significantly higher than the England rate (368 per 100,000). Thus, the rise in cardiovascular complications increases the demand for heart monitoring thereby driving the segment growth over the forecast period. Most CVDs can be inhibited by real-time monitoring of heart rate, which plays a vital role in reducing the mortality and cost of treatment. For instance, data published by American Heart Association (AHA) in November 2021 found that the Fitbit PPG detections identified atrial fibrillation (AF) events 98% of the time, as confirmed by ECG patch monitors. Thus, the rising efficiency of the PPG algorithm is expected to increase the demand for optical technology-based products in the coming years, thereby contributing to market growth.

In addition, numerous market players are focused on the execution of strategic initiatives, thereby contributing to the growth of the wearable heart monitoring devices market. For instance, in April 2022, Google-owned Fitbit received product approval from the FDA for a new photoplethysmography (PPG) algorithm named 'AFib' to identify AF. This algorithm is likely to power a new irregular heart rhythm notification feature on the Fitbit device. Therefore, due to the advancements offered by the key players in optical technology-based products for wearable heart monitoring devices, this market segment is expected to witness significant growth during the forecast period.

Hence, due to the increase in cardiac diseases, and the surge in optical technology-based cardiac monitoring wearable product launches, the studied segment in the market is anticipated to witness growth over the forecast period.

North America is likely to hold a significant share of the wearable heart monitoring devices market. This is due to factors such as the rising incidences of CVDs and the presence of major market players and their strategic initiatives. For instance, as per the CARES 2021 annual report, 62.5% of males were reported with out-of-hospital cardiac arrest (OHCA) in the United States. As per the same source, 97.6% of adults and 2.4% of children experienced OHCA in 2021 in the United States. Thus, as the number of cardiac complications increases, the demand for wearable heart monitoring devices rises and drives the market growth over the forecast period.

Due to government initiatives and the growing nature of the wearable heart monitoring device market, the major players have shifted their focus in this industry and engaged in the implementation of strategic initiatives. For instance, in March 2022, Biotricity Inc., a medical diagnostic and consumer healthcare technology company, launched its FDA-cleared, wireless wearable cardiac monitoring device, Biotres. The product was available for physicians, medical offices, hospitals, and individual use since late-February 2022.

Furthermore, in August 2022, Samsung Canada launched the Galaxy Watch5 and Galaxy Watch5 Pro equipped with a unique BioActive Sensor technology from Samsung that drives the next era of digital health. It comes with Samsung BioActive Sensor (Optical Heart Rate + Electrical Heart Signal + Bioelectrical Impedance Analysis), Temperature Sensor, Accelerometer, Barometer, Gyro Sensor, Geomagnetic Sensor, and Light Sensor.

Hence, due to the increase in cardiac diseases, and the surge in cardiac monitoring wearable product launches, North America is anticipated to witness significant growth over the forecast period.

The wearable heart monitoring devices market is highly fragmented and consists of several major players. In terms of market share, a few of the major players are currently dominating the market. Some of the companies which are currently dominating the market are Medtronic plc, iRhythm Technologies, Inc., Baxter, Vital Connect, Inc., Asahi Kasei Corporation (ZOLL Medical Corporation), Koninklijke Philips N.V. (BioTelemetry, Inc.), Hemodynamics Company LLC, ACS Diagnostics, Inc., General Electric Company (GE Healthcare, Inc.), Boston Scientific (Preventice Solutions, Inc.), Qardio, Inc., Heartbit Holdings Plc.