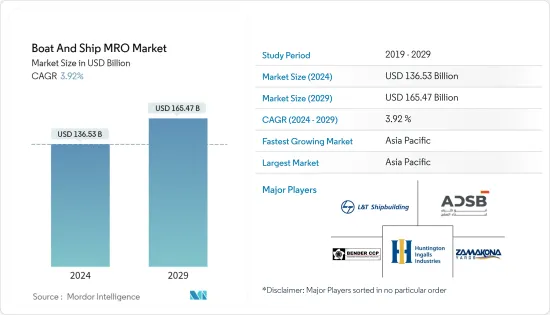

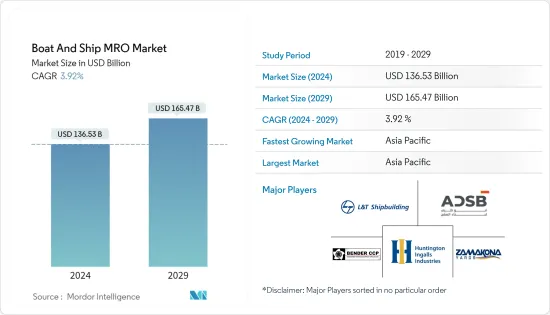

보트 및 선박 MRO 시장 규모는 2024년에 1,365억 3,000만 달러에 이를 것으로 추정됩니다. 2029년까지 1,654억 7,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 3.92%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다.

코로나19 바이러스 감염증의 대유행으로 인해 선박 MRO 시장은 악영향을 받았습니다. 각국 정부의 국가 봉쇄와 국경 폐쇄로 인해 주요 국가 간의 무역 활동이 일시적으로 중단되었습니다. 그러나 각국 정부가 경제 상황을 개선하기 위해 완화 조치를 취함에 따라 향후 몇 달 안에 해상 무역이 회복될 것으로 예상됩니다.

선박 보유량 증가, 신조선 판매 증가, 선박의 평균 연령 증가 등의 요인으로 인해 해양 산업에서 유지보수, 수리, 오버홀 서비스에 대한 수요가 증가하고 있습니다. 국가 간 무역 및 교역 증가로 인해 상선의 이용이 증가하고 그 활약이 활발해지고 있습니다. 이러한 요인으로 인해 계획된 유지보수 및 사후 유지보수에 대한 수요가 증가하여 MRO 시장의 성장을 가속하고 있습니다.

에너지 소비 증가, 친환경 선박 및 운송 서비스에 대한 수요, 조선업의 로봇 공학의 출현과 같은 다른 요인들도 시장 성장을 주도하고 있습니다.

세계 인구가 계속 증가하는 가운데, 특히 신흥국에서 저비용의 효율적인 해상 운송이 성장과 지속 가능한 개발에 중요한 역할을 하고 있기 때문에 해상 운송은 세계 무역과 세계 경제의 근간이 되고 있습니다.

해사 산업은 최근 몇 년동안 국가 선박에 선박이 추가되고 전 세계 민간 기업과 정부 기업이 모두 투자하면서 빠르게 성장하고 있습니다.

세계 선박의 수송능력은 2021년 1월 기준 21억 DWT로 전년 대비 6,300만 DWT 증가하였습니다. 일반 화물 운송업체를 제외하고 톤수는 최근 몇 년동안 크게 증가했습니다. 부정기 운송업체는 빠르게 성장했습니다. 2011 년부터 2021년까지 전체 운송 능력에서 유조선이 차지하는 비율은 39%에서 43%로 증가했지만 유조선의 비율은 31%에서 29%로 감소하고 일반화물의 비율은 6%에서 4%로 증가했습니다. 또한 국제적으로 거래되는 약 56,000척의 상선 중 약 17,000척이 일반 화물선이며, 이는 전 세계 상선 선단의 약 30%를 차지합니다.

규모의 이점을 통해 비용을 최적화하기 위해 선단의 평균 연령과 선박의 크기가 수년에 걸쳐 증가하고 있습니다. 이러한 장기 운항 선박은 정기적이고 지속적인 유지보수 점검이 필요하며, 그 결과 예측 기간 동안 보트 및 선박 MRO 시장이 성장할 것으로 예상됩니다.

2021년 1월 세계 선복량의 52%는 상위 5개국이 차지했습니다. 가장 큰 시장 점유율은 그리스(18%), 중국(12%), 일본(11%), 싱가포르(7%), 홍콩 특별행정구(7%) 순이었습니다. 홍콩 특별행정구(7%). 아시아 기업이 전 세계 톤수의 절반을 소유하고 있었습니다. 유럽 출신 선주가 전체의 40%, 북미 출신 선주가 6%를 차지했습니다. 아프리카, 라틴아메리카, 카리브해 기업은 시장의 1%를 조금 넘는 점유율을 차지했고, 오세아니아는 1% 미만이었습니다.

적재 중량 톤수 기준으로 보면 벌크선이 가장 젊은 선박으로 평균 선령이 9.28년, 컨테이너선(9.91년), 유조선(10.38년)이 그 뒤를 이었습니다. 평균적으로 일반 화물선이 가장 오래된 선종(19.46년)입니다.

이러한 요인 외에도 정부 기관은 전 세계적으로 다른 민간 기업과 합작 사업을 시작하여 보유 차량의 역량을 강화하고 있습니다.

2021년 9월, 라센 앤 투브로(L&T)는 영국 해군으로부터 함대 고체 지원함 설계 및 개발 계약을 수주했습니다. L&T는 영국 해군의 물류 부문인 영국 왕립 함대 보조 부대를 위해 새로운 함대 고체 지원(FSS) 함정 3척을 건조하는 계약을 체결했습니다.

2021년 7월, COSCO Shipping Holdings는 15억 달러에 10척의 신규 컨테이너선박을 발주하여 선복량을 운항 중인 선대의 거의 15%까지 확대했습니다. Cosco Shipping과 OOCL의 모회사는 2023년 12월부터 2024년 9월까지 인도 예정인 14,092TEU급 선박 6척을 미화 8억7600만 달러에 발주하고, 자회사가 건조할 16,180TEU급 선박 4척을 미화 6억 2,000만 달러에 발주할 것이라고 발표했습니다. Cosco의 제품으로 2025년 6월부터 12월까지 인도될 예정입니다.

아시아태평양에는 인도, 중국 등 강력한 신흥 경제국들이 자리 잡고 있으며, 현재 국제 수출을 늘리기 위해 투자를 늘리고 있습니다. 이 지역에서는 강력한 모터보트가 대규모로 도입되면서 어업도 급성장하고 있습니다. 아시아태평양 국가들은 해적 행위와 국경 침범에 대응하기 위해 기존 해군을 현대화하기 위해 많은 투자를 하고 있습니다.

이 지역에 존재하는 함대의 대부분은 적시에 수리 및 유지 보수가 필요한 오래된 선박으로 구성되어 있습니다. 인도 해군은 지난 몇 년동안 예상치 못한 선박 고장 사고가 발생했습니다.

중국은 2020년 군사비 지출에서 세계 2위를 차지했습니다. 그러나 2020년 국방비 지출을 GDP 대비 약 -1.7% 줄였습니다. ?33? GDP ?35? GDP ?34? 중국 정부는 올해 국방예산을 전년 대비 0.5% 증액했습니다. ?33? year ?35?년?34? 국방 예산이 처음으로 2,000억 달러를 넘어섰습니다. ?33?% ?35?% ?34? 인민해방군에는 약 500여 척의 선박과 230여 척의 보조 선박이 소속되어 있습니다. 이 나라의 상선단에는 6,459척의 다양한 선박이 포함되어 있습니다. 선박 유지 보수 및 수리 산업은 이 지역의 주요 산업 중 하나입니다. 이 나라의 조선소는 세계 각지에서 온 컨테이너 운반선 및 기타 선박의 대량 운송을 처리합니다.

인도 정부는 선박 MRO 시장을 활성화하기 위해 업계 세액표를 수정하는 등 필요한 조치를 취하고 있습니다. 예를 들어,

2021년 6월, 국방부는 수중 전투 능력을 강화하기 위해 공격형 핵잠수함 6척을 포함한 24척의 새로운 잠수함을 인수할 계획을 발표했습니다.

2021년 5월 정부는 싱가포르 등 경쟁국과 세율을 맞추기 위해 해운 부문의 MRO(Maintenance, Repair, Overhaul) 서비스에 대한 GST를 현행 18%에서 5%로 인하할 계획을 발표했습니다. 이 분야에서는 아랍에미리트(UAE)와 스리랑카가 참여하고 있습니다.

이 지역에는 수많은 IT 및 기술 기업이 존재하며, 가상현실, 증강현실, 복합 현실, 증강현실과 같은 기술의 성장을 가속하고 있습니다. 이러한 기술은 이 지역의 보트 및 선박 MRO 시장을 크게 견인할 것으로 예상됩니다.

인도 정부의 최신 기술 선박 조달을 위한 국방부 지출 증가와 선박 MRO 산업을 촉진하기 위한 개혁으로 인해 수요는 예측 기간 동안 증가할 것으로 예상됩니다.

보트 및 선박 MRO 시장은 다소 세분화되어 있으며, Larsen and Toubro Shipbuilding Limited, Huntington Ingalls Industries, Abu Dhabi Ship Building Company와 같은 대기업들이 시장을 시장을 독점하고 있습니다.

시장에서는 운송회사와 소프트웨어 회사가 협력하여 비용을 절감하고 유지보수, 수리 및 점검 프로세스를 신속하게 운영할 수 있도록 하는 것을 볼 수 있습니다.

2021년 4월, BAE시스템즈는 포츠머스 함대 전체에 선박 지원 관리, 수리 및 유지보수를 제공하는 9억 파운드 규모의 계약에 따라 영국 해군을 지원한다고 발표했습니다. 또한 KBR과 합작회사를 설립하여 3 억 6,500 만 파운드의 계약에 따라 기지에서 기술 주도 및 데이터 기반 시설 관리 및 부두 서비스를 제공 할 계획이었습니다.

미쓰비시중공업은 2021년 3월 미쓰비시 E&S 홀딩스와 공공선박 사업 및 해군 사업을 인수하는 계약을 체결했습니다.

Maindeck, Nautix Technologies, Closelink와 같은 일부 신생 기업은 데이터 과학 및 클라우드 컴퓨팅과 같은 기술을 통합하여 유지 보수 프로세스를 통해 운영 시간을 단축하기 위해 노력하고 있습니다.

The Boat And Ship MRO Market size is estimated at USD 136.53 billion in 2024, and is expected to reach USD 165.47 billion by 2029, growing at a CAGR of 3.92% during the forecast period (2024-2029).

The boat and ship MRO market was negatively impacted due to the COVID-19 pandemic. Trade activities between leading countries were temporarily shut down due to governments imposing national lockdowns and closing international borders. However, with relaxations allowed by governments to improve economic conditions, marine trade is expected to revive over the next few months.

Factors such as the increasing boat and ship fleet, increasing sales of new boats and ships, and the increase in the average age of a vessel are driving demand for maintenance, repair, and overhaul services in the marine industry. Due to the increase in trade and commerce between various nations, usage of commercial ships has increased, and they are being put more into work. Due to this factor, the need for scheduled maintenance and breakdown maintenance is increasing, propelling the growth of the MRO market.

Other factors like rising energy consumption, the demand for eco-friendly ships and shipping services, and the advent of robotics in shipbuilding are driving the growth of the market.

Maritime transport is the backbone of global trade and the global economy as the world's population continues to grow, particularly in developing countries where low-cost and efficient maritime transport has an essential role in growth and sustainable development.

The maritime industry has been growing rapidly over the recent years with the addition of ships to the national fleet and investments being made by both private and government players worldwide.

The world fleet had a carrying capacity of 2.1 billion dwt in January 2021, up by 63 million dwt from the previous year. With the exception of general freight carriers, tonnage has climbed significantly in recent years. Bulk haulers saw a speedy growth. Between 2011 and 2021, their proportion of the overall carrying capacity increased from 39% to 43%, while oil tankers' share decreased from 31% to 29%, and general cargo's share increased from 6% to 4%. Moreover, of the around 56,000 merchant ships trading internationally, around 17,000 ships were general cargo ships, accounting for roughly 30% of the world's merchant fleet.

The average age of fleet and vessel sizes have been increasing over the years to optimize costs through economies of scale. These long-run ships need regular and continuous maintenance checkups, which is expected to result in the boat and ship MRO market witnessing growth during the forecast period.

The top five ship-owning economies accounted for 52% of the global fleet tonnage in January 2021. Greece had the largest market share (18%), followed by China (12%), Japan (11%), Singapore (7%), and Hong Kong SAR (7%). Asian firms possessed half of the world's tonnage. Owners from Europe made up 40% of the total, while those from northern America made up 6%. Companies from Africa, Latin America, and the Caribbean represented a little over 1% of the market, while Oceania had just under 1%.

In terms of dead-weight tonnage, bulk carriers are the youngest vessels, with an average age of 9.28 years, followed by container ships (9.91 years) and oil tankers (10.38 years). On average, general cargo ships are the oldest vessel type (19.46 years).

Apart from these factors, government organizations are entering into joint ventures with other private players globally to enhance their fleet capacity.

In September 2021, Larsen and Toubro (L&T) won a prestigious contract from the British Royal Navy for developing designs for Fleet Solid Support ships. L&T was awarded the contract to build three new Fleet Solid Support (FSS) ships for the British Royal Fleet Auxiliary, the logistics arm of the British Royal Navy.

In July 2021, Cosco Shipping Holdings placed a USD 1.5 billion order for 10 new container ships, extending the carrier's on-order capacity to almost 15% of its in-service fleet. The parent of Cosco Shipping and OOCL announced a USD 876 million order for six 14,092 TEU ships to be delivered between December 2023 and September 2024, and a USD 620 million order for four vessels of 16,180 TEU that will be built by a wholly-owned subsidiary of Cosco and delivered between June and December 2025.

The Asia-Pacific region is home to strong developing economies such as India and China, which are now investing more to boost their international exports. The fishing industry has also boomed in the region due to the large-scale adoption of powerful motorized boats. The countries in the Asia-Pacific region are also investing heavily to modernize their existing naval fleets to counter piracy and sea border violation activities.

A large portion of the fleet present in this region consists of old ships that need timely repairs and maintenance. Indian Navy has witnessed incidents of the untimely breakdown of their vessels over the past few years.

China ranked 2nd globally in terms of spending on the military in 2020. However, the country reduced its defense spending during 2020 by around -1.7% of its GDP. In 2021, the government hiked its defense budget by 6.8% from the previous year. The defense budget crossed the USD 200 billion mark for the first time. There are around 500 different types of vessels and 230 auxiliary ships fleet with the People's Liberation Army of the country. The commercial fleet of the country includes 6,459 units of different marine vessels. The ship maintenance and repairing industry is one of the leading industries in the region. The shipyards in the country handle huge traffic of container carriers and other ships from different parts of the world.

The Indian government is taking necessary steps to boost the ship MRO market by making necessary amendments to the tax slab for the industry. For instance,

In June 2021, the Ministry of Defence announced that it was planning to acquire 24 new submarines, including six nuclear attack submarines, to bolster its underwater fighting capability.

In May 2021, the government announced that it was planning to reduce GST on maintenance, repair, and overhaul (MRO) services in the shipping sector from the current 18% to 5% in order to align the tax rates with competing nations like Singapore, the United Arab Emirates (UAE), and Sri Lanka in the sector.

The presence of a large number of IT and technology firms in the region is fueling the growth of technologies, such as Virtual Reality, Augmented Reality, Mixed Reality, and Extended Reality. These technologies are expected to significantly drive the Boat and Ship MRO market in the region.

With increased spending in the defense sector from the Government of India in procuring the latest technology marine vessels and reforms to boost the ship MRO industry, the demand is expected to grow during the forecast period.

The boat and ship MRO market is slightly fragmented, with major players such as Larsen and Toubro Shipbuilding Limited, Huntington Ingalls Industries, and Abu Dhabi Ship Building Company dominating the market.

The market is witnessing collaborations among shipping and software companies, leading to cost reduction and rapid operational execution of maintenance, repair, and overhaul processes.

In April 2021, BAE Systems announced that it would deliver ship assist management, repair, and maintenance for the entire Portsmouth flotilla, supporting the Royal Navy under a GBP 900 million contract. It also planned to establish a joint venture with KBR to deliver technology-led and data-driven facilities management and dockside services at the base under a GBP 365 million contract.

In March 2021, Mitsubishi heavy industries signed an agreement with Mitsubishi E&S Holdings to take over government ship business and naval services with Mitsubishi E&S Holdings.

Several startups such as Maindeck, Nautix Technologies, and Closelink are working toward integrating technologies such as data science and cloud computing, with maintenance processes boosting the reduction in operational time.