ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

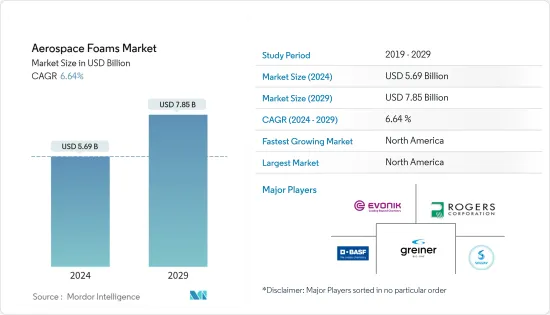

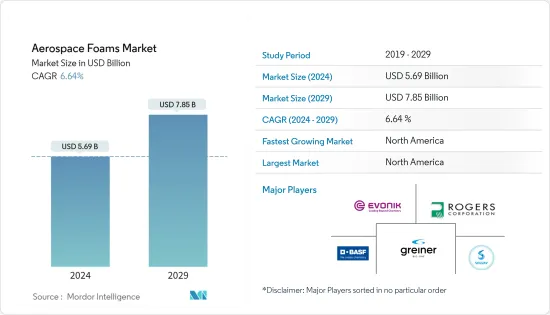

항공우주용 폼 시장 규모는 2024년 56억 9,000만 달러로 추정되고, 2029년까지 78억 5,000만 달러에 이를 것으로 예측되며, 예측 기간 동안 복합 연간 성장률(CAGR) 6.64%로 성장할 전망입니다.

주요 하이라이트

2020년 시장은 COVID-19에 의해 악영향을 받았습니다. 팬데믹의 영향으로 여객 수요가 침체되었기 때문에 그에 따른 여행 제한과 경기 후퇴로 인해 항공사는 비용 절감 방법을 모색할 필요가 있었습니다. 항공기 발주 중지 및 연기 등의 비용 절감책이 실시되었습니다. 그러나 2021년과 2022년에 제한이 해제되자마자 여행이 증가하여 항공화물 수요가 증가했습니다.

단기적으로 조사 대상 시장을 추진하는 주요 요인은 가볍고 연료 효율이 높은 항공기에 대한 수요 증가입니다. 폴리우레탄(PU) 폼의 제조는 여전히 석유에 대한 의존도가 높아, 이것이 시장 성장 억제요인이 되고 있습니다.

바이오 폴리우레탄 폼 제조에 대한 동향 증가는 예측 기간 동안 시장에 기회가 될 수 있습니다. 예측 기간 동안 북미가 시장을 독점할 것으로 예상됩니다.

항공우주 폼 시장 동향

민간항공에서 수요 증가

연료 가격 변동의 감소와 운항 효율의 향상은 지난 몇 년간 민간 항공기 운항의 성장을 지원해 왔습니다. 주로 아시아태평양과 남미 신흥 경제국에서 항공 여행 요금의 상승과 세계 가처분 소득 증가가 세계 항공기 보유 수 증가를 추진하고 있습니다.

승객 수 증가와 퇴직자 증가는 향후 20년간 6조 8,000억 달러에 해당하는 44,040대의 새로운 제트기의 필요성을 높일 것으로 예상됩니다. 세계 상용 항공기는 2038년까지 50,660대에 이를 것으로 예상됩니다.

또한 Boeing상업시장 전망 2022-2041에 따르면 2031년까지 항공기는 연률 2.6%로 상용기재를 증가시켰으며 운항기수는 35,400대에 이르며 2041년까지 이 수는 47,080대에 이르며 연간의 비율로 2019년에서 2041년의 기간은 2.8%.

게다가 2022년부터 2041년까지의 라틴아메리카에 있어서의 민간 항공기에의 신규 항공기 납입은 납입 총수에 차지하는 비율이 5%, 중동이 7%, 북미가 23%, 아시아가 21%, 유럽이 21%가 된다 합니다.

앞서 언급한 모든 요인들은 앞으로 수년간 이러한 항공기 제조 중 항공우주용 양식에 대한 수요를 증가시켜 조사 대상 시장이 확대될 것으로 예상됩니다.

북미가 시장을 독점

북미는 항공우주 산업을 위한 세계 최대 시장입니다. 북미 항공우주 제조업체는 최근 지역의 항공 승객 수 증가와 군사 지출 증가로 인해 사업을 확대할 것으로 예상됩니다.

미국은 북미 최대 항공 시장이며 세계 최대 규모의 항공기 규모를 가지고 있습니다. 따라서 항공우주 양식의 가장 큰 시장 중 하나입니다. 연방항공국(FAA)에 따르면 항공화물 증가로 민간 항공기의 총 보유 수는 2037년 8,270대에 이를 것으로 예상됩니다. 또한 미국 메인 라이너 항공 모함 함대는 기존 함대가 노후화되어 연간 54대의 비율로 증가할 것으로 예상됩니다.

2022년 국방예산에서 미국 정부는 국방 프로그램에 7,682억 달러를 인정했는데, 이는 바이덴 정권의 당초 예산 요구보다 약 2% 증가했으며, 이 분야에서 항공우주재료 사용이 증가하고 있음을 보여줍니다.

Boeing의 상업 전망 2022-2041에 따르면 북미에서는 항공 여행의 13%가 비즈니스 목적, 50%가 레저, 37%가 친구와 친척을 방문하기 위해 이루어지고 있습니다.

또한 보고서에 따르면 2022년부터 2041년까지 북미 화물 운송량은 3분의 1 증가할 것으로 추정됩니다. 이 지역의 상용 서비스에 대한 시장 수요는 다른 지역에 비해 가장 높으며 총액은 1조 450억 달러에 달할 전망입니다.

세계적으로 캐나다는 민간 비행 시뮬레이션에서 1위, 민간 엔진 생산에서 3위, 민간 항공기 생산에서 4위를 차지하고 있습니다. 모든 주요 카테고리 중에서 전국적으로 유일하게 상위 5위를 차지하고 있습니다. 캐나다 항공우주 산업은 제품의 70% 이상을 6대륙의 190개 이상의 국가로 수출하고 있습니다.

멕시코에서 보라리스는 저렴한 항공사 중 하나이며 유행 전 상황과 비교하여 2021년 7월 국내 여행 여객 유입이 23%, 국제선에서 10% 증가했습니다. 보라리스항공은 에어버스기 3기와 몇몇을 발주해 98기로 연말을 맞이한다고 보도되고 있습니다.

이러한 모든 요인들로 인해 항공우주 양식 수요는 예측 기간 동안 이 지역에서 증가할 것으로 예상됩니다.

항공우주용 양식 산업 개요

항공우주 폼 시장은 최상위 기업들 사이에서 부분적으로 통합됩니다. 주요 기업은 Greiner Aerospace, BASF SE, Evonik Industries AG, Rogers Corporation 및 Solvay를 포함합니다(순차적).

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

가볍고 연비가 좋은 항공기에 대한 수요 증가

항공우주산업의 꾸준한 성장

기타 촉진요인

억제요인

PU 폼의 사용에 관한 엄격한 규제

기타 구속구

업계의 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체 제품 및 서비스의 위협

경쟁도

제5장 시장 세분화(금액 기준 시장 규모)

유형

폴리우레탄

폴리이미드

금속 발포체

멜라민

폴리에틸렌

기타 유형

용도

민간항공

군용 항공

비즈니스 및 일반 항공

지역

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

합병과 인수, 합작사업, 협업 및 계약

시장 랭킹 분석

유력 기업이 채용한 전략

기업 프로파일

3A Composites

Aerofoam Industries, LLC

ARMACELL

BASF SE

Boyd

Diab Group

DuPont

ERG Aerospace Corporation

Evonik Industries AG

General Plastics Manufacturing Company

Grand Rapids Foam Technologies

Greiner Aerospace

Rogers Corporation

Technifab, Inc.

UFP Technologies, Inc.

Zotefoams plc

Recticel NV/SA

제7장 시장 기회와 미래 동향

바이오의 PU 폼 제조에의 동향이 높아진다

기타 기회

BJH

영문 목차

영문목차

The Aerospace Foams Market size is estimated at USD 5.69 billion in 2024, and is expected to reach USD 7.85 billion by 2029, growing at a CAGR of 6.64% during the forecast period (2024-2029).

Key Highlights

The market was negatively impacted by COVID-19 in the year 2020. As passenger demand was low because of the pandemic, the corresponding travel restrictions and the economic recession forced airlines to find ways to cut costs. Cost-cutting measures such as the cancellation or postponement of aircraft orders were carried out. However, traveling increased as soon as the restrictions were picked up in the years 2021 and 2022, and this has increased the demand for air freights.

Over the short term, the major factor driving the market studied is the increasing demand for lightweight and fuel-efficient aircraft. The production of polyurethane (PU) foam is still highly petroleum-dependent, and this acts as a restraint for the market.

Increasing trends toward bio-based polyurethane foam manufacturing may act as an opportunity for the market during the forecast period. North America is expected to dominate the market over the forecast period.

Aerospace Foams Market Trends

Increasing Demand from Commercial Aviation

The decreasing fuel price fluctuations and the increasing operational efficiencies have supported the growth of commercial aircraft operations in the past few years. The increasing air travel rates, majorly in emerging economies in Asia-Pacific and South America, along with increasing disposable incomes around the world, have been driving the growth in the aircraft fleet globally.

The increasing volumes of passengers and the increasing retirements are expected to drive the need for 44,040 new jets, valued at USD 6.8 trillion, over the next two decades. The global commercial fleet is expected to reach 50,660 airplanes by 2038, with all the new airplanes and jets would remaining in service considered.

Additionally, according to the Boeing Commercial Market Outlook 2022-2041, by 2031, airplanes will grow their commercial fleet with an annual rate of 2.6% and reach 35,400 airplanes in service, and by 2041 this number will reach 47,080, representing an annual rate of 2.8% over the 2019-2041 period.

Further, new airplane deliveries for commercial fleet from 2022-2041 in Latin America will be 5%, Middle East 7%, North America 23%, Asia 21%, and Europe 21% out of the total deliveries.

All the aforementioned factors are expected to enhance the demand for aerospace foams during the manufacture of these aircraft in the coming years, thereby boosting the market studied.

North America to Dominate the Market

North America is the largest market for the aerospace industry across the world. Aerospace manufacturers in North America are expected to expand their operations on account of the rising number of air passengers and increasing military expenditure in the region in recent times.

The United States is the largest aviation market in North America and has one of the largest fleet sizes in the world; hence, it is one of the largest markets for aerospace foams. According to the Federal Aviation Administration (FAA), the total commercial aircraft fleet is expected to reach 8,270 in 2037, owing to the growth in air cargo. Also, the US mainliner carrier fleet is expected to grow at a rate of 54 aircraft per year due to the existing fleet getting older.

In the 2022 defense budget, the United States government allowed USD 768.2 billion for national defense programs, which is about a 2% increase from the Biden administration's original budget request, registering a growing usage of aerospace materials in the sector.

According to the Boeing Commercial Outlook 2022-2041, in North America, 13% of travel by air is done for business purposes, 50% for leisure, and 37% for visiting friends and relatives.

Further, according to the report, the North American freight fleet is estimated to grow by one-third from 2022-2041. The market demand for commercial services in the region is highest as compared to other regions, with a total value of USD 1,045 billion.

Globally, Canada ranks first in civil flight simulation, third in civil engine production, and fourth in civil aircraft production. It is the only nationally ranked in the top five of all the key categories. The Canadian aerospace industry exports over 70% of its products to over 190 countries across six continents.

In Mexico, Volaris is one of the low-cost airlines, which witnessed a 23% growth in passenger influx of domestic travel and 10% in international flights during July 2021 compared to the pre-pandemic situation. Volaris airlines were reported to order three Airbus aircraft and some more to close the year with 98 aircraft.

Owing to all these factors, the demand for aerospace foams is projected to grow in the region during the forecast period.

Aerospace Foams Industry Overview

The aerospace foams market is partially consolidated among the top-level players. The major companies include (not in any particular order) Greiner Aerospace, BASF SE, Evonik Industries AG, Rogers Corporation, and Solvay.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Demand for Lightweight and Fuel-efficient Aircraft

4.1.2 Steady Growth in the Aerospace Industry

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Stringent Regulations Regarding the Use of PU Foams

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

5.1 Type

5.1.1 Polyurethane

5.1.2 Polyimide

5.1.3 Metal Foams

5.1.4 Melamine

5.1.5 Polyethylene

5.1.6 Other Types

5.2 Application

5.2.1 Commercial Aviation

5.2.2 Military Aviation

5.2.3 Business and General Aviation

5.3 Geography

5.3.1 Asia Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 France

5.3.3.4 Italy

5.3.3.5 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle-East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 3A Composites

6.4.2 Aerofoam Industries, LLC

6.4.3 ARMACELL

6.4.4 BASF SE

6.4.5 Boyd

6.4.6 Diab Group

6.4.7 DuPont

6.4.8 ERG Aerospace Corporation

6.4.9 Evonik Industries AG

6.4.10 General Plastics Manufacturing Company

6.4.11 Grand Rapids Foam Technologies

6.4.12 Greiner Aerospace

6.4.13 Rogers Corporation

6.4.14 Technifab, Inc.

6.4.15 UFP Technologies, Inc.

6.4.16 Zotefoams plc

6.4.17 Recticel NV/SA

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Increasing Trends toward Bio-based PU Foam Manufacturing