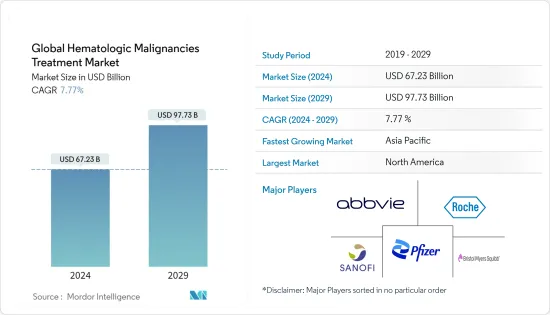

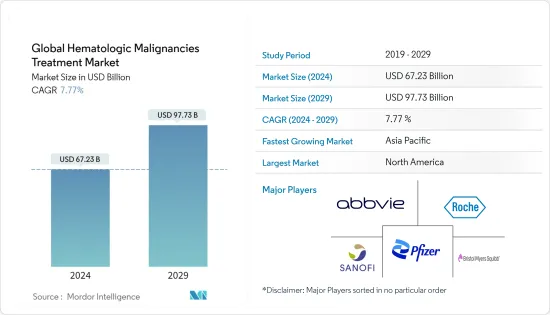

혈액 악성 종양 치료 세계 시장 규모는 2024년에 672억 3,000만 달러로 추계되고, 2029년에는 977억 3,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2024-2029년)의 CAGR은 7.77%로 성장할 것으로 예상됩니다.

COVID-19 팬데믹성 발병으로 인해 대부분의 선택적 치료가 연기되었기 때문에 혈액 악성 종양 치료 시장도 큰 영향을 받았습니다. 그러나 급성 백혈병을 비롯한 심각한 질환에서는 치료 연기가 권장되지 않기 때문에 유행 기간 동안에도 만전의 방어 체제로 혈액 악성 종양의 치료를 실시할 수 있도록, 최근에는 필요한 가이드라인이나 대책이 내세워지고 있다 합니다. Acta Haematologica, 2020에 게재된 조사 논문에 따르면, 보다 집중적이지 않은 치료법을 채택하고 환자와 직원 간의 접촉을 최소화하고, 임상 방문 횟수를 줄이고, 경과 관찰을 위한 원격 의료 장려하면 혈액 악성 종양 환자의 치료의 효과적인 결과를 도울 수 있습니다. United Kingdom Coronavirus Cancer Monitoring Project(UKCCMP)가 2020년에 실시한 조사에 따르면 COVID-19 감염의 중증화 위험은 혈액암 환자에서 약 57%로 높은 것으로 밝혀졌습니다. 따라서 앞서 언급한 요인을 고려하면 COVID-19 팬데믹은 조사 시장의 성장에 영향을 미칠 것으로 예상됩니다.

혈액 악성 종양 치료 시장의 성장에 기여하는 주요 요인은 혈액 암의 신흥국 시장에서의 이환율의 상승과 혈액 악성 종양 치료 시장을 견인하는 새로운 치료법의 개척에 중점을 두도록 하는 것입니다. Globocan 2020에 따르면 백혈병의 추정 이환율은 아시아가 가장 높았으며, 2020년에는 230,650명이 진단되었으며, 이어 유럽의 100,020명, 북미 67,784명이 되었습니다. 이와 같이 세계적으로 백혈병의 이환율이 높은 것이 시장 성장의 원동력이 될 것으로 예상됩니다.

합병, 인수, 제품상시, 제휴, 공동연구 등 주요 기업의 노력이 시장 성장을 뒷받침할 것으로 예상됩니다. 예를 들어, 2021년 5월 도쿄에 본사를 두는 Chugai Pharmaceutical Co. Ltd은 재발 또는 난치성(R/R)의 확산성 대세포형 B세포 림프종(DLBCL)의 치료에 사용할 수 있는 항암제/항미소관 결합 항CD79b 단클론항체 「폴리비 점적 정주 30mg 및 140mg」의 발매를 발표했습니다.

2021년 2월, 미국 식품의약국은 적어도 2종의 다른 전신 치료에 반응하지 않는 특정 유형의 대세포형 B 세포 림프종의 성인 환자를 치료하기 위한 세포-기반 유전자 치료제입니다. Breyanzi(lisocabtagene maraleucel)를 승인했습니다. 이러한 제품 상시 증가는 연구 대상 시장에 성장 기회를 가져올 가능성이 높습니다. 그러나 치료에 드는 약비가 높은 것이 시장의 주요 억제요인이 되고 있습니다.

화학 요법은 치료의 첫 번째 선택 약물이기 때문에이 시장에서 화학 요법이 가장 큰 부문입니다. 일반적으로, 대부분의 유형의 혈액암에서는 화학요법이 일반적인 치료법이며, 암의 유형에 따라 특정 약물 또는 약물 조합이 사용됩니다. 대규모 환자 풀과 혈액암의 이환율 증가가 조사한 부문의 성장의 주요 촉진요인입니다. 또한 조기 단계에서 질병의 가능성과 후속 치료에 대한 이해가 증가함에 따라이 부문의 성장을 가속할 것으로 예상됩니다.

미국 암 학회에 따르면, 시타라빈(시토신 아라비노사이드 또는 아라 C) 및 다우노루비신(다우노마이신) 또는 이달비신과 같은 안트라사이클린계 약물은 급성 골수성 백혈병의 치료에 사용되는 가장 흔한 화학요법 약물 입니다. 클라드리빈(2-CdA), 플루다라빈, 미톡산트론, 에토포사이드(VP-16), 6-티오구아닌(6-TG), 히드록시우레아, 프레드니손 및 덱사메타손과 같은 부신피질 스테로이드제, 메토트렉세이트(MTX), 6- 퓨린(6-MP), 아자시티딘, 데시타빈 등이 급성 골수성 백혈병의 화학요법에 사용됩니다. 또한 제품 인가 증가는 조사 대상 시장의 성장을 조장할 것으로 예상됩니다. 예를 들어, 2020년 9월, 미국 FDA는 급성 골수성 백혈병 성인 환자의 치료를 계속하기 위해 Bristol Myers Squibb사의 아자시티딘(Onuleg) 300mg 정제, CC-486을 승인했습니다. 유사하게, 2019년 6월, 미국 식품의약국은 적어도 2회의 전치료 후에 진행 또는 재발한 확산성 대세포형 B세포 림프종(DLBCL)의 성인 환자를 치료하기 위해 화학요법제 벤담스틴 및 리툭시맙과의 병용으로 폴리비의 사용을 승인했습니다. 이와 같이 앞서 언급한 요인들로부터 연구 부문은 예측 기간 동안 큰 성장을 이룰 것으로 예상됩니다.

북미는 예측 기간을 통해 혈액 악성 종양 치료 시장 전체를 지배할 것으로 예상됩니다. 주요 기업의 존재, 혈액암 환자의 높은 유병률, 확립된 헬스케어 인프라, 브랜드 의약품의 이용가능성 등이 북미에서의 조사 시장 점유율의 큰 요인이 되고 있습니다.

Global Cancer Observatory에 따르면 2020년에는 북미에서 67,784명에 가까운 백혈병과 35,318명의 다발성 골수종이 보고되었습니다. 백혈병 림프종 협회에 따르면 2021년에는 미국에서 백혈병을 앓고 있거나 관해 상태에 있는 사람은 함께 397,501명으로 추정됩니다. 또한 2021년에는 미국에서 약 61,090명이 백혈병으로 진단될 전망이라고 합니다. 이처럼 이 지역에서 혈액암 환자수 증가는 시장 성장의 주요 촉진요인입니다.

정부의 유익한 노력과 연구 제휴 증가는 시장 성장 촉진요인으로 기대됩니다. 예를 들어, 2020년 12월 백혈병 림프종 협회(LLS)는 백혈병, 림프종, 골수종 및 기타 혈액암 환자에 대한 효과적인 치료 옵션을 찾기 위한 연구를 진전시키기 위해 주요 암 기관 과 재단과 제휴를 맺고, 약 1,700만 달러의 연구 조성금을 공동 출자하는 공동 연구를 개시했습니다. 2020년 12월 재즈 퍼머슈티컬즈는 급성 림프모구성 백혈병(ALL) 또는 림프모구성 림프종(LBL) 환자의 치료에서 다제 병용 화학요법 요법의 일부로 사용하기 위한 JZP- 458의 생물 제제 승인 신청(BLA)을 제출했습니다.

많은 기업들이 시장 점유율을 확대하기 위해 제품 상시, 제휴, 공동 연구, 합병, 인수 등 다양한 전략적 노력을 실시했습니다. 예를 들어, 2020년 10월, AstraZeneca Pharma India는 Calquence 브랜드 이름으로 다양한 유형의 백혈병(백혈병(CLL) 및 작은 림프구성 림프종)을 치료하는 데 사용되는 아카라브루티닙 100mg 캡슐의 출시를 발표했습니다. 2019년 5월 미국 식품의약국은 만성 림프성 백혈병 또는 작은 림프구성 림프종을 가진 성인 환자를 대상으로 베네토크락스의 공동 개발을 수행하는 아비 잉크와 제넨텍 잉크를 승인했습니다. 이상의 신흥국 시장의 개척에 의해 이 시장은 견조한 성장이 전망됩니다.

혈액 악성 종양 치료 시장은 적당히 통합되어 있으며 여러 대형 기업으로 구성되어 있습니다. 현재 시장을 독점하고 있는 기업으로는 Pfizer Inc., F. Hoffmann-LA Roche Ltd, Sanofi SA, Bristol-Myers Squibb Company, AbbVie Inc., Novartis AG, GlaxoSmithKline PLC, Amgen Inc., Johnson & Johnson, Takeda Pharmaceutical Co. Ltd. 등이 있습니다. M&A나 신제품 개발 등의 전략을 실시했습니다. 예를 들어, GlaxoSmithKline PLC는 2020년 8월 재발 또는 난치성 다발성 골수종 환자에 대한 첫 번째 클래스의 항-BCMA(B 세포 성숙 항원) 요법인 BLENREP(belantamab mafodotin-blmf)의 미국 FDA 승인을 받았습니다.

The Global Hematologic Malignancies Treatment Market size is estimated at USD 67.23 billion in 2024, and is expected to reach USD 97.73 billion by 2029, growing at a CAGR of 7.77% during the forecast period (2024-2029).

As most elective treatments were deferred due to the outbreak of the COVID-19 pandemic, the hematologic malignancies treatment market was also impacted significantly. However, delayed treatment is not recommended for severe diseases, especially acute leukemia, and thus, necessary guidelines and measures have been put forth recently to allow hematologic malignancies' treatments during the pandemic with all protective measures. According to the research article published in Acta Haematologica, 2020, employing less intensive therapy options, minimizing the exposure between patient and staff, reducing the number of clinical visits, and encouraging telemedicine for follow-up consultations can aid in the effective outcome of treatment of patients with hematologic malignancies. As per the research study carried out by the United Kingdom Coronavirus Cancer Monitoring Project (UKCCMP), 2020, the risk of experiencing severe cases of COVID-19 infection was found to be higher, at about 57%, among patients with blood cancers. Thus, given the aforementioned factors, the COVID-19 pandemic is expected to impact the growth of the studied market.

The major factors attributing to the growth of the hematologic malignancies treatment market are the growing incidence of blood cancer and an increasing emphasis on the development of new treatments, driving the hematologic malignancies treatment market. According to Globocan 2020, the estimated incidence of leukemia was the highest in Asia, with 230,650 cases diagnosed in 2020, followed by 100,020 cases in Europe and 67,784 cases in North America. Thus, the high incidence of leukemia worldwide is expected to drive market growth.

Initiatives by major players such as mergers, acquisitions, product launches, partnerships, and collaborations are expected to boost the market growth. For instance, in May 2021, Tokyo-based Chugai Pharmaceutical Co. Ltd announced the launch of an anticancer agent/antimicrotubule binding anti-CD79b monoclonal antibody called Polivy intravenous infusion 30 mg and 140 mg that can be used for the treatment of relapsed or refractory (R/R) diffuse large B-cell lymphoma (DLBCL).

In February 2021, the United States Food and Drug Administration approved Breyanzi (lisocabtagene maraleucel), a cell-based gene therapy to treat adult patients with certain types of large B-cell lymphoma who have not responded to at least two other types of systemic treatment. Such rising product launches will likely provide growth opportunities to the market studied. However, the high cost of the medication involved in the treatment is the major restraint to the market.

As chemotherapy is the first line of treatment, it is the largest segment in the studied market. Generally, for most types of blood cancers, chemotherapy is the common treatment, and a particular drug or combination of drugs is used depending on the type of cancer. The large patient pool and the increasing incidence of blood cancers are the major drivers for the growth of the studied segment. Also, the growing understanding of the possibility of the disease at the early stage and its subsequent treatment are expected to drive the segment growth.

According to the American Cancer Society, Cytarabine (cytosine arabinoside or ara-C) and anthracycline drugs, such as daunorubicin (daunomycin) or idarubicin, are the most common chemo drugs used in the treatment of acute myeloid leukemia. Cladribine (2-CdA), Fludarabine, Mitoxantrone, Etoposide (VP-16), 6-thioguanine (6-TG), Hydroxyurea, Corticosteroid drugs, such as prednisone or dexamethasone, Methotrexate (MTX), 6-mercaptopurine (6-MP), Azacitidine, and Decitabine are used in chemotherapy of acute myeloid leukemia. Also, the rising product approvals are expected to aid in the growth of the studied market. For instance, in September 2020, the US FDA approved Bristol Myers Squibb's azacytidine (Onureg) 300 mg tablets, CC-486, to continue treating adult patients with acute myeloid leukemia. Similarly, in June 2019, the United States Food and Drug Administration granted approval to Polivy to be used in combination with the chemotherapy drug bendamustine and a rituximab, to treat adult patients with diffuse large B-cell lymphoma (DLBCL) that has progressed or returned after at least two prior therapies. Thus, owing to the aforementioned factors, the studied segment is expected to witness significant growth over the forecast period.

North America is expected to dominate the overall hematologic malignancies treatment market throughout the forecast period. The presence of key players, high prevalence of blood cancer patients, established healthcare infrastructure, and availability of branded drugs are some of the key factors accountable for the large share of the studied market in North America.

According to the Global Cancer Observatory, in 2020, nearly 67,784 cases of leukemia and an estimated 35,318 cases of multiple myeloma were reported in the North American region. According to the Leukemia and Lymphoma Society, in 2021, an estimated combined total of 397,501 people in the United States were living with or in remission from leukemia in the United States. It also stated that around 61,090 people were expected to be diagnosed with leukemia in the United States in 2021. Thus, the increasing number of blood cancer cases in the region is a major driving factor for the growth of the market.

Beneficial government initiatives and an increase in the number of research partnerships are some of the drivers expected to drive market growth. For instance, in December 2020, the Leukemia and Lymphoma Society (LLS) initiated a collaboration to form alliances with leading cancer institutions and foundations to co-fund nearly USD 17 million in research grants to progress the research in finding effective treatment options for patients with leukemia, lymphoma, myeloma, and other blood cancers. In December 2020, Jazz Pharmaceuticals submitted the Biologics License Application (BLA) for its JZP-458 for use as a component of a multiagent chemotherapy regimen in the treatment of patients with acute lymphoblastic leukemia (ALL) or lymphoblastic lymphoma (LBL).

Many companies are undertaking a variety of strategic initiatives like product launches, partnerships, collaborations, mergers, and acquisitions to boost their market share. For instance, in October 2020, AstraZeneca Pharma India announced the launch of Acalabrutinib 100 mg capsules, which are used for the treatment of various types of leukemias (leukemia (CLL) and small lymphocytic lymphoma) under the brand name Calquence. In May 2019, the United States Food and Drug Administration approved AbbVie Inc. and Genentech Inc., jointly developing venetoclax for adult patients with chronic lymphocytic leukemia or small lymphocytic lymphoma. Thus, due to the above-mentioned developments, the market is expected to see robust growth.

The hematologic malignancies treatment market is moderately consolidated and consists of several major players. Some of the companies currently dominating the market include Pfizer Inc., F. Hoffmann-LA Roche Ltd, Sanofi SA, Bristol-Myers Squibb Company, AbbVie Inc., Novartis AG, GlaxoSmithKline PLC, Amgen Inc., Johnson & Johnson, and Takeda Pharmaceutical Co. Ltd. Most of the major players are focusing on expanding their businesses in the developing regions to boost their market shares. They are implementing strategies like mergers and acquisitions and new product developments. For instance, in August 2020, GlaxoSmithKline PLC received US FDA approval for its BLENREP (belantamab mafodotin-blmf), a first-in-class anti-BCMA (B-cell maturation antigen) therapy for the treatment of patients with relapsed or refractory multiple myeloma.