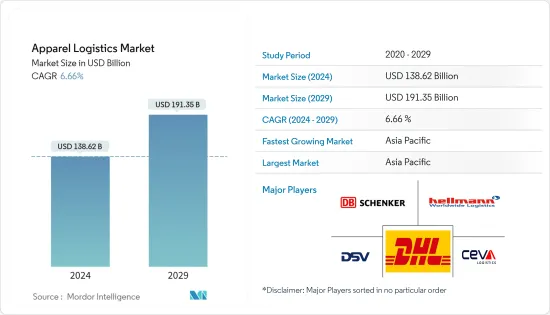

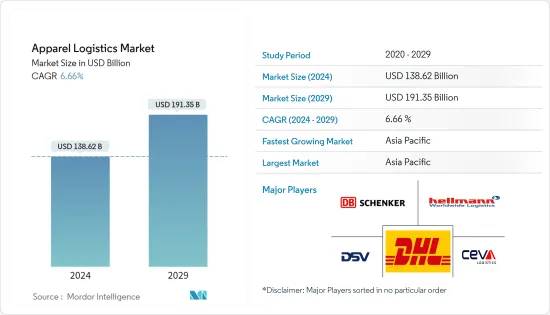

의류 물류(Apparel Logistics) 시장 규모는 2024년에 1,386억 2,000만 달러로 추정되며, 2029년까지 1,913억 5,000만 달러에 이를 것으로 예측되며, 예측 기간(2024년부터 2029년) 동안 6.66%의 CAGR로 추이하며 성장할 전망입니다.

의류 산업의 신속한 보충 사이클이 시장 성장을 가속하는 주요 요인입니다. 소매업체부터 제조업체에 이르기까지 의류 공급망은 최신 동향과 최고의 고객 경험을 제공하기 위해 격하게 경쟁하고 있습니다. 한편, 소비자의 기대와 이행 모델의 변화가 의류 기업에 압력을 가하고 있습니다.

COVID-19 팬데믹은 지역 전역에서 록다운, 노선 제한, 교통기능 장애를 일으켰습니다. 급증하는 사건으로 의류 물류 시장 전체가 다방면에서 영향을 받고 있습니다. 록다운과 감염 확대로 개인이 실내에 머물러야 하기 때문에 노동력의 입수가 용이성이 의류물류시장의 재고 네트워크를 혼란시키고 있습니다.

많은 주요 패션 소매업체는 단일 시설 내에서 단일 정보 시스템을 사용하여 다중 채널 유통을 수행하는 개념을 채택하여 노동 생산성과 재고 최적화의 극적인 향상을 실현 하고 있습니다. 의류 마켓플레이스는 정기적으로 진화하고 재발명되었습니다. 새로운 판매 채널이 개발되고 있으며 기업은 물류 및 운송 네트워크를 지속적으로 평가하고 재구축해야 합니다.

세계의 의류 산업은 끊임없이 변화하는 패션 동향에 의해 매우 역동적입니다. 경쟁이 치열하기 때문에 의류 회사는 데이터 분석 및 AI와 같은 새로운 기술을 도입하고 있습니다. 의류업계는 대규모 아웃소싱 업무를 하고 있으며, 물류 관계자에게 국내외 업무로 큰 기회를 제공하고 있으며, 경쟁이 치열한 산업이 되고 있습니다. 공급망의 단절은 의류 기업에 상당한 손실을 초래합니다. 따라서 공급망에 미치는 영향을 최소화하기 위해 의류 회사는 일반적으로 물류업체에게 업무를 아웃소싱하는 것을 선호합니다.

2021년 6월, Fast Fashion 전자상거래 사이트 shein.com은 전 세계 패션 및 의류 카테고리에서 가장 많은 액세스를 획득했으며 데스크톱 트래픽의 3.29%를 차지했습니다. 스웨덴 의류 소매업체 HM의 전자상거래 포털이 1.75%의 방문수로 2위를 차지했습니다. 2020년과 2021년에 의류의 온라인 소매 사이트는 디지털 시장에서의 존재감으로 인해 매출이 증가했습니다. 이러한 영향으로 시장 관계자 접근 방식의 변화가 추진되고 있으며, 이는 향후 몇 년간 지속될 것으로 예상되며, 전자상거래, 모바일 쇼핑 성장, 고객 개인화에 대한 점점 높아지는 기대에 대한 대응이 더욱 중시됩니다.

웹사이트 트래픽의 연간 성장률에 따라 shein.com은 2020년 4분기에 미국 주요 패스트패션 소매점 웹사이트로 부상했습니다. 소비자는 가격과 제품을 비교하기 위해 웹 사이트에 자주 방문하지만, 세계의 온라인 플랫폼은 서비스를 확장할 계획입니다. 패션 브랜드와의 파트너십을 강화하고 디지털 쇼핑 분야에서 경쟁력을 유지하기 위한 추가적인 참여 방법을 개발합니다. 증가하는 온라인 주문을 수용하기 위해 제3자 물류 회사는 수백만 평방 피트의 공간을 흡수하여 소비재, 전자상거래, 제조 및 의류 기업에 개방하고 있습니다.

의류 시장에서 얻은 수익은 조사 기간 동안 꾸준히 증가했습니다. 2020년 시장 수익은 약 1조 4,600억 달러였습니다. 소비자 기술 브랜드는 오랫동안 호주, 일본, 한국의 온라인 쇼핑객을 타겟으로 해 왔습니다. 그러나 의류 및 미용 분야 브랜드도 다른 지역을 타겟팅합니다. 따라서 브랜드는 계속 현지화에 주력하고 있으며 이러한 제품의 주요 구매자인 밀레니얼 세대 고객에게 대응할 수 있습니다.

2020년 의류와 신발의 전년 대비 성장률은 크게 감소했습니다. COVID-19 팬데믹을 배경으로 성장률은 총 10% 이상 감소했습니다. 2020년에는 스포츠 용품과 양판점/클럽 소매업이 성장했습니다. 나이키와 아디다스와 같은 세계 스포츠 의류 및 신발 브랜드는 다른 지역을 버리고 베트남과 같은 동남 아시아 신흥 국가에서 생산을 늘리고 있으며 운송 회사 및 기타 제3자 물류에 긍정적인 전망을 제공합니다.

의류 물류 시장은 세계 대기업과 중소규모 현지 기업의 존재로 세분화됩니다. 일부 주요 기업은 시장 점유율의 대부분을 차지합니다. 세계 물류 기업의 대부분은 시장의 요구와 수요를 충족하기 위해 소매 및 의류 물류 부문을 가지고 있습니다. 또한 현지 기업은 차량 규모, 제공하는 서비스, 취급 제품 및 기술 측면에서 자사의 능력을 더욱 강화하고 있습니다. 전자상거래 매출의 급증은 속도와 배송 등의 측면에서 물류기업에 기회와 과제를 가져오고 있습니다. 엄청난 자본과 자산을 보유한 세계 기업들은 첨단 저장 공간과 선불 센터에 투자하여 이 시나리오의 혜택을 누릴 수 있습니다. 한편, 지역 및 현지 기업은 제작 회사와 소매업체의 요구를 지원하기 위해 더 나은 솔루션을 고안하고 있습니다.

The Apparel Logistics Market size is estimated at USD 138.62 billion in 2024, and is expected to reach USD 191.35 billion by 2029, growing at a CAGR of 6.66% during the forecast period (2024-2029).

Rapid replenishment cycles of the apparel industry are the main factor driving the market's growth. From retailers to manufacturers, apparel supply chains compete strongly to provide the latest trends and the best customer experience. Meanwhile, changing consumer expectations and fulfillment models pressure apparel businesses.

The COVID-19 pandemic caused lockdowns, line limitations, and breakdown of transportation organizations across regions. With the rapidly increasing cases, the overall apparel logistics market is being influenced from multiple points of view. The accessibility of the labor force is disturbing the inventory network of the apparel logistics market, as the lockdowns and the spread of the infection are forcing individuals to remain indoors.

Many leading fashion retailers have embraced the concept of performing multi-channel distribution within a single facility with a single information system, achieving dramatic improvements in labor productivity and inventory optimization. The apparel marketplace is evolving and reinventing itself regularly. New sales channels are being developed, requiring companies to continuously evaluate and remodel their logistics and transportation networks.

The global apparel industry is extremely dynamic due to the ever-changing fashion trends. Due to the intense competition, apparel companies are implementing new technologies, such as data analytics and AI. The apparel industry has massive outsourcing operations that provide logistics players with considerable opportunities in domestic and international operations, making it a highly competitive industry. Any disruption in the supply chain leads to a huge loss for apparel companies. Thus, to have a minimal impact on their supply chain, apparel companies usually prefer outsourcing their operations to logistics players.

In June 2021, the fast-fashion e-commerce site, shein.com, was the most visited in the fashion and apparel category worldwide, accounting for 3.29% of desktop traffic. The e-commerce portal of the Swedish clothing retailer HM ranked second, with 1.75% visits. In 2020 and 2021, online apparel retail sites experienced a sales increase due to their digital market presence. This effect has fuelled changes in the approach of the market players, which may be expected to continue in the coming years, with more emphasis on the growth of e-commerce, mobile shopping, and meeting ever-rising expectations of personalization among customers.

Based on the yearly percentage growth in terms of website traffic, shein.com emerged as the leading fast-fashion retailer website in the United States in Q4 2020. While consumers frequently visit websites to compare prices and products, global online platforms plan to expand their fashion brand partnerships and develop additional engagement methods to stay competitive in the digital shopping space. To handle the growing online orders, third-party logistics companies are absorbing millions of sq. ft of space and letting it out to consumer goods, e-commerce, manufacturing, and apparel companies.

Revenue generated by the apparel market steadily increased through the study period. In 2020, the market revenue was approximately USD 1.46 trillion. Consumer technology brands have long targeted online shoppers in Australia, Japan, and South Korea. However, brands in the apparel and beauty sectors are also targeting other regions. Hence, brands may continue focusing on localization and catering to millennial customers who are the key buyers of these products.

The Y-o-Y growth rate for apparel and footwear experienced severe losses in 2020. Against the backdrop of the COVID-19 pandemic, growth declined by a total of over 10%. Sporting goods and mass/club retail grew in 2020. Global sports apparel and footwear brands like Nike and Adidas are ditching other regions and increasing their production in emerging Southeast Asian countries like Vietnam, offering a positive outlook for transportation companies and other third-party logistics service providers.

The apparel logistics market is fragmented with the presence of large global players and small- and medium-sized local players. Some of the key players occupy most of the market share. Most global logistics players have a retail and apparel logistics division to meet the market needs and demand. Additionally, local players are increasingly enhancing their capabilities in terms of fleet size, service offerings, products handled, and technology. The surging e-commerce sales are creating opportunities and challenges for logistics companies in terms of speed, delivery, etc. Global companies with high capital and assets can invest in advanced storage spaces and fulfillment centers and benefit from this scenario. On the other hand, regional and local players are coming up with better sector solutions to support the needs of the production companies and retailers.