프로세스 오일 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)

Process Oils - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

상품코드:1438253

리서치사:Mordor Intelligence

발행일:2024년 02월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

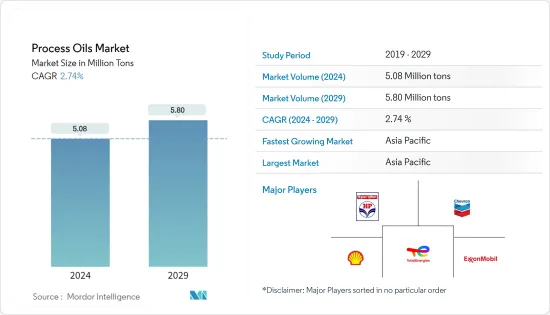

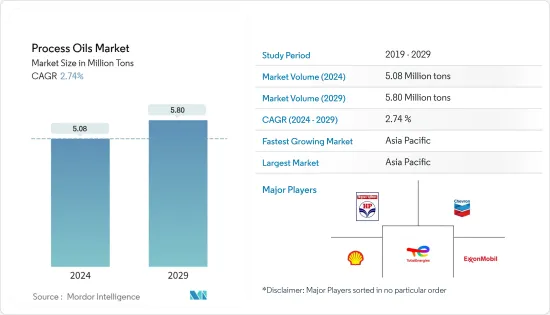

프로세스 오일(Process Oils) 시장 규모는 2024년 508만 톤으로 추정되며, 2029년까지 580만 톤에 이를 것으로 예측되며, 예측 기간(2024-2029년) 동안 2.74%의 CAGR로 추이하며 성장 할 것으로 전망됩니다.

COVID-19 팬데믹은 2020년시장에 악영향을 미쳤습니다. 그러나 시장은 전염병 이전 수준에 도달했으며 앞으로 몇 년동안 꾸준히 성장할 것으로 예상됩니다.

주요 하이라이트

단기적으로 시장 성장을 가속하는 주요 요인은 고분자 생산 수요 증가입니다. 고무유 사용량이 급증함에 따라 향후 수년간 프로세스 오일 수요도 증가할 수 있습니다.

그러나 엄격한 규제로 인한 PAH 및 DAE 사용의 감소는 조사 기간 동안 시장 성장을 방해할 수 있습니다.

그럼에도 불구하고, 바이오 고무 프로세스 오일의 조사와 전기자동차용 프로세스 오일 수요 가속은 곧 세계 시장 성장 기회의 요인이 될 수 있습니다.

아시아 태평양은 시장을 독점할 것으로 예상되며 예측 기간 동안 가장 높은 CAGR을 나타낼 수 있습니다.

프로세스 오일 시장 동향

시장을 독점하는 고무 용도

고무 프로세스 오일은 휘발성이 높은 가솔린을 사용하여 제조되며 등유 분획은 증류 공정을 사용하여 분리됩니다.

천연 프로세스 오일과 합성 프로세스 오일은 모두 고무 고무, 장난감, 타이어와 같은 여러 고무 제품의 제조에 상업적으로 사용됩니다.

이들은 충전제의 분산을 증가시키고 혼합물의 유동 특성을 증가시키기 때문에 고무 화합물의 혼합 공정에도 사용됩니다.

세계의 고무 산업의 확대는 다양한 용도 산업에 걸쳐 고무 프로세스 오일 사용을 촉진하고 있습니다. 일반적인 고무 용도로는 타이어, 건축자재, 백색 가전, 생물 의학, 섬유 등이 있습니다.

중국은 세계 최대의 타이어 생산국입니다. 중국국가통계국에 따르면 2021년 중국의 타이어 생산량은 9억246만개로 2020년에 비해 약 9,500만개 증가했습니다.

말레이시아 고무 평의회에 따르면 2022년 상반기 세계 고무 생산량은 약 1,390만 톤으로 약 1,410만 톤이 생산된 전년 동기와 비교해 1.5% 감소했습니다.

상기 요인에 근거하여, 프로세스 오일로서 고무유 용도가 시장을 독점할 것으로 예상됩니다.

아시아 태평양이 시장을 독점

아시아 태평양은 인도나 중국 등의 국가에서 섬유 제품이나 퍼스널케어 제품에 대한 광범위한 수요가 있기 때문에 헤아릴 수 없는 가능성을 지닌 지역입니다.

중국은 1994년부터 세계 최대의 섬유 및 의류 수출국으로, 주로 OEM 제조 및 가공에 종사함으로써 세계의 저가에서 중가 시장을 독점하고 있습니다. 동시에 유럽 연합은 세계의 첨단 시장과 고품질 섬유 제품을 계속 지배하고 있습니다.

OICA에 따르면 2021년 중국의 자동차 생산 대수는 2,608만대로 2020년 2,522만대에서 3% 증가했습니다. 예측 기간 동안 프로세스 오일 시장에 긍정적인 영향을 미칠 것으로 예상됩니다.

현재 인도의 퍼스널케어 제품의 보급률은 선진국 및 기타 신흥 경제 국가에 비해 상대적으로 낮습니다.

그러나 경제환경의 개선과 인도 국민의 구매력 향상으로 국내에서 퍼스널케어 제품의 채택이 증가할 것으로 예상됩니다.

NIPFA 인도에 따르면 인도의 미용 및 개인 관리 산업 규모는 현재 268억 달러로 향후 3년간 372억 달러까지 성장할 것으로 예상됩니다. 인도 시장 성장은 조사 기간 동안 프로세스 오일 시장의 발전을 촉진할 것으로 예상됩니다.

OICA에 따르면 인도 자동차 산업은 2021년에 30%의 성장을 기록해 약 439만대를 생산했습니다. 자동차 부문의 급속한 성장은 조사 대상 시장에 긍정적인 영향을 미칠 것입니다.

위의 요인으로 인해 아시아 태평양의 프로세스 오일 시장은 예측 기간 동안 세계 시장을 독점할 것으로 예상됩니다.

프로세스 오일 산업 개요

프로세스 오일 시장은 본질적으로 부분적으로 통합됩니다. 시장의 주요 기업으로는 Chevron Corporation, ExxonMobil Corporation, HP Lubricants, Royal Canadian Shell Plc, Total 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진 요인

폴리머 생산량 증가

억제 요인

쇠퇴하는 자동차 부문

엄격한 규제에 의해 PAH 및 DAE 사용 감소

산업 가치사슬 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체 제품 및 서비스의 위협

경쟁도

제5장 시장 세분화

유형별

아로마틱

파라핀

나프텐

용도

고무

폴리머

퍼스널케어

섬유

기타 용도

지역

아시아 태평양

중국

인도

일본

한국

기타 아시아 태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카공화국

기타 중동 및 아프리카

제6장 경쟁 구도

합병과 인수, 합작사업, 협업 및 계약

시장 점유율(%)**/랭킹 분석

유력 기업이 채택한 전략

기업 개요

Chevron Corporation

Ergon Inc.

Exxon Mobil Corporation

HollyFrontier Refining &Marketing LLC

HP Lubricants

Idemitsu Kosan Co. Ltd

LUKOIL

Nynas AB

ORGKHIM Biochemical Holding

Panama Petrochem Ltd

PetroChina

PETRONAS Lubricants International

Phillips 66 Company

Repsol

Royal Dutch Shell PLC

ENEOS Corporation

제7장 시장 기회 및 향후 동향

LYJ

영문 목차

영문목차

The Process Oils Market size is estimated at 5.08 Million tons in 2024, and is expected to reach 5.80 Million tons by 2029, growing at a CAGR of 2.74% during the forecast period (2024-2029).

The COVID-19 pandemic negatively impacted the market in 2020. However, the market reached pre-pandemic levels and is expected to grow steadily in the coming years.

Key Highlights

Over the short term, the primary factor driving the market's growth is the increasing demand for polymer production. The surge in the use of rubber oils is also likely to augment the demand for process oils in the coming years.

However, declining usage of PAH and DAE due to stringent regulations is likely to hinder the market's growth during the studied period.

Nevertheless, research in bio-based rubber process oils and the accelerating demand for process oils in electric vehicles can soon be the factors behind growth opportunities for the global market.

The Asia-Pacific region is expected to dominate the market and is also likely to witness the highest CAGR during the forecast period.

Process Oils Market Trends

Rubber Applications to Dominate the Market

Rubber process oil is manufactured using petroleum after the more volatile petrol, and heating oil fractions are separated using the distillation process.

Both natural and synthetic process oils are commercially used in producing several rubber products, including rubber bands, toys, and tires.

They are also used in the mixing process for rubber compounds as they increase the dispersion of fillers and enhance the flow characteristics of the mixture.

The expansion of the global rubber industry is promoting the use of rubber process oils across various application industries. Some typical rubber applications include tires, construction materials, white goods, biomedical, and textiles.

China is the largest tire-producing country in the world. According to the National Bureau of Statistics of China, tire production in China in 2021 was 902.46 million units, an increase of around 95 million units compared to 2020.

According to Malaysian Rubber Council, the global rubber production in the first half of 2022 was around 13.9 million metric tons, with a decline of 1.5% from the corresponding period of the previous year, where about 14.1 million metric tons were produced.

Based on the factors above, the rubber oil application for process oils is expected to dominate the market.

Asia-Pacific Region to Dominate the Market

Asia-Pacific is an area of immense potential due to the extensive demand for textiles and personal care products in countries such as India and China.

China continued to be the biggest textile and apparel exporter in the world since 1994. The country dominates the global low-to-medium-end market by mainly engaging in OEM manufacturing and processing. At the same time, the European Union continues to dominate the global upmarket and high-quality textiles.

According to OICA, automotive production in China in 2021 was at 26.08 million units, with a 3% growth from 25.22 million units in 2020. It is anticipated to positively impact the process oil market during the forecast period.

Presently, the penetration of personal care products in India is comparatively low compared to developed and other developing economies.

However, the improving economic environment and the increasing purchasing power of the Indian population are expected to increase the adoption of personal care products in the country.

According to NIPFA India, the Indian beauty and personal care industry is currently worth USD 26.8 billion and is anticipated to grow to USD 37.2 billion over the next three years. The growth of the Indian market is expected to boost the development of the process oil market during the studied period.

According to OICA, the automotive industry in India observed a growth of 30% in 2021 and produced around 4.39 million units. Rapid growth in the Automotive sector would positively impact the studied market.

Due to the factors above, the market for process oils in the Asia-Pacific region is expected to dominate the global market during the forecast period.

Process Oils Industry Overview

The process oils market is partially consolidated in nature. Some of the major players in the market are Chevron Corporation, ExxonMobil Corporation, HP Lubricants, Royal Dutch Shell Plc, and Total.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Rising Polymer Production

4.2 Restraints

4.2.1 Declining Automotive Sector

4.2.2 Declining Usage of PAH and DAE due to Stringent Regulations

4.3 Industry Value Chain Analysis

4.4 Porters Five Force Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

5.1 Type

5.1.1 Aromatic

5.1.2 Paraffinic

5.1.3 Naphthenic

5.2 Application

5.2.1 Rubber

5.2.2 Polymers

5.2.3 Personal Care

5.2.4 Textile

5.2.5 Other Applications

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle-East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share(%)**/ Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Chevron Corporation

6.4.2 Ergon Inc.

6.4.3 Exxon Mobil Corporation

6.4.4 HollyFrontier Refining & Marketing LLC

6.4.5 HP Lubricants

6.4.6 Idemitsu Kosan Co. Ltd

6.4.7 LUKOIL

6.4.8 Nynas AB

6.4.9 ORGKHIM Biochemical Holding

6.4.10 Panama Petrochem Ltd

6.4.11 PetroChina

6.4.12 PETRONAS Lubricants International

6.4.13 Phillips 66 Company

6.4.14 Repsol

6.4.15 Royal Dutch Shell PLC

6.4.16 ENEOS Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Research in Bio-based Rubber Process Oils

7.2 Rising Demand for Process Oils in Electric Vehicles