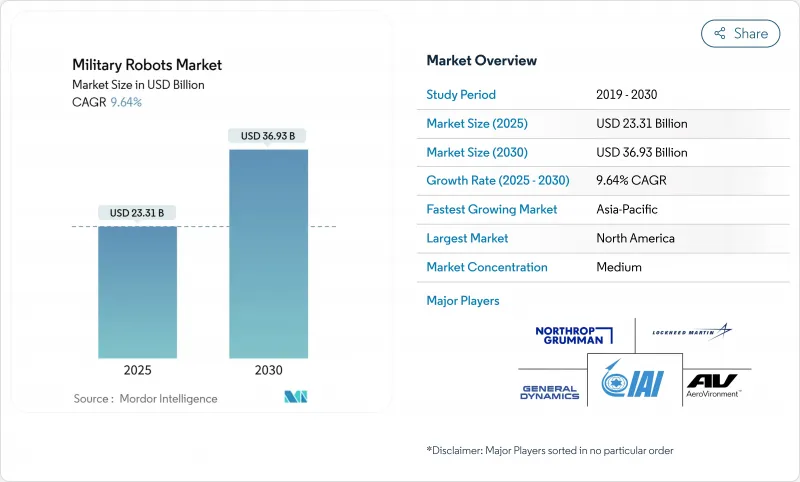

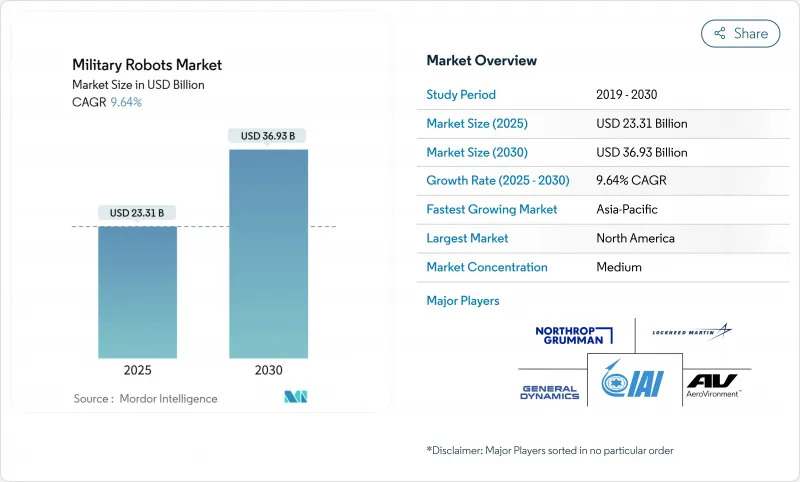

군용 로봇 시장 규모는 2025년에 233억 1,000만 달러로 추정되고, 2030년에는 369억 3,000만 달러에 이를 전망이며, CAGR 9.64%로 확대될 것으로 예측됩니다.

성장의 원동력은 우크라이나 분쟁의 교훈, NATO와 AUKUS의 독트린의 변화, 급속한 엣지 AI 혁신을 반영한 육해공에 걸친 자율 및 반자율 시스템의 급속한 채용입니다. 기존의 탑승자 플랫폼에서 무리를 잡는 무인 항공기와 비승객 지상 차량(UGV)으로의 예산 재배분이 수요를 확대하고 있습니다. 동시에 안전한 통신 및 견고한 프로세서 발전으로 인해 방해받는 환경에서도 안정적인 운영이 가능합니다. 미국 방총성의 복제 프로그램은 적대 세력을 정교한 단위가 아닌 양으로 압도하는 소모품 시스템의 대량 생산을 가속화하고 있습니다. 중국의 민군 융합 정책은 아시아태평양 전역에서 조달을 강화하는 지역적 반응을 일으키고 있습니다. 동시에 치사적 자율성에 대한 유럽 수출 규제의 강화와 사막 작전에서의 배터리 밀도의 지속적인 제한은 대항수단으로서 기능하는 것, 군용 로봇 시장의 전체적인 상승 궤도를 탈선시키기까지는 이르지 못했습니다.

동맹국의 방위 예산의 지속적인 증가는 네트워크 대응의 무인 플랫폼을 위해 계상되고 있으며, 미국 육군의 각 사단은 2026년까지 무인기를 실전 배치할 예정이며, AUKUS 파트너는 플러그 앤 파이트의 상호 운용성을 가능하게 하기 위해 커맨드 아키텍처의 조화를 도모하고 있습니다. 대규모 프라임 기업은 여러 로봇이 데이터 링크를 공유할 수 있도록 개방형 컨트롤러를 표준화하고, 통합 사이클을 단축하며, 방해 전파에 대해 향상된 소프트웨어 정의 라디오를 제공하는 공급업체를 지원합니다. 유럽 연간 국방 지출은 현재 6.1% 증가하고 있으며 레거시 탑승원 자산에서 디지털화된 포메이션에 적합한 기민하고 미션에 특화된 로봇으로 조달의 축족을 옮기는 움직임이 강해지고 있습니다. 이러한 역학을 종합하면 10년 말까지 군용 로봇 시장을 지원하는 새로운 수주 동향이 보입니다.

2025년 3월 도네츠크의 완전 로봇 공격은 저비용 UGV와 FPV의 조합으로 중장갑을 무력화할 수 있음을 증명하여 NATO의 전선 부대에 대량의 소모품 플랫폼을 중심으로 한 기동 여단의 재설계를 촉구했습니다. 수천 대의 심플한 로봇을 신속하게 제공할 수 있는 신흥기업에 자본이 흐르고, 프레임워크 계약에서는 계획적인 손실률을 상정한 비용 상한이 지정되는 경우가 많아지고 있습니다. 그 결과, 군용 로봇 시장에서는 최종 조립과 테스트를 자동화할 수 있는 규모가 큰 기업이 보상되며, 단위 이폭이 축소해도 수량이 증가하고 있습니다.

유엔 결의 78/241과 ICRC의 구속력있는 규칙에 대한 요구는 유럽 수출 허가를 늦추고, 문서화 비용을 증가시키며, AI 대응 치사 페이로드 개발주기를 늘리는 컴플라이언스 계층을 추가합니다. 이는 '휴먼 온 더 루프' 세이프가드의 기술 혁신에 박차를 가하는 한편, 단기적인 주문의 일부를 제약이 적은 지역으로 시프트시켜, 인증된 수요를 단편화하고, 군용 로봇 시장의 성장세를 약화시킵니다.

2024년 군용 로봇 시장 매출의 46.58%는 항공기 탑재형 로봇입니다. 그러나 육상 플랫폼은 13.49%의 연평균 복합 성장률(CAGR)로 확대되어 전장에서 입증된 UGV가 돌파, 부상자 피난, 센서 중계 미션에 필수적인 것으로 입증되었습니다. Ghost X와 같은 대형 쿼드 로터는 여단 ISR에 필수적인 도달범위 및 높이를 여전히 제공하고 있지만, 큰 손실을 흡수할 수 있는 공격 가능한 지상군에 대한 수요는 급격히 높아지고 있습니다. 우크라이나의 250,000 달러의 무인 항공기 탑재 USV는 해군 운영자를 군용 로봇 시장으로 끌어들이는 크로스 도메인 혁신을 강조합니다.

육상 로봇의 성장은 보다 저렴한 드라이브 트레인, 가벼운 복합 장갑, GPS 없이 장애물과의 협상을 가능하게 하는 AI 스택에 의해 더욱 촉진됩니다. 항공 플랫폼은 관련성을 유지하기 위해 멀티 페이로드 베이 및 전자 공격 포드를 추가하여 대응합니다. 약간의 슬라이스이지만, 해양 로봇은 오일 터미널 방위에 중점을 둔 GCC 해군으로부터 적을 짜낸 지출을 받고 있습니다. 영역을 넘어서는 상호작용은 공급업체의 비즈니스 기회를 넓혀 군용 로봇 시장에 새로운 진입을 가져옵니다.

인간이 조작하는 로봇이 2024년 군용 로봇 시장 점유율의 56.50%를 차지했습니다. 그러나 완전 자율 모드는 몇 밀리초 내에 위협을 분류하는 온보드 신경망 가속기 덕분에 12.84%의 연평균 복합 성장률(CAGR)로 발전하고 있습니다. CJADC2와 같은 프로그램은 지휘관이 단일 콘솔에서 대기 시간 없이 플릿을 재작업할 수 있도록 시간에 민감한 네트워킹을 통합하여 혁명적인 변화라는 보다 진화를 나타냅니다.

세미오토노미는 인지적 부하를 분할하기 때문에 여전히 주력입니다. 운영자는 임무 목표를 정의하고 오토노미는 경로 계획 및 장애물 회피를 관리합니다. 오버랜드 AI의 울트라 차량은 한 군인이 여러 자매 유닛과 함께 조종할 수 있으며 임무주기 모니터링이 노동력 요구를 완화하는 방법을 보여줍니다. 교리적 신뢰가 높아짐에 따라, 군용 로봇 시장에서는 미리 정의된 규칙 세트에 묶인 자율적으로 시작되는 교전 옵션을 볼 수 있을 것입니다.

북미는 여전히 가장 큰 지출국이며, 복제자에 대한 10억 달러의 자금 투입 및 2026년까지 미국 육군의 모든 부대에의 드론 배치가 의무화되는 것이 그 요인이 되고 있습니다. 캐나다의 NORAD 업그레이드는 극지 조건에 강한 자율형 북극 감시 타워를 실전 배치함으로써 이러한 노력을 보완하고 있습니다. 프라임기업 및 신흥기업에 걸친 성숙한 공급업체 기반이 기술의 리더십을 유지하고 이 지역에서 군용 로봇 시장의 지속적인 우위를 확보하고 있습니다.

아시아태평양은 중국의 민군 융합 보조금이 국내 규모 확장을 가속화하고 인도, 한국, 일본에서의 반응에 박차를 가하고 있기 때문에 가장 급성장하는 부문입니다. 베이징이 인형 로봇과 대량 무기를 추진함으로써 지역 조달은 저렴하고 다수의 시스템으로 이동하고, 서울 한화 에어로스페이스는 비무장지대 순찰에 최적화된 무장 UGV를 전개합니다. 남중국해의 해양 분쟁은 USV와 해저 감시 크롤러에 대한 병행 투자의 방아쇠가 됩니다.

유럽의 방위 예산은 2035년까지 매년 6.1% 증가하여 우크라이나 전쟁의 교훈에서 무인 항공기 및 지상군에 의한 방위가 유효시됩니다. 프랑스의 DROIDE 프레임워크와 독일의 새로운 연방군 로봇 계획은 NATO의 동쪽을 강화하는 긴급성을 반영합니다. 치명적인 자율성을 둘러싼 수출 허가 조사는 출하 속도를 완화시키면서도 연구개발 자금을 '인간이 관여하는' 안전 가드에 돌려 군용 로봇 시장에 유럽의 공헌을 차별화하고 있습니다.

중동에서는 석유기지 경비를 위한 해군 USV에 대한 투자가 주목받고 있습니다. 이스라엘에서는 RobDozer와 로봇형 M113의 실전 배치로 가혹한 사막 지역에서의 신뢰성이 증명되었습니다. 동시에 아랍에미리트(UAE)의 EDGE 그룹은 비전 2030의 국산화 목표를 따르는 국산 보트와 지상 로봇의 능력을 구축하고 있습니다. 사우디아라비아의 자율형 초계기에 관한 합작 사업은 군용 로봇 시장의 틈새 시장이지만 유리한 슬라이스를 더욱 확대합니다.

브라질의 2025년 국방 예산은 237억 달러로 광대한 국경과 아마존을 단속하기 위한 네트워크화된 대포 및 감시 드론에 자금이 할당되어 있습니다. 경제적인 제약이 있기 때문에 수량은 한정되지만, 반마약 감시나 재난 구호이라고 하는 지역 특유의 요구가, 정글의 상황에 맞춘 견고하고 코스트 효율이 높은 로봇의 기회를 넓히고 있습니다.

The military robots market size stands at USD 23.31 billion in 2025 and is forecast to reach USD 36.93 billion by 2030, expanding at a 9.64% CAGR.

Growth is powered by surging adoption of autonomous and semi-autonomous systems across air, land, and sea, reflecting lessons from the Ukraine conflict, shifting NATO and AUKUS doctrines, and rapid edge-AI innovation. Budget reallocations from traditional crewed platforms toward swarming drones and uncrewed ground vehicles (UGVs) are broadening demand. At the same time, advances in secure communications and ruggedized processors enable reliable operations in jammed environments. The Pentagon's Replicator program is accelerating mass production of expendable systems that overwhelm adversaries by volume rather than unit sophistication. China's civil-military fusion policies are triggering a regional response that lifts procurement across Asia-Pacific. At the same time, tightening European export rules on lethal autonomy and persistent battery-density limits in desert operations act as counterweights but have yet to derail the overall upward trajectory of the military robots market.

Sustained increases in allied defense budgets are earmarked for network-ready unmanned platforms, with every US Army division slated to field drones by 2026 and AUKUS partners harmonizing command architectures to enable plug-and-fight interoperability. Larger primes are standardizing open controllers so multiple robots can share data links, shortening integration cycles and favoring vendors that provide software-defined radios hardened against jamming. Europe's annual defense spending now grows 6.1%, reinforcing a procurement pivot from legacy crewed assets to agile, mission-specific robots that fit within digitised formations. Collectively, these dynamics add fresh order visibility that underpins the military robots market through the end of the decade.

The March 2025 fully robotic assault in Donetsk proved that low-cost UGV-and-FPV combinations can neutralise heavier armour, prompting NATO front-line armies to re-engineer manoeuvre brigades around massed expendable platforms. Capital flows to start-ups able to deliver thousands of simple robots at pace, and framework contracts increasingly specify cost ceilings that assume planned loss rates. As a result, the military robots market sees rising volumes even where unit margins compress, rewarding scale players that can automate final assembly and test.

The UN Resolution 78/241 and the ICRC's call for binding rules add compliance layers that slow European export licences, increase documentation costs, and lengthen development cycles for AI-enabled lethal payloads. While this spurs innovation in "human-on-the-loop" safeguards, it shifts some near-term orders to regions with fewer constraints, fragmenting certified demand and tempering growth momentum within the military robots market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Airborne robots generated 46.58% of the military robots market revenue in 2024. Yet, land platforms expand at a 13.49% CAGR as battle-tested UGVs prove indispensable for breaching, casualty evacuation, and sensor-relay missions. Large quadrotors such as the Ghost X still provide the reach and height essential for brigade ISR, but demand for attritable ground swarms that can absorb heavy losses is rising sharply. Ukraine's USD 250,000 drone-carrying USVs underscore cross-domain innovation that pulls naval operators into the military robots market.

Land-robot growth is further propelled by cheaper drivetrains, lighter composite armour, and AI stacks that enable obstacle negotiation without GPS. Air platforms respond by adding multi-payload bays and electronic-attack pods to stay relevant. Although a small slice, Marine robots receive targeted spending from GCC navies focused on oil-terminal defense. The interplay across domains broadens supplier opportunities and brings fresh entrants into the military robots market.

Human-operated robots held 56.50% of the military robots market share in 2024 because policy still requires human confirmation for lethal action. Fully autonomous modes, however, advance at 12.84% CAGR thanks to onboard neural-network accelerators that classify threats within milliseconds. Programs such as CJADC2 integrate time-sensitive networking so commanders can retask fleets from a single console without latency, representing evolutionary rather than revolutionary change.

Semi-autonomy remains the workhorse because it splits cognitive load: operators define mission goals while autonomy manages route-planning and obstacle avoidance. Overland AI's Ultra vehicle, one soldier can control alongside multiple sister units, illustrates how duty-cycled oversight eases workforce demands. As doctrinal trust grows, the military robots market will likely see autonomously initiated engagement options bounded by predefined rulesets.

The Military Robots Market Report is Segmented by Platform (Land, and More), Mode of Operation (Human Operated, and More), Application (Intelligence, Surveillance and Reconnaissance (ISR), and More), Payload (EO/IR Sensor Suites, and More), Weight Class (Nano/Micro, and More), Mobility (Tracked Platforms, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America remains the largest spender, anchored by USD 1 billion in Replicator funding and mandated drone deployment across all US Army divisions by 2026. Canada's NORAD upgrade complements these efforts by fielding autonomous Arctic surveillance towers resilient to polar conditions. A mature supplier base spanning primes and start-ups sustains technology leadership, ensuring continued dominance of the military robots market in the region.

Asia-Pacific is the fastest-growing segment as China's civil-military fusion subsidies accelerate domestic scale-out and spur responses from India, South Korea, and Japan. Beijing's push for humanoid robots and mass-swarms shifts regional procurement toward cheap, numerous systems, while Seoul's Hanwha Aerospace rolls out armed UGVs optimised for DMZ patrols. Maritime disputes in the South China Sea trigger parallel investment in USVs and seabed-monitoring crawlers.

Europe's defense budgets grow 6.1% annually through 2035, driven by the lessons of the Ukraine war that validate attributable drones and ground swarms. France's DROIDE framework and Germany's new Bundeswehr robotics plan reflect the urgency of reinforcing NATO's eastern flank. Export-licence scrutiny over lethal autonomy tempers shipment speed yet channels R&D funds into "human-in-the-loop" safeguards, differentiating European contributions to the military robots market.

The Middle East focuses on spending on naval USVs to guard oil terminals. Israel's operational deployment of RobDozer and robotic M113 variants proves reliability in austere desert theatres. At the same time, the UAE's EDGE Group builds indigenous boats and ground-robot capacity that is aligned with Vision 2030's localisation goals. Saudi Arabia's joint ventures on autonomous patrol craft further expand a niche but lucrative slice of the military robots market.

South America invests selectively; Brazil's USD 23.7 billion 2025 defense budget allocates funds for networked artillery and surveillance drones to police vast borders and Amazonia. Economic constraints limit volume, yet region-specific needs for anti-narcotics monitoring and disaster relief open opportunities for rugged, cost-efficient robots tailored to jungle conditions.