세계 육상 시추 리그 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2024-2029년)

Land Drilling Rig - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

상품코드:1437932

리서치사:Mordor Intelligence

발행일:2024년 02월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

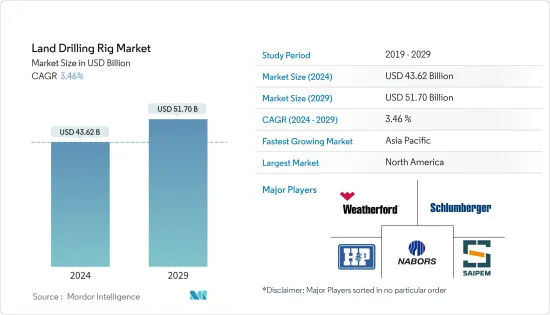

육상 시추 리그 시장 규모는 2024년에 436억 2,000만 달러로 추정되며, 2029년까지 517억 달러에 이를 것으로 예측되며, 예측 기간(2024-2029년) 동안 3.46%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다.

주요 하이라이트

중기적으로는 고마력 리그와 하이테크 리그의 사용이 증가하고 대형 리그 수요가 증가함에 따라 랜드 리그 시장은 최근 크게 진화했습니다. 게다가 원유와 천연가스 수요 증가에 대응하기 위해 비재래형 매장량을 개발하는 것은 예측 기간 동안 육상 시추 리그 시장에 큰 수요를 창출할 것으로 예상됩니다.

한편, 발전용 신재생에너지원으로의 세계의 이행은 석유 및 가스 부문에 있어서 큰 위협이 되고, 나아가 예측기간 중에 육상 굴삭 리그 시장의 성장에 있어 큰 과제가 될 것으로 예상됩니다. 기간.

그럼에도 불구하고 아시아태평양 및 중동의 대량 수요 시장은 중류 인프라에 많은 투자를 하고 있습니다. 새로운 인프라와 비교적 견고한 자본 투자 예산은 리그가 이 지역에 진입/재진입할 기회를 제공합니다.

북미는 주로 타이트 오일과 셰일 매장량의 탐사와 생산 활동 증가로 미국이 주도하는 육상 시추 리그의 가장 큰 시장 중 하나입니다.

육상 시추 리그 시장 동향

시장을 독점하는 모바일 리그 부문

휴대용 또는 모바일 리그는 데릭, 드로우 워크, 진흙 펌프를 포함한 트럭에 장착 된 유닛입니다. 휴대용 리그의 주요 이점은 리그업과 리그다운에 소요되는 시간이 짧고 트랙 대여 요건이 낮다는 것입니다.

휴대용 리그는 리노베이션 작업이나 약 10,000피트 깊이까지 시추할 때 자주 사용됩니다. 리그는 하루 8, 12 또는 24시간 기준으로 사용할 수 있으며 기존의 리그에 비해 몇 가지 장점이 있습니다.

많은 육상 리그 계약자들은 더 높은 마력의 새로운 건축물로 자사의 함대를 업그레이드하고, 탑 드라이브에서 자동화된 파이프 핸들링, 한 갱정 현장에서 다른 갱정 현장으로 빠르게 이동하기 위한 기동성 까지 고급 기술 능력을 갖춘 더 강력한 장비를 추가합니다.

베이커 퓨즈에 따르면, 2023년 10월 시점에서 육상 리그의 총 수는 736기로, 리그 총수의 약 75%를 차지했습니다. 육상 지역의 장비 수가 증가함에 따라 시추 및 생산 활동에 대한 수요가 증가할 것으로 예상되며, 이는 육상 시추 장비 시장을 견인하게 됩니다.

또한 캐나다, 중국, 아르헨티나 등 국가(미국 이외)에서 비재래형 매장량에서의 시추이 점차 기세를 늘리고 있기 때문에 하이테크리그 설계와 보다 큰 마력을 갖춘 휴대용 리그가 모바일 시추에 큰 기회를 창출할 것으로 기대됩니다. 곧 장비.

또한 원유가격 상승으로 비재래형 유전 개발로의 단계적 전환이 촉진되고 있습니다. 그 결과, 비재래형 매장량으로의 향후 프로젝트는 토지 시추 시장 수요를 촉진할 것으로 예상됩니다.

그러므로 위의 점에서 모바일 리그 부문은 예측 기간 동안 시장을 독점할 것으로 예상됩니다.

북미가 시장을 독점

석유 및 가스의 가격 상승에 따라 북미에서의 시추 활동이 증가하고 있습니다. 북미의 육상 리그 수는 2022년에 897기에 달하고, 2021년부터 약 48% 증가했습니다.

미국은 시추 활동을 강화하고 있으며 가동중인 시추 장비의 수가 가장 많습니다. 2023년 6월 현재 활성 리그 수는 약 9% 증가하여 687개를 넘었습니다. 그 결과 시추 장비에 대한 높은 수요가 발생하고 있습니다.

수압 파쇄에 있어서의 기술의 향상과 낮은 손익 분기점 가격이, 이 나라의 활발한 굴삭 활동을 지지하고 있습니다. 그 결과 국내 항공기 이용률은 2년간 하락한 후 46%로 상승했습니다. 미국에서 수평 시추 점유율이 증가함에 따라 높은 사양의 시추 장비에 대한 높은 수요가 발생했습니다.

일부 주요 계약자는 새로운 장비 주문을 받을 뿐만 아니라 이러한 요구 사항을 충족하기 위해 장비를 업그레이드합니다. 향후 수년간 미국의 시추이 개선됨에 따라 하이스펙 시추 장비에 대한 수요가 증가할 것으로 예상됩니다.

또한 캐나다에서는 기획된 수많은 오일 샌드 프로젝트의 시작과 확대로 인해 리그 수요가 크게 성장할 수 있으며 예측 기간 동안 육상 시추 리그 시장의 발전으로 이어집니다.

따라서 위의 요인을 바탕으로 북미는 예측기간 동안 세계 육상 시추 리그 시장을 독점할 것으로 예상됩니다.

육상 시추 리그 산업 개요

육상 시추 리그 시장은 적당히 통합되어 있습니다. 시장의 주요 기업(순부동)에는 Nabors Industries Ltd, Helmerich & Payne Inc., Schlumberger Limited, Saipem SpA, Weatherford International PLC 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제조건

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

소개

2028년까지 시장 규모와 수요 예측(금액)

세계 주요국 육상 가동 리그수(2022년까지)

2028년까지 온쇼어 설비 투자 예측(금액)

최근 동향과 발전

정부의 정책과 규제

시장 역학

성장 촉진요인

고마력 및 하이테크리그의 사용 증가

비재래형 매장량의 활용

억제요인

신재생에너지원으로의 이행

공급망 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 격렬

제5장 시장 세분화

유형

기존

휴대

구동 방식

기계식

전기

컴파운드

지역

북미

미국

캐나다

기타

유럽

영국

프랑스

이탈리아

독일

기타

아시아태평양

중국

인도

한국

기타

남미

브라질

아르헨티나

기타

중동 및 아프리카

아랍에미리트(UAE)

사우디아라비아

이란

이라크

카타르

기타

제6장 경쟁 구도

합병과 인수, 합작사업, 협업 및 계약

유력 기업이 채용한 전략

기업 프로파일

Nabors Industries Ltd

Helmerich &Payne Inc.

Eurasia Drilling Company Limited

Ensign Energy Services Inc.

Precision Drilling Corp.

Patterson-UTI Energy Inc.

Schlumberger Limited

Saipem SpA

Weatherford International PLC

KCA Deutag Group

제7장 시장 기회와 미래 동향

새로운 인프라와 비교적 견고한 설비 투자 예산

JHS

영문 목차

영문목차

The Land Drilling Rig Market size is estimated at USD 43.62 billion in 2024, and is expected to reach USD 51.70 billion by 2029, growing at a CAGR of 3.46% during the forecast period (2024-2029).

Key Highlights

Over the medium period, the land rig market has evolved significantly in recent years with the increasing use of high horsepower and hi-tech rigs and the increasing demand for heavy rigs. Moreover, exploiting unconventional reserves to meet the increasing demand for crude oil and natural gas is expected to create significant demand for the land drilling rig market during the forecast period.

On the other hand, the global shift towards renewable energy sources for electricity generation poses a huge threat to the oil and gas sector, which, in turn, is expected to be a major challenge for the growth of the land drilling rig market during the forecast period.

Nevertheless, the high-volume and demand markets in Asia-Pacific and the Middle Eastern regions are investing highly in midstream infrastructure. New infrastructure and relatively robust CAPEX budgets provide rigs opportunities to enter/re-enter these geographies.

North America is one of the largest markets for land drilling rigs, led by the United States, mainly due to increased exploration and production activities of its tight oil and shale reserves.

Land Drilling Rigs Market Trends

The Mobile Rig Segment to Dominate the Market

A portable or mobile rig is a truck-mounted unit that contains the derrick, draw-works, and mud pumps. The principal advantage of the portable rig includes low rig-up and rig-down time, as well as lower truck hire requirements.

Portable rigs are used frequently in workover operations and when drilling to depths of about 10,000 ft. The rigs may be used on an 8, 12, or 24-hr/day basis and have several advantages over conventional rigs.

Many land rig contractors have upgraded their fleet with higher-horsepower new builds, adding more powerful rigs with advanced technological capabilities, from top drives to automated pipe handling and the mobility to quickly move from one well site to another.

According to Baker Hughes, as of October 2023, the total land rig counts accounted for 736 units, approximately 75% of the total rig counts. With the increasing rig counts on the land region, drilling and production activity are expected to be in demand, which, in turn, will drive the land drilling rig market.

Moreover, as drilling in unconventional reserves is gradually gaining momentum in countries (other than the United States) such as Canada, China, and Argentina, portable rigs with high-tech rig designs and bigger horsepower are expected to create a significant opportunity for the mobile rigs soon.

Also, the increasing crude oil prices have favored the gradual shift towards developing unconventional fields. As a result, the upcoming projects in unconventional reserves are expected to drive the demand in the land drilling market.

Thus, owing to the above points, the mobile rig segment is expected to dominate the market in the forecast period.

North America to Dominate the Market

Drilling activities in North America have increased amid rising oil and gas prices. The North American land rig count reached 897 in 2022, i.e., an increase of around 48% from 2021.

The United States has increased its drilling activity and has the highest active rig counts. As of June 2023, the active rig count increased by around 9%, i.e., the count crossed 687, resulting in high demand for drilling rigs.

Technological improvements in hydraulic fracturing and low breakeven prices support the robust drilling activity in the country. As a result, fleet utilization in the country rose to 46% after two years of decline. The increasing share of horizontal drilling in the United States has resulted in high demand for high-specification drilling rigs.

In addition to receiving new rig orders, some large contractors upgrade their rigs to meet these requirements. As the United States drills better in the coming years, the demand for high-spec drilling rigs is expected to grow.

Also, there is a significant potential growth for rig demand in Canada, driven by the start-up and expansion of numerous planned oil sand projects, leading to the development of the land drilling rig market during the forecast period.

Therefore, based on the factors mentioned above, North America is expected to dominate the global land drilling rig market during the forecast period.

Land Drilling Rigs Industry Overview

The land drilling rig market is moderately consolidated. The key players in the market (in no particular order) include Nabors Industries Ltd, Helmerich & Payne Inc., Schlumberger Limited, Saipem SpA, and Weatherford International PLC, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2028

4.3 Global Onshore Active Rig Count of Major Countries, till 2022

4.4 Onshore CAPEX Forecast in USD billion, till 2028

4.5 Recent Trends and Developments

4.6 Government Policies and Regulations

4.7 Market Dynamics

4.7.1 Drivers

4.7.1.1 Increasing Use of High Horsepower and Hi-Tech Rigs

4.7.1.2 Exploiting Unconventional Reserves

4.7.2 Restraints

4.7.2.1 The Global Shift Towards Renewable Energy Sources

4.8 Supply Chain Analysis

4.9 Porter's Five Forces Analysis

4.9.1 Bargaining Power of Suppliers

4.9.2 Bargaining Power of Consumers

4.9.3 Threat of New Entrants

4.9.4 Threat of Substitutes Products and Services

4.9.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 Type

5.1.1 Conventional

5.1.2 Mobile

5.2 Drive Mode

5.2.1 Mechanical

5.2.2 Electrical

5.2.3 Compound

5.3 Geography

5.3.1 North America

5.3.1.1 United States of America

5.3.1.2 Canada

5.3.1.3 Rest of the North America

5.3.2 Europe

5.3.2.1 United Kingdom

5.3.2.2 France

5.3.2.3 Italy

5.3.2.4 Germany

5.3.2.5 Rest of the Europe

5.3.3 Asia-Pacific

5.3.3.1 China

5.3.3.2 India

5.3.3.3 South Korea

5.3.3.4 Rest of the Asia-Pacific

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of the South America

5.3.5 Middle-East and Africa

5.3.5.1 United Arab Emirates

5.3.5.2 Saudi Arabia

5.3.5.3 Iran

5.3.5.4 Iraq

5.3.5.5 Qatar

5.3.5.6 Rest of the Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 Nabors Industries Ltd

6.3.2 Helmerich & Payne Inc.

6.3.3 Eurasia Drilling Company Limited

6.3.4 Ensign Energy Services Inc.

6.3.5 Precision Drilling Corp.

6.3.6 Patterson-UTI Energy Inc.

6.3.7 Schlumberger Limited

6.3.8 Saipem SpA

6.3.9 Weatherford International PLC

6.3.10 KCA Deutag Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 New Infrastructure and Relatively Robust CAPEX Budgets