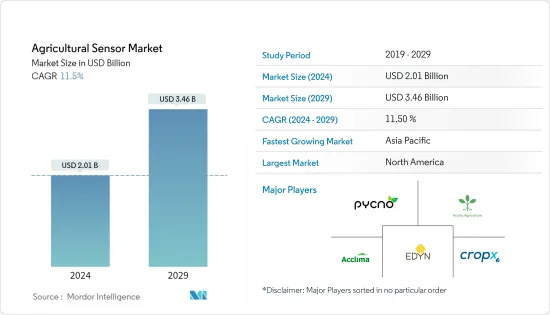

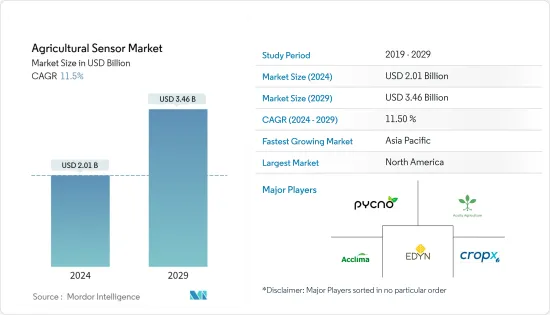

농업용 센서 시장 규모는 2024년 20억 1,000만 달러로 추정되며, 2029년까지 34억 6,000만 달러에 이를 것으로 예측되며, 예측 기간(2024-2029년) 동안 11.5%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다.

정밀한 실내 농업 기술에는 변화하는 기후 조건과 숙련 노동력 감소 과제를 해결하기 위한 새로운 기술이 필요합니다. 농부는 실내에서만 작물을 재배하는 경우 광량, 영양 수준, 수분 수준을 제어할 수 있습니다. 견고한 기능을 갖춘 소규모 제어 시스템을 갖춘 센서를 통해 기업은 시스템을 자동화하고 더 나은 방법으로 수율을 향상시킬 수 있습니다. 센서를 도입한 후에는 노동력이 약 20.0% 줄어들 수 있습니다. 농업용 센서는 실내 농장에서 노동력 문제를 해결할 수 있습니다.

대규모 산업용 실내 농장에서는 수질 오염, 잔류 농약, 영양소 부족, 질병 공격 등을 감지 할 수있는 센서가 사용됩니다. 실내 농업과 농업용 센서의 조합은 작물의 생산 능력을 향상시키고 향후 농업용 센서 시장을 견인할 수 있습니다.

따라서 토양 수분 센서와 같은 하이테크 관개 도구는 농부가 각 지역에서 필요한 물의 수준을 결정하는 데 도움이 됩니다. IoT 지원 장치의 스마트 관개 애플리케이션은 관개 장비의 제어 및 모니터링을 지원하고 변화하는 요구 사항에 따라 조정할 수 있습니다. 둘 다 지하수위가 저하된 지역에서 정밀 관개를 실시할 수 있는 폭넓은 범위를 나타내고 있습니다. 이러한 요인은 예측 기간 동안 시장을 견인할 수 있습니다.

북미는 농업용 센서의 가장 규모가 큰 지역 시장입니다. 농업 생산을 증가시키는 정부의 강력한 지원, 인프라 지원 가용성, 스마트 및 세차 농업법의 수락으로 첨단 농업 솔루션의 도입이 증가했습니다. 북미에서는 토양 수분 센서의 채용이 급속히 증가하고 있습니다. 토양 수분측정기는 잔디밭의 보다 효율적인 모니터링 및 전환을 위해 스포츠 잔디 분야에서 사용됩니다. 연구에 따르면 센서를 도입함으로써 농가는 가뭄 스트레스를 최소화하고 보호 재배 유지비와 인건비를 적어도 20% 절감할 수 있다는 것을 알고 있습니다.

미국은 정밀 농업 기술을 신속하게 도입하고 있으며, 이는 이 지역 세계 시장에서 가장 큰 점유율의 주요 요인이 되고 있습니다. 미국의 농업 부문은 최근 스마트 농업 실천 도입과 관련하여 획기적인 혁명을 경험하고 있습니다. 사물인터넷(IoT) 휴대폰 장치, 기어 센서 기반 관개 및 시비 장치, 밸브 위치 센서 등의 센서 기반 기술의 출현은 이 분야에서 비교적 새로운 것으로, 이 나라에서는 새로운 현상이 보입니다. 주로 농민들이 채용하는 기계화율 증가와 스마트 농업 관행에 의해 센서 수요가 발견되었습니다. 캐나다의 현대 농업 기법의 상당한 수용은 산업 성장에 기여하고 있습니다.

농업용 센서 시장은 세분화되어 있으며, 다양한 중소기업과 소수의 대기업이 시장에서 활동하고 있어 치열한 경쟁이 발생하고 있습니다. 시장의 주요 기업으로는 Edyan, Acclima Inc., CropX inc., Pycno, Acquity Agriculture 등이 있습니다. 세계 각지에서 지역 시장과 현지 기업의 발전이 시장 세분화의 주요 요인입니다. 북미와 아시아태평양은 경쟁사의 활동이 가장 활발한 두 지역입니다.

The Agricultural Sensor Market size is estimated at USD 2.01 billion in 2024, and is expected to reach USD 3.46 billion by 2029, growing at a CAGR of 11.5% during the forecast period (2024-2029).

Precision and indoor farming techniques demand new techniques to address the challenges of fluctuating climatic conditions and decreased skilled labor force. The farmer can control light amounts, nutrition levels, and moisture levels when they are growing crops solely indoors. Sensors with small-scale control systems with robust functionality would allow businesses to automate their systems and increase yields in a better way. The post-adoption of sensors may reduce the labor force by around 20.0%. Agricultural sensors can address the labor challenge in indoor farms.

Big industrial indoor farms use sensors that can sense water contamination, pesticide residues, nutrient shortages, disease attacks, etc. The combination of indoor farming and agricultural sensors will likely enhance crops' production capacities, which may drive the agricultural sensors market in the future.

As such, high-technology irrigation tools, such as soil moisture sensors, can help farmers determine the level of water requirement in each area. Smart irrigation applications in IoT-enabled devices can help control and monitor the irrigation equipment to adjust it based on changing requirements. Both represent a wide scope for undertaking precision irrigation in regions with depleted groundwater levels. These factors are likely to drive the market during the forecast period.

North America is the largest regional market for agricultural sensors. Strong government support to increase agricultural production, availability of infrastructure support, and acceptance of smart and precession farming methods increased the deployment of advanced farming solutions. In North America, the adoption of soil moisture sensors has rapidly increased. Soil moisture instruments are used in the sports turf segment for more efficient monitoring and conversion of turfgrass. Studies indicate that adopting sensors helps farmers minimize drought stress and reduces maintenance and labor costs of protected cultivation by at least 20%.

The United States is the early adopter of precision farming technologies, the primary factor responsible for the region's most significant share in the global market. The US agricultural sector has undergone a groundbreaking revolution regarding adopting smart farming practices in recent years. Although the advent of sensor-based technologies, such as Internet of Things (IoT) cellular devices, gear tooth sensor-based irrigation and fertilization equipment, and valve position sensors, is relatively new in the domain, the country has been witnessing a new-found demand for sensors, primarily due to the increased rate of mechanization and smart agricultural practices adopted by the farmers. A considerable acceptance of modern agriculture methods by Canada is contributing to industry growth.

The agricultural sensor market is fragmented, with various small and medium-sized companies and a few big players operating in the market, resulting in stiff competition. Some of the major players in the market include Edyan, Acclima Inc., CropX inc., Pycno, and Acquity Agriculture. The development of regional markets and local players in different parts of the world is the major factor for the fragmented nature of the market. North America and Asia-Pacific are the two regions showing maximum competitor activities.