ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

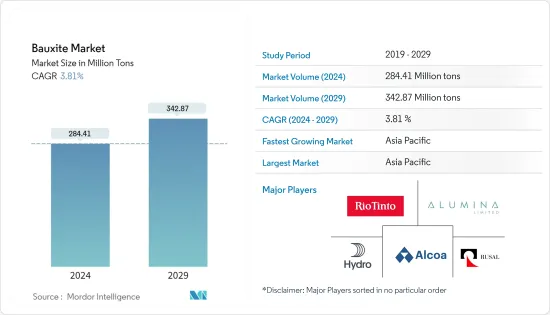

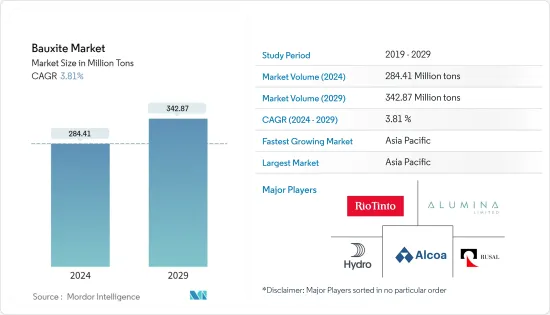

보크사이트 시장 규모는 2024년 2억 8,441만 톤으로 추정되며, 2029년까지 3억 4,287만 톤에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 3.81%의 CAGR로 성장할 것으로 예상됩니다.

주요 하이라이트

2020년 신종 코로나바이러스 감염증(COVID-19)의 확산으로 인해 시장은 부정적인 영향을 받았으며, 전 세계적으로 국가 봉쇄가 시행되어 제조 활동과 공급망 중단, 생산 중단이 발생했습니다. 그러나 2021년에는 상황이 회복되기 시작하면서 시장의 성장 궤도를 회복하기 시작했습니다.

중기적으로 조사 대상 시장을 이끄는 주요 요인은 시멘트 산업에서의 사용 가속화와 산업 응용 분야에서 알루미나의 지속적인 사용입니다.

보크사이트 채굴과 관련된 환경 문제는 향후 몇 년 동안 시장 성장을 저해할 것으로 예상됩니다.

내화물 및 연마재와 같은 상업적 용도의 수요 증가와 중국의 보크사이트 생산량 정체는 조사 대상 시장의 기회로 작용할 것으로 예상됩니다.

아시아태평양은 세계 보크사이트 시장을 독점하고 있으며 향후 몇 년 동안 가장 빠른 성장을 기록할 것으로 예상됩니다.

보크사이트 시장 동향

야금용 알루미나 수요 증가

보크사이트는 알루미늄을 많이 함유한 퇴적암입니다. 그것은 알루미늄과 갈륨의 주요 공급원이며 주로 gibbsite, bemite 및 diaspore와 같은 알루미늄 광물로 구성됩니다.

보크사이트는 알루미나 함량이 높기 때문에 알루미나 생산의 주요 공급원이며, 이후 가공을 거쳐 최종 제품 및 알루미나 생산이 이루어집니다. 따라서 알루미나 생산량의 증가가 조사 대상 시장을 주도하고 있습니다.

알루미나는 저밀도, 무독성, 높은 열전도율, 우수한 내식성, 쉬운 주조, 가공 및 성형 등 다양한 우수한 특성으로 인해 수요가 증가하고 있습니다. 알루미나 생산량 증가는 향후 몇 년 동안 보크사이트 시장을 견인할 것으로 예상됩니다.

알루미나는 주요 산업 목적으로 사용됩니다. 알루미늄 제조 외에도 점화 플러그의 절연체 및 금속 페인트 제조에 사용되며, 고체 로켓 부스터의 연료 성분으로도 사용됩니다.

또한 알루미나는 양자 간섭 장치 및 전자 트랜지스터와 같은 초전도 장치 제조에도 사용됩니다. 산화알루미늄 또는 알루미나는 방사선 방호용 선량계로도 사용됩니다.

미국 지질 조사에 따르면 세계 보크사이트 자원은 550억 톤에서 750억 톤으로 추정되며, 이는 향후 세계 금속 수요를 충족시키기에 충분합니다.

미국 인구 조사국에 따르면, 2021년에는 광업 및 채석업의 수익이 1,360억 8,000만 달러, 2022년에는 1,430억 9,000만 달러에 달할 것으로 예상했습니다. 이 부문의 수익은 2023년에 15억 2,250만 달러에 달할 것으로 예상됩니다.

미국 지질조사국이 발표한 데이터에 따르면 보크사이트와 알루미나는 27억 9,000만 톤에서 크게 증가했습니다.

광업과 야금은 캐나다의 주요 산업입니다. 캐나다는 전 세계에 60개 이상의 금속과 광물을 공급하고 있습니다. 광업은 혁신과 신기술에 투자하고 있으며, 이로 인해 이 분야가 빠르게 재편되고 있습니다. 광업 업계에서도 통합이 이루어지고 있어 향후 몇 년 동안 업계의 성장 전망에 대한 추측을 불러일으켰습니다.

따라서 위의 모든 요인으로 인해 야금 목적의 알루미나에 대한 수요 증가는 예측 기간 동안 조사 된 시장의 수요를 증가시킬 것으로 예상됩니다.

아시아태평양이 시장을 독점

아시아태평양은 예측 기간 동안 보크사이트 시장을 지배할 것으로 예상됩니다. 중국, 호주, 인도와 같은 국가의 급속한 산업화와 건축, 건설, 호일 및 포장과 같은 다양한 산업에서 알루미늄 사용량이 증가함에 따라이 지역의 보크사이트에 대한 수요가 계속 증가하고 있습니다.

또한 내식성, 고연성, 고강도, 경량 등 알루미늄의 우수한 특성으로 인해 경차 부품 제조에 알루미늄 채택이 증가하여이 지역의 보크 사이트 시장을 주도하고 있습니다.

또한 보크사이트는 높은 융점으로 인해 내화 제품의 원료로 사용되기 때문에 이 지역에서 수요가 증가하고 있습니다. 내화 등급 보크사이트는 전기 아크로와 용광로 지붕을 받쳐주는 벽돌을 만드는 데 사용됩니다.

보크사이트는 시멘트 제조를 위해 석회석과 혼합하여 시멘트를 만드는데도 사용됩니다. 생산된 시멘트는 알루미나 함량이 높고 침강 시간이 빠르고 강도가 높아 이 지역에서 보크사이트에 대한 수요가 증가하고 있습니다.

전기차의 증가 추세는 알루미늄 합금에 대한 수요를 더욱 증가시킬 수 있습니다. 중국 정부는 2025년까지 전기자동차 생산 보급률이 20%에 달할 것으로 예상하고 있습니다. 이는 2022년 사상 최고치를 기록한 중국의 전기차 판매 추세에 반영되어 있습니다. 중국 승용차 협회에 따르면, 중국은 전기자동차 판매량을 기록했습니다. 2022년에는 567만 대의 전기차 및 플러그인 자동차가 판매될 것으로 예상되며, 이는 2021년 판매량의 거의 두 배에 달합니다.

국내 전자제품 제조 부문은 100% 해외직접투자(FDI), 산업 허가증 불필요, 수동에서 자동 생산 공정으로의 기술 전환 등 정부의 유리한 정책 덕분에 안정적인 속도로 성장하고 있습니다. 수정된 인센티브 특별 패키지 제도(M-SIPS)와 전자제품 개발 기금(EDF)과 같은 새로운 인센티브가 1억 1,400만 달러의 예산으로 인도 내에서 전자제품의 국내 제조를 위해 시작되었습니다.

아시아태평양에서 사업을 전개하고 있는 주요 제조업체로는 Alumina Limited, Australian Bauxite Limited, Rio Tinto 등이 있습니다.

따라서 앞서 언급한 요인으로 인해 예측 기간 동안 이 지역의 보크사이트에 대한 수요가 증가할 수 있습니다.

보크사이트 산업 개요

보크사이트 시장은 본질적으로 부분적으로 통합되어 있으며, 주요 기업들이 세계 시장에서 큰 점유율을 차지하고 있습니다. 주요 기업으로는 Rio Tinto, RusAL, Alcoa Corporation, Alumina Limited, Norsk Hydro ASA 등이 있습니다.

기타 혜택

엑셀 형식의 시장 예측(ME) 시트

3개월간 애널리스트 지원

목차

제1장 서론

조사 가정

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

산업 용도에서 알루미나의 지속적 사용

시멘트 산업에서의 사용 가속

기타 촉진요인

성장 억제요인

보크사이트 채굴에 관한 환경 문제

기타 저해요인

산업 밸류체인 분석

Porter's Five Forces 분석

공급 기업의 교섭력

소비자의 협상력

신규 참여업체의 위협

대체품의 위협

경쟁 정도

생산 분석

제5장 시장 세분화(시장 규모 : 수량 기준)

용도

야금용 알루미나

시멘트

내화물

연마재

기타

지역

아시아태평양

중국

인도

일본

한국

호주 및 뉴질랜드

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

러시아

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카공화국

기타 중동 및 아프리카

제6장 경쟁 상황

M&A, 합작투자, 제휴, 협정

시장 점유율(%)/순위 분석

주요 기업의 전략

기업 개요

Alcoa Corporation

Alumina Limited

Aluminum Corporation of China Limited

Australian Bauxite Limited

Compagnie des Bauxites de Guinee(CBG)

GRAFIT MADENCILIK SAN. TIC. A.S.

Iranian Aluminium Co.

LKAB Minerals

Norsk Hydro ASA

Possehl Erzkontor GmbH & Co. KG

Queensland Alumina Limited

Rio Tinto

RusAL

Vimetco NV

YunXiang Develop Co.,Limited

제7장 시장 기회와 향후 동향

ksm

영문 목차

영문목차

The Bauxite Market size is estimated at 284.41 Million tons in 2024, and is expected to reach 342.87 Million tons by 2029, growing at a CAGR of 3.81% during the forecast period (2024-2029).

Key Highlights

The market experienced negative impacts in 2020 due to the COVID-19 outbreak, which led to nationwide lockdowns worldwide, disruptions in manufacturing activities and supply chains, and production halts. However, in 2021, the conditions began to recover, restoring the growth trajectory of the market.

In the medium term, the major factors driving the market studied are accelerating usage in the cement industries and continuous usage of alumina from industrial applications.

Environmental concerns related to bauxite mining are expected to hinder market growth in the coming years.

Increasing demand from commercial applications such as refractories and abrasives and leveling off of bauxite production from China is expected to act as an opportunity for the market studied.

Asia-Pacific dominated the global bauxite market and is also expected to register the fastest growth in the years to come.

Bauxite Market Trends

Increasing Demand of Alumina for Metallurgical Purposes

Bauxite is a sedimentary rock having a high content of aluminum. It is the main source of aluminum & gallium and consists mostly of aluminum minerals, namely gibbsite, boehmite, and diaspore.

Because of its high alumina content, bauxite is a primary source for alumina production, which is then processed to produce finished products and alumina production. Thus rising alumina production is driving the market studied.

The demand for alumina is increasing owing to its various superior properties such as low density, non-toxic nature, high thermal conductivity, excellent corrosion resistivity, and its ability to be easily cast, machined, and formed. Rising alumina production is expected to drive the market for bauxite through the upcoming years.

Alumina is used for key industrial purposes. Other than producing aluminum, it is used for the production of spark plug insulators and metallic paints, and it is used as a fuel component for solid rocket boosters.

Furthermore, alumina is used for the fabrication of superconducting devices, such as quantum interference devices and electron transistors. Aluminum oxide or alumina is also used as a dosimeter for radiation protection.

According to a US Geological survey, global resources of bauxite are estimated to be between 55 billion and 75 billion tons and are sufficient to meet world demand for metal well into the future.

As per the United States Census Bureau, revenue in mining and quarrying amounted to USD 14.39 billion in 2022, as compared to USD 13.68 billion in 2021. The revenue from this sector is projected to amount to USD 15.25 billion in 2023.

As per data published by the United States Geological Survey, the bauxite and alumina increased significantly from 2790 million metric tons.

Mining and metallurgy are key industries in the country. Canada supplies over 60 metals and minerals to different countries worldwide. The mining industry invests in innovation and new technologies, which rapidly reshapes the sector. The mining industry also witnessed consolidations, which led to speculations regarding the growth prospects for the industry in the coming years.

Therefore, owing to all the above-mentioned factors, increasing demand for alumina for metallurgical purposes is expected to boost the demand for the market studied over the forecast period.

Asia-Pacific to Dominate the Market

Asia-Pacific is expected to dominate the market for bauxite during the forecast period. In countries such as China, Australia, and India, owing to rapid industrialization and an increase in the usage of aluminum in various industries, such as building and construction, foil, and packaging, the demand for bauxite continues to increase in the region.

Furthermore, superior properties of aluminum, like corrosion resistance, high ductility, high strength, and lightweight, have led to an increase in the adoption of aluminum for producing light vehicle parts, which is propelling the bauxite market in the region.

Additionally, demand for bauxite is rising in the region due to its usage as a raw material in making refractory products since it has a high melting point. Refractory grade bauxite is used to manufacture bricks to line the roof of electric arc steel-making furnaces and blast furnaces.

Bauxite is also used for manufacturing cement by mixing it with limestone. The cement produced has high alumina content and is known for its rapid settling time and strength, leading to an increasing demand for bauxite in the region.

The increasing trend of electric vehicles may further propel the demand for aluminum alloys. The government of China estimates a 20% penetration rate of electric vehicle production by 2025. This is reflected in the electric vehicle sales trend in the country, which went record-breaking high in 2022. As per the China Passenger Car Association, the country sold 5.67 million EVs and plug-ins in 2022, touching almost double the sales figures achieved in 2021.

The domestic electronics manufacturing sector has been expanding at a steady rate, owing to favorable government policies, such as 100% Foreign Direct Investment (FDI), no requirement for an industrial license, and the technological transformation from manual to automatic production processes. New incentives, such as the Modified Incentive Special Package Scheme (M-SIPS) and Electronics Development Fund (EDF), have been started in the country with a budget of USD 114 million for the domestic manufacturing of electronics in India.

Some of the major manufacturers of the market studied operating in Asia-Pacific include Alumina Limited, Australian Bauxite Limited, and Rio Tinto.

Therefore, the aforementioned factors are likely to boost the demand for bauxite in the region during the forecast period.

Bauxite Industry Overview

The bauxite market is partially consolidated in nature, with top players accounting for a significant share of the global market. Some of the major companies in the market include Rio Tinto, RusAL, Alcoa Corporation, Alumina Limited, and Norsk Hydro ASA, among others (not in any particular order).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Continuous Usage of Alumina from Industrial Applications

4.1.2 Accelerating Usage in the Cement Industries

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Environmental Concern Related to Bauxite Mining

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

4.5 Production Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

5.1 Application

5.1.1 Alumina for Metallurgical Purposes

5.1.2 Cement

5.1.3 Refractories

5.1.4 Abrasives

5.1.5 Other Applications

5.2 Geography

5.2.1 Asia-Pacific

5.2.1.1 China

5.2.1.2 India

5.2.1.3 Japan

5.2.1.4 South Korea

5.2.1.5 Australia and New Zealand

5.2.1.6 Rest of Asia-Pacific

5.2.2 North America

5.2.2.1 United States

5.2.2.2 Canada

5.2.2.3 Mexico

5.2.3 Europe

5.2.3.1 Germany

5.2.3.2 United Kingdom

5.2.3.3 Italy

5.2.3.4 France

5.2.3.5 Russia

5.2.3.6 Rest of Europe

5.2.4 South America

5.2.4.1 Brazil

5.2.4.2 Argentina

5.2.4.3 Rest of South America

5.2.5 Middle-East and Africa

5.2.5.1 Saudi Arabia

5.2.5.2 South Africa

5.2.5.3 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Alcoa Corporation

6.4.2 Alumina Limited

6.4.3 Aluminum Corporation of China Limited

6.4.4 Australian Bauxite Limited

6.4.5 Compagnie des Bauxites de Guinee (CBG)

6.4.6 GRAFIT MADENCILIK SAN. TIC. A.S.

6.4.7 Iranian Aluminium Co.

6.4.8 LKAB Minerals

6.4.9 Norsk Hydro ASA

6.4.10 Possehl Erzkontor GmbH & Co. KG

6.4.11 Queensland Alumina Limited

6.4.12 Rio Tinto

6.4.13 RusAL

6.4.14 Vimetco NV

6.4.15 YunXiang Develop Co.,Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Increasing Demand from Commercial Applications such as Refractories and Abrasives

7.2 Levelling Off of Bauxite Production from China