ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

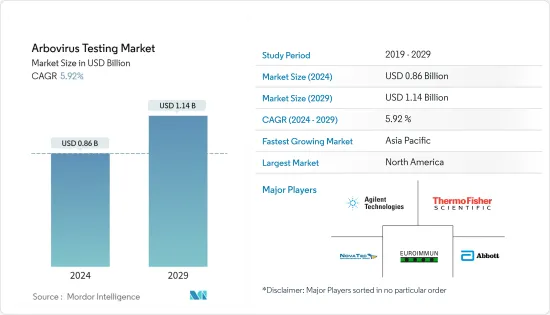

아르보바이러스 검사 시장 규모는 2024년 8억 6,000만 달러로 추정되고, 2029년까지 11억 4,000만 달러에 이를 것으로 예측되며, 예측 기간(2024-2029년) 동안 5.92%의 연평균 복합 성장률(CAGR)로 성장할 것으로 예상됩니다.

주요 하이라이트

아르보바이러스 검사 시장의 성장을 설명하는 주요 요인은 세계의 아르보바이러스 발생률과 유병률 증가, 최근 기술의 진보 및 예측 기간 동안 아르보바이러스 검사 시장을 견인할 가능성이 있는 신흥 신속혈청학 검사입니다.

예를 들어 WHO 보고에 따르면 뎅기열 증례보고 수는 지난 20년간 15배 이상으로 증가했으며, 2000년 50만 5,430명에서 2010년 2,400,138명 이상, 2015년에 3,312,040명으로 되었습니다. 2000년부터 2015년까지 사망자 수는 960명에서 200명 이상으로 증가했습니다. 4032는 아르보바이러스 질환의 발생률 증가를 강력하게 뒷받침합니다.

따라서 아르보바이러스 질환의 발생률은 예측 기간 동안 아르보바이러스 검사 시장 성장을 가속합니다. 그러나 시험관 내 시설 부족, 의식 부족 및 진단 검사 절차의 가용성 제한으로 인해 예측 기간 동안 조사 대상 시장의 성장이 억제될 수 있습니다.

아르보바이러스 검사 시장 동향

검사 유형 부문에서 역전사 중합효소 연쇄반응(RT-PCR) 기반 검사는 시장을 독점하고 있으며 예측 기간 동안 유사한 경향이 예상됩니다.

RT-PCR 기반 검사 부문은 이점으로 인해 예측 기간 동안 아르보바이러스 검사 시장을 독점할 것으로 예상됩니다. ELISA(효소 결합 면역흡착 측정법)와 PCR 검사의 주요 차이점은 검출 한계입니다. 통상, ELISA 베이스의 방법에서는 104-106 CFU/ml가 한계이지만, PCR 방법에서는 103 CFU/ml의 범위에서 검출할 수 있습니다. 검출 한계의 이러한 차이는 일반적으로 ELISA 방법에 더 긴 농축 시간이 필요하다는 것을 의미합니다. 감도면에서도 PCR 기술은 ELISA보다 훨씬 민감하고 특이합니다. PCR 기술을 채택함으로써 실험실에서 발생하는 폐기물은 ELISA에 비해 적습니다. 따라서 이러한 모든 요인들을 종합하면 예측 기간 동안 RT-PCR 기반 검사가 아르보바이러스 검사 시장을 독점하고 있음을 시사합니다.

북미는 시장을 독점하고 있으며 예측 기간 동안에도 비슷한 상황이 예상됩니다.

북미는 예측 기간 동안 전체 시장을 지배할 것으로 예상되며, 이는 이 지역의 선진 경제, 의료 지출 증가, 기술적으로 선진적인 제품의 높은 채용으로 인한 것으로 예상됩니다. 따라서 예측 기간 동안 북미는 아르보바이러스 검사 시장을 독점합니다. 아시아태평양 시장은 인구 밀도가 높고 아르보바이러스 질환이 쉽게 확산되기 쉽기 때문에 높은 CAGR을 나타낼 것으로 예상됩니다.

아르보바이러스 검사 산업 개요

아르보바이러스 검사 시장은 적당한 경쟁을 가지고 있으며 여러 주요 기업으로 구성되어 있습니다. 헬스케어 분야에서는 다양한 조직의 통합이나 제품 리콜이 증가하고 있어, 장래에 주요 기업간에서 경쟁기업간의 적대관계가 발생할 것으로 예상됩니다. 시장의 주요 기업으로는 Agilent Technologies Inc., Thermo Fisher Scientific, NovaTec Immundiagnostica GmbH, Euroimmun AG, Abbott Laboratories 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 서론

조사의 성과

조사의 전제

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

시장 개요

시장 성장 촉진요인

아르보바이러스 발생률 및 유병률 증가

기술의 진보

신속혈청 검사

시장 성장 억제요인

시험관내 시설의 부족

진단 검사 절차의 인식 부족 및 제한된 이용 가능성

Porter's Five Forces 분석

신규 참가업체의 위협

구매자 및 소비자의 협상력

공급기업의 협상력

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

검사 유형별

ELISA 기반 검사

RT-PCR 베이스 검사

기타

최종 사용자별

진단 실험실

병원

연구센터

기타

지역별

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

스페인

기타 유럽

아시아태평양

중국

일본

인도

호주

한국

기타 아시아태평양

중동 및 아프리카

GCC

남아프리카

기타 중동 및 아프리카

남미

브라질

아르헨티나

기타 남미

제6장 경쟁 구도

기업 프로파일

Agilent Technologies Inc.

Thermo Fisher Scientific

NovaTec Immundiagnostica GmbH

Euroimmun AG

Abbott Laboratories

DiaSorin SpA

Bio-Rad

Fluke Biomedical

Copley Scientific

Distek

제7장 시장 기회 및 앞으로의 동향

AJY

영문 목차

영문목차

The Arbovirus Testing Market size is estimated at USD 0.86 billion in 2024, and is expected to reach USD 1.14 billion by 2029, growing at a CAGR of 5.92% during the forecast period (2024-2029).

Key Highlights

The major factors accounting for the growth of the arbovirus testing market are the increasing rate of incidence and prevalence of Arbovirus throughout the world, recent advancements in technology, and emerging rapid Serology Tests that may drive the arbovirus testing market during the forecast period.

For example, WHO has reported that the number of dengue cases reported increased over 15-fold over the last two decades, from 505,430 cases in 2000 to over 2,400,138 in 2010 and 3,312,040 in 2015. Deaths from 2000 to 2015 increased from 960 to more than 4032, which strongly supports the increase in the incidence of arboviral diseases.

Thus, the incidence rate of Arboviral diseases drives the growth of the arbovirus testing market during the forecast period. However, the lack of in vitro facilities, lack of awareness, and limited availability of diagnostic testing procedures may restrain the studied market's growth during the forecast period.

Arbovirus Testing Market Trends

In Test Type Segment, Reverse Transcriptase Polymerase Chain Reaction (RT-PCR) Based Tests Dominates the Market and the Same is Expected Over the Forecast Period.

The RT-PCR based tests segment is expected to dominate the arbovirus testing market over the forecast period, attributing to its advantages. A key difference between ELISA (Enzyme-linked immunosorbent assay) and PCR tests is the detection limit. Typically, an ELISA-based method will have a limit of 104-106 CFU/ml, whereas a PCR method can detect in the range of 103 CFU/ml. This difference in detection limit usually means that a longer enrichment time is required for an ELISA method. Even in terms of sensitivity, the PCR technique is very sensitive and specific over ELISA. The wastes produced in the laboratories by adopting the PCR technique are less compared to ELISA. Hence, all these factors together suggest that RT-PCR based tests dominate the arbovirus testing market during the forecast period.

North America Dominates the Market and the Same is Expected Over the Forecast Period.

North America is expected to dominate the overall market, throughout the forecast period, which has been attributed to the developed economy, increasing health care expenditure, and high adoption of technologically advanced products in the region. Thus, North America dominates the arbovirus testing market during the forecast period. The market in Asia-Pacific is expected to register a high CAGR due to larger population density, which facilitates the easy spread of the arboviral diseases.

Arbovirus Testing Industry Overview

The arbovirus testing market is moderately competitive and consists of several major players. With the increasing consolidations of various organizations and product recalls in the healthcare sector, it is expected to generate competitive rivalry among the key players in the future. Some of the major players of the market are Agilent Technologies Inc., Thermo Fisher Scientific, NovaTec Immundiagnostica GmbH, Euroimmun AG, and Abbott Laboratories, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Deliverables

1.2 Study Assumptions

1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.2.1 Increase in the Incidence and Prevalence of Arbovirus

4.2.2 Advancement in Technology

4.2.3 Rapid Serology Tests

4.3 Market Restraints

4.3.1 Lack of In vitro Facilities

4.3.2 Lack of Awareness and Limited Availability of Diagnostic Testing Procedures