ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

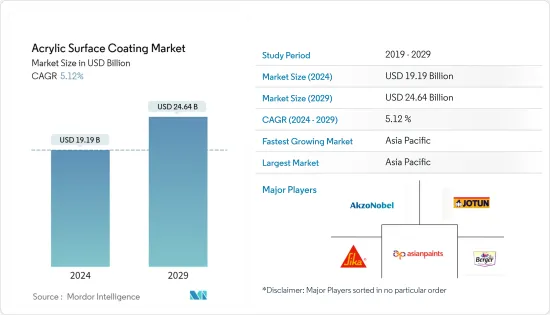

아크릴 표면 코팅 시장 규모는 2024년에 191억 9,000만 달러로 추정되고, 2029년까지 246억 4,000만 달러에 이를 것으로 예측되며, 예측 기간(2024-2029년) 동안 5.12%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다.

건축용 코팅의 용도 증가는 시장 성장을 가속할 것으로 예상됩니다. 반면에 세계의 자동차 생산 감속은 시장 성장을 방해할 것으로 예상됩니다.

주요 하이라이트

아크릴 표면 코팅 시장은 건축 및 건설 산업 수요 증가로 예측 기간 동안 성장할 것으로 예상됩니다.

아시아태평양은 세계 시장을 독점하고 있으며 주요 소비국은 중국, 인도, 일본입니다.

아크릴 표면 코팅 시장 동향

건축 및 건설 부문에서의 수요 증가

아크릴 표면 코팅은 옥외 조건에 노출된 경우에도 불활성이고 색 유지성이 우수하기 때문에 건축 및 건설 분야에서 널리 사용됩니다. 아크릴은 에멀젼(라텍스), 래커, 에나멜, 파우더 등 다양한 형태로 사용할 수 있습니다.

아크릴 폴리머의 주성분은 아크릴산과 메타크릴산이며, 자외선을 흡수하기 어려운 폴리머 구조로 되어 있습니다. 유성 페인트, 알키드, 에폭시보다 내후성과 산화에 대한 내성이 높기 때문에 건축 및 건설 분야에서의 용도가 증가했습니다.

남아프리카 정부는 2050년까지 에너지, 교통, 디지털 통신, 수도에 걸친 인프라 정비를 실현하는 '국가 인프라 계획 2050'을 책정했습니다. 2040년까지 3,300억 달러가 인프라 정비에 투자될 예정입니다.

또한 미국 인구조사국이 작성한 추가 통계에 따르면 미국의 연간 신축건설액은 2021년 1조 4,998억 2,200만 달러에 비해 2022년에는 1조 6,575억 9,000만 달러에 달했습니다. 게다가 미국의 주택건설의 연간액은 미국의 평가액은 2021년의 7,406억 4,500만 달러에 대해, 2022년의 8,491억 6,400만 달러에 달했습니다. 이 나라의 연간 비주택 건설액은 2021년 7,591억 7,700만 달러에 비해 2022년 8,084억 2,700만 달러로 시장 소비가 감소하고 있습니다.

캐나다 건설 협회에 따르면, 건설 부문은 캐나다 최대의 고용주 중 하나이며 국가의 경제적 성공에 크게 기여하고 있다고 합니다. 이 산업은 연간 약 1,410억 달러를 창출해 국가의 국내총생산(GDP)의 7.5%에 공헌하고 있습니다.

건축 및 건설 산업은 아크릴 표면 코팅의 사용으로 주도하고 있으며, 중국, 독일, 미국, 인도, 일본이 시장에서 주요 역할을 수행하고 있습니다.

아시아태평양이 시장을 독점

아시아태평양은 예측 기간 동안 아크릴 표면 코팅 시장을 독점할 것으로 예상됩니다. 건축 및 건설 부문의 성장으로 중국, 인도, 일본 등 국가에서 아크릴 표면 코팅 수요가 증가하고 있습니다.

아크릴 표면 코팅의 가장 큰 생산자는 아시아태평양에 있습니다. 아크릴 표면 코팅을 제조하는 선도 기업은 아시아 페인트, 버거 페인트 인디아 리미티드, Akzo Nobel NV, Jotun, Sika AG 등이 있습니다.

중국의 14차 5년 계획은 에너지, 교통, 수도 시스템, 도시화의 새로운 인프라 프로젝트에 중점을 둡니다. 추계에 의하면, 제14차 5개년 계획 기간(2021-2025년)중의 새로운 인프라에의 총 투자액은 약 27조원(4조 2,000억 달러)에 달할 것으로 보여지고 있습니다.

중국의 도시화율은 세계에서 가장 높은 부류에 들어갑니다. 중국의 도시화율은 2022년에 64.7%에 달했지만, 이 도시 재생 정책은 정부가 중국의 도시생활조건 개선을 목표로 하는 가운데 보다 환경친화적이고 보다 효율적인 도시를 개발한다 목적으로 합니다.

인도의 거대한 건설 부문은 세계 3위 건설 시장이 될 것으로 예상됩니다. 스마트시티 프로젝트나 모두의 주택 등, 인도 정부가 실시하는 다양한 정책은 인도의 건설 업계에 탄력을 가져올 것으로 기대되고 있습니다.

인도 통계 및 프로그램 실시성에 따르면 건설 섹터의 GDP 점유율은 2022년 4분기에 372억 6,000만 달러에 이르렀고, 2022년 3분기 GDP 점유율은 329억 5,000만 달러를 상회했습니다.

아크릴 표면 코팅은 페인트, 직물 및 가죽 마감, 바닥 연마제, 종이 코팅 이외의 항공우주 응용 분야에서 보호 코팅으로 사용됩니다.

위의 요인과 정부의 지원은 예측 기간 동안 아크릴 표면 코팅 시장 수요 증가에 기여합니다.

아크릴 표면 코팅 산업 개요

세계의 아크릴 표면 코팅 시장은 부분적으로 세분화되어 있으며, 대기업은 업계의 단지 작은 부분을 차지하고 있습니다. 시장에서 활동하는 주요 기업으로는 Asian Paints, Berger Paints India Limited, Akzo Nobel NV, Jotun, Sika AG 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 서론

조사의 전제 조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

건축용 도료로의 용도 확대

자동차 산업에서의 용도의 급 확대

기타 촉진요인

억제요인

낮은 VOC 및 관련된 엄격한 환경 규제

기타 억제요인

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화(금액 기반 시장 규모)

용도별

수성

용제계

파우더 베이스

기타 용도

최종 사용자 산업별

건축 및 건설

주택

비주택

자동차

항공우주

기타 최종 사용자 산업

지역별

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴 및 협정

시장 점유율(%)** 및 랭킹 분석

주요 기업의 전략

기업 프로파일

3M

Akzo Nobel NV

Arkema Group

Asian Paints

BASF SE

Berger Paints India Limited

Dow

Jotun

PPG Industries Inc.

Sika AG

Solvay

The Sherwin-Williams Company

제7장 시장 기회 및 앞으로의 동향

바이오베이스 아크릴 페인트 개발

기타 기회

AJY

영문 목차

영문목차

The Acrylic Surface Coating Market size is estimated at USD 19.19 billion in 2024, and is expected to reach USD 24.64 billion by 2029, growing at a CAGR of 5.12% during the forecast period (2024-2029).

Increasing applications in architectural coatings are expected to drive the market growth. On the flip side, the slowdown in global automotive production is expected to hinder the growth of the market.

Key Highlights

The acrylic surface coating market is expected to grow during the forecast period, owing to the increasing demand from the building and construction setor.

The Asia-Pacific region dominates the global market, with the major consumption being registered in China, India, and Japan.

Acrylic Surface Coating Market Trends

Growing Demand from the Building and Construction Sector

Acrylic surface coatings are widely used in the building and construction sector because of their inertness and excellent color retention when exposed to outdoor conditions. Acrylics are available in various forms, such as emulsions (latex), lacquers, enamels, and powders.

The chief component of acrylic polymers is acrylic and methacrylic acid which provide a polymer structure with a little tendency to absorb UV light. It increases its resistance to weathering and oxidation than oil-based paints, alkyds, or epoxies, so its application increased in the buildings & construction sector.

The South African government devised a 'National Infrastructure Plan 2050' to deliver infrastructure development across energy, transport, digital communications, and water by 2050. USD 0.33 trillion will be invested through 2040 in infrastructure development.

Further, as per further statistics generated by the US Census Bureau, the annual value for new construction in the United States accounted for USD 1,657,590 million in 2022, compared to USD 1,499,822 million in 2021. Moreover, the annual value of residential construction in the United States was valued at USD 849,164 million in 2022, compared to USD 740,645 million in 2021. The country's annual non-residential construction value was USD 808,427 million in 2022, compared to USD 759,177 million in 2021. It is thereby decreasing the consumption of the market studied in the short term.

According to the Canadian Construction Association, the construction sector is one of Canada's largest employers and a major contributor to the country's economic success. The industry generates about USD 141 billion annually and contributes 7.5% of the country's Gross Domestic Product (GDP).

The building & construction industry leads in using acrylic surface coatings, with China, Germany, the United States, India, and Japan playing a major role in the market.

Asia-Pacific Region to Dominate the Market

The Asia-Pacific region is expected to dominate the market for acrylic surface coatings during the forecast period. The demand for acrylic surface coatings is increasing in countries like China, India, and Japan because of the growing building and construction sector.

The largest producers of acrylic surface coatings are located in the Asia-Pacific region. Some leading companies producing acrylic surface coatings are Asian Paints, Berger Paints India Limited, Akzo Nobel NV, Jotun, and Sika AG.

China's 14th Five-Year Plan focuses on new infrastructure projects in energy, transportation, water systems, and urbanization. According to estimates, overall investment in new infrastructure during the 14th Five-Year Plan period (2021-2025) will reach roughly CNY 27 trillion (USD 4.2 trillion).

China's urbanization rate is among the highest in the world. While China's urbanization rate reached 64.7% in 2022, this urban renewal policy aims to develop greener and more efficient cities as the government seeks to improve China's urban living conditions.

India's huge construction sector is expected to become the world's third-largest construction market. Various policies implemented by the Indian government, such as the Smart Cities project, Housing for All, etc., are expected to bring impetus to the Indian construction industry.

As per the Ministry of Statistics and Programme Implementation of India, the construction sector contributed a GDP share amounting to USD 37.26 billion in Q4 2022, higher than the GDP share of USD 32.95 billion in Q3 2022.

Acrylic surface coatings are used as protective coatings in aerospace applications other than paints, fabric and leather finishes, floor polishes, and paper coatings.

The above factors and government support contribute to the increasing demand for the acrylic surface coatings market during the forecast period.

Acrylic Surface Coating Industry Overview

The global acrylic surface coating market is partially fragmented, with the major players accounting for a marginal portion of the industry. Some major companies operating in the market are Asian Paints, Berger Paints India Limited, Akzo Nobel NV, Jotun, and Sika AG, among others (not in particular order).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Application in Architectural Coatings

4.1.2 Rapidly Growing Application in the Automotive Industry

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Stringent Environmental Regulations Related to Lower VOC

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

5.1 Application

5.1.1 Water-borne

5.1.2 Solvent-borne

5.1.3 Powder-based

5.1.4 Other Applications

5.2 End-user Industry

5.2.1 Building and Construction

5.2.1.1 Residential

5.2.1.2 Non-residential

5.2.2 Automotive

5.2.3 Aerospace

5.2.4 Other End-user Industries

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 France

5.3.3.4 Italy

5.3.3.5 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle-East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements