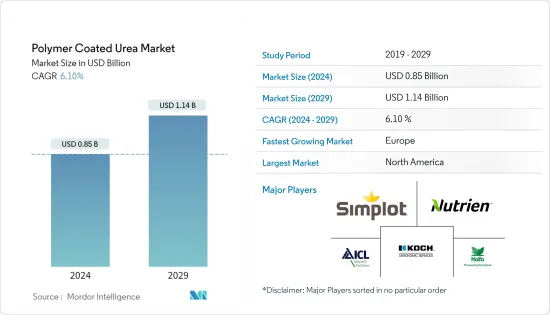

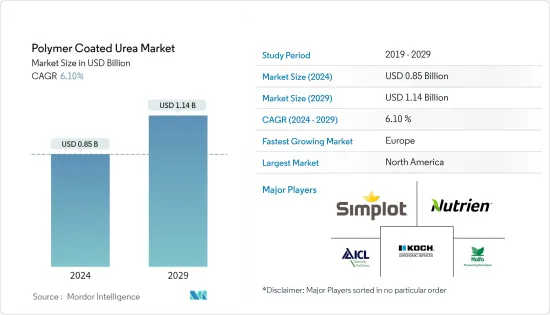

폴리머 코팅 요소 시장 규모는 2024년 8억 5,000만 달러로 추정되고, 2029년까지 11억 4,000만 달러에 이를 것으로 예측되며, 예측 기간(2024-2029년) 동안 6.10%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다.

USDA-NASS에 따르면, 2019년 기상조건이 불리했음에도 불구하고(봄에는 비가 많고 그 후 시원한 6월이 이어졌습니다), 미국의 옥수수 농가는 2019년에 옥수수의 수확 면적을 9,170 만으로 증가해 전년 대비 3% 증가했습니다. 이는 생분해성까지 있는 폴리코팅 비료 등 최첨단 비료의 채용률이 증가했기 때문입니다. 면화는 주요 상품 작물 중 하나이며, 면화 수요는 북미에서 증가하는 경향이 있으며, 면화에서는 섬유의 품질을 향상시키기 위해 시비가 중요한 역할을 수행하고 있습니다. 적절한 비료원, 적절한 시기, 적절한 장소, 적절한 비율로 4R 영양 관리에 따라 폴리코팅 비료는 면화의 영양 이용 효율을 향상시키는 것으로 주목받고 있습니다. 또한 2019년 캐나다 농업 및 농식품부(AAFC)는 국내 밀과 캐놀라 생산이 증가하고 있다고 발표했습니다. 이 주로 재배되는 작물의 생산량 증가는 국내 폴리머 코팅 요소 비료 시장에서 더욱 기대됩니다.

2018년 핀란드에서 실시한 조사에 따르면, 방출 조절 비료 또는 완효성 비료는 작물 사이클 전반에 걸쳐 질소의 가용성을 보장합니다. 또한 곡물 단백질의 함량이 낮기 때문에이 지역에서는 밀 로트가 밀링에 적합하지 않다는 것이 밝혀졌습니다. 이 문제는 생분해성 폴리머 코팅 요소 비료를 사용하여 극복할 수 있습니다. PLOS UK가 2015년에 발표한 조사논문에 따르면 방출제어형 비료 사용으로 국내 암모니아의 휘발이 51.3% 감소하여 옥수수 광합성 속도도 향상됐다고 합니다. 이는 미래에 생분해성 폴리머 코팅 요소 비료와 같은 방출 조절 비료의 사용을 촉진할 수 있습니다. 또한 사과의 생산은 재배(토양에 비료 살포 포함), 전정 및 수확과 관련된 작업에서 매우 노동 집약적입니다. 서유럽에서는 농업 노동력이 부족하고 인건비가 높아지고 있습니다. 따라서 시비 사이클의 단축으로 인한 노동력의 필요성이 줄어들기 때문에 기존의 비료를 생분해성 폴리머 코팅 요소 비료로 대체해야 합니다.

폴리머 코팅 요소 비료 시장은 통합되어 세계의 기업들이 시장을 독점하게 되었습니다. Nutrien Ltd, JRSimplot Company, Koch Agronomic Service, Haifa Group, ICL Specialty Fertilizers, DeltaChem GmbH는 시장의 주요 기업의 일부입니다. 일부 기업에서는 합병 및 인수가 주요 전략 중 하나이며 연구개발 지원, 재무 및 마케팅 지원을 위해 파트너십 전략이 채택됩니다. 예를 들어, 2018년에 Grupa Azoty는 폴란드 최대의 화학 회사인 Compo Expert를 인수했습니다. 이 인수를 통해 Groupa Azoty는 생산과 시장 개발을 확대할 계획을 세웠습니다. 생산 능력 증가는 또한 수요 증가에 대응하기 위해 비료 회사들 사이에서 발견되는 중요한 접근법 중 하나입니다. 하이파 그룹은 2016년 사바나에 CRF 생산 시설을 시작했습니다. 이 유닛은 연간 20,000톤의 멀티코트 및 코트 비료를 생산할 예정입니다.

The Polymer Coated Urea Market size is estimated at USD 0.85 billion in 2024, and is expected to reach USD 1.14 billion by 2029, growing at a CAGR of 6.10% during the forecast period (2024-2029).

According to USDA-NASS, 2019, despite the weather conditions being unfavorable (wet spring followed by cool June), the American corn farmers increased the area harvested under maize to 91.7 million in 2019, which was up by 3% from the previous year. This was owing to the increased adoption rate of cutting-edge fertilizers like poly-coated fertilizers, which are even biodegradable. The demand for cotton is on the rise in North America, as cotton is one of the major commercial crops, where fertilization plays a vital role in improving the quality of fiber. In accordance with 4R nutrient stewardship, which includes the right fertilizer source, at the right time, right place, and with right rate, poly-coated fertilizers have been noted to enhance nutrient-use efficiency in cotton. Further in 2019, Agriculture and Agri-Food Canada (AAFC) stated that wheat and canola production in the country is on the rise. This increase in the production of the majorly grown crops is further expected to the market for polymer-coated urea fertilizers in the country.

According to a research conducted in Finland in 2018, controlled release or slow-release fertilizers ensure nitrogen availability for the entire crop cycle. It was also noticed that due to low grain protein content, wheat lots were not suitable for milling in the region. This can be overcome by the application of biodegradable polymer-coated urea fertilizers. According to a research article published by PLOS UK in 2015, the use of controlled-release fertilizers has reduced ammonia volatilization by 51.3% in the country, and also enhanced the photosynthetic rate of maize. This is likely to boost the use of controlled-release fertilizers, including biodegradable polymer-coated urea fertilizers in the future. Furthermore, apple production is highly labor-intensive with operations involving growing (also includes fertilizer application to soil), pruning, and harvesting. There is a shortage of farm labor in the Western Europe region and labor costs are high. Hence, there is a need to replace conventional fertilizers with biodegradable polymer-coated urea fertilizers owing to fewer labor requirements due to reduced fertilizer application cycles.

The polymer-coated urea fertilizer market is consolidated, resulting in the dominance of the global players over the market. Nutrien Ltd, J.R.Simplot Company, Koch Agronomic Service, Haifa Group, ICL Specialty Fertilizers, and DeltaChem GmbH, are some of the major players in the market. Mergers and acquisitions are one of the prime strategies followed by some companies, along with adopted partnership strategies for R&D support, and financial and marketing support. For instance, in 2018, Grupa Azoty acquired Compo Expert, which is the largest chemical company in Poland. With this acquisition, Grupa Azoty planned to increase its production and market outreach. An increase in the production capacity is also one of the key approaches observed among the fertilizer companies to meet the growing demand. Haifa Group started its CRF production facility at Savannah in 2016. This unit is expected to produce 20,000 metric ton of Multicote and Cote fertilizer, annually.