ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

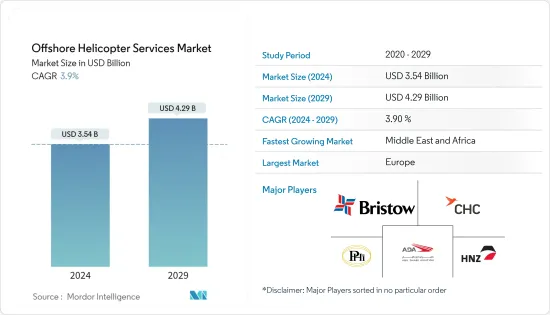

오프쇼어 헬리콥터 서비스(해양 헬리콥터 서비스, Offshore Helicopter Services) 시장 규모는 2024년 35억 4,000만 달러로 추정되며, 2029년에는 42억 9,000만 달러에 이를 것으로 예측 되고, 예측 기간 중(2024-2029년) CAGR은 3.9%로 추이하며 성장 할 것으로 예상됩니다.

시장은 2020년 COVID-19에 의해 부정적인 영향을 받았습니다. 현재 시장은 팬데믹 이전 수준에 도달했습니다.

주요 하이라이트

중기적으로 연구 대상 시장을 이끄는 주요 요인은 원유 수요 증가와 육지 및 얕은 수역에서 새로운 발견 범위가 거의 없기 때문에 심해 해양 탐사 및 개발 활동이 증가하고 있다는 점입니다. 해상 풍력 산업이 더 깊고 열악한 환경으로 이동함에 따라 풍력 터빈 유지보수 활동과 이에 따른 해상 풍력 산업을 위한 해상 헬리콥터 서비스 수요가 증가할 것으로 예상됩니다.

반면에 해상 석유 및 가스 활동의 부족과 함께 승무원 이송 선박의 낮은 일일 요금으로 인해 헬리콥터 서비스 제공업체는 일일 요금을 낮춰야 했고, 이는 연간 수익에 부정적인 영향을 미쳤습니다.

그럼에도 불구하고 최근 지중해, 가이아나, 동아프리카에서 발견되고 예정된 프로젝트는 오프쇼어 헬리콥터 서비스에 있어 비교적 새롭고 매력적인 시장이 될 것으로 예상되어 서비스 제공업체가 시장 입지를 확대할 수 있는 기회가 될 것입니다.

오프쇼어 헬리콥터 서비스 시장 동향

급성장이 기대되는 해상 풍력 발전 산업

초기의 많은 해상 풍력 발전 단지는 육지와 가까운 곳에 설치되어 배로 쉽게 접근할 수 있었습니다. 그러나 새로 건설되는 해상 풍력 발전 단지는 해안에서 멀리 떨어져 있으며, 헬리콥터는 승무원을 운송하는 데 경제적인 옵션이 되고 있습니다. 이로 인해 해상 헬리콥터 서비스를 위한 새로운 비즈니스 영역이 생겨났습니다.

해상 헬리콥터 서비스는 주로 풍력 터빈을 유지보수하기 위해 승무원을 플랫폼으로 이송하는 데 사용됩니다. 해상 풍력 터빈은 더 거칠고 부식성이 강한 환경에 직면하기 때문에 해상 풍력 발전 단지는 잦은 유지보수가 필요합니다.

해상 풍력 발전 산업이 더 깊고 열악한 환경으로 이동함에 따라 풍력 터빈 유지보수 활동과 이에 따른 해상 풍력 산업을 위한 해상 헬리콥터 서비스에 대한 수요가 증가하고 있습니다.

국제재생에너지기구에 따르면 2022년 전 세계 해상 풍력 설치 용량은 총 63,200MW였습니다. 2021년 대비 연간 성장률은 약 16.5%였습니다. 따라서 해상풍력 설치 용량이 증가함에 따라 풍력 터빈의 유지보수 활동도 지속적으로 이루어질 것으로 예상되며, 이는 곧 시장을 견인할 것입니다.

역사적으로 덴마크, 독일, 영국과 같은 유럽 국가들이 해상 풍력 발전 산업을 주도해 왔습니다. 그러나 중국, 대만, 인도와 같은 아시아 국가들도 국내 해상 풍력 부문을 개발할 계획을 발표했으며, 이는 예측 기간 동안 풍력 발전 단지용 헬리콥터 서비스 시장의 지리적 확장을 주도 할 것으로 예상됩니다.

또한 미국 에너지부에 따르면 미국에서는 여러 해상 풍력 발전 프로젝트가 다양한 개발 단계에 있습니다. 예를 들어, 2022년 9월, 바이든-해리스 행정부는 미국 정부가 새로운 부유식 해상 풍력 플랫폼을 개발하기 위한 조율된 조치를 시작한다고 발표했습니다. 이 나라는 2030년까지 30기가와트(GW)의 해상 풍력을 배치한다는 목표를 세웠으며, 이는 예측 기간 동안 해양 에너지 시장을 주도할 것으로 보입니다.

최종 사용자 산업 중 해상 풍력 산업은 예측 기간 동안 가장 빠르게 성장할 것으로 예상됩니다.

유럽이 시장을 독점

유럽은 연구 대상 지역 중 가장 큰 시장으로 추정됩니다. 이는 주로 많은 해상 석유 및 가스 플랫폼, 혹독한 해상 조건, 운송용 헬리콥터 서비스를 장려하는 엄격한 안전 규정이 있기 때문입니다.

영국(UK) 생산량의 대부분은 북해, 아일랜드해, 웨스트 셰틀랜드에 걸쳐 있는 풍부한 해양 자원 기반에서 나옵니다. 또한 영국 정부는 현지 생산량을 늘리기 위해 수백 개의 북해 석유 및 가스 탐사 면허를 추가로 발표할 것으로 예상됩니다. 이러한 발표는 영국 대륙붕(UKCS) 전역에서 향후 E&P 활동을 위한 강력한 플랫폼으로 작용하고 탐사 활동 수준을 변화시켜 연구 대상 시장의 성장에 긍정적인 영향을 미칠 것으로 예상됩니다.

노르웨이 대륙붕(NCS)에서 예상되는 회수 가능한 자원의 약 절반만이 생산되었습니다. 동시에 대륙붕에 있는 많은 시설이 예상 수명을 다하고 있습니다. 앞으로 몇 년 안에 이러한 시설 중 일부는 폐쇄되고 책임감 있게 해체될 가능성이 높으며, 이로 인해 오프쇼어 헬리콥터 서비스에 대한 수요가 발생할 수 있습니다.

또한, 2022년 1월 Var Energi와 Equinor는 북해에서 5년간 헬리콥터 공유 계약을 체결했습니다. Var Energi는 주당 12회의 북해 정기 항공편을 운항하며 평균 180명의 승객을 태우고 있습니다. 북해에서 발더 부유식 생산 장치와 링혼 플랫폼을 운영하고 있으며, 반잠수식 웨스트 피닉스(West Phoenix)는 발더 퓨처 프로젝트를 위해 추가 유정을 시추하고 있습니다. 두 회사는 헬리콥터와 비어 있는 좌석을 조정하고 공유하여 상호 가용 수송 능력의 활용도를 극대화하는 것을 목표로 하고 있습니다.

또한 2017-2025년 동안 북해 전역의 349개 유전에서 해체가 진행될 것으로 예상되며, 이 중 영국 대륙붕에 약 214개, 네덜란드 대륙붕에 106개, 노르웨이 대륙붕(NCS)에 23개, 덴마크 대륙붕에 6개 유전이 있습니다.

UKCS와 NCS에서 해양 해체 활동이 증가함에 따라 예측 기간 동안 시장 성장을 주도할 것으로 예상됩니다.

오프쇼어 헬리콥터 서비스 산업 개요

세계의 오프쇼어 헬리콥터 서비스 시장은 집중 되어 있습니다. 주요 기업으로는 CHC Group Ltd, Bristow Group Inc., PHI Inc., Abu Dhabi Aviation, HNZ Group Inc. 등이 있습니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사 범위

시장 정의

조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

소개

시장 규모 및 수요 예측(금액)(-2028년)

해양 굴착 리그의 실적 및 수요 예측(금액)(-2028년)

오프쇼어 CAPEX의 실적 및 수요 예측(금액) : 수심별(2019-2028년)

오프쇼어 CAPEX 수요 예측(금액) : 지역별(2019-2028년)

향후 주요 해외 업스트림 프로젝트

오프쇼어 지원 플릿 : 헬리콥터 유형별

최근 동향 및 전개

정부 규제 및 정책

시장 역학

성장 촉진 요인

심해 오프쇼어 탐사·개발 활동의 활성화

억제 요인

승무원 수송선과의 경쟁 격화

공급망 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

유형

소형 헬리콥터

중형·대형 헬리콥터

최종 사용자 산업

석유 및 가스 산업

해상 풍력 산업

기타 최종 사용자 산업

용도

드릴링

생산

이전 및 해체

기타 용도

지역

북미

미국

캐나다

기타 북미

아시아 태평양

중국

인도

일본

기타 아시아 태평양

유럽

독일

영국

프랑스

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

아랍에미리트(UAE)

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작 사업, 제휴, 협정

주요 기업 전략

시장 점유율 분석

기업 개요

서비스 제공업체

Bristow Group Inc.

CHC Group Ltd

HNZ Group Inc.

PHI Inc.

Abu Dhabi Aviation Airways PJSC(Abu Dhabi Aviation)

헬리콥터 제조

Airbus SE

Leonardo SpA

Textron Inc.

Lockheed Martin Corporation

제7장 시장 기회 및 향후 동향

지중해, 가이아나, 동아프리카에서 최근 발견 및 예정된 프로젝트

LYJ

영문 목차

영문목차

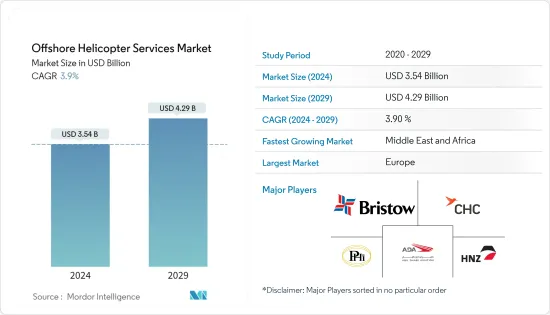

The Offshore Helicopter Services Market size is estimated at USD 3.54 billion in 2024, and is expected to reach USD 4.29 billion by 2029, growing at a CAGR of 3.9% during the forecast period (2024-2029).

The market was negatively impacted by COVID-19 in 2020. Presently the market has now reached pre-pandemic levels.

Key Highlights

Over the medium period, major factors driving the market studied are rising deepwater offshore exploration and development activities, due to the growing crude oil demand and little scope for new discovery in land and shallow water areas. As the offshore wind power industry is moving toward deeper and harsher environments, the demand for wind turbine maintenance activity and in turn, offshore helicopter services for the offshore wind industry is expected to increase.

On the other hand, the low day rates of crew transfer vessels, coupled with a lack of offshore oil and gas activities, have forced helicopter service providers to reduce their day rates, which negatively impacted their annual revenue.

Nevertheless, the recent discovery and upcoming projects in Mediterranean, Guyana, and East Africa are expected to be relatively new and attractive markets for the offshore helicopter services, creating an opportunity for service providers to expand their market presence.

Offshore Helicopter Services Market Trends

Offshore Wind Power Industry Expected to Witness Fastest Growth

Many of the earlier offshore wind farms were installed close to the land and are easily accessible by boat. However, the newly built offshore wind farms are located farther from the shore, and helicopters are becoming an economical option for transporting crew members to and from the installations. This has created new business areas for offshore helicopter services.

Offshore helicopter services are mainly used for transferring the crew to the platforms to maintain the wind turbines. As offshore wind turbines face rougher and more corrosive environments, offshore wind farms require frequent maintenance.

As the offshore wind power industry moves toward deeper and harsher environments, the demand for wind turbine maintenance activities and, in turn, offshore helicopter services for the offshore wind industry is increasing.

In 2022, according to the International Renewable Energy Agency, the total offshore wind installed capacity worldwide was 63,200 MW. The annual growth rate was approximately 16.5% compared to 2021. Thus, as the installed offshore wind capacity increases, maintenance activities for wind turbines are expected to occur continuously, which, in turn, will drive the market.

Historically, European nations like Denmark, Germany, and the United Kingdom dominated the offshore wind power industry. But Asian countries, such as China, Taiwan, and India, have also announced plans to develop the domestic offshore wind sector, which is expected to drive the geographical expansion of the helicopter services market for wind farms during the forecast period.

Furthermore, according to the US Department of Energy, several offshore wind power projects are in various stages of development in the country. For instance, in September 2022, the Biden-Harris Administration announced that the country's government was launching coordinated actions to develop new floating offshore wind platforms. The country set a target of deploying 30 gigawatts (GW) of offshore wind by 2030, which will likely drive the offshore energy market during the forecast period.

Among the end-user industries, the offshore wind industry is expected to grow fastest during the forecast period.

Europe to Dominate the Market

Europe is estimated to be the largest market among the regions for the market studied. This is mainly due to the many offshore oil and gas platforms, severe sea conditions, and strict safety regulations promoting helicopter services for transportation.

Most of the United Kingdom's (UK) production comes from the rich offshore resource base straddling the North Sea, Irish Sea, and West Shetlands. Moreover, the British government is expected to announce hundreds of additional North Sea oil and gas exploration licenses to enhance local production. These announcements are expected to act as a robust platform for future E&P activities across the United Kingdom Continental Shelf (UKCS) and help transform exploration activity levels, thus positively impacting the growth of the market studied.

Only about half of the expected recoverable resources on the Norwegian Continental Shelf (NCS) have been produced. At the same time, many of the facilities on the shelf are approaching the end of their expected lives. In the coming years, several of these facilities will likely be shut down and decommissioned responsibly, which may create a demand for offshore helicopter services.

Moreover, in January 2022, Var Energi and Equinor signed a five-year helicopter-sharing agreement in the North Sea. Var Energi operates 12 regular North Sea flights per week, carrying 180 passengers on average. In the North Sea, it operates the Balder floating production unit and the Ringhorne platform, while the semisubmersible West Phoenix drills additional wells for the Balder Future project. The two companies aim to maximize the utilization of mutually available transportation capacity by coordinating and sharing helicopters and unoccupied seats.

In addition, decommissioning is expected to take place on 349 fields across the North Sea during 2017-2025, out of which around 214 fields are in the UKCS, 106 fields in the Dutch Continental Shelf, 23 fields in the Norwegian Continental Shelf (NCS), and six fields on the Danish Continental Shelf.

The growing offshore decommissioning activities in the UKCS and NCS are expected to drive market growth during the forecast period.

Offshore Helicopter Services Industry Overview

The global offshore helicopter services market is concentrated. Some of the major companies ( not in a particular order) include CHC Group Ltd, Bristow Group Inc., PHI Inc., Abu Dhabi Aviation, and HNZ Group Inc., among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2028

4.3 Historic and Demand Forecast of Offshore Drilling Rigs in Numbers, till 2028

4.4 Historic and Demand Forecast of Offshore CAPEX in USD, by Water Depth, 2019-2028

4.5 Demand Forecast of Offshore CAPEX in USD, by Region, 2019-2028

4.6 Major Upcoming Offshore Upstream Projects

4.7 Offshore Support Fleets, by Helicopter Type

4.8 Recent Trends and Developments

4.9 Government Policies and Regulations

4.10 Market Dynamics

4.10.1 Drivers

4.10.1.1 Rising Deepwater Offshore Exploration and Development Activities

4.10.2 Restraints

4.10.2.1 Increasing Competition from Crew Transfer Vessels

4.11 Supply Chain Analysis

4.12 Porter's Five Forces Analysis

4.12.1 Bargaining Power of Suppliers

4.12.2 Bargaining Power of Consumers

4.12.3 Threat of New Entrants

4.12.4 Threat of Substitute Products and Services

4.12.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 Type

5.1.1 Light Helicopters

5.1.2 Medium and Heavy Helicopters

5.2 End-user Industry

5.2.1 Oil and Gas Industry

5.2.2 Offshore Wind Industry

5.2.3 Other End-user Industries

5.3 Application

5.3.1 Drilling

5.3.2 Production

5.3.3 Relocation and Decommissioning

5.3.4 Other Applications

5.4 Geography

5.4.1 North America

5.4.1.1 United States of America

5.4.1.2 Canada

5.4.1.3 Rest of North America

5.4.2 Asia-Pacific

5.4.2.1 China

5.4.2.2 India

5.4.2.3 Japan

5.4.2.4 Rest of Asia-Pacific

5.4.3 Europe

5.4.3.1 Germany

5.4.3.2 United Kingdom

5.4.3.3 France

5.4.3.4 Rest of the Europe

5.4.4 South America

5.4.4.1 Brazil

5.4.4.2 Argentina

5.4.4.3 Rest of the South America

5.4.5 Middle East and Africa

5.4.5.1 Saudi Arabia

5.4.5.2 United Arab Emirates

5.4.5.3 Rest of the Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Market Share Analysis

6.4 Company Profiles

6.4.1 Service Providers

6.4.1.1 Bristow Group Inc.

6.4.1.2 CHC Group Ltd

6.4.1.3 HNZ Group Inc.

6.4.1.4 PHI Inc.

6.4.1.5 Abu Dhabi Aviation Airways PJSC (Abu Dhabi Aviation)

6.4.2 Helicopter Manufacturers

6.4.2.1 Airbus SE

6.4.2.2 Leonardo SpA

6.4.2.3 Textron Inc.

6.4.2.4 Lockheed Martin Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Recent Discovery and Upcoming Projects in Mediterranean, Guyana, and East Africa