ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

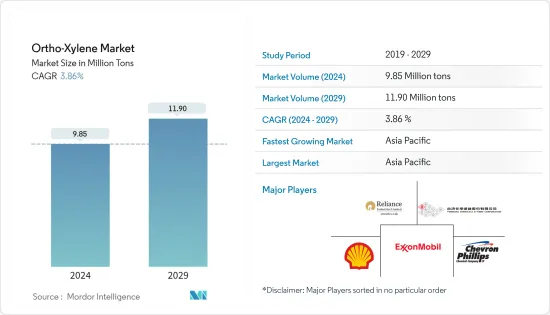

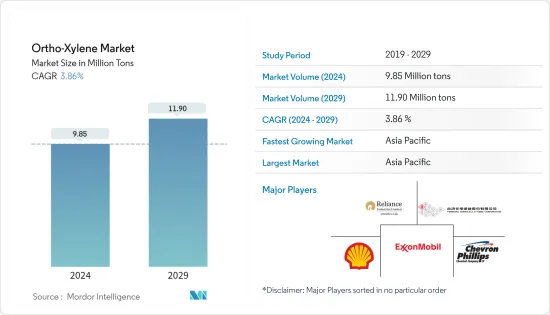

오르토크실렌(오르톡실렌)(Ortho-Xylene) 시장 규모는 2024년에 985만 톤으로 추정되고, 2029년에는 1,190만 톤에 달할 것으로 예측 되며, 예측기간(2024-2029년)의 CAGR은 3.86%로 추이하며 성장할 것으로 예측됩니다.

연구 대상 시장을 이끄는 주요 요인은 PVC 생산의 중간체로서 오르토크실렌에 대한 수요 증가와 페인트 및 접착제 생산에 오르토크실렌이 광범위하게 사용되고 있다는 점입니다.

주요 하이라이트

오르토크실렌의 해로운 신경 학적 영향과 무수 프탈산 (PA) 생산을위한 나프탈렌의 사용은 연구 된 시장의 성장을 방해 할 것으로 예상됩니다.

아시아 태평양은 세계 시장을 독점하고 중국과 인도 등 국가들이 최대 소비량을 기록했습니다.

오르소 크실렌 시장 동향

시장을 독점하는 무수 프탈산(PA)

무수 프탈산은 산업적으로 안트라퀴논 생산에 중요한 원료입니다. 또한 많은 통 염료와 알리자린 및 알리자린 유도체 제조에도 사용됩니다. 플루오레세인, 에오신 및 로다민 염료에 직접 사용됩니다.

무수 프탈산로 여러 가지 에스테르가 만들어지며 플라스틱 산업에서 가소제로 주로 사용됩니다. 또한 알키드 수지, 글리프탈 및 레질 수지, 디옥틸 프탈레이트, 폴리비닐 수지를 제조하는 데도 사용됩니다.

무수 프탈산에 대한 수요가 계속 증가함에 따라 대체 원료에 대한 탐색이 활발해졌습니다. 석유 정제소에서 대량으로 생산되는 오르토크실렌이 가장 적합한 것으로 나타났습니다.

O-자일렌은 무수 프탈산 생산의 원료로서 몇 가지 장점이 있습니다. O-자일렌의 산화는 O-자일렌의 액체 상태로 인해 나프탈렌의 산화보다 더 간단한 공급 시스템을 허용합니다.

이론적으로 O-자일렌 산화에 필요한 공기의 양은 나프탈렌 산화에 필요한 양의 3분의 2에 불과합니다. 반응 중에 방출되는 열은 나프탈렌보다 121kcal 적습니다. 생성물의 순도가 더 높고 이론적 수율도 나프탈렌보다 높습니다. 또한, 오자일렌은 상온에서 액체이기 때문에 공급 시스템이 더 간단합니다.

따라서 무수 프탈산에 대한 수요가 증가함에 따라 예측 기간 동안 O-자일렌의 소비가 증가 할 것으로 예상됩니다.

아시아 태평양이 시장을 독점

아시아 태평양에서는 중국이 GDP에서 가장 큰 경제 강국입니다. 오르토크실렌의 주요 비율은 프탈산계 PVC 가소제의 제조에 사용되는 무수 프탈산의 제조에 사용됩니다. 중국은 가소제의 유일한 최대 시장이며 세계 소비량의 40% 이상을 차지합니다.

PVC는 자동차 산업에서 널리 사용됩니다. PVC의 열가소성 특성은 금속에 비해 무게가 가볍습니다. 또한 다른 제조 방법에 비해 저렴한 비용입니다. 외부 부품 및 자동차 내부 부품에 이상적입니다. PVC는 가볍고 내구성이 있으며 성형이 용이하며 외관이 매력적이며 외장 부품에 선호됩니다.

대체 재료 대신 PVC를 사용하면 전체 부품 비용을 20-60% 낮출 수 있습니다. PVC로 만든 자동차 부품에는 계기판, 바닥 커버, 머드 플랩, 씰, 선바이저, 석해 방지 등이 있습니다.

중국은 2009년 이래 세계 최대의 자동차 제조업체이며 현재의 생산 점유율은 약 29.06%입니다.

내수 감소와 자동차 제조업체의 다른 국가로의 침투로 2018년 생산량은 4.2% 감소했습니다. 수요는 여전히 증가하고 있기 때문에 감소는 일시적인 것으로 예상됩니다.

그 때문에 전술한 요인으로부터 무수 프탈산의 소비량은 많습니다. 이로 인해 예측 기간 동안 오르토크실렌 수요가 증가 할 수 있습니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 성과

조사의 전제

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진 요인

PVC 제조의 중간체로서 수요 증가

도료 및 접착제 산업에 있어서 오르토크실렌의 광범위한 사용

억제 요인

오르토크실렌의 신경학적 악영향

무수 프탈산(PA) 제조에 있어서 나프탈렌의 사용

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화

용도

무수 프탈산

살균제

대두 제초제

윤활유 첨가제

기타 용도

지역

아시아 태평양

중국

인도

일본

한국

기타 아시아 태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카공화국

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작 사업, 제휴, 협정

시장 점유율 분석

주요 기업 전략

기업 개요

China Petroleum&Chemical Corporation

Exxon Mobil Corporation

Flint Hills Resources

Formosa Chemicals and Fibre Corporation

KP Chemical Corp.

Nouri Petrochemical Company

Reliance industries Ltd

Royal Dutch Shell PLC

SK Global Chemical Co. Ltd

제7장 시장 기회 및 향후 동향

LYJ

영문 목차

영문목차

The Ortho-Xylene Market size is estimated at 9.85 Million tons in 2024, and is expected to reach 11.90 Million tons by 2029, growing at a CAGR of 3.86% during the forecast period (2024-2029).

The major factors driving the market studied are the increasing demand for ortho-xylene as an intermediate for PVC production, and extensive usage of ortho-xylene in the production of paints and adhesive.

Key Highlights

Detrimental neurological effects of ortho-xylene and usage of naphthalene for the production of phthalic anhydride (PA) areexpected to hinder the growth of the market studied.

Asia-Pacific dominated the global market, with the largest consumption recorded from the countries, such as China and India.

Ortho-Xylene Market Trends

Phthalic Anhydride (PA) to Dominate the Market

Phthalic anhydride is industrially an important raw material for the production of anthraquinone. Itis also used in the manufacture of many vat dyes, as well as in alizarin and alizarin derivatives. It is used directly for the fluorescein, eosin, and rhodamine dyes.

Several esters are made from phthalic anhydride, and are largely used in the plastics industry, as plasticizers. It is also used to manufacture alkyd resins, the glyptal and rezyl resins, dioctyl phthalate, and the poly-vinyl resins.

The ever-increasing demand for phthalic anhydride has stimulated a search for alternative raw materials. Ortho-xylene, which is available in abundant quantities from the petroleum refineries, appears to be the most suitable.

O-xylene has several advantages as a raw material for the production of phthalic anhydride. The oxidation of o-xylene permits a simpler feed system than that of the oxidation of naphthalene, due tothe liquid state of o-xylene.

The theoretical amount of air required for oxidizing o-xylene is only two-thirdof the amount required for the oxidation of naphthalene. The heat emitted off during the reaction is 121 kcal less than that of naphthalene. The product is of higher purity, and the theoretical yield percentage is higher than that of naphthalene. Furthermore, as o-xylene is a liquid at ordinary temperature, its use permits a simpler feed system.

Thus, with increasing demand for phthalic anhydrade, the consumption of o-xylene is likely to increase during the forecast period.

Asia-Pacific to Dominate the Market

In the Asia-Pacific region, China is the largest economy in terms of GDP. The major proportion of ortho-xylene is used in the manufacture of phthalic anhydride that is used in the production of phthalate-based PVC plasticizers. China is the single largest market for plasticizers, with more than 40% of the global consumption. Some of the manufacturers of PVC in the country are Shin-Etsu Chemical Co. Limited, Xinjiang Zhongtai Chemical Co. Ltd, Lubrizol, Hanwha Chemical, Formosa Plastics, etc.

PVC is widely used in the automotive industry. PVC's thermoplastic properties have lesser weight compared to metals. It has a lower cost of manufacturing methods compared to the cost of other methods. It is an ideal choice for exterior and automotive interior parts. PVC is favored for exterior parts, owing to its light weight, durability, easily shapeable quality, and attractive appearance.

The overall cost of a component can be brought down to 20-60%, by using PVC instead of alternative materials. Some of the automotive components made with PVC include instrument panels, floor coverings, mud flaps, seals, sun visors, and anti-stone damage protection.

China is by far the largest automotive manufacturer in the world, since 2009, with a current share of production of about 29.06%.

The production decreased by 4.2% in 2018, owing to the decrease in domestic demand and penetration of automotive manufacturers to other countries. The decline is expected to be temporary, as the demand is still increasing.

Therefore, owing to the aforementioned factors, the consumption of phthalic anhydride is high. This may lead to an increase in demand for ortho-xylene, during the forecast period.

Ortho-Xylene Industry Overview

The ortho-xylene market is fragmented in nature. The major companies includeRoyal Dutch Shell PLC,Reliance Industries Limited,China Petroleum & Chemical Corporation, andExxon Mobil Corporation, and Formosa Chemicals & Fibre Corp.among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Deliverables

1.2 Study Assumptions

1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Demand as an Intermediate for PVC Production

4.1.2 Extensive Usage of Ortho-xylene in Paints and Adhesive Industries

4.2 Restraints

4.2.1 Detrimental Neurological Effects of Ortho-xylene

4.2.2 Usage of Naphthalene for the Production of Phthalic Anhydride (PA)

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION

5.1 Application

5.1.1 Phthalic Anhydride

5.1.2 Bactericides

5.1.3 Soybean Herbicides

5.1.4 Lube Oil Additives

5.1.5 Other Applications

5.2 Geography

5.2.1 Asia-Pacific

5.2.1.1 China

5.2.1.2 India

5.2.1.3 Japan

5.2.1.4 South Korea

5.2.1.5 Rest of Asia-Pacific

5.2.2 North America

5.2.2.1 United States

5.2.2.2 Canada

5.2.2.3 Mexico

5.2.3 Europe

5.2.3.1 Germany

5.2.3.2 United Kingdom

5.2.3.3 Italy

5.2.3.4 France

5.2.3.5 Rest of Europe

5.2.4 South America

5.2.4.1 Brazil

5.2.4.2 Argentina

5.2.4.3 Rest of South America

5.2.5 Middle East & Africa

5.2.5.1 Saudi Arabia

5.2.5.2 South Africa

5.2.5.3 Rest of Middle East & Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements