ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

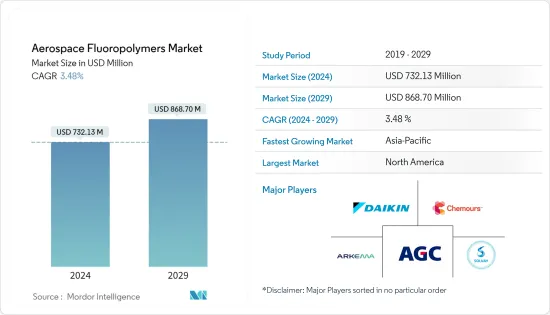

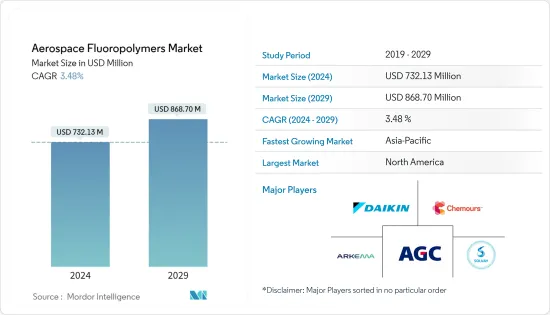

항공우주용 불소수지 시장 규모는 2024년에 7억 3,213만 달러로 추정되며, 2029년에는 8억 6,870만 달러에 이를 것으로 예측되며, 예측기간(2024-2029년)의 CAGR은 3.48%로 성장할 전망입니다.

주요 하이라이트

2020년 COVID-19 팬데믹기간에 발생한 공급망 혼란과 항공기 수주 잔여는 우주 항공 불소 수지 시장에 큰 영향을 미쳤습니다. 주요 불소수지 제조업체(OEM)는 최종사용자 수요가 줄어들어 생산량을 줄일 수밖에 없었고, 수익원이 줄어들어 소규모 시장기업에 있어서는 지속가능성 문제가 떠올랐습니다. 그러나 COVID 이후는 항공 섹터의 회복으로 수요가 급증하고 항공우주 용도에서 불소 수지의 사용 증가가 예상되기 때문에 앞으로도 견조하게 추이할 것으로 보입니다.

불소수지는 항공기와 같은 최종 사용자 플랫폼을 보다 안전하고 연비가 좋게 하는 독특한 특성을 가지고 있기 때문에 항공우주 산업에서 높은 수요가 있습니다. 높은 내구성과 열, 특수 연료, 습도 및 엔진 진동에 대한 효과적인 보호는 항공우주 및 항공우주 부품 제조업체의 눈길을 끄는 불소 수지의 특성의 일부입니다. 또, 불소수지가 다른 재료에 비해 경량인 것도, 항공우주 분야에서 불소수지의 채용이 진행되고 있는 이유입니다. 그러나 일부 불소 수지는 비용이 많이 들고 시장 성장을 방해할 수 있습니다.

항공우주용 불소수지 시장 동향

예측기간 동안 민간항공부가 시장을 선도할 전망

앞으로 몇 년동안 민간 항공 플랫폼이 시장을 선도할 것으로 예상됩니다. 2020년에는 COVID-19 팬데믹에 의해 민간 항공기의 납품이 감소했습니다. 그러나 2021년에는 항공기 납품이 개선되었으며 Airbus와 Boeing 등 주요 민간 항공기 OEM은 항공기 생산과 납품률을 향상시켰습니다. 여행 제한이 해제됨에 따라 항공 여객 수송량이 개선되기 시작했습니다.

항공 여객 수가 증가함에 따라 항공사는 모든 주요 노선에서 운항을 시작했으며 새로운 노선도 추가했습니다. 유나이티드 항공은 신노선 취항을 발표하고 "최대 규모의 대서양 횡단 노선 확대"라고 표현했습니다. 모든 것이 평상시로 돌아와 새로운 항공사도 운항을 시작했습니다. 인도의 새로운 항공사 Akasa Air은 2022년 8월에 운항을 시작하여 주 28편의 1노선에서 출발하여 점차 2노선을 추가했습니다.

2022년 10월, 알래스카 항공은 Boeing B737 MAX를 52대 주문하고 장비 확대를 계획하고 있습니다. 이 항공은 2023년 말까지 전기 보잉제 메인라인 장비를 도입할 계획을 발표했습니다. 민간항공기의 증산에 따라 불소수지 수요도 증가하여 시장의 성장이 예상됩니다.

예측기간 중 가장 높은 CAGR로 추이하는 것은 아시아태평양

아시아태평양은 불소 수지 시장 평가 기간 동안 현저한 성장을 이룰 것으로 예상됩니다. 아시아태평양은 수년간 항공 산업의 중요한 기지가 되었습니다. 인도나 중국 등 이 지역의 신흥국들은 항공 수요가 증가함에 따라 각각의 민간항공시장에서 큰 진전을 경험하고 있습니다. 중국은 큰 내수로 세계 민간 항공 시장의 회복을 이끌고 있으며 항공사의 재정 회복에 기여하고 있습니다.

Boeing에 따르면 중국은 국내 항공 여객 수송량 증가로 항공 업계 최대 시장이 되고 있으며, 북미을 웃돌아 2040년까지 4.4%의 급성장이 전망되고 있습니다. 인근 국가 간의 긴장으로 인한 역내 국가의 군사비 증가와 호주와 같은 국가에 군사 기지국을 배치하기 위해 투자하는 외국과 함께 아시아태평양의 군사 항공도 증가하고 있습니다.

중국은 군사항공 능력을 높이고 있으며, 2022년 10월에는 세계 최초의 쌍좌 스텔스 전투기인 J-20의 신형 스텔스 전투기가 발표되었습니다. 또한 아시아태평양 국가들은 인건비가 싸기 때문에 비용면에서 뛰어나 제조 능력을 갖추기 위한 투자도 적어집니다. 이처럼 아시아태평양에서는 항공우주산업이 급속히 발전하고 있기 때문에 항공우주용 불소수지 시장은 앞으로도 계속 성장할 것으로 보입니다.

항공우주용 불소수지산업 개요

항공우주용 불소 수지 시장은 원래 통합형입니다. Daikin Industries, The Chemours Company, AGC Group, Arkema SA, Solvay SA는 이 시장에서 유력한 기업입니다. 이러한 선도 기업은 M&A, 신제품 출시, 사업 확대, 계약, 합작 투자, 파트너십 등 다양한 유기적·무기적 성장 전략을 채택하여 이 시장에서의 입지를 강화하고 있습니다.

그러나 항공우주용 불소수지 시장에서 기능하는 중소기업도 몇 가지 존재하고 있습니다. 각 회사는 고객 기반을 늘리기 위해 모든 지역에서 존재감을 높이려고합니다. 예를 들어, 2021년 3월, Arkema는 상숙(중국)의 불소수지 생산능력을 추가로 35% 증강하기 위해 투자를 늘릴 것이라고 발표했습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

시장 개요

시장 성장 촉진요인

시장 성장 억제요인

Porter's Five Forces 분석

신규 참가업체의 위협

구매자·소비자의 협상력

공급기업의 협상력

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

플랫폼

민간항공

일반항공

군용기

수지 유형

PTFE

ETFE

PFA

FKM

기타 수지 유형

유형

파우더

펠렛

분산액

성분 유형

씰

와이어 및 케이블

호스 및 튜브

필름

코팅

기타 부품

지역

북미

미국

캐나다

유럽

영국

독일

프랑스

러시아

기타 유럽

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

라틴아메리카

브라질

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

아랍에미리트(UAE)

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

기업 프로파일

Daikin Industries, Ltd.

The Chemours Company

AGC Group

Arkema SA

Solvay SA

Fluorotherm

Plastics Europe

Dongyue Group

The 3M Company

HaloPolymer, OJSC

Saint-Gobain Group

제7장 시장 기회와 앞으로의 동향

JHS

영문 목차

영문목차

The Aerospace Fluoropolymers Market size is estimated at USD 732.13 million in 2024, and is expected to reach USD 868.70 million by 2029, growing at a CAGR of 3.48% during the forecast period (2024-2029).

Key Highlights

The supply chain disruption and aircraft order backlogs caused during the COVID-19 pandemic in 2020 greatly affected the aerospace fluoropolymers market. Major fluoropolymer original equipment manufacturers (OEMs) had to reduce their production rate due to less demand from the end-users, leading to trickling revenue streams and raising sustainability issues for small market players. However, post-COVID, the demand witnessed rapid growth due to the recovery demonstrated by the aviation sector and was likely to remain robust as the use of fluoropolymers is expected to increase in aerospace applications.

Fluoropolymers have been witnessing high demand from the aerospace industry due to their unique properties that make end-user platforms such as aircraft safer and more fuel-efficient. High durability and effective protection against heat, specialty fuels, humidity, and engine vibrations, are a few of those characteristics of fluoropolymers that are catching the eyes of aerospace and aerospace component manufacturers. In addition, the lightweight nature of fluoropolymers in comparison to other materials is another reason leading to the greater adoption of fluoropolymers in aerospace. However, the costs of some of the fluoropolymer resins are at the higher end, which can act as a hindrance to market growth.

Aerospace Fluoropolymers Market Trends

Commercial Aviation Segment is Expected to Lead the Market During the Forecast Period

The commercial aviation platform is expected to lead the market in the years to come. In 2020, there was a decline in commercial aircraft deliveries due to the COVID-19 pandemic. However, aircraft deliveries improved in 2021, and the major commercial aircraft OEMs, like Airbus and Boeing, increased their aircraft production and delivery rates. With the lifting of travel restrictions, air passenger traffic started to improve.

With the increase in air passenger traffic, airlines have started operating on all major routes and have also added new routes. United Airlines has announced that it has started operating on new routes, describing it as its "largest transatlantic expansion." With everything returning to normal, new airlines have started operations. Akasa Air, a new Indian airline, started its operations in August 2022, starting with one route with 28 flights a week and gradually adding two more routes.

In October 2022, Alaska Airlines placed an order for 52 Boeing B737 MAX aircraft with a plan to expand its fleet. The airline announced plans to have an all-Boeing mainline fleet by the end of 2023. With the increase in the production of commercial aircraft, the demand for fluoropolymers will also increase, resulting in the growth of the market.

Asia Pacific to Register the Highest CAGR During the Forecast Period

Asia-Pacific is anticipated to witness tremendous growth over the assessment period in the fluoropolymers market. Asia-Pacific has become a significant hub for the aviation industry over the years. The emerging economies in the region, like India and China, are experiencing a massive surge in their respective commercial aviation markets due to an increased demand for air travel. China is leading the recovery of global commercial aviation due to great domestic demand, helping the airlines witness financial recovery.

China is the largest market in aviation due to an increase in domestic air passenger traffic, which has surpassed the North American region and is expected to grow rapidly at a rate of 4.4% by 2040, according to Boeing. With the increase in military spending of the countries in the region due to tensions between neighboring countries and with foreign nations investing in arranging military base stations in countries like Australia, military aviation in the Asia-Pacific region is also increasing.

China is increasing its military airborne capabilities, and a new stealth fighter aircraft, the new version of the J-20, which is the world's first twin-seat stealth fighter aircraft, was unveiled in October 2022. In addition, countries in the Asia-Pacific are cost-friendly due to the low cost of labor and require low investments to set up manufacturing capabilities. Thus, due to the rapidization of the aerospace industry in Asia Pacific, the aerospace fluoropolymers market will continue to experience growth in the region.

Aerospace Fluoropolymers Industry Overview

The aerospace fluoropolymers market is consolidated in nature. Daikin Industries, Ltd., The Chemours Company, AGC Group, Arkema S.A., and Solvay S.A. are the prominent players in the market. These major players have adopted various organic as well as inorganic growth strategies such as mergers & acquisitions, new product launches, expansions, agreements, joint ventures, partnerships, and others to strengthen their position in this market.

However, there are several smaller players that function in the aerospace fluoropolymers market. The companies are trying to increase their presence across all regions to increase their customer base. For example, in March 2021, Arkema announced to increase its investment to further increase its fluoropolymer production capacities in Changshu (China) by 35%.