ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

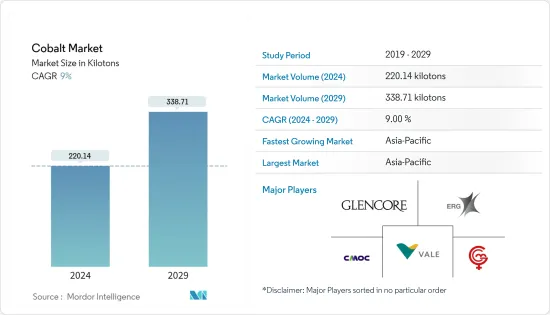

코발트 시장 규모는 2024년에 220.14킬로톤으로 추계되어 2029년까지는 338.71킬로톤에 이를 것으로 예측되며, 예측기간(2024-2029년)의 CAGR은 9%로 성장할 전망입니다.

자동차, 일렉트로닉스, 석유 및 가스 산업에 영향을 미치는 세계의 억제요인으로 인해 COVID-19 팬데믹은 코발트와 다양한 시장에 큰 영향을 미쳤습니다. 그러나 최종 사용자 산업의 성장으로 유행 후 코발트 시장은 크게 회복되었습니다.

충전식 배터리 제조에서 광범위한 사용은 시장 조사를 추진하는 주요 요인입니다. 또한 고속 절삭 공구의 생산에 있어서의 사용량 증가도 시장을 전진시킬 것으로 예상됩니다.

그러나 코발트의 희소성과 광상에서 코발트를 추출하는 데 필요한 집중적인 정제 공정으로 인한 고비용은 시장 성장을 방해할 가능성이 높습니다.

또한, 환경 친화적 인 재활용 가능한 코발트의 상업화는 코발트 시장의 미래 성장에 기회를 제공하는 것으로 보입니다.

아시아태평양이 가장 높은 시장 점유율을 차지하고 있으며 예측 기간 동안에도 시장을 독점할 것으로 예상됩니다.

코발트 시장 동향

시장을 독점하는 이차 전지 부문

코발트는 다양한 용도로 널리 사용되지만 가장 일반적인 것은 이차 전지입니다. 코발트의 리튬 이온 이차 전지(LIB)에의 응용은 잘 알려진 LiCoO2(LCO) 양극으로 거슬러 올라갈 수 있습니다.

코발트는 리튬 이온 배터리에 필요한 성분입니다. 코발트는 양극의 과열을 방지하고 배터리 수명을 줄입니다. 그 결과, 코발트는 배터리 수명 연장에 큰 역할을 하고 있으며, 휴대폰 및 기타 배터리 구동 장치에 사용되는 충전식 배터리의 대부분에 포함되어 있습니다.

가솔린차와 디젤차에 대한 규제 강화의 결과, 전기차 시장은 큰 성장을 이루었습니다. EV의 대수에 따르면 2022년에는 1,050만대의 배터리 전기자동차(BEV)와 플러그인 하이브리드 전기자동차(PHEV)가 새롭게 납품되어 2021년 대비 55% 증가했습니다.

전 세계적으로 스마트폰 수요가 크게 증가하고 있습니다. Telefonaktiebolaget LM Ericsson에 따르면 스마트폰 계약 수는 전년 59억 2,400만 대에 비해 2021년 전 세계 62억 5,900만 대에 이릅니다. 게다가 이 계약수는 2027년에는 76억 9,000만에 이를 전망이며, 스마트폰 분야에서의 코발트 이용이 촉진됩니다.

북미, 특히 미국에서는 전자 산업이 완만한 성장을 기대합니다. 미국에서는 일렉트로닉스 산업의 기술 진보와 연구 개발 활동이라는 점에서 기술 혁신의 속도가 빠르기 때문에 보다 새롭고 빠른 일렉트로닉스 제품에 대한 수요가 높아지고 있습니다. 소비자 기술 협회에 따르면 미국의 소비자 전자 제품 또는 기술 판매를 통한 소매 수입은 2021년 4,610억 달러에 비해 2022년 5,050억 달러에 달할 것으로 추정됩니다.

경제분석국에 따르면 2022년 3분기 미국의 전기제품, 기기, 부품 제조에 따른 부가가치는 약 738억 달러로 전년 동기 대비 8% 증가했습니다. 1-3분기 동안 이 나라의 부가가치 총액은 2,200억 달러에 달했습니다.

또한 미국의 컴퓨터 및 전자 제품 제조업의 총 생산량은 2022년 1-3분기에 약 1조 3,000억 달러였습니다. 전년 동기(1조 2,000억 달러)와 비교하면 이 기간은 7% 성장을 보였습니다.

이러한 전기자동차의 대수 증가와 신흥국의 전자기기 사용 증가로 이차전지 수요가 높아지고 있어 향후 수년간 코발트 시장을 견인할 가능성이 있습니다.

아시아태평양이 시장을 독점

중국, 인도, 일본, 한국에서는 전자, 자동차, 세라믹, 안료, 유리 산업이 고도로 발전하고 있으며, 전지 기술 분야의 발전을 위해 장기간 투자가 계속되고 있기 때문에 아시아태평양 는 세계의 코발트 시장을 독점할 것으로 예측됩니다.

중국과 인도에서는 내연 엔진의 사용 금지와 내연차에 대한 높은 세금으로 지난 몇 년동안 전기 자동차와 하이브리드 자동차의 생산이 가속화되었습니다.

중국은 전기자동차의 생산국으로도 소비국으로도 가장 높아 세계 시장의 약 절반을 차지하고 있습니다. 중국기차공업협회(CAAM)에 따르면 2022년 중국의 신에너지차의 총 생산대수는 약 700만대로 추정되고 있습니다. 2021년의 생산 대수(354만대)와 비교하면, 97% 가까운 대폭 증가가 됩니다.

인도는 최근 몇 년간 일본의 전기 자동차 시장에 주목하고 있습니다. CEEW Centre for Energy Finance의 조사에 따르면 인도에서는 2030년까지 전기차에 2,060억 달러의 비즈니스 기회가 있다고 인식되고 있으며, 이를 위해 국내 자동차 제조 및 충전 인프라에 1,800억 달러의 투자가 필요합니다.

인도 브랜드 에퀴티 재단(IBEF)은 인도의 전자기기 제조업은 2025년까지 5,200억 달러 규모에 이를 것으로 예측했습니다. Make in India, National Policy of Electronics, Net Zero Imports in Electronics, Zero Defect, Zero Effect 등의 정책에 의한 정부의 이니셔티브는 국내 제조업의 성장, 수입 의존도의 저하, 수출과 제조업의 활성화에 약속을 제공하고 인도에서 전기 및 전자 제품의 급속한 성장을 가속할 것으로 예상됩니다.

전자정보기술산업협회(JEITA)는 2022년 11월까지 일본의 일렉트로닉스 산업 전체의 생산액이 10조 1,000억엔(845억 달러)을 넘어 전년 대비 약 100.7%가 될 것으로 추산하고 있습니다.

에너지 절약 장치의 지속적인 성장과 이 지역의 고효율 배터리에 대한 필요성 증가는 향후 몇 년동안 코발트 시장을 이끌 것으로 예상됩니다.

코발트 산업 개요

코발트 시장은 소수의 기업이 시장 점유율의 대부분을 차지하고 부분적으로 통합되어 있습니다. 시장의 주요 기업(순부동)에는 Glencore, Vale, Eurasian Resources Group, Gecamines SA, CMOC 등이 있습니다.

기타 혜택:

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트·지원

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

2차 전지 제조에 있어서의 폭넓은 용도

고속 절삭 공구의 생산에 있어서의 사용량 증가

억제요인

광상으로부터의 추출에 필요한 방대한 정제 공정

기타 억제요인

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

가격 동향

제5장 시장 세분화(시장 규모 : 수량 기준)

형태

화합물

금속

구입 스크랩

용도

배터리

합금

촉매

공구 재료

자석

세라믹과 안료

기타 용도

지역

생산 분석

호주

캐나다

중국

콩고

쿠바

인도

인도네시아

마다가스카르

모로코

파푸아뉴기니

필리핀

러시아

미국

세계 기타 지역

소비 분석

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

기타 유럽

세계 기타 지역

남미

중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

시장 점유율(%)/랭킹 분석

주요 기업의 전략

기업 프로파일

BHP

CMOC

Cobalt Blue Holdings Limited

Eramet

Eurasian Resources Group

Gecamines SA

Glencore

Huayou Cobalt Co., Ltd.

Jervois

Jinchuan Group International Resources Co. Ltd

Panoramic Resources

Sherritt International Corporation

Umicore NV

Vale

Wheaton Precious Metals Corp

제7장 시장 기회와 앞으로의 동향

환경 친화적 인 재활용 가능한 코발트의 상업화

JHS

영문 목차

영문목차

The Cobalt Market size is estimated at 220.14 kilotons in 2024, and is expected to reach 338.71 kilotons by 2029, growing at a CAGR of 9% during the forecast period (2024-2029).

Because of global constraints affecting the automobile, electronics, and oil and gas industries, the COVID-19 pandemic had a substantial impact on the market for cobalt and its different types. However, the cobalt market recovered significantly in the post-pandemic era, owing to the growing end-user industries.

The extensive use in the manufacturing of rechargeable batteries is a major factor driving market research. Rising usage in the production of high-speed cutting tools is also expected to drive the market forward.

However, the high cost of cobalt due to its scarcity and the intensive refining process required to extract it from ore deposits is likely to hamper market growth.

Additionally, the commercialization of environmentally friendly recyclable cobalt will likely provide opportunities for the future growth of the cobalt market.

The Asia-Pacific region accounts for the highest market share and is expected to dominate the market during the forecast period.

Cobalt Market Trends

Rechargeable Batteries Segment to Dominate the Market

Cobalt is widely employed in a variety of applications, although it is most commonly found in rechargeable batteries. Cobalt's application in lithium-ion batteries (LIBs) may be traced back to the well-known LiCoO2 (LCO) cathode, which provides good conductivity and structural stability during charge cycling.

Cobalt is a necessary component in lithium-ion batteries. It prevents cathodes from overheating, which can shorten the battery's life. As a result, cobalt plays a major role in battery life extension and is found in practically every rechargeable battery used in a mobile phone or other battery-powered devices.

The electric vehicle market has experienced significant growth as a result of increased regulation on gasoline and diesel-powered automobiles. According to EV volumes, 10.5 million new battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs) were delivered in 2022, representing a 55% increase over 2021.

Globally, the demand for smartphones is increasing at a significant rate. According to Telefonaktiebolaget LM Ericsson, the number of smartphone subscriptions accounted for 6,259 million in 2021 globally, compared to 5,924 million in the prior year. Moreover, the subscription is likely to reach 7,690 million by 2027, enhancing the usage of cobalt in the smartphone segment.

In North America, especially in the United States, the electronics industry is expected to grow at a moderate rate. In the United States, the rapid pace of innovation in terms of the advancement of technologies and R&D activities in the electronics industry is driving the demand for newer and faster electronic products. According to the Consumer Technology Association, the retail revenue from consumer electronics or technology sales in the United States was estimated at USD 505 billion in 2022, compared to USD 461 billion in 2021.

According to the Bureau of Economic Analysis, the value added by the manufacturing of electrical appliances, equipment, and components in the United States in the third quarter of 2022 was around USD 73.8 billion, representing an 8% rise over the same period the previous year. Throughout the first three quarters, the country's total value added was close to USD 220 billion.

Furthermore, the gross output of computer and electronic products manufacturing in the United States was approximately USD 1,300 billion in the first three quarters of 2022. When compared to the same period the previous year (USD 1,200 billion), this period showed a 7% growth.

These rising numbers of electric vehicles and the increasing usage of electronic equipment in developing countries are driving the demand for rechargeable batteries, which may drive the market for cobalt through the coming years.

Asia-Pacific Region to Dominate the Market

Due to the highly developed electronics, automotive, ceramics and pigments, and glass industries in China, India, Japan, and Korea, as well as the region's ongoing investments made to advance the battery technology sector over time, the Asia-Pacific region is predicted to dominate the global cobalt market.

Internal combustion engine bans and high taxes on internal combustion vehicles in China and India have accelerated the production of electric and hybrid vehicles during the past few years in both countries.

China has been the highest producer as well as consumer of electric vehicles, covering approximately half the market all around the globe. According to the China Association of Automobile Manufacturers (CAAM), the total production of new energy vehicles in China in 2022 was estimated to be about 7 million units. This saw a whopping increase of close to 97% when compared with the production of vehicles in 2021 (3.54 million units).

India has also been focusing on the electric vehicle market for the country for the past few years. A study by the CEEW Centre for Energy Finance recognized a USD 206 billion opportunity for electric vehicles in India by 2030, which will necessitate a USD 180 billion investment in vehicle manufacturing and charging infrastructure in the country.

The India Brand Equity Foundation (IBEF) predicts that the Indian electronics manufacturing industry will be worth USD 520 billion by 2025. Government initiatives with policies such as Make in India, National Policy of Electronics, Net Zero Imports in Electronics, and Zero Defect, Zero Effect, which offer a commitment to growth in domestic manufacturing, lowering import dependence and energizing exports and manufacturing, are expected to drive rapid growth in electrical and electronic products in India.

The Japan Electronics and Information Technology Industries Association (JEITA) estimated that the whole production value of Japan's electronics sector was over JPY 10.1 trillion (USD 84.5 billion) by November 2022, which is around 100.7% of the previous year's figure.

Continuous growth in energy-saving devices along with the increasing need for high-efficiency batteries in the region are expected to drive the market for cobalt through the coming years.

Cobalt Industry Overview

The cobalt market is partially consolidated in nature with a few players holding the majority of the market share. Some of the market's major players (not in any particular order) include Glencore, Vale, Eurasian Resources Group, Gecamines SA and CMOC, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Extensive Usage in the Manufacturing of Rechargeable Batteries

4.1.2 Rising Usage in the Production of High Speed Cutting Tools

4.2 Restraints

4.2.1 Intensive Refining Process Required to Extract From Ore Deposits

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

4.5 Price Trends

5 MARKET SEGMENTATION (Market Size in Volume)

5.1 Form

5.1.1 Chemical Compound

5.1.2 Metal

5.1.3 Purchased Scrap

5.2 Application

5.2.1 Batteries

5.2.2 Alloys

5.2.3 Catalysts

5.2.4 Tool Materials

5.2.5 Magnets

5.2.6 Ceramics and Pigments

5.2.7 Other Applications

5.3 Geography

5.3.1 Production Analysis

5.3.1.1 Australia

5.3.1.2 Canada

5.3.1.3 China

5.3.1.4 Congo

5.3.1.5 Cuba

5.3.1.6 India

5.3.1.7 Indonesia

5.3.1.8 Madagascar

5.3.1.9 Morocco

5.3.1.10 Papua New Guinea

5.3.1.11 Philipppines

5.3.1.12 Russia

5.3.1.13 United States

5.3.1.14 Rest of the World

5.3.2 Consumption Analysis

5.3.2.1 Asia-Pacific

5.3.2.1.1 China

5.3.2.1.2 India

5.3.2.1.3 Japan

5.3.2.1.4 South Korea

5.3.2.1.5 Rest of Asia-Pacific

5.3.2.2 North America

5.3.2.2.1 United States

5.3.2.2.2 Canada

5.3.2.2.3 Mexico

5.3.2.3 Europe

5.3.2.3.1 Germany

5.3.2.3.2 United Kingdom

5.3.2.3.3 Italy

5.3.2.3.4 France

5.3.2.3.5 Rest of Europe

5.3.2.4 Rest of the World

5.3.2.4.1 South America

5.3.2.4.2 Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%) **/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 BHP

6.4.2 CMOC

6.4.3 Cobalt Blue Holdings Limited

6.4.4 Eramet

6.4.5 Eurasian Resources Group

6.4.6 Gecamines SA

6.4.7 Glencore

6.4.8 Huayou Cobalt Co., Ltd.

6.4.9 Jervois

6.4.10 Jinchuan Group International Resources Co. Ltd

6.4.11 Panoramic Resources

6.4.12 Sherritt International Corporation

6.4.13 Umicore N.V.

6.4.14 Vale

6.4.15 Wheaton Precious Metals Corp

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Commercialization of Environmentally Friendly Recyclable Cobalt