ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

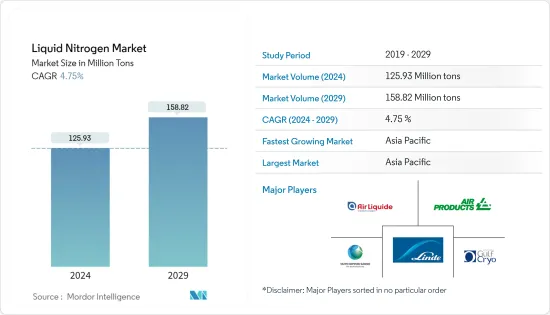

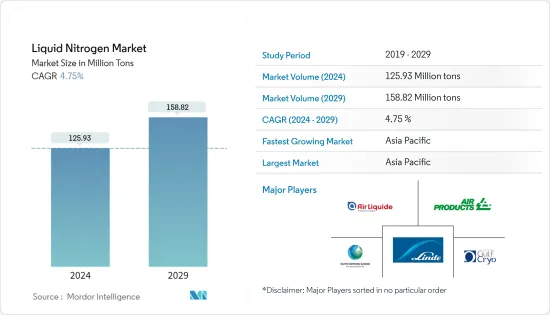

액체 질소 시장 규모는 2024년 1억 2,593만 톤으로 추정되며, 2029년에는 1억 5,882만 톤에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 4.75%의 CAGR로 성장할 것으로 예상됩니다.

COVID-19는 시장 성장을 저해했습니다. 운송 산업은 세계 규제로 인해 전염병으로 인해 어려움을 겪었습니다. 그러나 전염병으로 인해 건강 관리 산업은 건강에 대한 우려가 증가함에 따라 큰 성장을 보였습니다. 의료기기에 대한 수요가 크게 증가함에 따라 액체 질소 시장의 수요도 증가했습니다. 현재 시장은 전염병에서 회복되어 상당한 성장을 보이고 있습니다.

주요 하이라이트

중기적으로는 화학 및 제약 산업의 수요 증가와 헬스케어 산업에서의 사용 확대가 시장 성장의 원동력이 되고 있습니다.

그러나 액체 질소 플랜트 유지보수에 대한 규제 제약이 있어 시장 성장에 걸림돌이 될 것으로 예상됩니다.

그러나 새로운 제조 기술의 개척은 향후 몇 년 동안 시장에 기회를 가져다 줄 가능성이 높습니다.

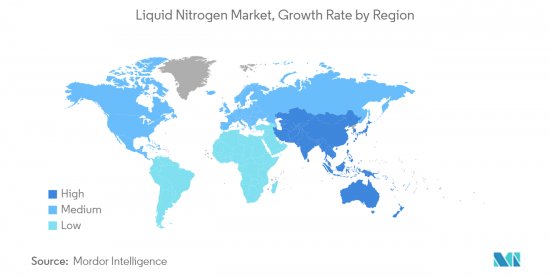

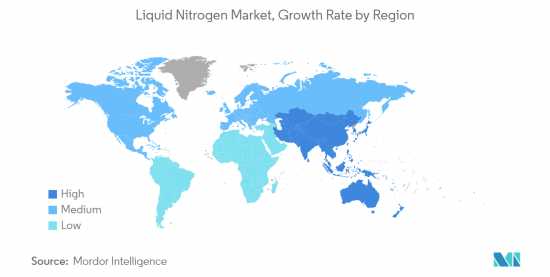

아시아태평양은 중국, 인도, 일본 등 국가들의 소비가 가장 많으며 세계 시장을 독점하고 있습니다.

액체 질소 시장 동향

화학 및 제약 업계의 수요 확대

액체 질소는 액체 공기의 분별 증류를 통해 상업적으로 생산되는 질소 원소의 액체입니다. 많은 냉각 및 극저온 응용 분야에서 사용됩니다.

무독성, 무취, 무색, 화학적으로 불활성이며 인화하기 쉬운 특성으로 인해 화학 및 제약 산업에서 많이 사용됩니다.

질소의 끓는점은 섭씨 -195도입니다. 이 때문에 화학 및 제약 산업에서 냉각제 및 냉매로 급속히 확대되고 있습니다.

중국의 제약 산업은 세계 최대 규모를 자랑합니다. 중국에서는 제네릭 의약품, 치료약, 원료 의약품, 한약이 생산되고 있습니다.

중국 국가통계국에 따르면 2022년 6월 중국 화학약품 원료의약품의월 생산량이 30만 톤을 넘어섰다고 합니다. 이 수치는 지난 3년 동안 점진적으로 증가하여 중국 화학약품 사업의 발전을 보여주고 있습니다. 의약품 유효성분은 질병을 치료하는 역할을 하는 의약화학제품입니다.

또한, 인도는 2022년 2월 현재 220억 달러 이상의 의약품을 공급하는 세계 최대 제네릭 의약품 공급국이라고 제약국에 따르면, 2022년 2월 현재 인도는 220억 달러 이상의 의약품을 공급하고 있습니다. 수량 측면에서 인도 의약품은 전 세계 제네릭 의약품 수출의 20%를 차지하며 북미가 대부분을 차지하고 있으며, 2030년에는 약 1,000억 달러에 달할 것으로 예상되며 향후 몇 년 동안이 시장의 잠재력이 높아질 것으로 예상됩니다.

질소는 건조하고 불활성 기체라는 것이 가장 큰 장점 중 하나입니다. 이는 다른 물질과 상호 작용하지 않는다는 것을 의미합니다. 그 결과, 산소나 기타 독성 가스 또는 원치 않는 가스, 특히 산소를 질소로 대체할 수 있습니다.

질소는 의약품을 생산할 때 반응 혼합물을 한 용기에서 다른 용기로 옮기는 데 자주 사용됩니다. 액체 또는 분말 의약품을 운반할 때 안전한 불활성 가스를 사용하는 것이 매우 중요합니다. 일부 의약품의 화학제품은 산소나 수증기와 접촉하면 유해하거나 폭발할 수 있습니다.

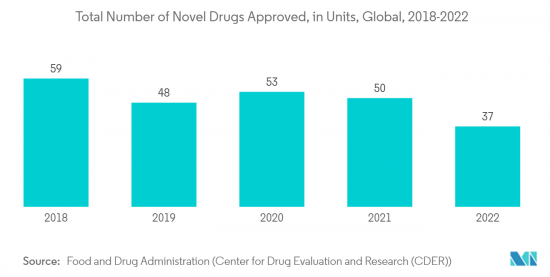

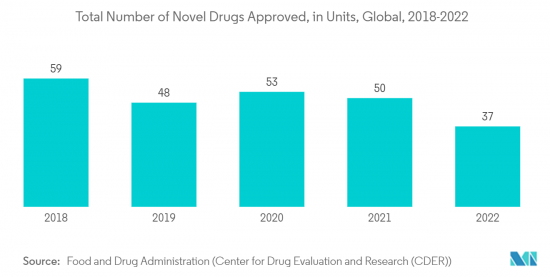

식품약품감독관리국(의약품평가연구센터(CDER)에 따르면 2022년 37개의 신약이 승인되었습니다. 시장에 출시되는 신약의 양은 매년 크게 변동하며, 2021년에는 50개의 독특한 약품이 승인되었습니다.

위의 모든 요인 덕분에 예측 기간 동안 화학 및 제약 산업에서 액체 질소에 대한 수요가 증가할 것으로 예상됩니다.

시장을 독점하는 아시아태평양

예측 기간 동안 아시아태평양이 액체 질소 시장을 주도할 것으로 예상됩니다. 중국, 인도, 일본 등의 국가에서 화학 및 제약 산업의 성장이 이 지역의 액체 질소 시장 수요를 촉진하고 있습니다.

China's Healthcare Report에 따르면, 중국의 의약품과 바이오의약품을 합친 R&D 투자는 2023년까지 연평균 23%씩 증가할 것으로 예상됩니다. 이는 490억 달러에 달해 전 세계 의약품 개발 및 시험 지출의 23%를 차지할 것으로 예상됩니다.

중국에는 약 5,000여 개의 제조업체로 구성된 대규모의 다양한 국내 제약 산업이 있으며, 그 중 상당수는 중소기업입니다. 이는 제약 산업에서 액체 질소 사용의 성장을 촉진할 것으로 기대됩니다.

국가약품감독관리국과 국가중의약관리국은 공동으로 "제14차 제약산업 성장 5개년 계획"을 발표하였습니다. 제14차 5개년 계획은 향후 5년간 중국 제약산업의 발전 목표와 방향을 명시하고 있습니다.

제14차 5개년 계획은 '국가 경제 및 사회 발전을 위한 제14차 5개년 계획 및 2035년 장기 목표의 틀'에서 제시된 개념과 기준에 따라 수립되었습니다.

인도는 화학 산업의 강력한 성장이 예상됩니다. 정부는 화학 산업이 2025년까지 3,040억 달러에 달할 것으로 예상하고 있으며, 향후 5년간 연간 약 9%의 수요 증가가 예상됨에 따라 그 기회가 제공될 것으로 보고 있습니다.

Integrated Cold Chain and Value Addition Infrastructure Scheme에 따르면, 인도에서는 2022년까지 식품 가공 산업에서 약 356개의 콜드체인 프로젝트가 승인되어 액체 질소에 대한 수요가 증가하고 있습니다.

아시아태평양의 주요 액체 질소 제조업체로는 Linde PLC, Southern Industrial Gas Sdn Bhd, MVS Engineering Pvt. Ltd, TAIYO NIPPON SANSO CORPORATION 등이 있습니다.

따라서 위의 요인은 예측 기간 동안이 지역의 액체 질소 시장 수요를 증가시킬 것으로 예상됩니다.

액체 질소 산업 개요

액체 질소 시장은 세분화되어 있습니다. 주요 기업으로는 Air Liquide, Air Products and Chemicals, Inc., Gulf Cryo, Linde plc, TAIYO NIPPON SANSO CORPORATION 등이 있습니다.

기타 혜택:

엑셀 형식의 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사 가정

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

화학·제약 업계로부터의 수요 증가

헬스케어 산업에서의 용도 확대

기타 촉진요인

성장 억제요인

액체 질소 플랜트 유지의 규제 제한

기타 저해요인

산업 밸류체인 분석

Porter's Five Forces 분석

공급 기업의 교섭력

구매자의 교섭력

신규 참여업체의 위협

대체품의 위협

경쟁 정도

제5장 시장 세분화(시장 규모, 수량 기준)

저장 유형

봄베

패키지 가스

기능

냉각제

냉매

최종 이용 산업

화학·제약

헬스케어

운송

기타 최종 이용 산업

지역

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카공화국

기타 중동 및 아프리카

제6장 경쟁 상황

M&A, 합작투자, 제휴, 협정

시장 점유율 분석(%)**/순위 분석

주요 기업의 전략

기업 개요

Air Liquide

Air Products and Chemicals, Inc.

Cryomech Inc.

Gulf Cryo

Linde plc

MVS Engineering Pvt. Ltd

Southern Industrial Gas Sdn Bhd

Praxair Technology, Inc.

Messer Group

TAIYO NIPPON SANSO CORPORATION

제7장 시장 기회와 향후 동향

새로운 제조 기술 개발

기타 기회

ksm

영문 목차

영문목차

The Liquid Nitrogen Market size is estimated at 125.93 Million tons in 2024, and is expected to reach 158.82 Million tons by 2029, growing at a CAGR of 4.75% during the forecast period (2024-2029).

COVID-19 hampered the market growth. The transportation industry suffered from the pandemic due to restrictions worldwide. However, due to the pandemic, the healthcare industry witnessed huge growth because of increased health concerns. It increased the demand for the liquid nitrogen market, as the demand for medical devices increased tremendously. Currently, the market recovered from the pandemic and is growing at a significant rate.

Key Highlights

Over the medium term, the increasing demand from the chemical and pharmaceutical industry and the growing application in the healthcare industry are driving market growth.

However, the regulatory restrictions in maintaining liquid nitrogen plants are expected to hinder the market's growth.

Nevertheless, developing new manufacturing techniques will likely create opportunities for the market in the coming years.

The Asia-Pacific region dominated the global market with the largest consumption from countries such as China, India, and Japan.

Liquid Nitrogen Market Trends

Growing Demand from the Chemical and Pharmaceutical Industry

Liquid nitrogen is the liquefied form of the element nitrogen produced commercially by the fractional distillation of liquid air. It is used in many cooling and cryogenic applications.

Owing to its non-toxic, odorless, colorless, chemically inert, and inflammable properties, its application is highly used in the chemical and pharmaceutical industry.

The boiling point of nitrogen is -195 degrees Celsius. Because of this, its application as a coolant and refrigerant in the chemical and pharmaceutical industry is rapidly increasing.

The pharmaceutical industry in China is one of the largest in the world. The country produces generics, therapeutic medicines, active pharmaceutical ingredients, and traditional Chinese medicine.

According to the National Bureau of Statistics of China, in June 2022, China's monthly output volume of chemical active pharmaceutical ingredients (API) topped 300,000 metric tonnes. The figure gradually climbed over the previous three years, indicating a development in China's chemical medication business. Active pharmaceutical ingredients are medicinal chemicals responsible for a condition's therapy.

Moreover, according to the Department of Pharmaceuticals, India is the world's largest supplier of generic medications, and as of February 2022, the country supplied pharmaceuticals worth more than USD 22 billion. Regarding volume, Indian pharmaceuticals accounted for 20% of worldwide generic drug exports, with North America accounting for the lion's share. It is expected to value about USD 100 billion by 2030, increasing the scope for this market during the coming years.

The fact that nitrogen is a dry, inert gas is one of its greatest advantages. It implies that it won't interact with other substances. As a result, oxygen and other toxic or unwanted gases, particularly oxygen, can be replaced by N2.

Nitrogen is frequently used to manufacture pharmaceuticals to transfer the reaction mixture from one container to another. When delivering liquid or powdered medications, it is crucial to employ safe, inert gas since doing so might be hazardous. Several pharmaceutical chemicals may be harmed or even explode if exposed to oxygen or water vapor.

According to the Food and Drug Administration (Center for Drug Evaluation and Research (CDER)), it authorized 37 new medications in 2022. The amount of new pharmaceutical products hitting the market each year fluctuates greatly. In 2021, there were 50 approvals for unique medications.

Owing to all the factors mentioned above, the demand for liquid nitrogen is expected to grow from the chemical and pharmaceutical industries during the forecast period.

Asia-Pacific Region to Dominate the Market

The Asia-Pacific region is expected to dominate the market for liquid nitrogen during the forecast period. The growing chemical and pharmaceutical industries in countries such as China, India, and Japan are boosting the demand for the liquid nitrogen market in the region.

According to China's Healthcare Report, China's pharmaceutical and biopharmaceutical combined R&D investment is projected to expand at a compound annual rate of 23% through 2023. It will be possible when it reaches USD 49 billion, accounting for 23% of global drug development and testing spending.

The country includes a large and diverse domestic drug industry, comprising around 5,000 manufacturers, of which many are small- or medium-sized companies. It is expected to boost the growth of liquid nitrogen usage in the pharmaceutical industry.

The National Medical Products Administration and the National Administration of Traditional Chinese Medicine collaborated to release the "14th Five-Year Plan for Pharmaceutical Industry Growth." The 14th Five-Year Plan specifies the aims and directions for China's pharmaceutical industry's development during the following five years.

The 14th Five-Year Plan was developed in compliance with the ideas and standards outlined in the Framework of the 14th Five-Year Plan for National Economic and Social Development and Long-Term Goals for 2035.

India is expected to witness robust growth in its chemical industry. The government predicts the chemical industry to reach USD 304 billion by 2025, with opportunities offered by the anticipated increase in demand by about 9% per annum over the next five years.

According to the Scheme of Integrated Cold Chain and Value Addition Infrastructure, about 356 Cold Chain Projects in the food processing industry were approved in India in 2022, creating an increasing demand for liquid nitrogen.

Some leading producers of liquid nitrogen in the Asia-Pacific region include Linde PLC, Southern Industrial Gas Sdn Bhd, MVS Engineering Pvt. Ltd, and TAIYO NIPPON SANSO CORPORATION.

Therefore, the factors above are expected to boost the demand for the liquid nitrogen market in the region during the forecast period.

Liquid Nitrogen Industry Overview

The liquid nitrogen market is fragmented in nature. Some of the major players in the market include Air Liquide, Air Products and Chemicals, Inc., Gulf Cryo, Linde plc, and TAIYO NIPPON SANSO CORPORATION, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Demand from the Chemical and Pharmaceutical Industry

4.1.2 Growing Application in the Healthcare Industry

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Regulatory Restrictions in Maintaining Liquid Nitrogen Plant

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

5.1 Storage Type

5.1.1 Cylinder

5.1.2 Packaged Gas

5.2 Function

5.2.1 Coolant

5.2.2 Refrigerant

5.3 End-user Industry

5.3.1 Chemical and Pharmaceutical

5.3.2 Healthcare

5.3.3 Transportation

5.3.4 Other End-user Industries

5.4 Geography

5.4.1 Asia-Pacific

5.4.1.1 China

5.4.1.2 India

5.4.1.3 Japan

5.4.1.4 South Korea

5.4.1.5 Rest of Asia-Pacific

5.4.2 North America

5.4.2.1 United States

5.4.2.2 Canada

5.4.2.3 Mexico

5.4.3 Europe

5.4.3.1 Germany

5.4.3.2 United Kingdom

5.4.3.3 Italy

5.4.3.4 France

5.4.3.5 Rest of Europe

5.4.4 South America

5.4.4.1 Brazil

5.4.4.2 Argentina

5.4.4.3 Rest of South America

5.4.5 Middle-East and Africa

5.4.5.1 Saudi Arabia

5.4.5.2 South Africa

5.4.5.3 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements