ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

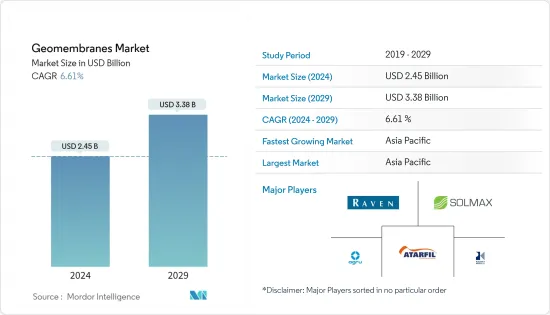

지오멤브레인 시장 규모는 2024년에 24억 5,000만 달러로 추정되고, 2029년에는 33억 8,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2024-2029년) CAGR은 6.61%로 성장할 전망입니다.

COVID-19 팬데믹의 다양한 최종 사용자 산업의 성장에 미치는 영향과 그에 따른 공급망의 혼란은 시장에 부정적인 영향을 미칩니다. 이 외에도 수처리 기술을 제공하는 많은 기업들이 경제 불안으로 인해 보조금 가격을 낮추고 있으며, 이는 시장 조사에 더욱 영향을 미치고 있습니다.

주요 하이라이트

시장 성장을 이끌고 있는 요인은 라이닝 용도에서의 사용 증가, 채광 용도에서의 지오멤브레인 사용 증가 및 환경 보호를 위한 엄격한 규제 틀입니다.

반면에, 라이닝 시스템과 매립지에서 지오신세틱 클레이 라이너의 사용이 증가하고 상황에 따라 응력 균열이 발생할 수 있다는 것은 조사 대상 시장의 성장을 방해합니다.

가혹한 운용 조건에 적합한 탄력성이 있는 지오멤브레인의 개발이나 제조 부문에서의 절수 의식 증가 등의 요인은 예측 기간 동안 제조업체에게 많은 기회를 제공할 것으로 보입니다.

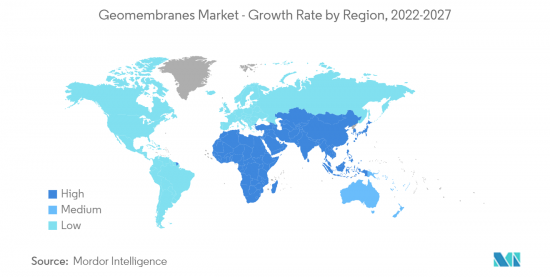

아시아태평양은 중국과 인도 등의 소비 증가로 시장 규모, 성장률 모두 세계 시장을 석권하고 있습니다.

지오멤브레인 시장 동향

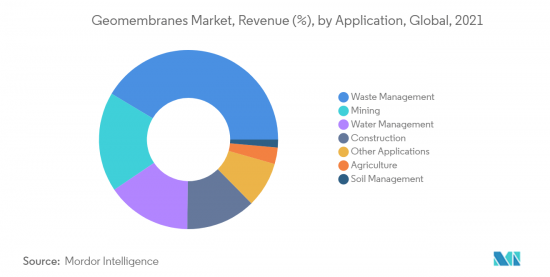

폐기물 관리 분야가 시장을 독점

최근 물 관리 용도가 세계 시장을 석권하고 있습니다. 연못과 운하에서 저수지에 이르기까지 지오멤브레인은 모든 곳에서 적용됩니다. 전 세계적으로 50,000개가 넘는 댐이 건설되고 더 많은 댐이 건설 중이기 때문에 물 보전을 위한 지오멤브레인의 사용이 많습니다.

그러나 담수 공급이 감소하는 가운데 물 관리의 필요성은 전례 없이 높아지고 있습니다.

침투는 도수 계획에서 물 손실의 주요 원인입니다. 그러나 적절한 라이닝을 적용하면 이 손실을 크게 줄일 수 있습니다.

절수에 대한 관심이 높아짐에 따라 지오멤브레인 수요도 예측 기간 동안 빠르게 증가할 것으로 예상됩니다.

지오멤브레인 수요는 물의 효율적인 이용과 지하수위 개선에 대한 요구가 높아짐에 따라 운하 라이닝 용도에서도 증가하고 있습니다. 중국, 인도, 우즈베키스탄 등 아시아태평양의 여러 나라가 운하 라이닝 용도에 사용되는 지오멤브레인에 대한 최대 수요를 창출하고 있습니다.

이러한 플러스 요인은 예측 기간 동안 물 관리 산업에서 지오멤브레인의 사용을 촉진할 것으로 예상됩니다.

독일이 유럽을 지배

독일은 2021년 3월 말과 4월에 새로운 코로나바이러스 집단 감염에 휩쓸려 기업, 영향을 받은 노동자 및 의료제도에 대한 보정예산과 재정지원의 연장이 승인되었습니다.

독일의 앙겔라 메르켈 총리는 16년 만에 독일 수장 자리에서 물러나게 돼, 독일 경제의 새로운 시대를 열게 됐습니다. 정치 지도자들이 디지털화와 기후 변화 정책을 꺼리는 가운데, 과세와 지출은 증가할 수 있으며, 정부 부채 증가에 대한 경계감은 후퇴할 수 있습니다.

주로 동국 북부 지역에서의 수처리 활동의 활성화가 막기술 시장 수요를 밀어 올리고 있습니다. 이러한 중요성으로부터 효율적인 상하수도 처리방법이 도입되어 독일에서는 거의 100%의 폐수가 유럽연합(EU)이 정하는 최고기준을 충족하도록 처리되고 있습니다.

독일에서는 일반 가정, 산업 및 무역으로 매년 50억 입방미터 이상의 오수가 발생합니다. 포장된 노면과 도로의 빗물은 약 30억 입방미터가 하수처리장으로 배출되고, 상당한 양의 침투수가 누수에 의해 하수도 시스템으로 유입되고 있습니다.

게다가 독일에서는 환경보전형 농업운동이 급성장하고 있으며, 보다 환경친화적인 농업부문을 목표로 하고 있습니다. 이 거대한 규모는 기세가 늘어나면서 예측 기간 동안 이 나라의 농업용도 시장에서 조사된 시장의 견인력이 될 것으로 예측됩니다.

지오멤브레인 산업 개요

세계의 지오멤브레인 시장은 매우 세분화된 시장이며 시장을 좌우하는 큰 점유율을 가진 기업이 없습니다. 지오멤브레인 시장의 주요 기업으로는 SOLMAX, Raven Industries, Inc., AGRU America, Inc., ATARFIL, SL, Plastika Kritis SA 등이 있습니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제 조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

라이닝 용도로의 사용 확대

채광 용도에서의 지오멤브레인 사용 증가

억제요인

라이닝 시스템 및 매립지에서의 지오신세틱 클레이 라이너의 사용 증가

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화

원재료

고밀도 폴리에틸렌(HDPE)

저밀도 폴리에틸렌(LDPE)

선형 저밀도 폴리에틸렌(LLDPE)

폴리염화비닐(PVC)

에틸렌 프로파일렌 디엔 단량체(EPDM)

폴리프로필렌(PP)

기타 원재료

용도

물 관리

폐기물 관리

광업

건설

농업

토양 관리

기타 용도

지역

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

스페인

기타 유럽

남미

브라질

아르헨티나

칠레

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴 및 협정

시장 점유율**(%) 및 랭킹 분석

주요 기업의 전략

기업 프로파일

AGRU America, Inc.

ATARFIL, SL

Firestone Building Products Company LLC

Istanbul Teknik

Jutta Ltd.

NAUE GmbH & Co. KG

Nilex Inc.

Officine Maccaferri Spa

Plastika Kritis SA

Raven Industries, Inc.

RENOLIT SE

Shanghai Yingfan Engineering Material Co., Ltd

SOLMAX

Sotrafa

Texel Industries

제7장 시장 기회 및 앞으로의 동향

제조업에 있어서의 절수 의식 고조

AJY

영문 목차

영문목차

The Geomembranes Market size is estimated at USD 2.45 billion in 2024, and is expected to reach USD 3.38 billion by 2029, growing at a CAGR of 6.61% during the forecast period (2024-2029).

The impact of COVID-19 pandemic on the various end-user industries' growth and the resultant supply chain disruptions has impacted the market negatively. Apart from this many companies that offer water treatment technologies have reduced subsidized prices due to economic instability which further has impacted the market studied.

Key Highlights

The factors driving the growth of the market studied are the growing use in lining applications, increased use of geomembranes in mining applications, and stringent regulatory framework for environmental protection.

On the flip side, increasing the use of geosynthetic clay liners in lining systems and landfills, and the potential for stress cracking in some situations will hinder the growth of the market studied.

Factors such as the development of resilient geomembrane suitable to harsh operational conditions and rising awareness about water conservation in the manufacturing sector are likely to offer numerous opportunities for the manufacturers over the forecast period.

Asia-Pacific dominated the global market both in terms of size and growth owing to the increasing consumption for countries such as China and India, among others.

Geomembranes Market Trends

Waste Management Segment to Dominate the Market

The water management application dominated the global market in the recent past. From ponds and canals to reservoirs, geomembranes have applications everywhere. With more than 50,000 dams worldwide and many more under construction, the use of geomembranes for water preservation is high.

However, with the declining freshwater supplies, the need for water management is higher than ever.

Seepage is a major source of water loss in conveyance schemes. However, this loss could be significantly curtailed through proper lining.

As concerns about water conservation are on the rise, the demand for geomembrane too is expected to rise at a rapid pace over the forecast period.

The demand for geomembrane is also increasing in canal lining applications, due to the growing need for the efficient usage of water and the remediate groundwater levels. Various countries in Asia-Pacific, such as China, India, and Uzbekistan, are generating the largest demand for geomembranes to be used in the canal lining application.

These positive factors are expected to drive the usage of geomembrane in the water management industry over the forecast period.

Germany to Dominate the European Region

Germany has been hit by new coronavirus outbreaks in late March and April 2021 and has approved supplementary budgets or extended financial support for businesses, affected workers, and the health care system.

German Chancellor Angela Merkel is about to bow out as head of Germany after 16 years, marking the start of a new era for the country's economy. Taxation and spending could increase as political leaders double down on digitization and climate policy, thus wariness about rising government debt may take a back seat.

The increasing water treatment activities, primarily in the northern region of the country, are boosting the demand for the membrane technologies market. This importance has led to efficient water and wastewater treatment methods, and nearly 100% of the wastewater in Germany is treated to meet the highest standards set by the European Union.

Germany has more than five billion cubic meters of sewage water, which is generated, each year by private households, industry, and trade. Approximately three billion cubic meter of rainwater from paved surfaces and roads are discharged into sewage treatment plants, with a considerable additional amount of infiltration water entering the sewer system through leaks.

Moreover, the green agriculture movement in Germany is growing fast, pushing the nation for an eco-friendlier agricultural sector. The huge size, coupled with the growing momentum, is projected to gain traction for the market studied in agricultural applications market in the country during the forecast period.

Geomembranes Industry Overview

The global geomembrane market is a highly fragmented market with no player having a significant share to influence the market. Key players in the geomembranes market include (not in any particular order) SOLMAX, Raven Industries, Inc., AGRU America, Inc., ATARFIL, S.L., and Plastika Kritis SA, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Growing Use in Lining Applications

4.1.2 Increased Use of Geomembranes in Mining Applications

4.2 Restraints

4.2.1 Increasing Use of Geosynthetic Clay Liner in Lining Systems and Landfill

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION

5.1 Raw Material

5.1.1 High-density Polyethylene (HDPE)

5.1.2 Low-density Polyethylene (LDPE)

5.1.3 Linear Low-density Polyethylene (LLDPE)

5.1.4 Polyvinyl Chloride (PVC)

5.1.5 Ethylene Propylene Diene Monomer (EPDM)

5.1.6 Polypropylene (PP)

5.1.7 Other Raw Materials

5.2 Application

5.2.1 Water Management

5.2.2 Waste Management

5.2.3 Mining

5.2.4 Construction

5.2.5 Agriculture

5.2.6 Soil Management

5.2.7 Other Applications

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Spain

5.3.3.6 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Chile

5.3.4.4 Rest of South America

5.3.5 Middle-East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share**(%)/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 AGRU America, Inc.

6.4.2 ATARFIL, S.L.

6.4.3 Firestone Building Products Company LLC

6.4.4 Istanbul Teknik

6.4.5 Jutta Ltd.

6.4.6 NAUE GmbH & Co. KG

6.4.7 Nilex Inc.

6.4.8 Officine Maccaferri Spa

6.4.9 Plastika Kritis SA

6.4.10 Raven Industries, Inc.

6.4.11 RENOLIT SE

6.4.12 Shanghai Yingfan Engineering Material Co., Ltd

6.4.13 SOLMAX

6.4.14 Sotrafa

6.4.15 Texel Industries

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Rising Awareness About Water Conservation in the Manufacturing Sector