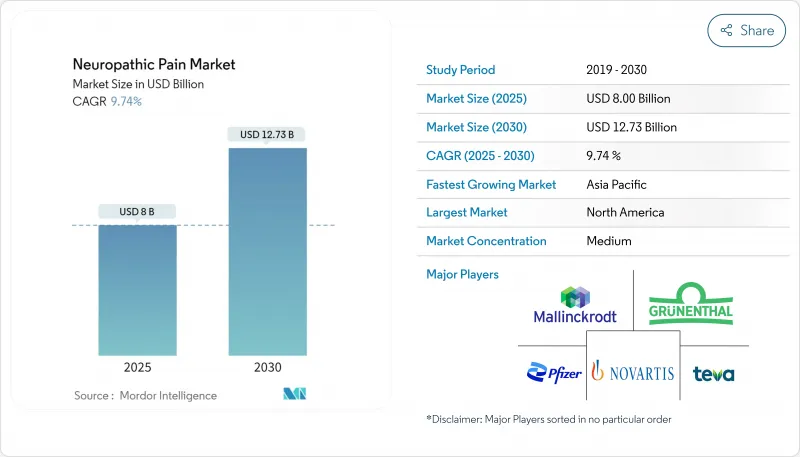

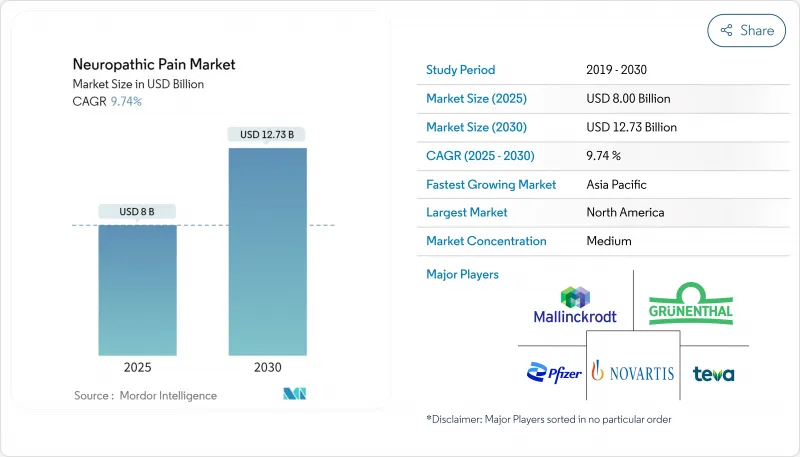

신경병증성 통증 시장 규모는 2025년 80억 달러로 추정되고, 예측 기간(2025-2030년)의 CAGR은 9.74%로, 2030년에는 127억 3,000만 달러에 달할 것으로 예상됩니다.

당뇨병, 암 생존, 바이러스 감염 등의 유병률이 상승하고 치료 대상 인구가 증가하는 한편, 규제 당국, 지불자, 임상의는 남용 위험이 낮은 비오피오이드 선택을 점점 선호하게 되고 있습니다. 실제 처방감사에서 얻은 증거에 따르면, 중추에 작용하는 진통제에서 말초에 선택적으로 작용하는 약제로 꾸준히 이동하고 있으며, 신경병증성 통증 시장 점유율의 구조적 재조정을 시사하고 있습니다. 저분자 나트륨 채널 차단제, 생물학적 신경성장 인자 길항제, 고급 외용제에 이르는 파이프라인의 다양성은 메커니즘 기반 차별화에 대한 상업적 확신을 뒷받침합니다. 게다가, 기능적인 향상을 측정할 수 있는 의료 제공업체의 환경에 있어서, 가장 빠른 속도로 도입이 진행되고 있는 것도, 결과에 연동한 상환이 이미 치료의 선택지를 형성하고 있는 것을 시사하고 있습니다.

당뇨병의 세계적인 유행은 당뇨병 말초 신경장애(DPN)가 당뇨병 환자의 약 50%에 영향을 미치는 등 신경병증성 통증의 상황을 근본적으로 바꾸고 있습니다. 이 높은 유병률은 효과적인 통증 관리 솔루션이 필요한 많은 환자를 의미합니다. 최근의 역학 조사에서 DPN은 종종 과소 진단되고 증상이 중증화 될 때까지 75%의 사례가 발견되지 않은 채로 남아있는 것으로 밝혀졌으며 미개척의 큰 시장 기회를 창출하고 있습니다. DPN의 경제적 부담은 직접적인 치료비에 그치지 않고, 고통스러운 DPN 환자는 생산성 저하 및 여러 전문 분야에 걸쳐 건강 관리 이용률의 상승을 경험하기 때문에 부작용을 최소화하면서 기능적 결과를 개선할 수 있는 보다 효과적이고 내약한 치료 옵션에 대한 수요가 높아지고 있습니다.

암치료의 효능이 향상됨에 따라 화학요법유발성 말초신경병증(CIPN)를 경험하는 생존자의 집단은 계속 확대되고 있으며, 효과적인 관리 전략의 긴급한 필요성이 생기고 있습니다. CIPN은 신경독성 화학요법제를 투여받은 환자의 30-40%가 병을 앓고 있으며, 치료가 끝난 후에도 증상이 지속되는 경우가 많습니다. 이 증상은 QOL에 큰 영향을 미치고 화학 요법의 체중 감소를 강요하고 종양 학적 결과를 손상시킬 수 있습니다. 최근 CIPN의 병태생리의 해명이 진행되어 산화스트레스와 신경염증의 역할이 밝혀져 기존의 진통제에 그치지 않는 새로운 치료법이 열리고 있습니다. CIPN의 조기 발견을 위한 바이오마커 개발은 기세를 늘리고 있으며, 신경영양인자와 마이크로RNA는 고위험 환자의 동정에 유망합니다. 이러한 추세는 CIPN 치료에 대처할 수 있는 시장을 축소시킬 수 있습니다. 예방적 개입은 의약품에 의한 관리가 필요한 중증례의 발생률이 저하될 가능성이 있기 때문입니다. 제약 회사는 치료의 혁신과 예방 및 조기 개입 전략의 개선으로 시장 억제 효과의 균형을 맞추는 전략적 과제에 직면하고 있습니다.

전통적인 신경병증성 통증 치료의 임상적 유용성은 안전성에 대한 우려와 규제 당국의 모니터링을 통해 점점 제약을 받고 있습니다. 오피오이드는 진통 효과에도 불구하고 남용의 가능성이 높고 오피오이드의 오용과 관련된 공중 보건 위기가 진행되고 있기 때문에 엄격한 처방 제한에 직면하고 있습니다. 가바펜티노이드(프레가발린과 가바펜틴)는 많은 신경병증성 통증 질환에 효과적이지만 오용 가능성과 의존성 문제가 새롭게 입증되었기 때문에 규제 당국의 모니터링이 강화되고 있습니다. 이러한 안전 과제는 리스크 혜택 프로파일이 개선된 치료법으로 시장의 근본적인 변화를 촉진하고 있습니다. 혈액 뇌 장벽을 통과하지 않는 말초 작동 진통제의 개발은 이러한 우려에 대한 전략적 대응이며 남용 가능성을 초래하는 중추 신경계에 영향을 미치지 않는 진통제입니다. 이러한 안전성 중심 시장 발전는 현재의 표준 치료의 한계를 다루면서 효과를 유지할 수 있는 새로운 치료 접근법의 기회를 창출하고 있습니다.

항경련제는 2024년에 33.50%로 가장 큰 시장 점유율을 차지하며, 프레가발린과 가바펜틴은 여러 신경병증성 통증 질환에 대한 효능이 확립되어 중심 치료제가 되었습니다. 이러한 약물의 작용기전은 주로 칼슘 채널의 조절과 GABA 활성의 증강에 관여하며, 신경병증성 통증 상태를 특징으로 하는 흥분성의 항진에 효과적으로 대처합니다. 최근의 비교 분석에 따르면, 프레가발린은 가바펜틴에 비해 뛰어난 진통 효과를 나타내며, 유해 사건도 적다는 것이 밝혀졌습니다. 항경련제는 우위성에도 불구하고 더 나은 안전성 프로파일과 표적 메커니즘을 가질 수 있는 새로운 약물 클래스별 과제에 직면하고 있습니다. 국소 치료제는 CAGR 10.10%(2025-2030년)로 가장 급성장하고 있는 부문이며, 특히 국소적인 신경병증성 통증에 대한 양호한 위험 베네핏 프로파일이 그 원동력이 되고 있습니다. SNRI는 당뇨병성 말초신경병증에 대한 듀록세틴의 확립된 효능으로 시장에서 큰 존재감을 유지하고 있는 반면, 오피오이드는 안전에 대한 우려와 규제상의 한계 속에서 사용률의 저하에 직면하고 있습니다. NMDA 길항제와 칸나비노이드를 포함한 "기타 클래스" 부문은 신경병성 통증 경로를 표적으로 하는 새로운 메커니즘의 연구가 진행됨에 따라 유망한 성장 잠재력을 보여줍니다.

제약 기업이 전략적으로 포트폴리오를 차별화된 메커니즘을 향해 재배치하고 있기 때문에 약물 클래스별 경쟁 역학이 진화하고 있습니다. 여러 통증 경로를 동시에 표적화하는 병용 요법은 단일 요법에 비해 우수한 치료 효과를 가져올 수 있으며, 치료 알고리즘을 재구성할 수 있다는 것이 새로운 증거에 의해 제안되었습니다. 이 동향은 개별 약물의 부작용을 최소화하면서 신경 병성 통증의 복잡한 병태 생리에 대응할 수있는 합리적인 polypharmacy와 합제에 대한 관심을 높입니다. 스제트리긴과 같은 새로운 약물의 최근 승인은 현재의 증상 기반 접근법이 아닌 메커니즘 기반 처방으로의 패러다임 이동의 가능성을 보여주며, 향후 몇 년 동안 약물 등급별 시장 점유율 분포를 근본적으로 바꿀 수 있습니다.

당뇨병성 말초신경병증(DPN)는 전 세계적으로 증가하는 당뇨병 환자에서 높은 유병률을 반영하여 2024년 시장 점유율 32.30%를 차지하며 적응증의 대부분을 차지했습니다. 이 질환은 당뇨병이 걸린 기간이 10년을 넘는 환자의 약 50%가 이환되어 환자 수가 크게 확대되고 있습니다. DPN의 치료 접근법은 증상 관리뿐만 아니라 근본적인 병태 생리학적 메커니즘을 다루는 것으로 진화하고 있으며, 신경 장애의 진행을 예방하거나 지연시키는 질병 수정 요법에 대한 주목이 높아지고 있습니다. 화학요법유발성 말초신경병증(CIPN)는 CAGR (2025-2030년)이 11.56%로 가장 급성장하고 있는 적응증으로, 암 생존율의 향상과 CIPN이 QOL에 미치는 영향에 대한 인식의 고조가 그 원동력이 되고 있습니다. 대상 포진 후 신경통은 그 특징적인 병태 생리와 치료 과제에 의해 큰 시장 점유율을 유지하고 있습니다. 한편, 3차 신경통은 작지만 치료 알고리즘이 특이한 부문입니다.

보다 조기 개입과 보다 정확한 환자층별화를 가능하게 하는 진단 능력과 바이오마커 개발의 진보로 적응증 상황이 재구성되고 있습니다. 최근 연구는 신경 영양 인자 및 마이크로 RNA와 같은 CIPN의 잠재적인 바이오마커를 확인하고 고위험 환자의 예방 전략을 촉진할 수 있습니다. HIV 관련 신경 장애에서는 직접 통증 개입과 함께 항 레트로 바이러스 요법의 최적화가 관리의 중요한 요소로 인식되고 있습니다. 환지통은 FDA가 승인한 Altius Direct Electrical Nerve Stimulation System을 포함한 혁신적인 접근 방식의 혜택을 누리고 있습니다. 이러한 적응증에 특화된 접근의 진보가 시장의 세분화를 촉진하고, 각 증상에 특유의 병태생리학적 특징에 대응하는 표적 치료의 기회를 창출하고 있습니다.

북미가 2024년 점유율 42.50%로 신경병증성 통증 시장을 독점하고 있으며, 높은 질병 유병률, 선진 헬스케어 인프라, 유리한 상환 정책이 그 원동력이 되었습니다. 이 지역의 주도적 지위는 혁신적 치료제의 주요 상시 시장으로서의 역할에 의해 강화되고 있으며, 그 예로 최근 FDA가 20년 이상 만에 진통제 클래스의 신약으로서 Journavx(suzetrigine)를 승인한 것을 들 수 있습니다. NOPAIN법의 시행은 외래환자에 있어서 비오피오이드 진통요법에 특화된 상환제도를 창설하는 것이며, 중요한 정책적 진보입니다. 이러한 규제의 추풍에 의해 신규 신경병증성 통증 치료제, 특히 기존의 선택보다 뛰어난 것으로 입증된 치료제 시장 진입이 가속될 것으로 기대됩니다. 북미에서는 환자 수가 많고 의료비 상승을 반영하여 미국이 가장 큰 점유율을 차지하고 있으며 캐나다와 멕시코는 액세스 프로그램 확대와 진단 능력 향상을 통해 지역 성장에 크게 기여하고 있습니다.

유럽은 두 번째로 큰 지역 시장이며, 진보된 신경병성 통증 치료에 대한 접근을 용이하게 하는 강력한 건강 관리 시스템과 종합적인 상환의 틀을 특징으로 합니다. 이 지역 시장 역학은 효능 비교와 비용 효과를 중시하는 엄격한 의료 기술 평가 프로세스에 의해 형성되며 기존의 선택에 대한 우위가 입증된 치료에 대한 수요를 촉진하고 있습니다. 영국과 독일은 혁신적인 치료법의 채택으로 선도하고 있지만, 프랑스, 이탈리아, 스페인은 환자 수가 많아 통증 관리 인프라가 확립되어 큰 시장 점유율을 유지하고 있습니다. 첨단 척수 자극 시스템을 포함한 유럽에서 최근 승인된 새로운 치료법 및 장치는 이 지역의 메드트로닉 환자의 치료 옵션 확장에 대한 노력을 반영합니다.

아시아태평양은 CAGR 12.37%(2025-2030년)로 가장 급성장하고 있는 지역 시장으로, 질병 유병률 증가, 헬스케어 액세스의 개선, 헬스케어 지출 증가가 그 원동력이 되고 있습니다. 중국은 보험 적용 범위 확대와 건강 관리 인프라에 대한 많은 투자로 지역 성장을 이끌고 있으며, 일본은 선진 건강 관리 시스템과 고령화 사회에 의한 높은 신경 인성 통증 유병률로 큰 시장 점유율을 차지하고 있습니다. 인도는 당뇨병 인구의 많음과 진단 능력의 향상으로 주요 성장 시장으로 대두되고 있지만, 농촌에서는 접근의 과제가 남아 있습니다. 이 지역에서는 전통적인 치료법과 병행하여 전통 의학 접근법의 채택이 증가하고 있으며 최근의 조사는 중국 전통 의학 치료의 잠재력을 강조하고 있습니다. 한국시장은 급속한 기술 도입과 강력한 의약품 연구능력을 특징으로 하며 지역의 혁신에 공헌하고 있습니다. 중동, 아프리카 및 남미 지역은 건강 관리 인프라 개선과 질병에 대한 의식 증가로 인해 규모는 작지만 성장하는 시장입니다.

The Neuropathic Pain Market size is estimated at USD 8.00 billion in 2025, and is expected to reach USD 12.73 billion by 2030, at a CAGR of 9.74% during the forecast period (2025-2030).

Escalating prevalence of diabetes, cancer survivorship and viral infections is enlarging the treated population, while regulators, payers and clinicians increasingly favour non-opioid options that lower abuse risk. Evidence from real-world prescription audits shows a steady shift away from centrally acting painkillers toward peripherally selective agents, hinting at a structural rebalancing of Neuropathic Pain market share. Pipeline diversity spanning small-molecule sodium-channel blockers, biologic nerve-growth-factor antagonists and advanced topical formulations underscores commercial confidence in mechanism-based differentiation. An additional observation is that the fastest uptake is occurring in provider settings able to measure functional gains, suggesting that outcome-linked reimbursement is already shaping treatment choices.

The escalating global diabetes epidemic is fundamentally reshaping the neuropathic pain landscape, with diabetic peripheral neuropathy (DPN) affecting approximately 50% of diabetic patients. This high prevalence translates to a substantial patient population requiring effective pain management solutions. Recent epidemiological studies reveal that DPN is often underdiagnosed, with 75% of cases remaining undetected until symptoms become severe, creating a significant untapped market opportunity Elafros et al.. The economic burden of DPN extends beyond direct treatment costs, as patients with painful DPN experience reduced productivity and higher healthcare utilization across multiple specialties, driving demand for more effective and tolerable treatment options that can improve functional outcomes while minimizing side effects.

As cancer treatment efficacy improves, the population of survivors experiencing chemotherapy-induced peripheral neuropathy (CIPN) continues to expand, creating an urgent need for effective management strategies. CIPN affects 30-40% of patients receiving neurotoxic chemotherapy agents, with symptoms often persisting long after treatment completion Dove Press. The condition significantly impacts quality of life and may necessitate chemotherapy dose reductions, potentially compromising oncological outcomes. Recent advances in understanding CIPN pathophysiology have revealed the role of oxidative stress and neuroinflammation, opening new therapeutic avenues beyond traditional analgesics. Biomarker development for early CIPN detection is gaining momentum, with neurotrophic factors and microRNAs showing promise for identifying high-risk patients Widyadharma. This trend could potentially reduce the addressable market for CIPN treatments, as preventive interventions might decrease the incidence of severe cases requiring pharmaceutical management. Pharmaceutical companies face the strategic challenge of balancing innovation in treatment with the market-constraining effects of improved prevention and early intervention strategies.

The clinical utility of traditional neuropathic pain treatments is increasingly constrained by mounting safety concerns and regulatory scrutiny. Opioids, despite their analgesic efficacy, face severe prescribing restrictions due to their high abuse potential and the ongoing public health crisis associated with opioid misuse. Gabapentinoids (pregabalin and gabapentin), while effective for many neuropathic pain conditions, are encountering growing regulatory oversight due to emerging evidence of misuse potential and dependence issues. These safety challenges are driving a fundamental market shift toward treatments with improved risk-benefit profiles. The development of peripherally-acting analgesics that do not cross the blood-brain barrier represents a strategic response to these concerns, offering pain relief without central nervous system effects that contribute to abuse potential NIH. This safety-driven market evolution is creating opportunities for novel therapeutic approaches that can maintain efficacy while addressing the limitations of current standard-of-care treatments.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Anticonvulsants command the largest market share at 33.50% in 2024, with pregabalin and gabapentin serving as cornerstone therapies due to their established efficacy across multiple neuropathic pain conditions. Their mechanism of action, primarily involving calcium channel modulation and enhanced GABA activity, effectively addresses the hyperexcitability that characterizes neuropathic pain states. Recent comparative analyses reveal that pregabalin demonstrates superior pain reduction and fewer adverse events compared to gabapentin, potentially explaining its growing preference among clinicians Mayoral et al.. Despite their dominance, anticonvulsants face challenges from emerging drug classes with potentially superior safety profiles and more targeted mechanisms. Topical agents represent the fastest-growing segment with a 10.10% CAGR (2025-2030), driven by their favorable risk-benefit profile, particularly for localized neuropathic pain. SNRIs maintain significant market presence due to duloxetine's established efficacy in diabetic peripheral neuropathy, while opioids face declining utilization amid safety concerns and regulatory restrictions. The "Other Classes" segment, including NMDA antagonists and cannabinoids, shows promising growth potential as research advances on novel mechanisms targeting neuropathic pain pathways.

The competitive dynamics within drug classes are evolving as pharmaceutical companies strategically reposition their portfolios toward differentiated mechanisms. Emerging evidence suggests that combination approaches targeting multiple pain pathways simultaneously may offer superior outcomes compared to monotherapy, potentially reshaping treatment algorithms Kumar et al.. This trend is driving increased interest in rational polypharmacy and fixed-dose combinations that can address the complex pathophysiology of neuropathic pain while minimizing individual drug side effects. The recent approval of novel agents like suzetrigine signals a potential paradigm shift toward mechanism-based prescribing rather than the current symptom-based approach, which could fundamentally alter market share distribution across drug classes in the coming years.

Diabetic peripheral neuropathy (DPN) dominates the indication landscape with 32.30% market share in 2024, reflecting its high prevalence among the growing diabetic population worldwide. The condition affects approximately 50% of patients with diabetes duration exceeding 10 years, creating a substantial and expanding patient pool. Treatment approaches for DPN are evolving beyond symptom management to address underlying pathophysiological mechanisms, with increasing focus on disease-modifying therapies that can prevent or slow neuropathy progression. Chemotherapy-induced peripheral neuropathy (CIPN) represents the fastest-growing indication segment with an 11.56% CAGR (2025-2030), driven by improving cancer survival rates and growing recognition of CIPN's impact on quality of life. Postherpetic neuralgia maintains significant market share due to its distinctive pathophysiology and treatment challenges, while trigeminal neuralgia represents a smaller but therapeutically distinct segment with specific treatment algorithms.

The indication landscape is being reshaped by advances in diagnostic capabilities and biomarker development that enable earlier intervention and more precise patient stratification. Recent research has identified potential biomarkers for CIPN, including neurotrophic factors and microRNAs, which could facilitate preventive strategies in high-risk patients Widyadharma. For HIV-associated neuropathy, antiretroviral therapy optimization is increasingly recognized as a critical component of management alongside direct pain interventions. Phantom limb pain is benefiting from innovative approaches, including the FDA-approved Altius Direct Electrical Nerve Stimulation System, which demonstrated significant pain reduction in clinical studies FDA. These advances in indication-specific approaches are driving market segmentation and creating opportunities for targeted therapies that address the unique pathophysiological features of each neuropathic pain condition.

The Neuropathic Pain Market Report Segments the Industry Into by Drug Class (Anticonvulsants, Tricyclic Antidepressants, and More), by Indication (Diabetic Peripheral Neuropathy, Postherpetic Neuralgia and More), by Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America dominates the neuropathic pain market with 42.50% share in 2024, driven by high disease prevalence, advanced healthcare infrastructure, and favorable reimbursement policies. The region's leadership position is reinforced by its role as the primary launch market for innovative therapies, exemplified by the recent FDA approval of Journavx (suzetrigine) as the first new analgesic class in over two decades FDA. The implementation of the NOPAIN Act represents a significant policy advancement, creating reimbursement pathways specifically for non-opioid pain management in outpatient settings Vertex Pharmaceuticals. This regulatory tailwind is expected to accelerate market access for novel neuropathic pain therapies, particularly those with demonstrated advantages over existing options. The United States accounts for the largest share within North America, reflecting its substantial patient population and high healthcare expenditure, while Canada and Mexico contribute significantly to regional growth through expanding access programs and improving diagnostic capabilities.

Europe represents the second-largest regional market, characterized by strong healthcare systems and comprehensive reimbursement frameworks that facilitate access to advanced neuropathic pain therapies. The region's market dynamics are shaped by stringent health technology assessment processes that emphasize comparative effectiveness and cost-utility, driving demand for treatments with demonstrable advantages over existing options. The United Kingdom and Germany lead in adoption of innovative therapies, while France, Italy, and Spain maintain substantial market shares due to their large patient populations and established pain management infrastructure. Recent European approvals of novel treatments and devices, including advanced spinal cord stimulation systems, reflect the region's commitment to expanding therapeutic options for neuropathic pain patients Medtronic.

Asia-Pacific represents the fastest-growing regional market with a 12.37% CAGR (2025-2030), driven by increasing disease prevalence, improving healthcare access, and rising healthcare expenditure. China leads regional growth with expanding insurance coverage and significant investments in healthcare infrastructure, while Japan contributes substantial market share through its advanced healthcare system and aging population with high neuropathic pain prevalence. India is emerging as a key growth market due to its large diabetic population and improving diagnostic capabilities, though access challenges persist in rural areas. The region is witnessing increasing adoption of traditional medicine approaches alongside conventional therapies, with recent research highlighting the potential of traditional Chinese medicine in treating neuropathic pain Zhang et al.. South Korea's market is characterized by rapid technology adoption and strong pharmaceutical research capabilities, contributing to regional innovation. The Middle East & Africa and South America regions represent smaller but growing markets, with improving healthcare infrastructure and increasing disease awareness driving expansion from a lower base.