Military Platforms Market by Type (Fighter, Transport, Special Mission, Helicopter, MBT, APC, IFV, MRAP, Aircraft Carrier, Destroyer, Submarine, Corvette, Frigate, Patrol Vessel), Technology (Legacy, Next-Gen), Customer, Region - Global Forecast To 2032

상품코드:1963144

리서치사:MarketsandMarkets

발행일:2026년 02월

페이지 정보:영문 466 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

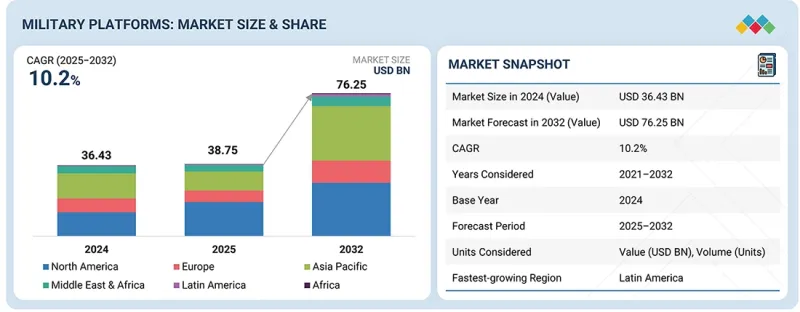

세계의 군용 플랫폼 시장 규모는 2025년 387억 5,000만 달러에서 2032년까지 약 762억 5,000만 달러에 달할 것으로 예측되며, 예측 기간 동안 CAGR로 약 10.2%의 성장이 전망됩니다.

조사 범위

조사 대상 기간

2021-2032년

기준 연도

2024년

예측 기간

2025-2032년

단위

10억 달러

부문

유형, 기술, 지역

대상 지역

북미, 유럽, 아시아태평양, 기타 지역

시장 성장은 주로 진행 중인 국방 현대화 활동, 노후화된 육상, 해상 및 항공 플랫폼의 갱신, 고성능 군용 시스템에 대한 지속적인 투자에 의해 촉진되고 있습니다. 함대의 급속한 확장보다는 플랫폼의 복잡성, 단가 상승, 주요 방위군 전반의 첨단 임무 시스템, 생존성 기능, 상호운용성 요구사항의 통합이 성장을 주도하고 있습니다.

"유형별로는 군용 선박이 예측 기간 동안 가장 높은 성장률을 보일 것으로 예상합니다."

해상 보안, 해안 감시, 배타적 경제수역(EEZ) 보호에 대한 관심이 높아짐에 따라 군용 순찰선이 플랫폼 카테고리 중 가장 빠른 성장세를 기록할 것으로 예상됩니다. 해군은 비대칭 위협, 해상 국경 단속, 해적 행위, 밀수, 회색지대 작전에 대응하기 위해 해안 순찰선, 고속 순찰선, 해안 경비 플랫폼에 대한 우선순위를 점점 더 높이고 있습니다.

대형 수상전투함에 비해 초계함은 건조 기간이 짧고, 조달 및 운영 비용이 낮으며, 작전 가용성이 높아 함대를 빠르게 확장하는 데 유리합니다. 특히 신흥 해군 세력들은 고가의 주력함의 재정적, 병참적 부담 없이 해상 존재감을 강화하기 위해 초계함에 대한 투자를 가속화하고 있습니다. 이러한 운영상의 중요성, 경제성, 확장성의 조합은 순찰선의 강력한 성장 전망을 뒷받침하고 있습니다.

"기술별로는 구식 플랫폼이 예측 기간 동안 가장 큰 시장 점유율을 차지할 것으로 예상됩니다."

구식 군용 플랫폼은 광범위한 배치, 운영 성숙도, 확립된 산업 생태계에 힘입어 시장에서 가장 큰 점유율을 유지할 것으로 예상됩니다. 국방 기관은 검증된 성능, 예측 가능한 수명주기 비용, 기존 인프라 및 독트린과의 호환성 때문에 구식 항공기, 차량, 함정에 계속 의존하고 있습니다. 이 부문의 지출은 근본적인 재설계보다는 주로 항공전자 업그레이드, 추진 시스템 개선, 구조 보강, 임무 시스템 강화 등 단계적인 현대화에 사용됩니다. 구식 플랫폼은 견고한 세계 공급망과 장기적인 유지보수 프레임워크의 혜택을 받아 기술적 리스크를 줄이고 높은 가동률을 보장합니다. 차세대 첨단 플랫폼이 전략적 주목을 받고 있지만, 구식 시스템은 여전히 즉각적인 대응태세와 전력 연속성 유지에 핵심적인 역할을 담당하고 있으며, 전체 군용 플랫폼 시장에서 지배적인 위치를 확고히 하고 있습니다.

"라틴아메리카가 예측 기간 동안 가장 높은 성장률을 보일 것으로 예상됩니다."

라틴아메리카는 상대적으로 낮은 수준에서 국방 투자가 증가하고 함대 갱신 및 현대화에 대한 관심이 높아짐에 따라 2025-2032년 군용 플랫폼 시장에서 가장 빠른 성장세를 기록할 것으로 예상됩니다. 이 지역의 성장은 작전 준비태세를 개선하고 기존 자산의 수명을 연장하기 위한 군용 차량, 항공기, 해상 플랫폼의 선택적 조달에 의해 뒷받침되고 있습니다. 대규모 방산 시장과 비교했을 때 전체 플랫폼의 규모는 여전히 제한적이지만, 지출 강도의 증가와 현대화가 주도하는 조달로 인해 지역 전체에서 금액 성장, 부문 간 운영상의 채택, 무인화 역량 개발에 대한 정부의 강력한 강조가 촉진되고 있습니다.

세계의 군용 플랫폼 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도 등의 정보를 전해드립니다.

목차

제1장 소개

제2장 주요 요약

제3장 중요한 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 고객 상황과 구매 행동

제7장 지속가능성과 규제 상황

제8장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 용도

제9장 군용 플랫폼 시장 : 플랫폼 유형별

제10장 군용 플랫폼 시장 : 고객별

제11장 군용 플랫폼 시장 : 기술별

제12장 군용 플랫폼 시장 : 지역별

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

KSM

영문 목차

영문목차

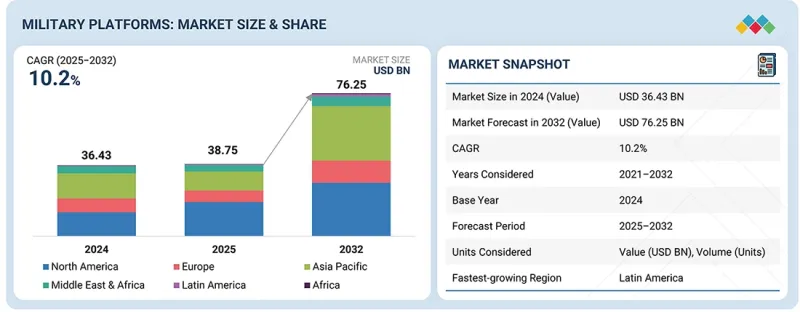

The military platforms market is projected to grow from USD 38.75 billion in 2025 to around USD 76.25 billion by 2032, registering a CAGR of about 10.2% during the forecast period.

Scope of the Report

Years Considered for the Study

2021-2032

Base Year

2024

Forecast Period

2025-2032

Units Considered

Value (USD Billion)

Segments

By Type, Technology and Region

Regions covered

North America, Europe, APAC, RoW

Market growth is largely driven by ongoing defense modernization efforts, replacement of aging land, naval, and air platforms, and sustained investment in higher-capability military systems. Rather than rapid fleet expansion, growth is being shaped by increasing platform complexity, higher unit costs, and the integration of advanced mission systems, survivability features, and interoperability requirements across major defense forces.

"By type, military vessels are projected to grow at the highest rate during the forecast period."

Military patrol vessels are expected to register the fastest growth among platform categories, driven by the rising emphasis on maritime security, coastal surveillance, and protection of exclusive economic zones. Navies are increasingly prioritizing offshore patrol vessels, fast patrol craft, and coastal security platforms to address asymmetric threats, maritime border enforcement, piracy, smuggling, and grey-zone operations.

Compared to larger surface combatants, patrol vessels offer shorter construction timelines, lower acquisition and operating costs, and higher operational availability, making them attractive for rapid fleet expansion. Emerging naval forces, in particular, are accelerating investments in patrol vessels to strengthen maritime presence without the financial and logistical burden of high-end warships. This combination of operational relevance, affordability, and scalability underpins the strong growth outlook for patrol vessels.

"By technology, legacy platforms are expected to account for the largest market share during the forecast period."

Legacy military platforms are projected to maintain the largest share of the market, supported by their widespread deployment, operational maturity, and well-established industrial ecosystems. Defense forces continue to rely heavily on legacy aircraft, vehicles, and vessels due to their proven performance, predictable lifecycle costs, and compatibility with existing infrastructure and doctrine. Spending in this segment is largely directed toward incremental modernization, including avionics upgrades, propulsion improvements, structural reinforcements, and enhanced mission systems, rather than radical redesigns. Legacy platforms also benefit from robust global supply chains and long-term sustainment frameworks, reducing technical risk and ensuring high availability. While next-generation and advanced platforms are gaining strategic attention, legacy systems remain central to maintaining readiness and force continuity, securing their dominant position within the overall military platforms market.

"Latin America is projected to grow at the highest rate during the forecast period."

Latin America is expected to register the fastest growth in the military platforms market between 2025 and 2032, driven by rising defense investments from a relatively low base and an increasing focus on fleet replacement and modernization. Growth in the region is supported by selective procurement of military vehicles, aircraft, and naval platforms aimed at improving operational readiness and extending the service life of existing assets. While overall platform volumes remain limited compared to larger defense markets, higher spending intensity and modernization-led procurement are driving strong value growth across the region, cross-sector operational adoption, and strong government emphasis on unmanned capability development

Research Coverage:

This market study covers the military platforms market across various segments and subsegments. It aims to estimate the size and growth potential of this market across different parts and regions. This study also includes an in-depth competitive analysis of the key players in the market, their company profiles, key observations related to their products and business offerings, recent developments, and key market strategies they adopted.

Reasons to buy this report:

The report will help the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall military platforms market. It will also help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report will also help stakeholders understand the market pulse and will provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

Market Drivers (Sustained defense modernization programs, Replacement of aging military fleets, Rising focus on multi-domain operations, Increasing investment in advanced platform capabilities), Restraints (High procurement and lifestyle costs, Long development and production timelines, Budgetary and fiscal constraints, Dependence on specialized suppliers and workforce), Opportunities (Fleet upgrades and life-extension programs, Demand for next-generation platforms, Growth in emerging defense markets, Integration of advanced digital and mission systems), Challenges (Complex procurement and approval processes, Program execution and delivery risks, Geopolitical uncertainty and policy shifts, Balancing modernization and fleet availability)

Market Penetration: Comprehensive information on military vessels, aircraft, and vehicles offered by the top players in the market

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product launches in the market

Market Development: Comprehensive information about lucrative markets across varied regions

Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the market

Competitive Assessment: In-depth assessment of market share, growth strategies, products, and manufacturing capabilities of leading players in the market

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.2.1 MILITARY AIRCRAFT

1.2.2 MILITARY VESSELS

1.2.3 MILITARY VEHICLES

1.3 STUDY SCOPE

1.3.1 MARKET SEGMENTATION

1.3.2 INCLUSIONS AND EXCLUSIONS

1.4 YEARS CONSIDERED

1.5 CURRENCY CONSIDERED

1.6 STAKEHOLDERS

1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

2.3 DISRUPTIVE TRENDS SHAPING MARKET

2.4 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS

2.5 GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN MILITARY PLATFORMS MARKET

3.2 MILITARY PLATFORMS MARKET, BY TYPE

3.3 MILITARY PLATFORMS MARKET, BY TECHNOLOGY

3.4 MILITARY PLATFORMS MARKET, BY CUSTOMER

4 MARKET OVERVIEW

4.1 INTRODUCTION

4.2 MARKET DYNAMICS

4.2.1 DRIVERS

4.2.1.1 Sustained defense modernization programs

4.2.1.2 Replacement of aging military fleets

4.2.1.3 Rising focus on multi-domain operations

4.2.1.4 Increasing investment in advanced platform capabilities

4.2.2 RESTRAINTS

4.2.2.1 High procurement and lifecycle costs

4.2.2.2 Long development timelines and cost overruns

4.2.2.3 Dependence on specialized suppliers and workforce

4.2.3 OPPORTUNITIES

4.2.3.1 Fleet upgrades and life extension programs

4.2.3.2 Demand for next-generation platforms

4.2.3.3 Growth in emerging defense markets

4.2.3.4 Integration of advanced digital and mission systems

4.2.4 CHALLENGES

4.2.4.1 Complex procurement and approval processes

4.2.4.2 Program execution and delivery risks

4.2.4.3 Geopolitical uncertainty and policy shifts

4.2.4.4 Balancing modernization and fleet availability

4.3 UNMET NEEDS AND WHITE SPACES

4.3.1 LIMITED UPGRADE AGILITY AND MODULAR INTEGRATION

4.3.2 INDUSTRIAL SCALABILITY AND SURGE PRODUCTION CAPABILITY

4.3.3 LIFECYCLE AVAILABILITY AND SUSTAINMENT FLEXIBILITY

4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

4.4.1 CIVIL AEROSPACE AND COMMERCIAL AVIATION

4.4.2 LAND TRANSPORT, HEAVY INDUSTRIAL, AND AUTOMOTIVE SYSTEMS

4.4.3 MARITIME COMMERCIAL SHIPBUILDING AND OFFSHORE INFRASTRUCTURE

4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

4.6 TOTAL COST OF OWNERSHIP

4.6.1 TOTAL COST OF OWNERSHIP OF MILITARY VESSELS

4.6.1.1 Acquisition costs

4.6.1.2 Operating costs

4.6.1.3 Downtime and disruption costs

4.6.1.4 Lifecycle extension costs

4.6.1.5 End-of-life costs

4.6.1.6 Risk management costs

4.6.1.7 Opportunity costs

4.6.2 TOTAL COST OF OWNERSHIP OF MILITARY VEHICLES

4.6.3 TOTAL COST OF OWNERSHIP OF MILITARY AIRCRAFT