데이터센터 네트워킹 시장 예측(-2031년) : 오퍼링별, 네트워크 인프라별, 소프트웨어별, 서비스별, 워크로드 유형별, 데이터센터 규모·용량별, 최종사용자별, 지역별

Data Center Networking Market by Offering (Network Infrastructure, Software), Network Infrastructure (Switches, Routers, NICs & Offload, AI/HPC Hardware), Workload (AI & HPC, General IT), Data Center Size, End User, and Region - Forecast to 2031

상품코드:1961004

리서치사:MarketsandMarkets

발행일:2026년 02월

페이지 정보:영문 415 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

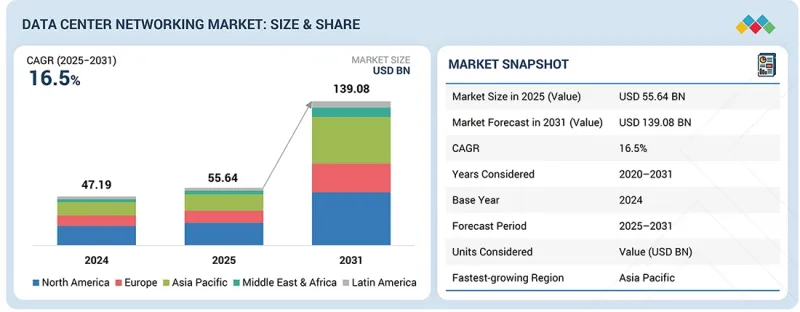

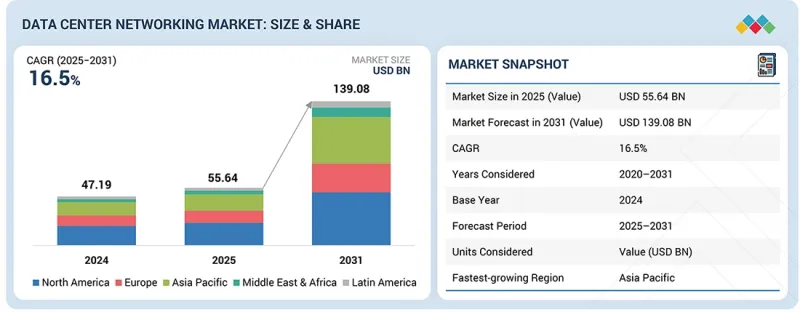

데이터센터 네트워킹 시장 규모는 급속히 확대하고 있으며, 시장 규모는 2025년 556억 4,000만 달러에서 2031년까지 1,390억 8,000만 달러로, CAGR 16.5%로 성장할 것으로 예측되고 있습니다.

AI 트레이닝 클러스터, AI 모델 생성, GPU 고밀도 컴퓨팅 환경의 도입이 가속화되면서 고성능 스위칭, 라우팅, 오프로드 하드웨어에 대한 수요가 크게 증가하고 있습니다. 조직은 방대한 동서방향 트래픽과 확장 가능한 클라우드 환경을 지원하기 위해 400G 및 800G 기술을 통해 네트워크 아키텍처를 현대화하고 있습니다.

하이퍼스케일 사업자가 용량을 확장하고 기업이 하이브리드 클라우드 및 멀티 클라우드 전략을 채택함에 따라 네트워크 패브릭은 결정론적 성능, 자동화, 고급 보안 기능을 제공해야 합니다. 소프트웨어 정의 네트워크, 자동화 플랫폼, 프로그래머블 네트워크 운영체제의 통합으로 확장성과 운영 효율성이 더욱 향상됩니다. AI 인프라, 소버린 클라우드 구상, 대규모 데이터센터 캠퍼스에 대한 투자 확대는 전 세계에서 강력하고 빠른 데이터센터 네트워크 솔루션에 대한 수요를 강화시키고 있습니다.

네트워크 관리, 자동화 및 가시성 소프트웨어는 네트워크의 복잡성 증가와 대규모 AI 인프라 도입의 진전에 따라 데이터센터 네트워킹 시장에서 가장 빠르게 성장하는 소프트웨어 분야가 될 것으로 예측됩니다. 하이퍼스케일 데이터센터가 확장되고 기업의 멀티 클라우드 하이브리드 아키텍처 도입이 확대되는 가운데, 400G, 800G 이상의 고속 패브릭을 운영하기 위해서는 첨단 자동화와 실시간 가시성이 필수적입니다. 이 플랫폼은 분산된 환경 전반에서 중앙 집중식 관리, 제로 터치 프로비저닝, 지능형 구성 관리, 지속적인 원격 모니터링이 가능합니다. AI 클러스터와 동서방향 트래픽의 급격한 성장에 따라 다운타임 최소화, 혼잡 감지, 성능 최적화를 위해 실시간 가시성 및 예측 분석이 필수적입니다. 자동화 툴은 또한 수동 개입 감소, 운영 비용 절감, 네트워크 안정성 향상에 기여합니다. 조직이 확장성, 탄력성, 운영 효율성을 우선시하는 가운데, 고급 네트워크 자동화 및 가시성 솔루션에 대한 수요는 계속 가속화되고 있으며, 이 분야는 데이터센터 네트워크 시장에서 가장 빠르게 성장하는 소프트웨어 카테고리로 자리매김하고 있습니다.

네트워크 인프라 부문은 고성능 스위칭, 라우팅, 오프로드 하드웨어에 대한 지속적인 투자에 힘입어 데이터센터 네트워크 시장에서 가장 큰 비중을 차지할 것으로 예측됩니다. 하이퍼스케일 데이터센터가 확장되고 AI 워크로드가 빠르게 확장됨에 따라 고급 이더넷 및 InfiniBand 스위치, 대용량 라우터, 지능형 NIC 및 DPU에 대한 수요는 계속 증가하고 있습니다. 이러한 하드웨어 구성 요소는 현대 데이터센터 아키텍처의 핵심으로, 클라우드, 기업, AI 환경을 가로지르는 고속의 동서 및 남북 트래픽 흐름을 실현합니다. 400G 및 800G 기술로의 전환과 GPU 고밀도 클러스터의 도입은 물리적 네트워크 인프라에 대한 자본 지출을 크게 증가시키고 있습니다. 또한 레거시 10G 및 40G 시스템의 지속적인 업데이트 주기가 하드웨어 수요를 더욱 강화하고 있습니다. 성능, 확장성, 안정성을 보장하는 데 중요한 역할을 하는 네트워크 인프라는 전체 데이터센터 네트워크 시장에서 가장 높은 매출을 창출하는 제품군으로 여전히 지배적인 위치를 차지하고 있습니다.

북미는 하이퍼스케일 클라우드 프로바이더의 강력한 존재감, 첨단 디지털 인프라, 고속 네트워크 기술의 조기 도입으로 데이터센터 네트워크 시장에서 가장 큰 점유율을 유지할 것으로 예측됩니다. 이 지역에는 대규모 데이터센터와 AI 트레이닝 시설이 집중되어 있으며, 400G/800G 스위칭, InfiniBand 패브릭, 고급 네트워크 인터페이스 장비에 대한 막대한 투자를 주도하고 있습니다. 성숙한 광섬유 연결 환경, 주요 기업의 강력한 설비 투자, 지속적인 클라우드 확장이 그 우위를 더욱 강화하고 있습니다.

그러나 예측 기간 중 가장 빠른 성장이 예상되는 지역은 아시아태평양입니다. 중국, 인도, 일본, 동남아시아의 급속한 디지털 전환, 클라우드 배포 증가, 정부 주도의 데이터 현지화 정책, AI 인프라에 대한 대규모 투자로 네트워크 인프라 구축이 가속화되고 있습니다. 이 지역 전체에서 하이퍼스케일 캠퍼스 및 소버린 클라우드 프로젝트가 확대되면서 고성능 데이터센터 네트워크 솔루션에 대한 수요가 크게 증가하고 있습니다.

이 보고서에는 데이터센터 네트워킹 시장에서 활동하는 주요 기업에 대한 상세한 조사가 포함되어 있습니다. 조사 대상 주요 시장 참여 기업 : NVIDIA Corporation(미국), Cisco Systems, Inc.(미국), Arista Networks, Inc.(미국), Huawei Technologies(중국), Hewlett Packard Enterprise Company(미국), Nokia Corporation(핀란드), Marvell Technology, Inc.(미국), H3C Technologies(중국), Dell Technologies Inc.(미국), Accton Technology Corporation(대만), Extreme Networks, Inc.(미국), Ruijie Network(중국), Alcatel-Lucent Enterprise(프랑스), Celestica Inc.(캐나다), Intel Corporation(미국), AMD(미국), Quanta Cloud Technology Inc.(대만), Delta Electronics, Inc.(대만), Palo Alto Networks, Inc.(미국), Foxconn(대만), Fortinet, Inc.(미국), Napatech(덴마크), Arrcus, Inc.(미국), Alkira, Inc.(미국), Aviz Networks, Inc(미국).

이 보고서의 조사 범위에는 데이터센터 네트워크 시장을 형성하는 성장 요인, 저해요인, 과제, 성장 기회 등 시장 성장에 영향을 미치는 주요 요인에 대한 상세한 정보가 포함되어 있습니다. 데이터센터 네트워크 시장의 주요 기업 개요, 사업 개요, 제품 포트폴리오, 기술 제공, 전략적 접근, 제휴 및 계약, 제품 출시, 인수합병, 데이터센터 네트워크 시장의 최근 동향에 대한 종합적인 분석 정보를 전해드립니다.

이 보고서 구매 이유

이 보고서는 시장 리더와 신규 진출기업에게 전체 데이터센터 네트워킹 시장과 그 하위 부문의 매출 수치에 대한 가장 정확한 근사치를 제공합니다. 이해관계자들이 경쟁 구도를 이해하고, 비즈니스 포지셔닝을 개선하고, 적절한 시장 진출 전략을 수립하기 위한 인사이트을 키울 수 있도록 돕습니다. 또한 시장 동향을 파악하고 주요 촉진요인, 억제요인, 과제, 기회에 대한 정보를 제공합니다.

이 보고서는 다음 사항에 대한 인사이트을 제공

이 보고서는 데이터센터 네트워킹 시장을 형성하는 주요 시장 성장 촉진요인, 저해요인, 기회 및 과제에 대한 인사이트을 제공합니다. 주요 시장 성장 촉진요인으로는 하이퍼스케일 용량 확장, AI 및 HPC 워크로드의 급격한 성장, 데이터 트래픽 증가, 400G/800G 및 InfiniBand 기반 패브릭의 채택 확대 등이 있습니다. 상호운용성 제한, 벤더 종속 우려, 전력망 제약, 높은 자본 지출 요건 등을 들 수 있습니다. 기회는 AI 클러스터의 확장, 스마트한 오프로드 기능을 갖춘 스위칭 플랫폼, 가상화, 소프트웨어 정의 네트워크(SDN)의 채택에서 비롯됩니다. 주요 과제로는 부품 공급의 제약, 장비의 리드타임 연장, 전력 인프라의 지연, 네트워크의 복잡성 증가 등을 들 수 있으며, 이 모든 것에 대해 첨단 자동화 및 가시성 솔루션이 요구되고 있습니다.

제품 개발/혁신 : 데이터센터 및 네트워킹 시장의 차세대 기술, R&D 활동, 제품 및 서비스 출시에 대한 심층적인 인사이트을 제공합니다.

시장 개발: 수익성 높은 시장에 대한 종합적인 정보 - 이 보고서는 다양한 지역의 데이터센터 및 네트워킹 시장을 분석합니다.

시장 다각화 : 데이터센터 및 네트워킹 시장의 신제품 및 서비스, 미개발 지역, 최근 동향, 투자에 대한 종합적인 정보 제공

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 고객 상황과 구매 행동

제7장 규제 상황

제8장 기술, 특허, 디지털, AI의 도입에 의한 전략적 파괴

제9장 데이터센터 네트워킹 시장(오퍼링별)

제10장 데이터센터 네트워킹 시장(네트워크 인프라별)

제11장 데이터센터 네트워킹 시장(소프트웨어별)

제12장 데이터센터 네트워킹 시장(서비스별)

제13장 데이터센터 네트워킹 시장(워크로드 유형별)

제14장 데이터센터 네트워킹 시장(데이터센터 규모·용량별)

제15장 데이터센터 네트워킹 시장(최종사용자별)

제16장 데이터센터 네트워킹 시장(지역별)

제17장 경쟁 구도

제18장 기업 개요

제19장 조사 방법

제20장 부록

KSA

영문 목차

영문목차

The data center networking market is expanding rapidly, with the market projected to grow from USD 55.64 billion in 2025 to USD 139.08 billion by 2031, at a CAGR of 16.5%.

Scope of the Report

Years Considered for the Study

2020-2031

Base Year

2024

Forecast Period

2025-2031

Units Considered

USD (Billion)

Segments

By Offering, Network Infrastructure Type, Software, Service, Workload Type, Data Center Size & Capacity, End User, Region

Regions covered

North America, Europe, Asia Pacific, Middle East & Africa, Latin America

The accelerating deployment of AI training clusters, generative AI models, and GPU-dense computing environments is significantly increasing demand for high-performance switching, routing, and offload hardware. Organizations are modernizing their network architectures with 400G and 800G technologies to support massive east-west traffic and scalable cloud environments.

As hyperscale operators expand capacity and enterprises adopt hybrid and multi-cloud strategies, network fabrics must deliver deterministic performance, automation, and advanced security capabilities. The integration of software-defined networking, automation platforms, and programmable network operating systems further enhances scalability and operational efficiency. Growing investments in AI infrastructure, sovereign cloud initiatives, and large-scale data center campuses are strengthening demand for resilient, high-speed data center networking solutions worldwide.

"In software, network management, automation & observability software is expected to register the fastest growth during the forecast period."

Network management, automation & observability software is projected to be the fastest-growing software segment in the data center networking market, driven by increasing network complexity and large-scale AI infrastructure deployments. As hyperscale data centers expand and enterprises adopt multi-cloud and hybrid architectures, managing high-speed fabrics operating at 400G, 800G, and beyond requires advanced automation and real-time visibility. These platforms enable centralized control, zero-touch provisioning, intelligent configuration management, and continuous telemetry monitoring across distributed environments. With the rapid growth of AI clusters and east-west traffic, real-time observability and predictive analytics have become critical for minimizing downtime, detecting congestion, and optimizing performance. Automation tools also help reduce manual intervention, lower operational costs, and improve network reliability. As organizations prioritize scalability, resilience, and operational efficiency, demand for advanced network automation and observability solutions continues to accelerate, positioning this segment as the fastest-growing software category within the data center networking market.

"By offering, the solutions segment is expected to hold the largest market share during the forecast period"

The network infrastructure segment is projected to account for the largest share of the data center networking market, driven by continuous investments in high-performance switching, routing, and offload hardware. As hyperscale data centers expand and AI workloads scale rapidly, demand for advanced Ethernet and InfiniBand switches, high-capacity routers, and intelligent NICs and DPUs continues to rise. These hardware components form the core backbone of modern data center architectures, enabling high-speed east-west and north-south traffic flow across cloud, enterprise, and AI environments. The transition to 400G and 800G technologies, along with the deployment of GPU-dense clusters, significantly increases capital expenditure on physical network infrastructure. Additionally, ongoing refresh cycles from legacy 10G and 40G systems further strengthen hardware demand. Given its critical role in ensuring performance, scalability, and reliability, network infrastructure remains the dominant and highest-revenue-generating offering in the overall data center networking market.

"North America leads the data center networking market, while Asia Pacific is the fastest-growing region driven by rapid hyperscale expansion and AI infrastructure investments."

North America is expected to hold the largest share of the data center networking market due to the strong presence of hyperscale cloud providers, advanced digital infrastructure, and early adoption of high-speed networking technologies. The region hosts a high concentration of large-scale data centers and AI training facilities, driving significant investments in 400G and 800G switching, InfiniBand fabrics, and advanced network interface hardware. Mature fiber connectivity, strong capital expenditure by leading technology companies, and ongoing cloud expansion continue to reinforce its dominant position.

Asia Pacific, however, is projected to be the fastest-growing region during the forecast period. Rapid digital transformation, increasing cloud adoption, government-backed data localization initiatives, and large-scale investments in AI infrastructure across China, India, Japan, and Southeast Asia are accelerating network infrastructure deployments. The expansion of hyperscale campuses and sovereign cloud projects across the region is significantly boosting demand for high-performance data center networking solutions.

Breakdown of Primaries

In-depth interviews were conducted with Chief Executive Officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the data center networking market.

By Company: Tier I - 27%, Tier II - 37%, and Tier III - 36%

By Designation: C-Level Executives - 29%, D-Level Executives -36%, and Others - 35%

By Region: North America - 35%, Europe - 19%, Asia Pacific - 26%, and RoW - 20%

The report includes a detailed study of key players operating in the data center networking market. The major market participants covered in the study include NVIDIA Corporation (US), Cisco Systems, Inc. (US), Arista Networks, Inc. (US), Huawei Technologies Co., Ltd. (China), Hewlett Packard Enterprise Company (US), Nokia Corporation (Finland), Marvell Technology, Inc. (US), H3C Technologies Co., Ltd. (China), Dell Technologies Inc. (US), Accton Technology Corporation (Taiwan), Extreme Networks, Inc. (US), Ruijie Networks Co., Ltd. (China), Alcatel-Lucent Enterprise (France), Celestica Inc. (Canada), Intel Corporation (US), AMD (US), Quanta Cloud Technology Inc. (Taiwan), Delta Electronics, Inc. (Taiwan), Palo Alto Networks, Inc. (US), Foxconn (Taiwan), Fortinet, Inc. (US), Napatech (Denmark), Arrcus, Inc. (US), Alkira, Inc. (US), and Aviz Networks, Inc. (US).

Research Coverage

This research report categorizes the data center networking market based on Offering (Network Infrastructure, Software, Services), Network Infrastructure Type (Data Center Switches, Data Center Routers, Network Interface & Offload Hardware, AI & HPC Networking Hardware), Port Speed (1-40 Gbps, 40-100 Gbps, 100-400 Gbps, 400 and above), Workload Type (AI & HPC, General-Purpose IT), Data Center Size & Capacity (Small - below 5 MW, Medium - 5-50 MW, Large - above 50 MW), End User (Colocation Data Centers, Hyperscale Data Centers, Enterprise Data Centers), and Region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America).

The report's scope encompasses detailed information regarding the major factors influencing market growth, including drivers, restraints, challenges, and opportunities shaping the data center networking landscape. A comprehensive analysis of key industry players has been conducted to provide insights into their business overview, product portfolios, technology offerings, strategic initiatives, partnerships, agreements, product launches, mergers & acquisitions, and recent developments within the data center networking market.

Reason to Buy this Report

The report would provide market leaders and new entrants with information on the closest approximations of the revenue numbers for the overall data center networking market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. It also helps stakeholders understand the market's pulse and provides information on key drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

The report provides insights into key drivers, restraints, opportunities, and challenges shaping the data center networking market. Major drivers include hyperscale capacity expansion, rapid growth in AI and HPC workloads, rising data traffic, and increasing adoption of 400G/800G and InfiniBand-based fabrics. Restraints include interoperability limitations, vendor lock-in concerns, grid power constraints, and high capital expenditure requirements. Opportunities stem from AI cluster expansion, smart, offload-capable switching platforms, virtualization, and the adoption of software-defined networking. Key challenges include component supply constraints, extended equipment lead times, delays in power infrastructure, and rising network complexity, all of which require advanced automation and observability solutions

Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the data center networking market

Market Development: Comprehensive information about lucrative markets - the report analyzes the data center networking market across varied regions

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the data center networking market

Competitive Assessment: In-depth assessment of market shares, growth strategies and network infrastructure offerings of leading players such as NVIDIA Corporation (US), Cisco Systems, Inc. (US), Arista Networks, Inc. (US), Huawei Technologies Co., Ltd. (China), Hewlett Packard Enterprise Company (US), Nokia Corporation (Finland), Marvell Technology, Inc. (US), H3C Technologies Co., Ltd. (China), Dell Technologies Inc. (US), Accton Technology Corporation (Taiwan), and Extreme Networks, Inc. (US). The report also helps stakeholders understand the data center networking market by providing information on key drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 MARKET SCOPE

1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 LIMITATIONS

1.6 STAKEHOLDERS

1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

2.3 DISRUPTIVE TRENDS IN DATA CENTER NETWORKING MARKET

2.4 HIGH-GROWTH SEGMENTS

2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DATA CENTER NETWORKING MARKET

3.2 DATA CENTER NETWORKING MARKET, BY OFFERING

3.3 DATA CENTER NETWORKING MARKET, BY NETWORK INFRASTRUCTURE

3.4 DATA CENTER NETWORKING MARKET, BY SOFTWARE

3.5 DATA CENTER NETWORKING MARKET, BY SERVICE

3.6 DATA CENTER NETWORKING MARKET, BY DATA CENTER SIZE & CAPACITY

3.7 DATA CENTER NETWORKING MARKET, BY END USER

3.8 DATA CENTER NETWORKING MARKET, BY ENTERPRISE DATA CENTER

4.2.1.2 AI back-end ethernet increasing network spend per cluster

4.2.1.3 High colocation pre-leasing converting capacity commitments into immediate networking demand

4.2.1.4 Increase in data traffic and bandwidth

4.2.2 RESTRAINTS

4.2.2.1 Interoperability limitations and vendor lock-in slowing multi-vendor adoption

4.2.2.2 Grid power constraints limiting the pace of networking expansion

4.2.3 OPPORTUNITIES

4.2.3.1 Higher revenue per deployment through smart, offload-capable switching

4.2.3.2 AI cluster expansion accelerating high-speed fabric adoption

4.2.3.3 Rise in adoption of virtualization technologies to optimize resource utilization

4.2.4 CHALLENGES

4.2.4.1 Power and grid constraints delaying networking deployment timelines

4.2.4.2 Component supply constraints and extended lead times limiting networking equipment availability

4.3 UNMET NEEDS AND WHITE SPACES

4.3.1 UNMET NEEDS IN DATA CENTER NETWORKING MARKET

4.3.2 WHITE SPACE OPPORTUNITIES

4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

4.4.1 INTERCONNECTED MARKETS

4.4.2 CROSS-SECTOR OPPORTUNITIES

4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

4.5.1 EMERGING BUSINESS MODELS

4.5.1.1 Data center networking business models

4.5.2 ECOSYSTEM SHIFTS

4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

5.1 PORTER'S FIVE FORCES ANALYSIS

5.1.1 THREAT OF NEW ENTRANTS

5.1.2 THREAT OF SUBSTITUTES

5.1.3 BARGAINING POWER OF BUYERS

5.1.4 BARGAINING POWER OF SUPPLIERS

5.1.5 INTENSITY OF COMPETITIVE RIVALRY

5.2 MACROECONOMIC INDICATORS

5.2.1 INTRODUCTION

5.2.2 GDP TRENDS & FORECASTS

5.2.3 TRENDS IN GLOBAL DATA CENTER SOLUTIONS INDUSTRY

5.2.4 TRENDS IN GLOBAL SOFTWARE-DEFINED NETWORKING INDUSTRY

5.3 SUPPLY CHAIN ANALYSIS

5.3.1 TECHNOLOGY & INFRASTRUCTURE PROVIDERS

5.3.2 DATA CENTER NETWORKING PROVIDERS

5.3.3 DISTRIBUTORS & RESELLERS

5.3.4 SYSTEM INTEGRATORS & CHANNEL PARTNERS

5.3.5 END USERS

5.4 ECOSYSTEM ANALYSIS

5.5 PRICING ANALYSIS

5.5.1 AVERAGE SELLING PRICE, BY SWITCH TYPE, 2025

5.5.2 INDICATIVE PRICING ANALYSIS OF SWITCHES, BY VENDOR, 2025

5.6 TRADE ANALYSIS

5.6.1 HS CODE: MACHINES FOR THE RECEPTION, CONVERSION, AND TRANSMISSION OR REGENERATION OF VOICE, IMAGES, OR OTHER DATA, INCLUDING SWITCHING AND ROUTING APPARATUS (851762)

5.6.1.1 Export Scenario

5.6.1.2 Import Scenario

5.7 KEY CONFERENCES AND EVENTS, 2026

5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.9 INVESTMENT AND FUNDING SCENARIO

5.10 CASE STUDY ANALYSIS

5.10.1 MODERNIZING DAIMLER'S DATA CENTER NETWORK THROUGH CISCO SDN

5.10.2 COREWEAVE ACCELERATING AI CLOUD PERFORMANCE THROUGH DPU-DRIVEN NETWORKING WITH NVIDIA

5.10.3 COSTAISA ACCELERATING HEALTHCARE IT MODERNIZATION WITH HUAWEI DCN SOLUTIONS

5.10.4 HOT AISLE BUILDING SCALABLE AI CLOUD INFRASTRUCTURE WITH DELL SONIC NETWORKING

5.10.5 MODERNIZING MUNICIPAL INFRASTRUCTURE WITH EXTREME FABRIC CONNECT

5.11 IMPACT OF 2025 US TARIFF - DATA CENTER NETWORKING MARKET

5.11.1 INTRODUCTION

5.11.2 KEY TARIFF RATES

5.11.3 PRICE IMPACT ANALYSIS

5.11.4 IMPACT ON COUNTRY/REGION

5.11.4.1 US

5.11.4.2 Europe

5.11.4.3 Asia Pacific

5.11.5 IMPACT ON END USERS

5.11.5.1 Hyperscale data centers

5.11.5.2 Colocation data centers

5.11.5.3 Enterprise data centers

6 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

6.1 DECISION-MAKING PROCESS

6.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

6.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

6.2.2 BUYING CRITERIA

6.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

6.4 UNMET NEEDS IN VARIOUS END-USER INDUSTRIES

6.5 MARKET PROFITABILITY

6.5.1 REVENUE POTENTIAL

6.5.2 COST DYNAMICS

6.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

7 REGULATORY LANDSCAPE

7.1 REGULATORY LANDSCAPE

7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

7.1.2 INDUSTRY STANDARDS, BY REGION

7.1.2.1 North America

7.1.2.2 Europe

7.1.2.3 Asia Pacific

7.1.2.4 Middle East & Africa

7.1.2.5 Latin America

8 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTION