AI 칩 시장 예측(-2032년) : 컴퓨트별, 메모리별, 네트워크별, 기술별, 기능별, 최종사용자별, 지역별

AI Chip Market By Offerings (GPU, CPU, FPGA, NPU, TPU, Trainium, Inferentia, T-head, Athena ASIC, MTIA, LPU, Memory {DRAM (HBM, DDR)}, Network {NIC/Network Adapters, Interconnects}), Function (Training, Inference), & Region - Global Forecast to 2032

상품코드:1961002

리서치사:MarketsandMarkets

발행일:2025년 12월

페이지 정보:영문 344 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

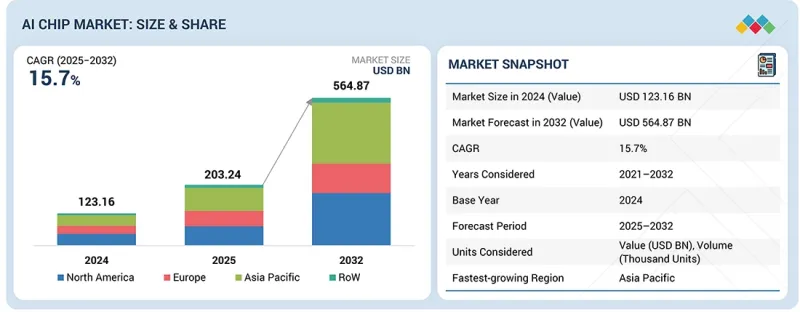

AI 칩 시장 규모는 2025년 2,032억 4,000만 달러에서 2032년까지 5,648억 7,000만 달러로 성장할 것으로 예측되고 있습니다.

2025-2032년 연평균 복합 성장률(CAGR) 15.7%로 확대될 것으로 예측됩니다.

조사 범위

조사 대상 기간

2020-2032년

기준연도

2024년

예측 기간

2025-2032년

대상 단위

금액(10억 달러)

부문

컴퓨팅별, 메모리별, 네트워크별, 기술별, 기능별, 최종사용자별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 기타 지역

신경처리장치(NPU) 부문은 2024-2029년까지 AI 칩 시장에서 높은 성장률을 나타낼 것으로 예측됩니다. 이러한 시장 성장은 엣지단에서 전용 AI 기능을 필요로 하는 하이엔드 스마트폰, AI PC, 노트북의 채택 증가에 기인합니다. NPU는 고급 AI 이미지 처리, 자연 언어 처리 등 AI 기반 작업을 수행하기 위한 신경망 처리를 가속화하는 역할을 합니다. 시장 기업은 경쟁력을 유지하기 위해 하이엔드 NPU 솔루션 개발에 집중하고 있습니다. 예를 들어 2023년 9월 애플(Apple Inc., 미국)은 A17 Pro 칩을 탑재한 아이폰 15 Pro 시리즈를 발표했습니다. 이 신형 AI 프로세서는 전용 16코어 뉴럴 엔진을 탑재해 초당 35조번의 연산 처리(TOPS)를 수행할 수 있습니다. 이러한 중요한 제품 개발 및 발표는 예측 기간 중 시장에서 NPU의 채택 확대에 기여할 것으로 예측됩니다.

AI 칩 시장에서 머신러닝 부문은 큰 시장 점유율을 차지할 것으로 예측됩니다. AI 칩은 학습 및 추론과 같은 머신러닝 작업에 최적화되어 있으며, 예측 분석을 가능하게 하는 대규모 데이터세트 처리와 실시간 의사결정을 지원하는 데 필수적입니다. 이 카테고리의 AI 칩에서 채택을 촉진하는 주요 요인은 자율 시스템내 머신러닝 모델의 유연성과 확장성, 그리고 개인화된 추천이 주요 요인으로 꼽혔습니다. 이 AI 칩은 클라우드 서비스, 의료, 금융, 자동차, 소매 등 다양한 분야에서 널리 활용되고 있습니다. 기업은 비즈니스 인사이트 확보, 고객 경험 개선, 전반적인 효율성 향상을 위한 머신러닝 기능을 지원하는 강력한 AI 칩을 개발하고 있습니다. 예를 들어 구글(미국)은 2024년 5월, 6세대 TPU로 Trillium을 발표했습니다. 이는 회사의 클라우드 플랫폼에 초점을 맞춘 것으로, 머신러닝 워크로드를 가속화하는 온보드 액셀러레이터를 특징으로 합니다. TPU를 광범위하게 도입한 기업은 예측 분석, 개인화, 업무 효율화를 위해 머신러닝의 힘을 활용하고 있습니다. 이는 해당 분야에서 AI 칩에 대한 의존도가 높아지고 있음을 보여줍니다. 기업이 데이터의 힘을 활용하여 인사이트, 효율성, 고객 경험을 향상시키기 위해 머신러닝 기능에 대한 수요가 급증하고 있습니다.

미국은 북미 AI 칩 시장에서 가장 큰 점유율을 차지할 것으로 예측됩니다. 주요 기술 기업 및 데이터센터 사업자의 존재가 북미 전역의 AI 칩 시장 성장을 주도하고 있습니다. 이 지역에는 NVIDIA Corporation(미국), Intel Corporation(미국), Advanced Micro Devices, Inc.(AMD)(미국), Google(미국) 등의 기업이 기반을 두고 있으며, 클라우드 서비스 제공 업체로는 Amazon Web Services, Inc.(AWS)(미국), Microsoft Azure(미국), Google Cloud(미국) 등이 존재합니다. 예를 들어 2024년 4월 구글(미국)은 미국 전역의 데이터센터 확장을 위해 30억 달러를 투자한다고 발표했습니다. 이러한 데이터센터는 AI 인프라를 통해 더욱 강화되어 전 세계에 실시간 서비스를 제공할 수 있게 됩니다. 또한 이 지역에는 데이터센터용 AI 칩을 제공하는 스타트업 기업도 다수 존재합니다. SAPEON Inc.(미국), Tenstorrent(캐나다), Taalas(캐나다), Kneron, Inc.(미국), SambaNova Systems, Inc.(미국) 등이 있습니다. 북미에는 첨단 AI 연구개발을 지원할 수 있는 탄탄한 기술 인프라가 구축되어 있습니다. 이 지역에는 최첨단 AI 하드웨어를 갖춘 현대식 데이터센터가 다수 존재하며, 최첨단 AI 하드웨어를 갖추고 있습니다. 여기에는 GPU, TPU 및 전용 AI 칩이 포함될 수 있습니다. 이 지역의 대규모 데이터센터와 주요 AI 칩 개발 기업의 존재가 AI 칩 시장의 성장을 촉진하고 있습니다.

AI 칩 시장의 주요 부문 및 하위 부문 시장 규모를 확정하고 검증하기 위해 2차 조사에서 수집한 데이터를 바탕으로 업계 주요 전문가를 대상으로 광범위한 1차 인터뷰를 실시했습니다. 이 보고서의 1차 조사 대상자 내역은 다음과 같습니다.

이 보고서에서 다루는 주요 기업으로는 NVIDIA Corporation(미국), Intel Corporation(미국), Advanced Micro Devices, Inc.(미국), Micron Technology, Inc.(미국), Google(미국), Samsung(한국), SK HYNIX INC.(한국), Qualcomm Technologies, Inc.(미국), Huawei Technologies(중국), Apple Inc.(미국), Imagination Technologies(영국), Graphcore(영국), Cerebras(미국) 등을 들 수 있습니다. 이 외에 Mythic(미국), Kalray(프랑스), Blaize(미국), Groq, Inc.(미국), HAILO TECHNOLOGIES LTD(이스라엘), GreenWaves Technologies(프랑스), SiMa Technologies, Inc.(미국), Kneron, Inc.(미국), Rain Neuromorphics Inc.(미국), Tenstorrent(캐나다), SambaNova Systems, Inc.(미국), Taalas(캐나다), SAPEON Inc.(미국), Rebellions Inc.(한국), Rivos Inc(미국), Shanghai BiRen Technology(중국) 등이 AI 칩 시장에서 신규 기업의 일부입니다.

이 보고서는 다음 사항에 대한 인사이트을 제공

AI 칩 시장의 주요 촉진요인(AI 서버의 GPU 및 ASIC 급증), 제약 요인(AI 칩의 계산 부하 및 높은 전력 소비), 기회(클라우드 서비스 프로바이더의 AI 지원 데이터센터 투자 증가), 과제(공급망 혼란) 분석

제품 개발/혁신 : AI 칩 시장의 향후 기술 동향, 연구개발 활동, 제품 출시/개선에 대한 상세한 분석.

시장 개발: 수익성 높은 시장에 대한 종합적인 정보. 이 보고서에서는 다양한 지역의 AI 칩 시장을 분석합니다.

시장 다각화 : AI 칩 시장의 신제품 출시, 미개발 지역, 최근 동향, 투자에 대한 종합적인 정보.

경쟁사 평가 : NVIDIA Corporation(미국), Intel Corporation(미국), Advanced Micro Devices, Inc. HYNIX INC.(한국), Qualcomm Technologies, Inc.(미국), Huawei Technologies(중국) 등 AI 칩 시장의 주요 기업 시장 점유율, 성장전략, 제공 제품에 대한 상세한 평가.

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 AI 칩 시장(컴퓨팅별)

제10장 AI 칩 시장(메모리별)

제11장 AI 칩 시장(네트워크별)

제12장 AI 칩 시장(기술별)

제13장 AI 칩 시장(기능별)

제14장 AI 칩 시장(최종사용자별)

제15장 AI 칩 시장(지역별)

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 부록

KSA

영문 목차

영문목차

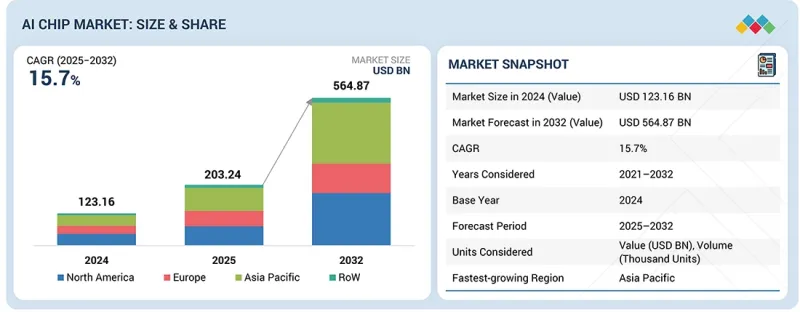

The AI chip market is projected to grow from USD 203.24 billion in 2025 to USD 564.87 billion by 2032; it is expected to grow at a compound annual growth rate (CAGR) of 15.7% from 2025 to 2032.

Scope of the Report

Years Considered for the Study

2020-2032

Base Year

2024

Forecast Period

2025-2032

Units Considered

Value (USD Billion)

Segments

By Offerings, Network, Function and Region

Regions covered

North America, Europe, APAC, RoW

"The neural processing unit (NPU) segment is projected to record a high growth rate during the forecast period."

The neural processing unit (NPU) segment is expected to record a high growth rate in the AI chip market from 2024 to 2029. The market growth is attributed to the increasing adoption of high-end smartphones, AI PCs, and laptops, which require dedicated AI capabilities at the edge. The NPUs help accelerate neural network processing to perform AI-driven tasks, including advanced AI image processing and natural language processing. Market players are extensively focusing on developing high-end NPU solutions to stay competitive in the market. For instance, in September 2023, Apple Inc. (US) launched the iPhone 15 Pro series, featuring the A17 Pro chip. The new AI processor is equipped with a dedicated 16-core Neural Engine, capable of performing 35 trillion operations per second (TOPS). Such significant product developments and launches are expected to amplify the adoption of NPUs in the market over the forecast period.

"The machine learning segment is expected to account for significant market share throughout the forecast period."

The machine learning segment of the AI chip market is expected to capture a significant market share. AI chips are crucial in processing large datasets to enable predictive analytics, supporting real-time decision-making, as they are optimized for machine learning tasks such as training and inference. For this category of AI chips, the foremost drivers of adoption were flexibility and scalability of machine learning models within autonomous systems and personalized recommendations. This AI chip is widely used in many sectors, including cloud services, healthcare, finance, automotive, and retail. Companies are developing powerful AI chips to support machine learning capabilities, which enable business insights, improve customer experience, and enhance overall efficiency. For instance, Google (US) announced Trillium in May 2024 as its sixth-generation TPU. It focuses on its cloud platform, featuring an onboard accelerator for accelerating machine learning workloads. Enterprises that have adopted TPUs widely bring machine learning power to predictive analytics, personalization, and operational efficiency. This represents increasing dependence on AI chips in this domain. As businesses seek to harness the power of data for insights, efficiencies, and enhanced customer experiences, demand is surging for machine learning capabilities.

"The US is expected to hold the largest share of the North American market during the forecast period."

The US is expected to hold the largest share of the AI chip market in North America. The presence of prominent technology firms and data center operators is driving the AI chip market across North America. The region hosts companies such as NVIDIA Corporation (US), Intel Corporation (US), Advanced Micro Devices, Inc. (AMD) (US), Google (US); and cloud service providers include Amazon Web Services, Inc. (AWS) (US), Microsoft Azure (US), and Google Cloud (US). For instance, in April 2024, Google (US) announced a USD 3 billion investment to expand its data centers across the US. These data centers are further supported by AI infrastructure, enabling them to provide real-time services worldwide. The region also hosts several startups established in the area to provide AI chips for data centers, including SAPEON Inc. (US), Tenstorrent (Canada), Taalas (Canada), Kneron, Inc. (US), and SambaNova Systems, Inc. (US). North America has a well-established technological infrastructure that supports advanced AI research and development. There are many modern data centers in this region, equipped with state-of-the-art AI hardware. They may include GPUs, TPUs, and specialized AI chips. The presence of large-scale data centers and leading AI chip developers in the region is driving the growth of the AI chip market.

Extensive primary interviews were conducted with key industry experts in the AI chip market to determine and verify the market size for various segments and subsegments, which were gathered through secondary research. The breakdown of primary participants for the report is shown below.

The study draws insights from a range of industry experts, including component suppliers, Tier 1 companies, and OEMs. The break-up of the primaries is as follows:

By Company Type - Tier 1 - 45%, Tier 2 - 32%, and Tier 3 - 23%

By Designation - C-level Executives - 30%, Directors - 45%, and Others - 25%

By Region - Asia Pacific - 26%, Europe - 40%, North America - 22%, and RoW - 12%

Note: Other designations include technology heads, media analysts, sales managers, marketing managers, and product managers.

The three tiers of companies are based on their total revenues as of 2024: Tier 1: >USD 1 billion, Tier 2: USD 500 million to 1 billion, and Tier 3: <USD 500 million.

Prominent players profiled in this report include NVIDIA Corporation (US), Intel Corporation (US), Advanced Micro Devices, Inc. (US), Micron Technology, Inc. (US), Google (US), Samsung (South Korea), SK HYNIX INC. (South Korea), Qualcomm Technologies, Inc. (US), Huawei Technologies Co., Ltd. (China), Apple Inc. (US), Imagination Technologies (UK), Graphcore (UK), Cerebras (US). Apart from this, Mythic (US), Kalray (France), Blaize (US), Groq, Inc. (US), HAILO TECHNOLOGIES LTD (Israel), GreenWaves Technologies (France), SiMa Technologies, Inc. (US), Kneron, Inc. (US), Rain Neuromorphics Inc. (US), Tenstorrent (Canada), SambaNova Systems, Inc. (US), Taalas (Canada), SAPEON Inc. (US), Rebellions Inc. (South Korea), Rivos Inc. (US), and Shanghai BiRen Technology Co., Ltd. (China) are among a few emerging companies in the AI chip market.

Report Coverage

The report defines, describes, and forecasts the AI chip market based on type, technology, frequency, application, and region. It provides detailed information regarding drivers, restraints, opportunities, and challenges influencing the growth of the AI chip market. It also analyzes competitive developments, including acquisitions, product launches, expansions, and strategic actions taken by key players to expand in the market.

Reasons to Buy This Report

The report will help market leaders/new entrants in the market with information on the closest approximations of revenue for the overall AI chip market and its subsegments. The report will help stakeholders understand the competitive landscape and gain more insight to position their business better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market, providing them with information on key drivers, restraints, opportunities, and challenges.

The report will provide insights into the following pointers:

Analysis of key drivers (Surging use of GPUs and ASICs in AI servers), restraints (Computational workloads and high power consumption by AI chips), opportunities (Increasing investments in AI-enabled data centers by cloud service providers), and challenges (Supply chain disruptions) in the AI chip market.

Product development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product launches/enhancements in the AI chip market.

Market Development: Comprehensive information about lucrative markets; the report analyzes the AI chip market across various regions.

Market Diversification: Exhaustive information about new products launched, untapped geographies, recent developments, and investments in the AI chip market.

Competitive Assessment: In-depth assessment of market share, growth strategies, and offering of leading players such as NVIDIA Corporation (US), Intel Corporation (US), Advanced Micro Devices, Inc. (US), Micron Technology, Inc. (US), Google (US), Samsung (South Korea), SK HYNIX INC. (South Korea), Qualcomm Technologies, Inc. (US), Huawei Technologies Co., Ltd. (China), among others in the AI chip market.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 LIMITATIONS

1.6 STAKEHOLDERS

1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

2.3 DISRUPTIONS SHAPING AI CHIP MARKET

2.4 HIGH-GROWTH SEGMENTS

2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AI CHIP MARKET

3.2 AI CHIP MARKET, BY COMPUTE

3.3 AI CHIP MARKET, BY FUNCTION

3.4 AI CHIP MARKET, BY END USER

3.5 ASIA PACIFIC: AI CHIP MARKET, BY FUNCTION AND COUNTRY

3.6 AI CHIP MARKET, BY COUNTRY

4 MARKET OVERVIEW

4.1 INTRODUCTION

4.2 MARKET DYNAMICS

4.2.1 DRIVERS

4.2.1.1 Pressing need for large-scale data handling and real-time analytics

4.2.1.2 Rising adoption of autonomous vehicles

4.2.1.3 Surging use of GPUs and ASICs in AI servers

4.2.1.4 Continuous advancements in machine learning and deep learning technologies

4.2.1.5 Increasing penetration of AI servers

4.2.2 RESTRAINTS

4.2.2.1 Shortage of skilled workforce with technical know-how

4.2.2.2 Computational workloads and power consumption in AI chips

4.2.2.3 Unreliability of AI algorithms

4.2.3 OPPORTUNITIES

4.2.3.1 Elevating demand for AI-based FPGA chips

4.2.3.2 Government initiatives to deploy AI-enabled defense systems

4.2.3.3 Growing trend of AI-driven diagnostics and treatments

4.2.3.4 Increasing investments in AI-enabled data centers by cloud service providers

4.2.3.5 Rising popularity of AI-based ASIC technology

4.2.4 CHALLENGES

4.2.4.1 Data privacy concerns associated with AI platforms

4.2.4.2 Availability of limited structured data to develop efficient AI systems

4.2.4.3 Supply chain disruptions

4.3 UNMET NEEDS AND WHITE SPACES

4.3.1 UNMET NEEDS IN AI CHIPS MARKET

4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

4.4.1 INTERCONNECTED MARKETS

4.4.2 CROSS-SECTOR OPPORTUNITIES

4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

4.5.1 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

5.1 INTRODUCTION

5.2 PORTER'S FIVE FORCES ANALYSIS

5.2.1 THREAT OF NEW ENTRANTS

5.2.2 THREAT OF SUBSTITUTES

5.2.3 BARGAINING POWER OF SUPPLIERS

5.2.4 BARGAINING POWER OF BUYERS

5.2.5 INTENSITY OF COMPETITIVE RIVALRY

5.3 MACROECONOMICS INDICATORS

5.3.1 INTRODUCTION

5.3.2 GDP TRENDS AND FORECAST

5.3.3 TRENDS IN AI CHIP MARKET

5.4 VALUE CHAIN ANALYSIS

5.5 ECOSYSTEM ANALYSIS

5.6 PRICING ANALYSIS

5.6.1 AVERAGE SELLING PRICE OF COMPUTE, BY KEY PLAYERS

5.6.2 AVERAGE SELLING PRICE TREND, BY REGION

5.7 TRADE ANALYSIS

5.7.1 IMPORT DATA (HS CODE 854231)

5.7.2 EXPORT SCENARIO (HS CODE 854231)

5.8 KEY CONFERENCES AND EVENTS, 2026

5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.10 INVESTMENT AND FUNDING SCENARIO

5.11 CASE STUDY ANALYSIS

5.11.1 CDW INTEGRATED AMD EPYC SOLUTIONS TO ENSURE ENERGY EFFICIENCY AND OPTIMUM SPACE UTILIZATION

5.11.2 OVH SAS LEVERAGED AMD EPYC PROCESSOR TO OPTIMIZE PERFORMANCE OF CLOUD SOLUTIONS IN AI WORKLOADS

5.11.3 INTEL XEON SCALABLE PROCESSORS POWER TENCENT CLOUD'S XIAOWEI INTELLIGENT SPEECH AND VIDEO SERVICE ACCESS PLATFORM

5.11.4 AIC HELPS WESTERN DIGITAL TO ENHANCE SSD TESTING AND VALIDATION EFFICIENCY USING AMD PROCESSOR

5.12 IMPACT OF 2025 US TARIFFS - AI CHIP MARKET

5.12.1 KEY TARIFF RATES

5.12.2 PRICE IMPACT ANALYSIS

5.12.3 IMPACT ON REGIONS/COUNTRIES

5.12.3.1 US

5.12.3.2 Europe

5.12.3.3 Asia Pacific

5.12.4 IMPACT ON END USERS

5.12.4.1 Consumers

5.12.4.2 Data centers

5.12.4.3 Other organizations

5.13 SERVER COST STRUCTURE/BILL OF MATERIALS

5.13.1 CPU SERVER

5.13.2 GPU SERVER

5.14 PENETRATION AND GROWTH OF AI SERVERS

5.15 UPCOMING DEPLOYMENT OF DATA CENTERS BY CLOUD SERVICE PROVIDERS (CSPS)

5.16 CAPEX OF CLOUD SERVICE PROVIDERS

5.17 SERVER PROCUREMENT BY CLOUD SERVICE PROVIDERS

5.18 PROCESSOR BENCHMARKING

5.18.1 GPU BENCHMARKING

5.18.2 CPU BENCHMARKING

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

6.1 TECHNOLOGY ANALYSIS

6.1.1 KEY TECHNOLOGIES

6.1.1.1 High-bandwidth memory (HBM)

6.1.1.2 GenAI workload

6.1.2 COMPLEMENTARY TECHNOLOGIES

6.1.2.1 Data center power management and cooling system

6.1.2.2 High-speed interconnects

6.1.3 ADJACENT TECHNOLOGIES

6.1.3.1 AI development frameworks

6.1.3.2 Quantum AI

6.2 TECHNOLOGY ROADMAP

6.3 PATENT ANALYSIS

6.4 FUTURE APPLICATIONS

7 REGULATORY LANDSCAPE

7.1 INTRODUCTION

7.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

7.3 STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

8.1 DECISION-MAKING PROCESS

8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

8.2.2 BUYING CRITERIA

8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

8.4 UNMET NEEDS FROM VARIOUS VERTICALS

9 AI CHIP MARKET, BY COMPUTE

9.1 INTRODUCTION

9.2 GPU

9.2.1 ABILITY TO HANDLE AI WORKLOADS AND PROCESS VAST DATA VOLUMES TO BOOST ADOPTION

9.3 CPU

9.3.1 RISING DEMAND FOR VERSATILE AND GENERAL-PURPOSE AI PROCESSING TO AUGMENT MARKET GROWTH

9.4 FPGA

9.4.1 GROWING NEED FOR FLEXIBILITY AND CUSTOMIZATION FOR AI WORKLOADS TO SPUR DEMAND

9.5 NPU

9.5.1 RISING DEMAND FOR HIGH-END SMARTPHONES TO DRIVE SEGMENTAL GROWTH

9.6 TPU

9.6.1 PRESSING NEED FOR FASTER PROCESSING IN AI RESEARCH AND APPLICATION DEVELOPMENT TO BOOST DEMAND

9.7 DOJO & FSD

9.7.1 ACCELERATING DEMAND FOR HIGH-PERFORMANCE, ENERGY-EFFICIENT AI PROCESSING IN AUTONOMOUS VEHICLES TO FUEL ADOPTION

9.8 TRAINIUM & INFERENTIA

9.8.1 ABILITY TO TRAIN COMPLEX AI AND DEEP LEARNING MODELS TO DRIVE ADOPTION

9.9 ATHENA ASIC

9.9.1 INCREASING NEED TO HANDLE COMPLEX NLP AND LANGUAGE-BASED AI TASKS TO ACCELERATE MARKET GROWTH

9.10 T-HEAD

9.10.1 RISING DEMAND FOR CUSTOMIZED, HIGH-PERFORMANCE AI CHIPS ACROSS CHINESE DATA CENTERS TO STIMULATE MARKET GROWTH

9.11 MTIA

9.11.1 META'S EXPANSION INTO AR, VR, AND METAVERSE TO FUEL DEMAND

9.12 LPU

9.12.1 INCREASING NEED TO HANDLE COMPLEX NLP AND LANGUAGE-BASED AI TASKS TO ACCELERATE MARKET GROWTH

9.13 ASCEND

9.13.1 RISING DEMAND FOR UNIFIED AI ARCHITECTURES AND DOMESTIC CHIP ECOSYSTEMS TO DRIVE MARKET EXPANSION

9.14 OTHER ASICS

10 AI CHIP MARKET, BY MEMORY

10.1 INTRODUCTION

10.2 DDR

10.2.1 RISING ADOPTION OF AI-ENABLED CPUS IN DATA CENTERS TO SUPPORT MARKET GROWTH

10.3 HBM

10.3.1 ELEVATING NEED FOR HIGH THROUGHPUT IN DATA-INTENSIVE AI TASKS TO FUEL MARKET GROWTH

11 AI CHIP MARKET, BY NETWORK

11.1 INTRODUCTION

11.2 NIC/NETWORK ADAPTERS

11.2.1 INFINIBAND

11.2.1.1 Growing utilization of HPC and AI models to minimize latency and maximize throughput to boost segmental growth

11.2.2 ETHERNET

11.2.2.1 Rising demand for scalable and cost-effective networking solutions to propel demand

11.3 INTERCONNECTS

11.3.1 GROWING COMPLEXITY OF AI MODELS REQUIRING HIGH-BANDWIDTH DATA PATHS TO FUEL DEMAND

12 AI CHIP MARKET, BY TECHNOLOGY

12.1 INTRODUCTION

12.2 GENERATIVE AI

12.2.1 RULE-BASED MODELS

12.2.1.1 Rising need to detect fraud in finance sector to propel market

12.2.2 STATISTICAL MODELS

12.2.2.1 Need for accurate predictions from complex data structures to boost segmental growth

12.2.3 DEEP LEARNING

12.2.3.1 Ability to advance AI technologies to boost demand

12.2.4 GENERATIVE ADVERSARIAL NETWORKS (GAN)

12.2.4.1 Pressing need to handle large-scale data to fuel demand

12.2.5 AUTOENCODERS

12.2.5.1 Ability to compress and restructure data to ensure optimum storage space in data centers to stimulate demand

12.2.6 CONVOLUTIONAL NEURAL NETWORKS

12.2.6.1 Surging demand for realistic and high-quality images and videos to accelerate market growth

12.2.7 TRANSFORMER MODELS

12.2.7.1 Increasing utilization in image synthesis and captioning applications to foster segmental growth

12.3 MACHINE LEARNING

12.3.1 RISING USE IN IMAGE & SPEECH RECOGNITION AND PREDICTIVE ANALYTICS TO CONTRIBUTE TO MARKET GROWTH

12.4 NATURAL LANGUAGE PROCESSING

12.4.1 INCREASING NEED FOR REAL-TIME APPLICATIONS TO SUPPORT MARKET GROWTH

12.5 COMPUTER VISION

12.5.1 ESCALATING NEED FOR ADVANCED PROCESSING CAPABILITIES TO BOOST DEMAND

13 AI CHIP MARKET, BY FUNCTION

13.1 INTRODUCTION

13.2 TRAINING

13.2.1 SURGING NEED TO PROCESS LARGE DATA SETS AND PERFORM PARALLEL COMPUTATION TO CREATE GROWTH OPPORTUNITIES

13.3 INFERENCE

13.3.1 SURGING DEPLOYMENT ACROSS VARIOUS INDUSTRIES TO BOOST DEMAND

14 AI CHIP MARKET, BY END USER

14.1 INTRODUCTION

14.2 CONSUMERS

14.2.1 GROWING ADOPTION OF AI-ENABLED PERSONAL DEVICES TO PROPEL MARKET

14.3 DATA CENTERS

14.3.1 CLOUD SERVICE PROVIDERS

14.3.1.1 Surging AI workloads and cloud adoption to stimulate market growth

14.3.2 ENTERPRISES

14.3.2.1 Escalating use of NLP, image recognition, and predictive analytics to create growth opportunities

14.3.2.2 Healthcare

14.3.2.2.1 Integration of AI in computer-aided drug discovery and development to foster market growth

14.3.2.3 BFSI

14.3.2.3.1 Surging need for fraud detection in financial institutions to boost demand

14.3.2.4 Automotive

14.3.2.4.1 Growing focus on safe and enhanced driving experiences to fuel demand

14.3.2.5 Retail & e-commerce

14.3.2.5.1 Increasing use of chatbots and virtual assistants to offer improved customer services to drive market

14.3.2.6 Media & entertainment

14.3.2.6.1 Real-time analysis of viewer preferences, engagement patterns, and demographic information to augment market growth

14.3.2.7 Others

14.4 GOVERNMENT ORGANIZATIONS

14.4.1 SIGNIFICANT FOCUS ON AUTOMATING ROUTINE TASKS AND EXTRACTING REAL-TIME ACTIONABLE INSIGHTS TO SUPPORT MARKET GROWTH

15 AI CHIP MARKET, BY REGION

15.1 INTRODUCTION

15.2 NORTH AMERICA

15.2.1 US

15.2.1.1 Government-led initiatives to boost semiconductor manufacturing to drive market

15.2.2 CANADA

15.2.2.1 Growing emphasis on commercializing AI to spur demand

15.2.3 MEXICO

15.2.3.1 Increasing shift toward digital platforms and cloud-based solutions to accelerate demand

15.3 EUROPE

15.3.1 UK

15.3.1.1 Growing investments in data center infrastructure to boost demand

15.3.2 GERMANY

15.3.2.1 Robust industrial base to offer lucrative growth opportunities

15.3.3 FRANCE

15.3.3.1 Increasing number of AI startups to accelerate demand

15.3.4 ITALY

15.3.4.1 Rising trend of digitalization in automotive and healthcare sectors to drive market

15.3.5 SPAIN

15.3.5.1 Growing collaborations and partnerships among AI manufacturers to spur demand

15.3.6 REST OF EUROPE

15.4 ASIA PACIFIC

15.4.1 CHINA

15.4.1.1 Surge in research funding and implementation of supportive regulatory policy to augment market growth

15.4.2 JAPAN

15.4.2.1 Rising focus on advancing robotic systems to boost market

15.4.3 INDIA

15.4.3.1 Government-led initiatives to boost AI infrastructure to foster market growth

15.4.4 SOUTH KOREA

15.4.4.1 Thriving semiconductor industry to drive market

15.4.5 REST OF ASIA PACIFIC

15.5 REST OF THE WORLD

15.5.1 MIDDLE EAST

15.5.1.1 Growing emphasis on digital transformation and technological innovation to drive market

15.5.1.2 GCC countries

15.5.1.3 Rest of Middle East

15.5.2 AFRICA

15.5.2.1 Rising internet penetration and mobile subscriptions to drive market

15.5.3 SOUTH AMERICA

15.5.3.1 Growing need to store vast volumes of data to boost demand

16 COMPETITIVE LANDSCAPE

16.1 OVERVIEW

16.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

16.3 REVENUE ANALYSIS, 2021-2024

16.4 MARKET SHARE ANALYSIS, 2024

16.4.1 COMPUTE MARKET SHARE, 2024

16.4.2 MEMORY (HBM) MARKET SHARE, 2023

16.5 COMPANY VALUATION AND FINANCIAL METRICS

16.6 BRAND/PRODUCT COMPARISON

16.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

16.7.1 STARS

16.7.2 EMERGING LEADERS

16.7.3 PERVASIVE PLAYERS

16.7.4 PARTICIPANTS

16.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

16.7.5.1 Company footprint

16.7.5.2 Regional footprint

16.7.5.3 Compute footprint

16.7.5.4 Memory footprint

16.7.5.5 Network footprint

16.7.5.6 Technology footprint

16.7.5.7 Function footprint

16.7.5.8 End user footprint

16.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024