IV Equipment Market by Type (IV Catheter, IV Administration Set, Needle-free Connectors), Application (Medication Administration, Parenteral Nutrition, Diagnostic Testing, Blood & Blood Product Transfusion), End User (Hospital) - Global Forecast to 2031

상품코드:1961000

리서치사:MarketsandMarkets

발행일:2026년 02월

페이지 정보:영문 425 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

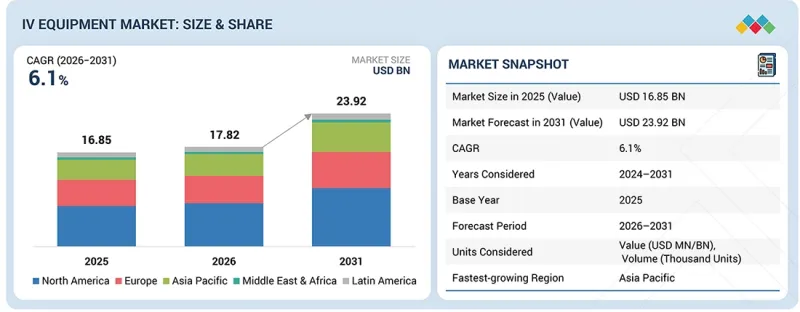

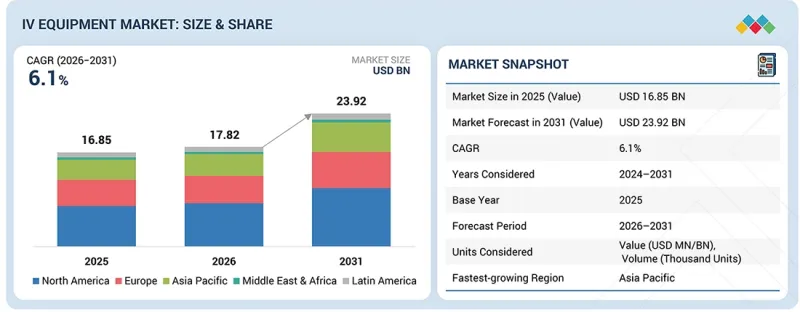

세계의 정맥내(IV) 장비 시장 규모는 2026년 178억 2,000만 달러에서 2031년까지 239억 2,000만 달러에 달할 것으로 예측되고 있으며, 예측 기간 중 CAGR 6.1%로 성장할 전망입니다.

조사 범위

조사 대상 기간

2024-2031년

기준연도

2025년

예측 기간

2026-2031년

대상 단위

금액(10억 달러)

부문

유형별, 용도별, 최종사용자별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카.

세계 만성질환 증가와 입원환자 증가를 배경으로 정맥주사(IV) 의료기기 수요는 꾸준히 확대되고 있습니다. 약물 투여, 수분 보충, 영양 보충을 위한 IV 요법의 보급 확대와 더불어 재택치료 및 외래 치료로의 전환이 진행됨에 따라 제품 이용이 촉진되고 있습니다. 병원 및 진료소에서는 정확한 약물 투여와 환자의 안전을 보장하기 위해 고품질의 안전하고 사용하기 쉬운 정맥 내(IV) 의료기기를 우선적으로 도입하고 있습니다. 바늘 없는 커넥터, 스마트 주입 펌프, 호환 가능한 다기능 IV 시스템과 같은 기술 혁신은 시장 보급을 더욱 촉진하고 있습니다. 또한 신흥 국가의 의료 인프라 확충과 현대적 의료행위를 촉진하기 위한 정부의 적극적인 정책은 향후 수년간 시장의 견고한 성장을 지속할 것으로 예측됩니다.

유형별로는 바늘 없는 커넥터 및 연장 세트가 정맥 내(IV) 의료기기 시장에서 가장 빠르게 성장하는 부문입니다. 그 배경에는 안전성 향상, 조작의 편리성, 감염 위험 및 침 찔림 사고의 현저한 감소 능력이 있습니다. 이 커넥터는 병원, 진료소, 재택치료 환경에서 약품 투여의 효율성, 오염 감소, 워크플로우의 효율화를 실현합니다. 또한 엄격한 감염 관리 규정과 의료 종사자들의 환자 안전에 대한 인식이 높아지면서 현대 의료시설에서 매우 선호되는 선택이 되고 있습니다.

용도별로는 약물 투여가 정맥내 투여 기기 시장에서 가장 큰 점유율을 차지하고 있습니다. 정맥내 요법은 약물을 혈류에 직접 주입하므로 약효 발현이 빠르고, 용량이 정확하며, 최적의 치료 효과를 기대할 수 있기 때문입니다. 이 용도는 특히 중환자실, 화학요법, 통증 관리, 중증 감염 치료에서 중요하며, 신속하고 정확한 약물 투여가 환자의 결과를 크게 개선합니다. 만성 및 급성 질환의 유병률 증가와 입원 환자 수 증가에 따라 정맥내 약물 투여에 대한 수요는 지속적으로 증가하고 있습니다.

정맥 투여 기기 시장은 북미, 유럽, 라틴아메리카, 아시아태평양, 중동 및 아프리카로 분류됩니다. 북미는 세계 정맥내 투여 기기 시장을 선도하고 있습니다. 이러한 우위는 높은 만성질환 유병률, 잘 구축된 의료 인프라, 첨단 의료기술의 빠른 도입에 기인합니다. 또한 주요 시장 진출기업의 강력한 존재감, 의료비 지출 증가, 병원 및 재택치료 환경에서의 첨단 주입 시스템에 대한 수요 증가는 이 지역 시장 선도적 지위를 더욱 지원하고 있습니다.

정맥 투여 기기 시장의 주요 업체는 다음과 같습니다. Becton, Dickinson and Company(미국), B. Braun SE(독일), Fresenius SE & Co. KGaA(독일), ICU Medical, Inc. Teleflex Incorporated(미국), Cardinal Health(미국), Shenzhen Mindray Bio-Medical Electronics(중국), Baxter(미국), Avanos Medical, Inc(미국), Nipro(일본), JMS(일본), Vitality, Inc. JMS(일본), Vygon(프랑스), Micrel Medical Devices SA(그리스) 등이 있습니다.

조사 범위

이 보고서는 정맥 내(IV) 의료기기 시장을 유형별, 용도별, 최종사용자별, 지역별로 분석합니다. 또한 시장 성장에 영향을 미치는 요인을 포괄하고, 시장의 다양한 기회와 과제를 분석하는 한편, 시장 리더경쟁 구도를 상세하게 제공합니다. 또한 마이크로마켓을 개별 성장 추세별로 분석하고, 5개 주요 지역(및 해당 지역내 국가) 시장 세분화에 대한 매출 예측을 제공합니다.

이 보고서 구매의 장점

이 보고서는 기존 기업 및 신규 진출기업/중소기업이 시장 동향을 파악하고 더 큰 시장 점유율을 확보하는 데 도움이 될 것입니다. 이 보고서를 구매하는 기업은 다음 전략 중 하나 또는 조합을 활용하여 시장에서의 입지를 강화할 수 있습니다.

이 보고서는 다음 사항에 대한 인사이트을 제공

정맥주사(IV) 기기 시장의 성장에 영향을 미치는 주요 촉진요인(전 세계 질병 부담 증가와 이에 따른 고령 인구 급증, 재택 및 외래 환자 투약으로의 전환), 억제요인(제품 리콜 및 고장), 기회(신흥 시장의 미개발 성장 잠재력), 과제(벤더 간 제휴) 등을 분석합니다.

시장 침투: 정맥내 투여 기기 시장의 주요 기업이 제공하는 제품 포트폴리오에 대한 종합적인 정보.

제품 개발/혁신 : 정맥내 투여 기기 시장의 향후 동향, 연구개발 활동, 제품 개발에 대한 상세한 분석.

시장 개발: 수익성이 높은 신흥 지역에 대한 종합적인 정보.

시장 다각화 : 정맥 내(IV) 의료기기 시장의 신제품, 성장 지역, 최근 동향에 대한 종합적인 정보를 제공합니다.

경쟁 평가: 주요 시장 진출기업 시장 세분화, 성장 전략, 매출 분석, 제품에 대한 상세한 평가.

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 테크놀러지, 특허, 디지털·AI 도입에 의한 전략적 파괴

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 정맥내(IV) 장비 시장(유형별)

제10장 정맥내(IV) 장비 시장(용도별)

제11장 정맥내(IV) 장비 시장(최종사용자별)

제12장 정맥내(IV) 장비 시장(지역별)

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

KSA

영문 목차

영문목차

The global IV equipment market is projected to reach USD 23.92 billion by 2031 from USD 17.82 billion in 2026, growing at a CAGR of 6.1% during the forecast period.

Scope of the Report

Years Considered for the Study

2024-2031

Base Year

2025

Forecast Period

2026-2031

Units Considered

Value (USD billion)

Segments

Type, Application, End User, and Region

Regions covered

North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa.

The demand for IV equipment is growing steadily, driven by the rising prevalence of chronic diseases and increasing hospitalizations worldwide. The growing adoption of IV therapy for medication administration, hydration, and nutrition, along with the shift toward home-based and outpatient care, is boosting product utilization. Hospitals and clinics are prioritizing high-quality, safe, and user-friendly IV devices to ensure accurate drug delivery and patient safety. Technological innovations, such as needle-free connectors, smart infusion pumps, and compatible multi-parameter IV systems, are further enhancing market adoption. Moreover, expanding healthcare infrastructure in emerging economies and favorable government initiatives promoting modern healthcare practices are expected to sustain strong market growth in the coming years.

"By type, the needle-free connectors & extension sets segment is projected to grow significantly during the forecast period."

Based on type, needle-free connectors & extension sets are the fastest-growing segment in the IV equipment market, driven by their enhanced safety, ease of use, and ability to significantly reduce the risk of infections and needlestick injuries. These connectors streamline medication administration, reduce contamination, and improve workflow efficiency in hospitals, clinics, and home care settings. Their growing adoption is also supported by stringent infection control regulations and increasing awareness among healthcare providers about patient safety, making them a highly preferred choice in modern healthcare facilities.

"By application, the medication administration segment held the largest market share in 2025."

By application, medication administration holds the largest market share in the IV equipment market, as IV therapy allows drugs to be delivered directly into the bloodstream, ensuring rapid onset of action, precise dosing, and optimal therapeutic effectiveness. This application is particularly critical in intensive care units, chemotherapy treatments, pain management, and severe infection management, where timely and accurate drug delivery can significantly improve patient outcomes. The growing prevalence of chronic and acute diseases, along with increasing hospital admissions, continues to drive the demand for IV-based medication administration.

"By region, North America accounted for the largest market share in 2025."

The IV equipment market is segmented into North America, Europe, Latin America, the Asia Pacific, and the Middle East & Africa. North America leads the global IV equipment market. This dominance is attributed to the high prevalence of chronic diseases, well-established healthcare infrastructure, and rapid adoption of advanced medical technologies. Additionally, the strong presence of key market players, increased healthcare spending, and growing demand for advanced infusion systems in hospitals and home healthcare settings further contribute to the region's leading market position.

A breakdown of the primary participants referred to for this report is provided below:

By Company Type: Tier 1 (35%), Tier 2 (40%), and Tier 3 (25%)

By Designation: Directors (25%), Managers (50%), and Others (25%)

By Region: North America (35%), Europe (30%), the Asia Pacific (15%), and the Rest of the World (20%)

The prominent players in the IV equipment market are Becton, Dickinson and Company (US), B. Braun SE (Germany), Fresenius SE & Co. KGaA (Germany), ICU Medical, Inc. (US), Terumo Corporation (Japan), Moog Inc. (US), Teleflex Incorporated (US), Cardinal Health (US), Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China), Baxter (US), Avanos Medical, Inc. (US), Nipro (Japan), JMS Co., Ltd. (Japan), Vygon (France), and Micrel Medical Devices SA (Greece), among others.

Research Coverage

This report analyzes the IV equipment market by type, application, end user, and region. It also covers the factors affecting market growth, analyzes the various opportunities and challenges in the market, and provides details of the competitive landscape for market leaders. Furthermore, the report analyzes micromarkets by their individual growth trends and forecasts market segment revenues across five main regions (and the respective countries in these regions).

Reasons to Buy the Report

The report will enable established firms as well as entrants/smaller firms to gauge the pulse of the market, which, in turn, would help them to garner a larger market share. Firms purchasing the report could use one or a combination of the following strategies to strengthen their market presence.

This report provides insights into the following pointers:

Analysis of key drivers (rising disease burden and the subsequent surge in the geriatric population globally as well as the shift toward home and ambulatory infusion), restraints (product recalls and failures), opportunities (untapped growth potential in emerging markets), and challenges (vendor collaborations) influencing the growth of the IV equipment market.

Market Penetration: Comprehensive information on the product portfolios offered by the top players in the IV equipment market.

Product Development/Innovation: Detailed insights on the upcoming trends, R&D activities, and product developments in the IV equipment market.

Market Development: Comprehensive information on lucrative emerging regions.

Market Diversification: Exhaustive information about new products, growing geographies, and recent developments in the IV equipment market.

Competitive Assessment: In-depth assessment of market segments, growth strategies, revenue analysis, and products of the leading market players.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 SEGMENTS CONSIDERED & GEOGRAPHICAL SCOPE

1.3.2 INCLUSIONS & EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 STAKEHOLDERS

1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

2.1 MARKET HIGHLIGHTS & KEY INSIGHTS

2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

2.3 DISRUPTIVE TRENDS IN IV EQUIPMENT MARKET

2.4 HIGH-GROWTH SEGMENTS

2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

3.1 IV EQUIPMENT MARKET OVERVIEW

3.2 ASIA PACIFIC: IV EQUIPMENT MARKET, BY COUNTRY AND END USER

3.3 GEOGRAPHIC SNAPSHOT OF IV EQUIPMENT MARKET

4 MARKET OVERVIEW

4.1 INTRODUCTION

4.2 MARKET DYNAMICS

4.2.1 DRIVERS

4.2.1.1 Rising disease burden and subsequent surge in geriatric population globally

4.2.1.2 Shift toward home and ambulatory infusion

4.2.1.3 Smart pumps, improved safety features, and precision infusion systems

4.2.2 RESTRAINTS

4.2.2.1 Product recalls and failures

4.2.2.2 Infection and complication risk associated with IV therapy

4.2.3 OPPORTUNITIES

4.2.3.1 Untapped growth potential in emerging markets

4.2.3.2 Technological advancements and vendor collaborations

4.2.4 CHALLENGES

4.2.4.1 Device reliability, maintenance requirements, and user-related errors

4.3 UNMET NEEDS & WHITE SPACES

4.3.1 UNMET NEEDS IN IV EQUIPMENT MARKET

4.3.1.1 Interoperable & smart IV systems

4.3.1.2 Affordable, reliable equipment for emerging markets

4.3.1.3 Better infection-prevention designs

4.3.1.4 Home care & ambulatory-friendly IV devices

4.3.1.5 Streamlined regulatory pathways

4.3.1.6 Wider access & supply consistency

4.3.2 WHITE SPACE OPPORTUNITIES

4.3.2.1 Low-cost smart infusion pumps for emerging markets