Elemental Analysis Market by Type (Heavy Metal (Lead, Arsenic, Mercury, Cadmium), Elemental (C, H, N, O, S), Organic), Technique (ICP-OES, ICP-MS, AAS, XRF), End User (Pharma-Biotech, Academia, Chemicals, F&B) - Global Forecasts to 2030

상품코드:1956051

리서치사:MarketsandMarkets

발행일:2026년 02월

페이지 정보:영문 248 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

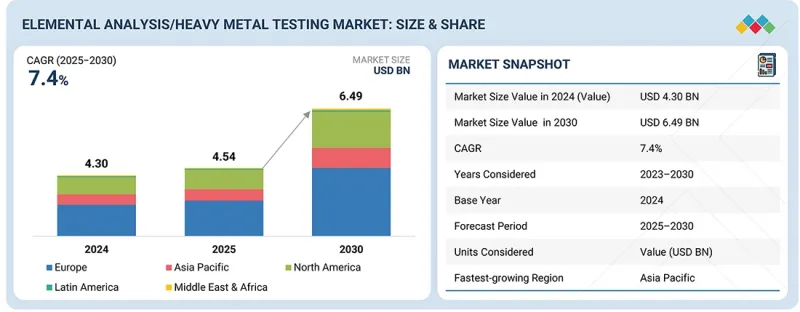

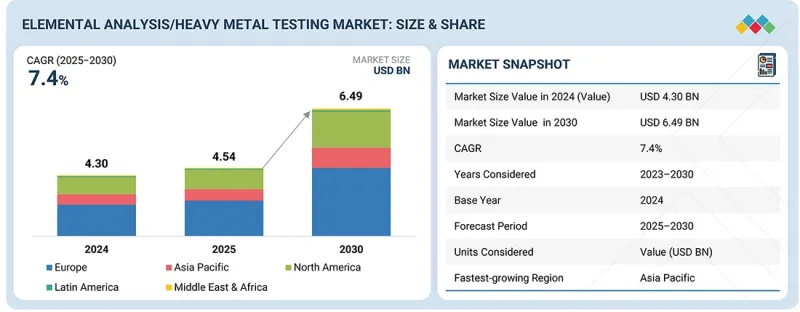

원소 분석 시장 규모는 상당한 성장이 전망되고, 2025년 45억 1,800만 달러에서 2030년까지 64억 8,870만 달러로, CAGR 7.4%로 증가할 것으로 예측됩니다.

조사 범위

조사 대상 기간

2024-2030년

기준 연도

2024년

예측 기간

2025-2030년

대상 단위

금액(10억 달러)

부문

기술별, 유형별, 최종사용자별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카

원소 분석 및 중금속 검사 시장은 규제, 기술, 산업적 요인이 복합적으로 작용하여 괄목할 만한 성장세를 보이고 있습니다. 납, 비소, 카드뮴, 수은 등 유해 금속과 관련된 건강 위험에 대한 인식이 높아짐에 따라 각국 정부와 기관은 의약품, 식품, 화장품, 환경 시료의 허용 원소 수준에 대해 보다 엄격한 규제를 시행하도록 촉구하고 있습니다. FDA(미국 식품의약국), EPA(미국 환경보호청), REACH(유럽 화학제품 규제) 등의 기관은 엄격한 시험 기준을 수립하고 산업계에 신뢰할 수 있고 정확한 분석 방법의 채택을 촉구하고 있습니다. 고감도 ICP-OES(유도결합 플라즈마 발광 분광분석법), ICP-MS(유도결합 플라즈마 질량 분석법), 자동 원소 분석기 등의 기술 발전으로 시험의 속도, 정확성, 효율성이 향상되어 연구소가 규정 준수를 쉽게 충족할 수 있게 되었습니다. 또한, 신흥 경제국의 급속한 산업화와 도시화로 인해 환경 오염이 증가하여 일상적인 원소 및 중금속 모니터링에 대한 수요가 증가하고 있습니다. 특히 헬스케어 및 퍼스널케어 분야에서 안전하고 고품질의 무공해 제품을 원하는 소비자의 선호는 첨단 테스트 솔루션의 도입을 더욱 촉진하고 있습니다. 이러한 요인들이 복합적으로 작용하여 세계 원소 분석 시장은 다양한 분야와 지역에서 꾸준히 성장하고 있습니다.

ICP-OES는 다원소 검출에 있어 뛰어난 성능으로 원소 분석 시장에서 가장 큰 점유율을 차지하고 있습니다. ICP-OES는 고감도, 고정밀도로 주요 원소, 미량원소, 미량원소를 동시에 분석할 수 있어 의약품, 환경 모니터링, 식품안전 등 다양한 용도에 적합합니다. 넓은 다이나믹 레인지로 고농도 및 저농도 원소 모두에 대응하며, 여러 장비와 기법의 필요성을 줄여줍니다. 현대의 ICP-OES 시스템은 자동화, 조작 용이성, 높은 처리량의 시료 처리가 가능하여 실험실의 효율성을 높이고 있습니다. 약전 및 환경 규제 당국의 ICP-OES 법에 대한 규제 승인은 컴플라이언스를 중시하는 산업 분야에서 이 기술의 채택을 촉진하고 있습니다. 또한, ICP-OES는 일상적인 검사를 위한 탁상용 장비부터 고급 연구 시스템까지 확장성이 높아 모든 규모의 실험실에서 범용적으로 활용할 수 있습니다. 이러한 요인들이 복합적으로 작용하여 ICP-OES는 원소 분석 시장에서 여전히 주요 기술로서의 지위를 유지하고 있으며, 가장 큰 점유율을 차지하고 있습니다.

제약 및 바이오 제약 기업은 의약품의 원소 불순물을 모니터링하는 것이 매우 중요하기 때문에 원소 분석 시장을 독점하고 있습니다. ICH Q3D와 USP<232> 등의 규제 가이드라인은 특히 경구 및 비경구 투여 약물에서 납, 비소, 카드뮴, 수은 등 유해 금속에 대해 엄격한 제한을 두고 있습니다. 단클론항체, 백신, 재조합 단백질을 포함한 바이오의약품은 안전성, 유효성 및 배치 간 일관성을 유지하기 위해 종합적인 원소 프로파일링이 필요합니다. 의약품 제제의 복잡성 증가와 더불어 시험을 CRO(위탁연구기관)에 위탁하는 경향이 높아진 것도 고정밀 원소분석기의 수요를 더욱 증가시키고 있습니다. 또한, 제약회사들은 국제 유통을 원활하게 하기 위해 세계 표준 준수를 우선시하고 있으며, 이는 ICP-OES, ICP-MS, CHNS/O 원소 분석기 도입을 촉진하고 있습니다. 그 결과, 제약 및 바이오의약품 분야는 원소 분석 시장에서 가장 큰 응용 분야를 차지하고 있으며, 전 세계적으로 견고하고 안정적인 점유율을 유지하고 있습니다.

북미는 잘 확립된 규제 프레임워크, 선진화된 실험실 인프라, 성숙한 제약 및 생명공학 산업으로 인해 현재 원소 분석 시장을 주도하고 있지만, 향후 몇 년 동안 아시아태평양이 가장 높은 CAGR을 기록할 것으로 예상됩니다. 급속한 산업화, 확대되는 제약 및 바이오테크놀러지 제조, 의료 인프라에 대한 정부 투자 증가가 주요 성장 요인입니다. 중국, 인도, 한국 등의 국가에서는 의약품 생산의 증가, 바이오 의약 연구의 확대, 첨단 분석 기기의 도입이 촉진되고 있습니다. 이 지역의 규제 당국은 원소 불순물에 대한 기준을 강화하고 있으며, 기업들은 정밀하고 높은 처리량의 테스트 솔루션을 도입해야 합니다. 또한, 위탁연구기관(CRO)의 확대와 제품 품질 및 안전성에 대한 인식이 높아진 것도 수요 확대에 기여하고 있습니다. 여기에 낮은 운영 비용과 숙련된 인력의 증가가 더해져 아시아태평양은 원소 및 중금속 테스트 분야에서 가장 빠르게 성장하는 시장으로 자리매김하며 세계 경쟁력을 유지하고 있습니다.

주요 기업으로는 Agilent Technologies Inc.(미국), Thermo Fisher Scientific Inc.(미국), Bruker Corporation(미국), PerkinElmer Inc.(미국) Shimadzu Corporation(일본), SPECTRO Analytical Instruments GmbH(독일), HORIBA Ltd.(일본), Analytik Jena AG(독일), Elementar Analysensensysteme GmbH(독일), Skyray Instruments USA, Inc.(미국), GBC Scientific(호주), Malvern Panalytical Ltd.(영국), Rigaku Holdings Corporation(일본), LECO Corporation(미국), Advion Inc. Teledyne Technologies Incorporated(미국), Hitachi High Tech Corporation(일본), Alpha Measurement Solutions(미국), Buck Scientific, Inc.(일본), PG Instruments Ltd.(영국), Aurora Biomed Inc.(캐나다) 등이 있습니다.

조사 범위

이 보고서는 브랜드, 제품 유형, 절차, 최종사용자 및 지역을 기반으로 원소 분석 시장을 조사합니다.

본 보고서에서는 시장 성장에 영향을 미치는 요인(촉진요인, 억제요인, 기회, 과제 등)을 분석하고 있습니다.

이 보고서는 이해관계자들에게 시장의 기회와 과제를 평가하고, 시장 리더들의 경쟁 상황을 자세히 설명합니다.

본 보고서는 성장 동향, 전망 및 세계 원소 분석 시장/중금속 검사 시장에 대한 기여도와 관련하여 마이크로 시장을 조사하고 있습니다.

본 보고서는 5개 주요 지역의 시장 세분화별 수익을 예측하고 있습니다.

본 보고서 구매의 주요 이점

이 보고서는 신규 진입 기업과 기존 기업 모두에게 가치 있는 정보원이며, 잠재적인 투자 기회를 파악하는 데 필수적인 정보를 제공합니다. 대기업과 중소기업을 모두 포괄적으로 개관하고, 효과적인 리스크 분석과 정보에 입각한 투자 판단을 촉진합니다. 최종사용자 및 지리적 지역을 기반으로 한 정밀한 세분화를 포함하여 틈새 시장 부문에 대한 심층적인 인사이트를 제공합니다. 또한, 주요 트렌드, 촉진요인, 도전과제, 기회를 강조하고 균형 잡힌 분석을 통해 전략적 의사결정을 지원합니다.

이 보고서를 통해 독자들은 다음과 같은 매개변수에 대한 인사이트를 얻을 수 있습니다:

원소 분석 시장 성장과 관련된 주요 촉진요인(엄격한 세계 환경 및 식품 안전 규제, 아웃소싱 검사로의 전환), 억제요인(높은 자본 및 운영 비용, 숙련된 인력 부족), 기회요인(신흥국 수요 증가, 세계 수질 모니터링 의무 확대), 도전요인(높은 장비 비용, 시료 오염 및 정확도 우려) 분석 관련 우려)에 대한 분석.

제품 개발 및 혁신 : 원소 분석 시장/중금속 검사 시장의 신기술 동향, 연구개발 활동, 신제품 및 서비스 출시에 대한 상세한 분석.

시장 개발 : 수익성 높은 시장에 대한 종합적인 정보 - 이 보고서는 다양한 지역의 원소 분석 시장을 분석합니다.

시장 다각화 : 원소 분석 시장의 신제품, 미개척 지역, 최근 동향, 투자에 대한 종합적인 정보.

The elemental analysis market is expected to experience significant growth, increasing from USD 4,518 million in 2025 to USD 6,488.7 million by 2030, at a CAGR of 7.4%.

Scope of the Report

Years Considered for the Study

2024-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD billion)

Segments

Technology, Product Type, End user, and Region

Regions covered

North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa

The elemental analysis and heavy metal testing market has witnessed substantial growth due to a combination of regulatory, technological, and industrial factors. Increasing awareness of the health hazards associated with toxic metals such as lead, arsenic, cadmium, and mercury has prompted governments and organizations to implement stricter regulations on permissible elemental levels in pharmaceuticals, food, cosmetics, and environmental samples. Agencies like the FDA, EPA, and REACH have established stringent testing standards, compelling industries to adopt reliable and precise analytical methods. Technological advancements, including high-sensitivity ICP-OES, ICP-MS, and automated elemental analyzers, have improved the speed, accuracy, and efficiency of testing, making it easier for laboratories to meet regulatory compliance. Additionally, rapid industrialization and urbanization in emerging economies have led to increased environmental contamination, creating higher demand for routine elemental and heavy metal monitoring. Consumer preference for safe, high-quality, contaminant-free products, particularly in healthcare and personal care segments, further drives the adoption of advanced testing solutions. Combined, these factors ensure steady expansion of the global elemental analysis market across sectors and geographies.

"ICP-OES is expected to register the largest CAGR ."

ICP-OES holds the largest share of the elemental analysis market due to its superior performance in multi-element detection. ICP-OES allows simultaneous analysis of major, minor, and trace elements with high sensitivity and precision, making it suitable for diverse applications in pharmaceuticals, environmental monitoring, and food safety. Its wide dynamic range accommodates elements present at both high and low concentrations, reducing the need for multiple instruments or methods. Modern ICP-OES systems are increasingly automated, user-friendly, and capable of handling high sample throughput, enhancing laboratory efficiency. Regulatory acceptance of ICP-OES methods by pharmacopeias and environmental authorities reinforces its adoption in compliance-driven industries. Furthermore, the scalability of ICP-OES-from benchtop units for routine testing to advanced research systems-makes it versatile for laboratories of all sizes. These factors collectively ensure that ICP-OES remains the preferred technology and maintains the largest share in the elemental analysis market.

"The pharmaceutical and biopharmaceutical companies held the largest share of the element alanalysis market in 2024."

Pharmaceutical and biopharmaceutical companies dominate the elemental analysis market due to the critical importance of monitoring elemental impurities in drug products. Regulatory guidelines such as ICH Q3D and USP <232> set strict limits on toxic metals including lead, arsenic, cadmium, and mercury, particularly for orally and parenterally administered medications. Biopharmaceuticals, including monoclonal antibodies, vaccines, and recombinant proteins, require comprehensive elemental profiling to maintain safety, efficacy, and batch-to-batch consistency. The increasing complexity of drug formulations, along with the rising trend of outsourcing testing to contract research organizations (CROs), further drives demand for high-precision elemental analysis instruments. Additionally, pharmaceutical manufacturers prioritize compliance with global standards to facilitate international distribution, reinforcing the adoption of ICP-OES, ICP-MS, and CHNS/O elemental analyzers. Consequently, the pharmaceutical and biopharmaceutical sectors represent the largest application segment in the elemental analysis market, maintaining a strong and consistent share worldwide.

"The Asia Pacific regional segment is expected to register the highest CAGR in the elemental analysis market during the forecast period."

While North America currently leads the elemental analysis market due to established regulatory frameworks, advanced laboratory infrastructure, and a mature pharmaceutical and biotech industry, the Asia-Pacific region is expected to register the highest CAGR in the coming years. Rapid industrialization, expanding pharmaceutical and biotechnology manufacturing, and increased government investment in healthcare infrastructure are major growth drivers. Countries such as China, India, and South Korea are witnessing rising drug production, growing biopharma research, and enhanced adoption of advanced analytical instruments. Regulatory authorities in the region are increasingly enforcing standards for elemental impurities, pushing companies to implement precise and high-throughput testing solutions. Additionally, the expansion of contract research organizations (CROs) and rising awareness of product quality and safety contribute to strong demand. Combined with lower operational costs and a growing skilled workforce, these factors position Asia-Pacific as the fastest-growing market segment for elemental and heavy metal testing, while maintaining global competitiveness.

A breakdown of the primary participants referred to for this report is provided below:

By Company: Tier 1 (35%), Tier 2 (45%), and Tier 3 (20%)

By Designation: C-level Executives (35%), Director-level Executives (25%), and Others (40%)

By Region: North America (40%), Europe (30%), Asia Pacific (20%), Latin America (5%), and the Middle East & Africa (5%)

Prominent players Agilent Technologies Inc. (US), Thermo Fisher Scientific Inc. (US), Bruker Corporation (US), PerkinElmer Inc. (US), Shimadzu Corporation (Japan), SPECTRO Analytical Instruments GmbH (Germany), HORIBA Ltd. (Japan), Analytik Jena AG (Germany), Elementar Analysensysteme GmbH (Germany), Skyray Instruments USA, Inc. (US), GBC Scientific (Australia), Malvern Panalytical Ltd. (UK), Rigaku Holdings Corporation (Japan), LECO Corporation (US), Advion Inc. (US), Teledyne Technologies Incorporated (US), Hitachi High Tech Corporation (Japan), Alpha Measurement Solutions (US), Buck Scientific, Inc. (US), Jeol Ltd. (Japan), PG Instruments Ltd. (UK), Aurora Biomed Inc. (Canada), among others.

Research Coverage

The report studies the elemental analysis market based on brand, product type, procedure, end user, and region.

The report analyzes factors (such as drivers, restraints, opportunities, and challenges) affecting the market growth.

The report evaluates the opportunities and challenges in the market for stakeholders and provides details of the competitive landscape for market leaders.

The report studies micro markets with respect to their growth trends, prospects, and contributions to the global elemental analysis market/heavy metal testing market.

The report forecasts the revenue of market segments with respect to five major regions.

Key Benefits of Buying this Report

This report is valuable for both new and current players in the market, offering essential information to identify potential investment opportunities. It provides a comprehensive overview of both major and minor players, facilitating effective risk analysis and informed investment decisions. The report includes precise segmentation based on end users and geographical regions, offering detailed insights into niche market segments. Additionally, it highlights key trends, growth drivers, challenges, and opportunities, supporting strategic decision-making through a balanced analysis.

Through this report, readers get insightful views into the following parameters:

Analysis of key drivers (Stringent global environmental and food safety regulations, Shift towards outsourced testing), restraints (High capital and operational cost, shortage of skilled labour), opportunities (Rising demand in emerging economies, expanding global water quality monitoring mandates), challenges (high cost of instruments, sample contamination and accuracy concerns), relating to the growth of the elemental analysis market.

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the elemental analysis market/heavy metal testing market.

Market Development: Comprehensive information about lucrative markets - the report analyses the element analysis market across varied regions.

Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the elemental analysis market

Competitive Assessment: A comprehensive analysis of market share, product offerings, and leading strategies of major players, such as Agilent Technologies Inc. (US), Thermo Fisher Scientific Inc. (US), Bruker Corporation (US), PerkinElmer Inc. (US), Shimadzu Corporation (Japan), SPECTRO Analytical Instruments GmbH (Germany), HORIBA Ltd. (Japan), Analytik Jena AG (Germany), Elementar Analysensysteme GmbH (Germany), Skyray Instruments USA, Inc. (US), GBC Scientific (Australia), Malvern Panalytical Ltd. (UK), Rigaku Holdings Corporation (Japan), LECO Corporation (US), Advion Inc. (US), Teledyne Technologies Incorporated (US), Hitachi High Tech Corporation (Japan), Alpha Measurement Solutions (US), Buck Scientific, Inc. (US), Jeol Ltd. (Japan), PG Instruments Ltd. (UK), Aurora Biomed Inc. (Canada)

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS SEGMENTATION & REGIONAL SCOPE

1.3.2 INCLUSIONS & EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.3.4 CURRENCY CONSIDERED

1.4 STAKEHOLDERS

2 EXECUTIVE SUMMARY

3 PREMIUM INSIGHTS

3.1 ELEMENTAL ANALYSIS MARKET/HEAVY METAL ANALYSIS MARKET OVERVIEW

3.2 ELEMENTAL ANALYSIS MARKET/HEAVY METAL ANALYSIS MARKET, BY REGION

3.3 ASIA PACIFIC: ELEMENTAL ANALYSIS MARKET/HEAVY METAL ANALYSIS MARKET, BY COUNTRY AND END USER

3.4 GEOGRAPHIC SNAPSHOT OF ELEMENTAL ANALYSIS MARKET/HEAVY METAL TESTING MARKET

4 MARKET OVERVIEW

4.1 INTRODUCTION

4.2 MARKET DYNAMICS

4.2.1 DRIVERS

4.2.1.1 Stringent global environmental and food-safety regulations

4.2.1.2 Rising public health burden and contamination events

4.2.1.3 Expansion of industrial and resource-extraction activities

4.2.1.4 Shift toward outsourced testing and accredited labs

4.2.2 RESTRAINTS

4.2.2.1 High capital and operating costs

4.2.2.2 Shortage of skilled analytical workforce

4.2.2.3 Limited laboratory infrastructure in emerging economies

4.2.3 OPPORTUNITIES

4.2.3.1 Rising demand in emerging economies

4.2.3.2 Expanding global water quality monitoring mandates

4.2.4 CHALLENGES

4.2.4.1 High cost of advanced analytical instruments

4.2.4.2 Regulatory complexity and variation

4.2.4.3 Sample contamination and accuracy concerns