산업용 패스너 시장 : 재료별, 유형별, 제품별, 용도별, 판매 채널별, 지역별 예측(-2032년)

Industrial Fasteners Market by Material, Type, Product, Application, Sales Channel, and Region - Global Forecast to 2032

상품코드:1944727

리서치사:MarketsandMarkets

발행일:2026년 02월

페이지 정보:영문 483 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

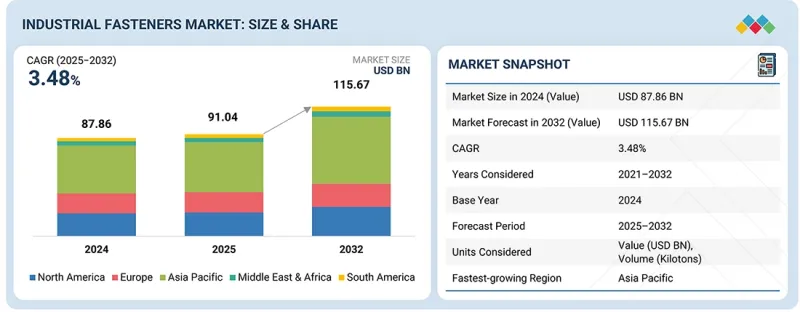

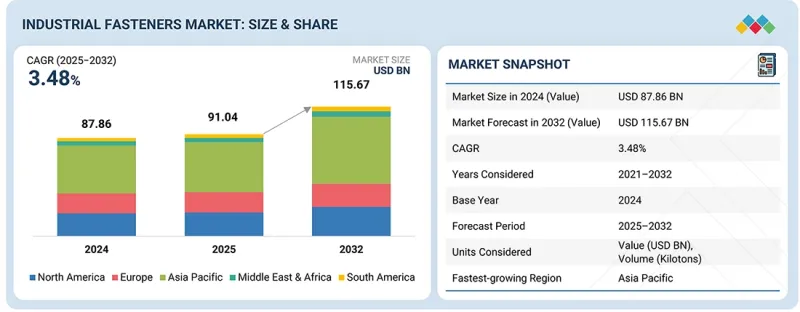

세계 산업용 패스너 시장 규모는 2025년 910억 4,000만 달러로 평가되었고, 2032년까지 1,156억 7,000만 달러에 이를 것으로 예측되며, 예측 기간에 CAGR 3.48%로 성장할 것으로 전망되고 있습니다.

조사 범위

조사 대상 기간

2021-2032년

기준 연도

2024년

예측 기간

2025-2030년

단위

100만 달러/킬로톤

부문

재료, 유형, 제품, 용도, 판매 채널

대상 지역

북미, 아시아태평양, 유럽, 중동, 아프리카, 남미

산업용 패스너 시장은 세계 인프라 투자 증가, 자동차 산업 수요 증가, 제조 기술의 발전으로 급속한 성장이 예상됩니다.

"나사 부문이 예측 기간에 가장 큰 부문이 될 것으로 예측됩니다."

가장 일반적인 산업용 패스너는 나사이며, 확실한 유지력과 용이한 설치 및 제거가 가능하기 때문에 최대 시장 점유율을 차지하고 있습니다. 나사 구조는 조립 부품의 양면에 접근할 필요 없이 높은 클램핑력과 진동 감쇠 효과를 제공합니다. 나사는 금속, 플라스틱, 목재 등 폭넓은 재료에 대응하고 있어 오토메이션을 촉진하여 토크 제어를 가능하게 합니다. 이는 조립 시간 단축과 비용 절감, 유지 보수 경감을 도모하여 대량 생산에 적합합니다.

"간접 판매 부문이 예측 기간에 가장 큰 시장 점유율을 차지할 것으로 예측됩니다."

판매 채널을 기반으로 한 산업용 패스너 시장에서 간접 판매 채널은 가장 큰 점유율을 차지합니다. 이는 패스너의 대부분이 제조업체 자체가 아니라 판매자, 도매업체 및 딜러를 통해 판매되기 때문입니다. 이러한 판매자는 광범위한 제품을 제공하고 대량 구매를 가능하게 하고 쉽게 배송할 수 있으므로 다양한 크기, 재료 및 사양의 지퍼가 필요한 건설, 자동차, 기계 등의 산업에서 필수적입니다. 기술 지원, 재고 관리, 특수 및 인증된 패스너에 대한 신속한 액세스도 간접 채널을 통해 이용 가능하며 최종 사용자의 시간을 절약합니다.

"건축 및 건설 부문은 예측 기간에 두 번째로 큰 성장이 예상됩니다."

산업용 패스너의 두 번째 주요 용도는 건축 및 건설 업계입니다. 주택 및 상업 인프라 건설 프로젝트에서는 구조물 조립, 건물 피복, 인테리어 마감 시공에 대량의 볼트, 나사, 너트, 앵커가 필요합니다. 급속한 도시화, 리노베이션 및 인프라 현대화가 지속적인 수요를 지원합니다. 이 산업에서 사용되는 패스너는 특히 강철 구조, 콘크리트 앵커, 외관 시공에서 강도, 안전성 및 내구성 기준을 충족해야합니다. 또한 조립식 건설과 모듈식 건설의 동향이 패스너 사용 증가를 촉진하고 있으며, 건축 및 건설 업계는 자동차 업계와 제조 업계에 이은 산업용 패스너의 중대하고 안정된 소비 업계입니다.

"금액 기준으로는 아시아태평양의 산업용 패스너 시장이 예측 기간에 가장 높은 CAGR을 나타낼 전망입니다."

아시아태평양 시장은 강력한 제조거점, 첨단 산업화 및 광범위한 인프라 개발을 지원하며 산업용 패스너에서 가장 크고 가장 빠르게 성장하는 시장입니다. 산업용 패스너의 사용은 자동차 조립, 중장비, 인프라, 생산 기계의 기본 요소입니다. 자동차 생산, 산업 생산, 건설 활동 증가에 따라 대량의 지퍼에 대한 수요가 높아지고 있으며, 이 지역은 세계 최대의 산업용 패스너 시장이며, 가장 빠르게 성장하고 있는 시장이 되고 있습니다. 중국, 인도, 한국, 일본 등 주요 제조국도 이 지역에 위치하고 있으며, 시장의 발전을 더욱 촉진하고 있습니다.

이 보고서는 세계 산업용 패스너 시장에 대한 조사 분석을 통해 주요 촉진요인과 억제요인, 제품 개발 및 혁신, 경쟁 구도에 대한 지식을 제공합니다.

목차

제1장 서론

제2장 주요 요약

제3장 중요한 지견

산업용 패스너 시장의 기업에게 매력적인 기회

아시아태평양의 산업용 패스너 : 재료별, 국가별

산업용 패스너 시장 : 유형별

산업용 패스너 시장 : 재료별

산업용 패스너 시장 : 제품별

산업용 패스너 시장 : 용도별

산업용 패스너 시장 : 판매 채널별

산업용 패스너 시장 : 국가별

제4장 시장 개요

시장 역학

성장 촉진요인

억제요인

기회

과제

미충족 수요와 미개척 시장

시공 효율과 현장 생산성

디지털 가시성과 추적성

지속가능성과 순환성에 대한 기대

에너지 전환 시장에 대한 특정 용도용 솔루션

상호접속된 시장과 부문간 기회

상호연결된 시장

부문간 기회

Tier 1/2/3 기업의 전략적 움직임

Tier 1 기업 : 통합과 혁신을 추진하는 세계 리더

Tier 2 기업 : 지역의 혁신자와 틈새 리더

Tier 3 기업 : 민첩한 혁신자 및 전문 공급자

제5장 업계 동향

Porter's Five Forces 분석

거시경제 분석

GDP의 동향과 예측

세계의 산업용 패스너 시장 동향

도시화와 인구동태의 변화

밸류체인 분석

생태계 분석

가격 설정 분석

주요 기업의 평균 판매 가격 동향 : 용도별(2024년)

평균 판매 가격의 동향 : 지역별(2021년-2025년)

무역 분석

HS코드 7318의 수출 데이터

HS코드 7318의 수입 데이터

주요 컨퍼런스 및 이벤트(2025년-2026년)

고객사업에 영향을 주는 동향과 혼란

투자 및 자금조달 시나리오

사례 연구 분석

산업용 패스너 시장에 대한 2025년 미국 관세의 영향

주요 관세율

가격의 영향 분석

각 지역에 중요한 영향

최종 용도 부문에 대한 영향

제6장 고객정세와 구매행동

의사결정 프로세스

구매 프로세스에 참여하는 주요 이해관계자와 그 평가 기준

구매 프로세스의 주요 이해 관계자

구입 기준

채택 장벽과 내부 과제

다양한 용도로부터의 미충족 요구

시장의 수익성

잠재적인 수익

비용역학

마진 기회 : 최종 용도별

자동차

전자

일반 공업

건축 및 건설

중장비

신에너지

태양광

제7장 지속가능성과 규제정세

지역 규제 및 규정 준수

규제기관, 정부기관, 기타 조직

업계 표준

지속가능성에 대한 노력

재생재료

친환경 코팅

냉간 성형 제조 기술

생분해성 폴리머

재생에너지에 의한 제조

지속가능성 대처에 대한 규제정책의 영향

인증, 라벨, 환경 기준

제8장 기술, 특허, 디지털, AI의 채택에 의한 전략적 파괴

주요 신기술

스마트 패스너

적층 조형

하이브리드 패스너

세라믹 패스너

지속 가능 패스너

보완 기술

표면 처리 및 코팅 기술

첨단 제조 기법

지능형 패스너

기술/제품 로드맵

단기 : 재료 최적화 및 디지털 이행 페이즈(2025년-2027년)

중기 : 첨단 재료 및 스마트 매뉴팩처링 페이즈(2027년-2030년)

장기 : 통합 에코시스템 및 차세대 재료 페이즈(2030년-2035년 이후)

특허 분석

접근

문헌 유형

관할분석

주요 출원자

미래의 용도

스마트 센서 통합 패스너(IoT/컨디션 모니터링)

자동 잠금 및 가역형 스마트 패스너

에너지 수확 탑재 패스너

적층 조형 패스너

산업용 패스너 시장에 대한 AI/생성형 AI의 영향

주요 이용 사례와 시장의 장래성

산업용 패스너에 있어서 제조업체/OEM가 따르는 모범 사례

산업용 패스너 시장에서 AI 도입의 사례 연구

상호 연결된 생태계와 시장 기업에 미치는 영향

AI 통합산업용 패스너 채택에 대한 고객의 준비

제9장 산업용 패스너 시장 : 재료별

금속

플라스틱

기타 재료

제10장 산업용 패스너 시장 : 유형별

볼트

나사

너트

와셔

리벳

기타 유형

제11장 산업용 패스너 시장 : 제품별

외부 나사

내부 나사

무나사

항공우주 등급

제12장 산업용 패스너 시장 : 용도별

자동차

건축 및 건설

일반 공업

중장비

전자

신에너지

태양광

기타 용도

제13장 산업용 패스너 시장 : 판매 채널별

직접

간접

제14장 산업용 패스너 시장 : 지역별

북미

미국

캐나다

멕시코

아시아태평양

중국

일본

인도

한국

말레이시아

기타 아시아태평양

유럽

독일

프랑스

이탈리아

영국

스페인

루마니아

슬로바키아

폴란드

체코 공화국

기타 유럽

중동 및 아프리카

GCC 국가

사우디아라비아

아랍에미리트(UAE)

기타 GCC 국가

남아프리카

모로코

기타 중동 및 아프리카

남미

브라질

아르헨티나

기타 남미

제15장 경쟁 구도

개요

주요 진입기업의 전략/강점

수익 분석(2020년-2024년)

시장 점유율 분석(2024년)

기업의 평가와 재무지표(2025년)

브랜드/제품 비교

기업 평가 매트릭스 : 주요 기업(2024년)

기업 평가 매트릭스 : 스타트업/중소기업(2024년)

경쟁 시나리오

제16장 기업 프로파일

주요 기업

ILLINOIS TOOL WORKS INC.

STANLEY BLACK & DECKER, INC.

SFS GROUP AG

LISI GROUP

BULTEN AB

KOELNER RAWLPLUG IP

FONTANA GRUPPO

BIRMINGHAM FASTENER AND SUPPLY INC.

MW INDUSTRIES(MWI)

HILTI GROUP

기타 기업

MACLEAN-FOGG COMPONENT SOLUTIONS(MFCS)

MISUMI GROUP INC.

PRECISION CASTPARTS CORP.

VESCOVINI GROUP

DEEPAK FASTENERS LIMITED

BOLLHOFF GROUP

AGRATI GROUP

KONINKLIJKE NEDSCHROEF

NIFCO INC.

PEINER UMFORMTECHNIK GMBH

PUHL GMBH & CO. KG

GROWERMETAL SPA

SESCO INDUSTRIES

BRUGOLA OEB INDUSTRIALE SPA

SHANGHAI AUTOCRAFT CO., LTD.

제17장 조사 방법

제18장 부록

SHW

영문 목차

영문목차

The industrial fasteners market is projected to grow from USD 91.04 billion in 2025 to USD 115.67 billion in 2032, at a CAGR of 3.48% during the forecast period.

North America, Asia Pacific, Europe, Middle East & Africa, and South America

The industrial fasteners market is poised for rapid growth, driven by rising global infrastructure investments, increasing demand from the automotive sector, and advances in manufacturing technologies.

"The screws segment is projected to be the largest segment during the forecast period."

The most common industrial fasteners are screws, which hold the largest market share due to their ability to provide reliable holding with easy installation and removal. The threaded construction provides a high level of clamping force and vibration damping without requiring access to both sides of an assembly. Screws are compatible with a broad spectrum of materials, including metal, plastic, and wood, which facilitates automation and allows control of torque, saving time and money on assembly and reducing maintenance; they are suitable for mass production.

"The indirect sales segment is projected to hold the largest market share during the forecast period."

The highest share in the market of industrial fasteners on the basis of sales channel is the indirect sales channel due to the fact that the majority of the fasteners are sold by distributors, wholesalers, and dealers as opposed to the manufacturers themselves. These distributors provide a broad range of products, offer bulk purchasing, and can easily deliver them, which is essential in industries such as construction, automotive, and machinery that require fasteners of different sizes, materials, and specifications. Technical assistance, stock keeping, and quicker access to special or certified fasteners are also available through indirect channels, saving the end user time.

"The building & construction segment is expected to have the second-largest growth during the forecast period."

The second-largest application of industrial fasteners is the building & construction industry, as construction projects (residential, commercial, and infrastructure) require large volumes of bolts, screws, nuts, and anchors to assemble structures, clad buildings, and install interior finishes. Constant demand is supported by rapid urbanization, renovation, and infrastructure modernization. The fasteners used in this industry should be based on the strength, safety, and durability standards, particularly in steel structures, concrete anchoring, and facade installations. Also, prefabricated construction and modular building trends are driving increased use of fasteners, as the building and construction industry is a significant, consistent consumer of industrial fasteners, following the automotive and manufacturing industries.

"In terms of value, the Asia Pacific industrial fasteners market is projected to grow at the highest CAGR during the forecast period."

The Asia Pacific market is the largest and fastest-growing market for industrial fasteners, driven by a strong manufacturing base, high industrialization, and broad infrastructure development. Industrial fastening is a basic element in the auto assembly, heavy machinery, infrastructure, and production machinery. With increased vehicle production, industry output, and construction efforts, demand for large quantities of fasteners rises, making the region the largest and fastest-growing market for industrial fasteners worldwide. Some of the leading manufacturing countries, such as China, India, South Korea, and Japan, are also located in the region, further driving market development.

By Company Type: Tier 1: 25%, Tier 2: 42%, and Tier 3: 33%

By Designation: C-level Executives: 20%, Directors: 30%, and Other Designations: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and Middle East & Africa 20%

Notes: Other designations include sales, marketing, and product managers.

Tier 1: >USD 1 Billion; Tier 2: USD 500 million-1 Billion; and Tier 3: <USD 500 million

Companies Covered: Illinois Tool Works Inc. (US), Stanley Black & Decker, Inc. (US), SFS AG (Switzerland), Lisi Group (France), Bulten AB (Sweden), Koelner Rawlplug IP (Poland), FONTANA GRUPPO (Italy), Birmingham Fastener and Supply Inc (US), MW Industries, Inc. (US), and Hilti Group (Liechtenstein), among others, are covered in the report.

The study includes an in-depth competitive analysis of these key players in the industrial fasteners market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the Industrial fasteners market based on by material (metal, plastic, other materials), by type (bolts, screws, nuts, washers, rivets, other types), by product (externally threaded, internally threaded, non-threaded, aerospace grade), by sales channel( direct, indirect), by application (automotive, building & construction, general industrial, heavy equipment, electronics, new energy, solar, other applications), and region (Asia Pacific, North America, Europe, South America, and Middle East & Africa). The report's scope covers detailed information regarding the drivers, restraints, challenges, and opportunities influencing the growth of the industrial fasteners market. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, product offerings, and key strategies, including partnerships, product launches, expansions, and acquisitions, in the industrial fasteners market. This report provides a competitive analysis of upcoming startups in the industrial fasteners market.

Reasons to Buy the Report

The report will provide market leaders/new entrants with information on the closest approximations of revenue for the overall industrial fasteners market and its subsegments. It will help stakeholders understand the competitive landscape, gain deeper insights into positioning their businesses, and plan effective go-to-market strategies. The report will help stakeholders understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

Analysis of key drivers (are increasing demand from the automotive sector, driven by growing infrastructure investments across the globe, and advancements in manufacturing technology), restraints ( Fluctuating raw material prices and replacement by advanced joining technologies), opportunities (Rapid urbanization in Africa and Asia and Expansion in Aerospace & Renewable Energy sector, development of smart fastener solutions, shift towards lightweight high performance and sustainable materials, and demand from growing electronics sector), and challenges (Counterfeiting and quality issues and diverse regional regulations).

Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the industrial fasteners market.

Market Development: Comprehensive information about profitable markets - the report analyzes the industrial fasteners market across varied regions.

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the industrial fasteners market.

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as Illinois Tool Works Inc. (US), Stanley Black & Decker, Inc. (US), SFS AG (Switzerland), Lisi Group (France), Bulten AB (Sweden), Koelner Rawlplug IP (Poland), FONTANA GRUPPO (Italy), Birmingham Fastener and Supply Inc (US), MW Industries, Inc. (US), and Hilti Group (Liechtenstein).

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 MARKET SCOPE

1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.3.4 CURRENCY CONSIDERED

1.3.5 UNITS CONSIDERED

1.4 LIMITATIONS

1.5 STAKEHOLDERS

1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

2.3 DISRUPTIVE TRENDS SHAPING MARKET

2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN INDUSTRIAL FASTENERS MARKET

3.2 ASIA PACIFIC: INDUSTRIAL FASTENERS, BY MATERIAL AND COUNTRY

3.3 INDUSTRIAL FASTENERS MARKET, BY TYPE

3.4 INDUSTRIAL FASTENERS MARKET, BY MATERIAL

3.5 INDUSTRIAL FASTENERS MARKET, BY PRODUCT

3.6 INDUSTRIAL FASTENERS MARKET, BY APPLICATION

3.7 INDUSTRIAL FASTENERS MARKET, BY SALES CHANNEL

3.8 INDUSTRIAL FASTENERS MARKET, BY COUNTRY

4 MARKET OVERVIEW

4.1 INTRODUCTION

4.1.1 DRIVERS

4.1.1.1 Increasing demand for fasteners from automotive sector