소비자용 모바일 비디오 카메라 시장 예측(-2035년) : 제품 유형별, 폼팩터별, 사양별, 사용 사례별, 가격별

Consumer Mobile Video Camera Market by Product Type (Gimbal, Action, 360), Form Factor (Wearable, Handheld, Modular), Specification (Frame Rate, Sensor Size), Use Case (Sports, Vlogging, Education), Price (Flagship, High, Low) - Global Forecast to 2035

상품코드:1942449

리서치사:MarketsandMarkets

발행일:2026년 02월

페이지 정보:영문 271 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

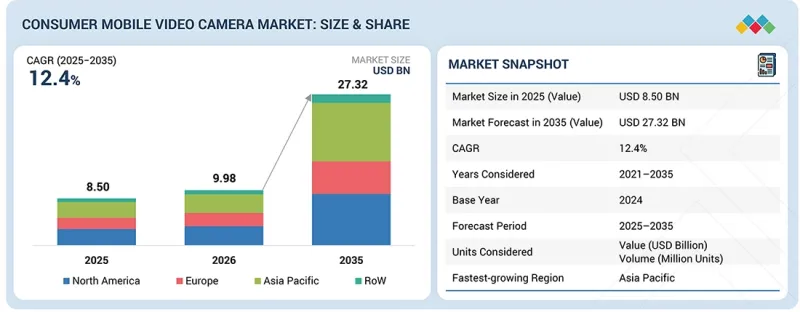

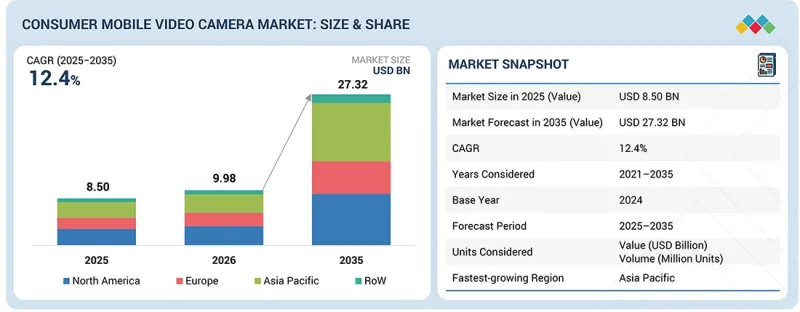

세계의 소비자용 모바일 비디오 카메라 시장 규모는 2025년 85억 달러에서 2035년까지 273억 2,000만 달러에 달할 것으로 예측되며, 예측 기간에 CAGR로 12.4%의 성장이 전망되고 있습니다.

동영상 중심의 소셜미디어 플랫폼과 크리에이터 경제의 폭발적인 확장이 시장의 주요 촉진요인으로 작용하고 있습니다.

조사 범위

조사 대상 기간

2021-2035년

기준연도

2024년

예측 기간

2025-2035년

단위

10억 달러

부문

제품 유형, 폼팩터, 최종사용자, 지역

대상 지역

북미, 유럽, 아시아태평양, 기타 지역

유튜브, 인스타그램, 틱톡과 같은 플랫폼과 신흥 쇼트 비디오 및 라이브 스트리밍 서비스는 동영상 제작을 틈새 취미에서 주류 활동으로 변화시켰습니다. 이러한 변화에 따라 소비자, 특히 프로슈머, 블로거, 세미프로 크리에이터들은 스마트폰이 안정적으로 제공하지 못하는 뛰어난 손떨림 보정, 저조도 성능, 높은 프레임 속도, 영화와 같은 화질을 구현하는 전용 모바일 비디오 카메라에 대한 투자를 진행하고 있습니다. 또한 브랜드 스폰서십, 광고 매출, 제휴 마케팅 등 크리에이터의 수익화 기회 확대, 액션 카메라, 포켓 짐벌 카메라, 360° 카메라로의 업그레이드를 촉진하고 있습니다. 이러한 추세는 중저가 부문 수요를 직접적으로 촉진하고, 2035년까지 온라인/오프라인 판매 채널 전반에서 지속적인 시장 성장을 지원할 것으로 예측됩니다.

"제품 유형별로는 핸드헬드 포켓/짐벌 카메라 부문이 예측 기간 중 가장 큰 시장 점유율을 차지할 것으로 예측됩니다. "

핸드헬드 포켓/짐벌 카메라 부문은 다용도성, 휴대성, 광범위한 사용자층에 대한 매력으로 인해 예측 기간 중 소비자 모바일 비디오 카메라 시장에서 가장 큰 점유율을 차지할 것으로 예측됩니다. 이 카메라는 전문가 수준의 화질과 사용 편의성의 최적의 균형을 실현하여 일반 사용자, 블로거, 프로슈머 모두에게 매력적으로 다가갈 수 있습니다. 기계식 또는 전자식 내장형 손떨림 보정 기능, 컴팩트한 폼팩터, 스마트폰과의 원활한 연결로 복잡한 설정 없이도 부드럽고 영화 같은 영상을 촬영할 수 있습니다. 이 부문은 Vlog 촬영, 여행 컨텐츠 제작, 라이프스타일 촬영의 급증으로 큰 혜택을 받고 있으며, 사용자는 고해상도 동영상, 우수한 저조도 성능, 안정적인 자동 초점 기능을 갖춘 경량 디바이스를 선호합니다. AI 추적, 배터리 수명 연장, 모듈형 액세서리, 짐벌 모터의 개선 등 지속적인 제품 혁신으로 더욱 대중화를 촉진하고 있습니다. 핸드헬드 포켓/짐벌 카메라는 액션캠이나 360° 카메라에 비해 다양한 이용 사례에 대한 유연성을 제공하고, 일상적인 컨텐츠 제작, 전문적인 스토리텔링, 소셜미디어 포스팅을 지원함으로써 시장 전반에서 우위를 점하고 있습니다. 유지하고 있습니다.

"온라인 판매 채널은 예측 기간 중 소비자 모바일 비디오 카메라 시장에서 주요 점유율을 차지할 것으로 예측됩니다. "

온라인 판매 채널은 소비자 구매 행동의 변화와 디지털 소매 생태계의 확장으로 인해 예측 기간 중 소비자 모바일 비디오 카메라 시장에서 지배적인 점유율을 차지할 것으로 예측됩니다. E-Commerce 플랫폼은 가격대, 브랜드, 사양에 상관없이 다양한 제품 선택권을 소비자에게 쉽게 제공하고, 리뷰, 비교 툴, 동영상 데모를 통해 정보에 입각한 구매 결정을 할 수 있도록 돕습니다. 모바일 비디오 카메라와 같은 첨단 기술을 활용한 제품에서는 온라인 채널이 특히 효과적으로 기능적 차별성, 소프트웨어 능력, 액세서리 호환성 등의 정보를 전달합니다. 제조업체의 소비자 직접 판매(DTC) 전략의 부상과 더불어 온라인 전용 할인, 번들 제공, 할부 옵션의 빈번한 제공은 온라인 채택을 더욱 가속화하고 있습니다. 또한 크리에이터와 프로슈머는 새로운 출시 모델과 생태계 액세서리에 대한 빠른 접근을 위해 온라인 채널을 선호하는 경향이 있습니다. 물류 개선, 유연한 반품 정책, 강력한 애프터 서비스 지원은 소비자의 신뢰를 강화하고, 온라인 판매는 시장의 주요 수입원이 되고 있습니다.

세계의 소비자용 모바일 비디오 카메라 시장에 대해 조사 분석했으며, 주요 촉진요인과 저해요인, 제품 개발 및 혁신, 경쟁 구도에 대해 조사 분석하여 전해드립니다.

목차

제1장 서론

제2장 개요

제3장 중요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 소비자용 모바일 비디오 카메라 사양

제10장 소비자용 모바일 비디오 카메라 시장 : 제품 유형별

제11장 소비자용 모바일 비디오 카메라 시장 : 폼팩터별

제12장 소비자용 모바일 비디오 카메라 시장 : 가격별

제13장 소비자용 모바일 비디오 카메라 시장 : 최종사용자별

제14장 소비자용 모바일 비디오 카메라 시장 : 사용 사례별

제15장 소비자용 모바일 비디오 카메라 시장 : 판매 채널별

제16장 소비자용 모바일 비디오 카메라 시장 : 지역별

제17장 경쟁 구도

제18장 기업 개요

제19장 조사 방법

제20장 부록

KSA

영문 목차

영문목차

The global consumer mobile video camera market is projected to grow from USD 8.50 billion in 2025 to USD 27.32 billion by 2035, registering a CAGR of 12.4% during the forecast period. The explosive rise of video-centric social media platforms and the creator economy is a primary driving factor for the market.

Scope of the Report

Years Considered for the Study

2021-2035

Base Year

2024

Forecast Period

2025-2035

Units Considered

Value (USD Billion)

Segments

By Product type, Form Factor, End User and Region

Regions covered

North America, Europe, APAC, RoW

Platforms such as YouTube, Instagram, and TikTok, and emerging short-form and live-streaming services have transformed video creation from a niche hobby into a mainstream activity. This shift is pushing consumers, especially prosumers, vloggers, and semi-professional creators, to invest in dedicated mobile video cameras that deliver superior stabilization, low-light performance, high frame rates, and cinematic video quality beyond what smartphones can consistently offer. Additionally, the growing monetization opportunities for creators, including brand sponsorships, ad revenue, and affiliate marketing, are encouraging upgrades to action cameras, pocket gimbal cameras, and 360° cameras. This trend directly drives demand across mid- to high-price segments and supports sustained market growth across online and offline sales channels through 2035.

"By product type, the handheld pocket/gimbal cameras segment is expected to capture the largest market share during the forecast period."

The handheld pocket/gimbal cameras segment is expected to capture the largest market share in the consumer mobile video camera market during the forecast period, driven by its versatility, portability, and broad appeal across user groups. These cameras strike an optimal balance between professional-grade video quality and ease of use, making them highly attractive to general users, vloggers, and prosumers alike. Integrated mechanical or electronic stabilization, compact form factors, and seamless smartphone connectivity enable smooth, cinematic footage without requiring complex setups. The segment benefits significantly from the surge in vlogging, travel content creation, and lifestyle videography, where users prioritize lightweight devices with high-resolution video, strong low-light performance, and reliable autofocus. Continuous product innovation, such as AI-assisted tracking, enhanced battery life, modular accessories, and improved gimbal motors, is further expanding adoption. Compared to action and 360° cameras, handheld pocket/gimbal cameras offer wider use-case flexibility, supporting daily content creation, professional storytelling, and social media publishing, thereby sustaining their dominance in the overall market.

"Online sales channel is expected to hold the dominant share of the consumer mobile video camera market during the forecast period."

The online sales channel is projected to account for the dominant share of the consumer mobile video camera market during the forecast period, supported by changing consumer purchasing behavior and expanding digital retail ecosystems. E-commerce platforms provide consumers with easy access to a wide range of product options across price bands, brands, and specifications, enabling informed purchase decisions through reviews, comparison tools, and video demonstrations. For technologically advanced products such as mobile video cameras, online channels are particularly effective in communicating feature differentiation, software capabilities, and accessory compatibility. The rise of direct-to-consumer (DTC) strategies by manufacturers, combined with frequent online-exclusive discounts, bundled offerings, and financing options, further accelerates online adoption. Additionally, creators and prosumers often prefer online channels for faster access to newly launched models and ecosystem accessories. Improved logistics, flexible return policies, and strong after-sales support are reinforcing consumer confidence, positioning online sales as the primary revenue-generating channel for the market.

"The Asia Pacific is emerging as the fastest-growing region in the consumer mobile video camera market."

The Asia Pacific is projected to be the fastest-growing regional market during the forecast period, driven by rapid digitalization, a large creator population, and expanding middle-class consumer bases. Countries such as China, India, Japan, and South Korea are witnessing strong growth in social media usage, short-video platforms, and live-streaming ecosystems, which directly fuel demand for dedicated video recording devices. Rising disposable incomes and increased affordability of mid-range cameras are enabling first-time buyers to upgrade from smartphones to specialized mobile video cameras. The region also benefits from a strong manufacturing ecosystem, frequent product launches, and competitive pricing by regional and global players. Additionally, the growing adoption of video-based education, e-commerce product showcasing, and event documentation is broadening use cases beyond entertainment. Government support for digital content creation and technology adoption further strengthens the growth outlook, positioning the Asia Pacific as a key engine of future market expansion.

Breakdown of primaries

A variety of executives from key organizations operating in the consumer mobile video camera market have been interviewed in-depth, including CEOs, marketing directors, and innovation and technology directors.

By Company Type: Tier 1 -20%, Tier 2 - 45%, and Tier 3 - 35%

By Designation: C-level Executives - 35%, Directors - 40%, and Others - 25%

By Region: North America - 25%, Europe - 30%, Asia Pacific - 35%, and RoW - 10%

Note: The RoW region includes the Middle East, Africa, and South America. Other designations include product, sales, and marketing managers. Three tiers of companies have been defined based on their total revenues: Tier 3: revenue less than USD 100 million; Tier 2: revenue between USD 100 million and USD 1 billion; and Tier 1: revenue more than USD 1 billion.

Major players profiled in this report are as follows: Major players operating in the consumer mobile video camera market include DJI (China), GoPro Inc. (US), Insta360 (China), Sony Corporation (Japan), Ricoh (Japan), AKASO Tech LLC (US), SJCAM (China), Nikon Corporation (Japan), and Panasonic Holdings Corporation (Japan).

These companies compete by continuously expanding their consumer mobile video camera portfolios, improving video resolution, image stabilization, low-light performance, and audio capture quality, and supporting diverse use cases across sports, travel, vlogging, education, and professional content creation. Strategic focus areas include compact and modular camera designs, AI-enabled shooting modes, seamless smartphone and cloud integration, and broad accessory ecosystems to enhance usability and creative flexibility. Manufacturers also emphasize durability, battery efficiency, and compatibility with editing and social media platforms to address evolving creator needs. Continued investment in imaging sensors, software-driven features, connectivity, and direct-to-consumer digital sales strategies is expected to sustain competition and drive steady innovation across the global consumer mobile video camera market.

The study provides a detailed competitive analysis of these key players in the consumer mobile video camera market, presenting their company profiles, most recent developments, and key market strategies.

Research Coverage

This report on the consumer mobile video camera market presents a detailed analysis based on product type, form factor, price range, use case, sales channel, end user, and region. By product type, the market is segmented into handheld pocket/gimbal cameras, action cameras, and 360-degree cameras. By form factor, the market is segmented into handheld, wearable/mountable/clip-on, and modular convertible. By price range, the market is segmented into low (<USD 300), medium (USD 300 to 500), high (USD 500 to 700), and flagship above 700. By use case, the market is segmented into sports & adventure, vlogging/social media, education & training, and real estate & events. By sales channel, the market is segmented into online and offline. By end user, the market is segmented into general users, prosumers/creators/vloggers, and professionals. The regional analysis covers North America, Europe, the Asia Pacific, and the Rest of the World, supporting evaluation of adoption patterns, growth drivers, and technology trends shaping the global consumer mobile video camera market.

Reasons to buy the report

The report will help the leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall market and the sub-segments. It will also help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report will help stakeholders understand the consumer mobile video camera market's pulse and provide information on key market drivers, restraints, challenges, and opportunities.

Key Benefits of Buying the Report

Analysis of key drivers (rapid growth of social media, vlogging, and creator economy, rising popularity of adventure sports, travel, and experiential lifestyles, continuous advancements in camera technology and mobile ecosystem integration), restraints (strong competition from advanced smartphone camera systems, limited product differentiation in lower-priced segments), opportunities (growing adoption of immersive, 360°, and spatial video content, expanding creator communities in emerging markets), and challenges (rapid technological change and short product lifecycles, price sensitivity, brand dominance, and customer retention) influencing the growth of the consumer mobile video camera market

Product Development/Innovation: Detailed insights into upcoming technologies, research and development activities, and product launches in the consumer mobile video camera market

Market Development: Comprehensive information about lucrative markets (the report analyzes the consumer mobile video camera market across varied regions)

Market Diversification: Exhaustive information about new products/services, untapped geographies, recent developments, and investments in the consumer mobile video camera market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like DJI (China), GoPro Inc. (US), Insta360 (China), Sony Corporation (Japan), Ricoh (Japan), AKASO Tech LLC (US), SJCAM (China), Nikon Corporation (Japan), and Panasonic Holdings Corporation (Japan).

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 UNIT CONSIDERED

1.6 STAKEHOLDERS

2 EXECUTIVE SUMMARY

2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

2.3 DISRUPTIONS SHAPING CONSUMER MOBILE VIDEO CAMERA MARKET

2.4 HIGH-GROWTH SEGMENTS

2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN CONSUMER MOBILE VIDEO CAMERA MARKET

3.2 CONSUMER MOBILE VIDEO CAMERA MARKET IN NORTH AMERICA, BY PRODUCT TYPE AND COUNTRY

3.3 CONSUMER MOBILE VIDEO CAMERA MARKET IN NORTH AMERICA, BY PRODUCT TYPE

3.4 CONSUMER MOBILE VIDEO CAMERA MARKET, BY GEOGRAPHY

4 MARKET OVERVIEW

4.1 INTRODUCTION

4.2 MARKET DYNAMICS

4.2.1 DRIVERS

4.2.1.1 Evolution of social media and video-centric digital experiences

4.2.1.2 Growing emphasis on adventure sports, travel, and experience-driven lifestyles

4.2.1.3 Rising innovation in video recording and image stabilization

4.2.2 RESTRAINTS

4.2.2.1 Intense competition from advanced smartphone camera systems

4.2.2.2 Limited product differentiation in lower-priced segments

4.2.3 OPPORTUNITIES

4.2.3.1 Growing popularity of 360° and spatial video content

4.2.3.2 Expanding content creator communities in emerging economies

4.2.4 CHALLENGES

4.2.4.1 Issues in managing short product lifecycles and rapid innovation cycles

4.2.4.2 Price sensitivity, brand dominance, and customer retention constraints

4.3 UNMET NEEDS AND WHITE SPACES

4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

5.1 INTRODUCTION

5.2 PORTER'S FIVE FORCES ANALYSIS

5.2.1 THREAT OF NEW ENTRANTS

5.2.2 THREAT OF SUBSTITUTES

5.2.3 BARGAINING POWER OF SUPPLIERS

5.2.4 BARGAINING POWER OF BUYERS

5.2.5 INTENSITY OF COMPETITIVE RIVALRY

5.3 MACROECONOMIC OUTLOOK

5.3.1 INTRODUCTION

5.3.2 GDP TRENDS AND FORECAST

5.3.3 TRENDS IN GLOBAL SPORTS & ADVENTURE INDUSTRY

5.3.4 TRENDS IN GLOBAL SOCIAL MEDIA & VLOGGING INDUSTRY

5.4 VALUE CHAIN ANALYSIS

5.5 ECOSYSTEM ANALYSIS

5.6 PRICING ANALYSIS

5.6.1 AVERAGE SELLING PRICE OF CONSUMER MOBILE VIDEO CAMERAS OFFERED BY KEY PLAYERS, BY PRODUCT TYPE, 2024

5.6.2 AVERAGE SELLING PRICE TREND OF CONSUMER MOBILE VIDEO CAMERAS, BY REGION, 2021-2024

5.7 TRADE ANALYSIS

5.7.1 IMPORT SCENARIO (HS CODE 852580)

5.7.2 EXPORT SCENARIO (HS CODE 852580)

5.8 KEY CONFERENCES AND EVENTS, 2026

5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.10 INVESTMENT AND FUNDING SCENARIO

5.11 CASE STUDY ANALYSIS

5.11.1 SCOTTIE DAVISON ADOPTS RICOH THETA 360-DEGREE CAMERA TO ENHANCE REAL ESTATE CONTENT CREATION