액랭식 EV 충전 케이블 시장 : 케이블 전력량별, 케이블 길이별, 케이블 직경별, 용도별, 외장재별, 냉각액별, 지역별 - 세계 예측(-2032년)

Liquid Cooled EV Charging Cable Market by Cable Power Capacity, Cable Length, Cable Diameter, Application, Jacket Material, Cooling Fluid, and Region - Global Forecast to 2032

상품코드:1936069

리서치사:MarketsandMarkets

발행일:2026년 01월

페이지 정보:영문 266 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

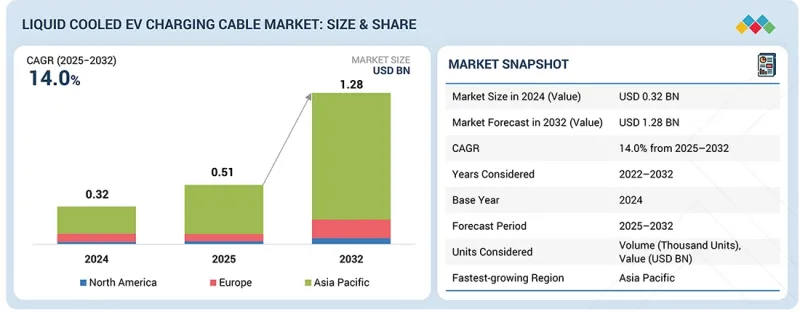

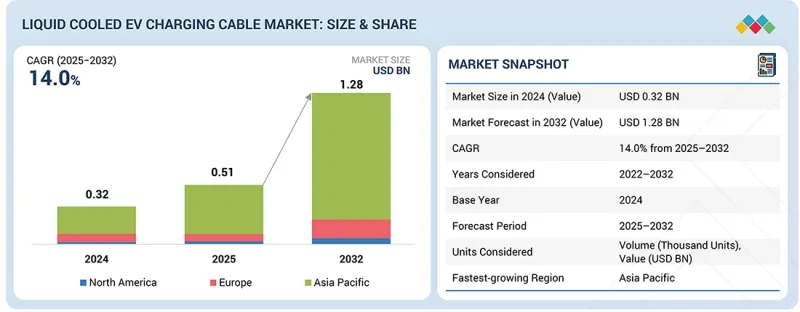

세계의 액랭식 EV 충전 케이블 시장 규모는 2025년 5억 1,000만 달러에서 2032년까지 12억 8,000만 달러에 달할 것으로 예측되며, CAGR로 14.0%의 성장이 전망됩니다.

차량 플랫폼이 800V 전기 아키텍처의 채택을 늘리면서 시장은 발전하고 있습니다. 또한, 높은 시스템 전압은 더 빠른 충전을 가능하게 하는 동시에 케이블 레벨의 전류 및 열 관리 요구 사항을 높입니다.

조사 범위

조사 대상 기간

2022-2032년

기준 연도

2024년

예측 기간

2025-2032년

단위

1,000대, 100만 달러

부문

케이블 전력량, 케이블 길이, 케이블 직경, 용도, 외장재, 냉각액

대상 지역

아시아태평양, 유럽, 북미

충전 인프라 사업자들은 안전과 취급을 해치지 않고 반복적인 고출력 충전 세션을 견딜 수 있는 케이블 솔루션을 중요하게 여깁니다. 수랭식 냉각은 고부하에서 열 안정성을 유지하면서 컴팩트한 케이블 설계를 지원합니다. 이와 함께 충전기 플랫폼 간의 표준화가 진행됨에 따라 각 지역에서의 배포가 단순화되고, 유연성과 인체공학적 설계의 개선이 공공 및 상업용 충전 시설에서의 보급 확대를 지원하고 있습니다.

"용도별로는 초급속 충전 부문이 예측 기간 동안 가장 큰 시장 규모를 차지할 것으로 예상됩니다."

초급속 충전 부문은 수랭식 EV 충전 케이블 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다. 이는 현재 전 세계 EV 차량의 대부분을 차지하는 승용 EV와 소형 상용차의 대규모 수요에 대응하기 위함입니다. 특히 고속도로 및 도시 회랑을 따라 공공 및 준공공 충전 인프라의 규모는 전기자동차 보급 증가에 대응하기 위해 빠르게 확대되고 있으며, 350kW 이상의 충전소를 광범위하게 배치할 수 있는 기회를 창출하고 있습니다. 메가 와트급 충전은 상대적으로 소수의 대형 상용차 및 특정 고급 전기자동차를 대상으로 하는 반면, 초급속 충전은 빈번하고 단시간 충전이 필요한 훨씬 더 큰 규모의 차량 기반에 활용되기 때문에 수랭식 케이블의 지속적인 사용을 촉진합니다. 또한, 고급 승용차에서 800V EV 아키텍처의 보급은 수랭식 솔루션에 대한 수요를 가속화시키고 있습니다. 이 차량은 더 높은 전류를 안전하고 효율적으로 전환할 수 있기 때문입니다.

"케이블 길이별로는 5-8m 부문이 예측 기간 동안 가장 큰 시장 규모를 차지할 것으로 예상됩니다."

5-8m 부문이 예측 기간 동안 수랭식 EV 충전 케이블 시장을 독점할 것으로 예상됩니다. 이는 고출력 충전 현장에서 전기적 성능, 열 제어, 배치 경제성 사이에서 가장 효율적인 균형을 이루는 케이블이기 때문입니다. 이 케이블은 고전류 DC 충전 시 전압 강하와 신호 감쇠를 최소화하면서 장거리 케이블에 따른 과도한 구리 재료, 냉각액량, 보강 비용을 피할 수 있습니다. 낮은 압력 손실로 냉각수 순환을 최적화할 수 있어 지속적인 초고속 충전 시에도 도체 온도를 안정적으로 유지합니다. 이 정도 길이의 케이블은 표준 충전기 받침대나 주차 레이아웃 주변에서 유연한 배선 경로를 확보할 수 있으며, 추가 연결부나 커넥터를 도입할 필요가 없습니다. 이를 통해 설치 시간을 단축하고 잠재적인 고장 지점을 줄일 수 있습니다. 충전기 제조업체와 사업자들은 대규모 공공 급속 충전 시설에서 가장 신뢰할 수 있고 비용 효율적인 사양으로 이 길이를 표준화하고 있습니다.

"유럽은 예측 기간 동안 가장 빠르게 성장하는 시장이 될 것으로 예상됩니다."

유럽은 공공 및 차량용 충전 인프라가 고출력 DC 및 초급속 충전으로 전환하면서 수랭식 EV 충전 케이블 시장에서 가장 빠르게 성장하는 지역으로 부상하고 있습니다. 유럽 자동차 제조업체들은 800V 차량 플랫폼을 적극적으로 개발하고 있으며, 이로 인해 충전 인터페이스의 전류 밀도가 증가하여 고출력 수준에서 공랭식 케이블의 실용성이 떨어지고 있습니다. 공공 충전 사업자들은 고속도로, 도심 허브, 물류 회랑 등에 150kW-350kW급 충전기를 증설하고 있으며, 높은 가동률로 인해 열적 한계에 부딪히고 있습니다. 따라서 수랭식 케이블은 열 관리, 인체공학적 디자인 개선, 연속 사용 시 충전 안정성 유지에 대한 최적의 솔루션이 되고 있습니다. 지역 경쟁 상황에는 HUBER+SUHNER(스위스), Phoenix Contact(독일), Leoni(독일) 등 세계 공급업체와 현지 공급업체가 진출해 있습니다.

세계의 수랭식 EV 충전 케이블 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도에 대한 정보를 전해드립니다.

목차

제1장 소개

제2장 주요 요약

제3장 중요한 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 용도

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 액랭식 EV 충전 케이블 시장 : 용도별

제10장 액랭식 EV 충전 케이블 시장 : 케이블 직경별

제11장 액랭식 EV 충전 케이블 시장 : 케이블 길이별

제12장 액랭식 EV 충전 케이블 시장 : 냉각 기술별

제13장 액랭식 EV 충전 케이블 시장 : 외장재별

제14장 액랭식 EV 충전 케이블 시장 : 케이블 전력량별

제15장 액랭식 EV 충전 케이블 시장 : 지역별

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 부록

KSM

영문 목차

영문목차

The liquid cooled EV charging cable market is projected to grow from USD 0.51 billion in 2025 to USD 1.28 billion by 2032, at a CAGR of 14.0%. The market is advancing as vehicle platforms are increasingly adopting 800 V electrical architectures. Additionally, high system voltages are enabling faster charging and raising current and thermal management requirements at the cable level.

Charging infrastructure operators are prioritizing cable solutions that can sustain repeated high-power charging sessions without compromising safety or handling. Liquid cooling supports compact cable designs while maintaining thermal stability under elevated loads. In parallel, increasing standardization across charger platforms is simplifying deployment across regions, while improvements in flexibility and ergonomics are supporting broader adoption in public and commercial charging locations.

"By application, the ultrafast charging segment is projected to account for the largest market during the forecast period."

The ultrafast charging segment is projected to account for the largest share in the liquid cooled EV charging cable market because it addresses the immediate high-volume demand of passenger EVs and light commercial vehicles, which represent the majority of global EV fleets today. The scale of public and semi-public charging infrastructure, particularly along highways and urban corridors, is expanding rapidly to meet rising EV adoption, creating extensive deployment opportunities for 350 kW and above charging stations. Unlike megawatt charging, which targets a relatively smaller fleet of heavy-duty vehicles and select luxury EVs, ultrafast charging serves a far larger base of vehicles requiring frequent, short-duration charges, driving consistent utilization of liquid cooled cables. Additionally, the growth of 800 V EV architectures in high-end passenger vehicles is accelerating the need for liquid cooled solutions, as these vehicles can exploit higher current flows safely and efficiently.

"By cable length, the 5-8 meters segment is projected to account for the largest market during the forecast period."

The 5-8 meters segment is projected to dominate the liquid cooled EV charging cable market during the forecast period as these cables deliver the most efficient balance between electrical performance, thermal control, and deployment economics at high-power charging sites. These cables minimize voltage drop and signal dilution during high current DC charging while avoiding the excess copper, coolant volume, and reinforcement costs associated with longer cable runs. They allow optimized coolant circulation with lower pressure losses, which helps maintain stable conductor temperatures during sustained ultra-fast charging. Cables in this length range enable flexible cable routing around standard charger pedestals and vehicle parking layouts without introducing additional joints or connectors, reducing installation time and potential failure points. Charger manufacturers and operators are standardizing this length as the most reliable and cost-efficient specification for large-scale public fast charging deployments.

"Europe is projected to be the fastest-growing market during the forecast period."

Europe is emerging as the fastest-growing region in the liquid cooled EV charging cable market, as public and fleet charging infrastructure is increasingly shifting toward high-power DC and ultrafast charging. Automakers in Europe are actively deploying 800 V vehicle platforms, which are increasing current density at charging interfaces and making air-cooled cables less practical at high power levels. Public charging operators are installing more 150 kW to 350 kW chargers along highways, urban hubs, and logistics corridors, where high utilization rates are pushing thermal limits. Liquid cooled cables are therefore becoming the preferred solution to manage heat, improve ergonomics, and maintain charging consistency under continuous use. Regional competitive landscape includes global and local suppliers, such as HUBER+SUHNER (Switzerland), Phoenix Contact (Germany), and Leoni (Germany).

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in this market.

By Company Type: EV Charging Cable Manufacturers - 40%, Charging Station Providers - 40%, Others - 20%

By Country: North America - 30%, Europe - 30%, Asia Pacific - 40%

The liquid cooled EV charging cable market is dominated by global players such as Phoenix Contact (Germany), HUBER+SUHNER (Switzerland), BRUGG eConnect (Switzerland), Sinbon Electronics Co., Ltd. (Taiwan), and LEONI (Germany). These companies have adopted strategies such as product launches, strategic deals, and geographic expansions to strengthen their market presence and technological capabilities.

Research Coverage:

The report covers the liquid cooled EV charging cable market by cable power capacity (300-499 kW, 500-900 kW, above 900 kW), application (ultrafast charging and megawatt charging), cable length (below 5 meters, 5-8 meters, and above 8 meters), cable diameter (below 30 mm, 30-50 mm, and above 50 mm), jacket material (rubber, thermoplastic elastomer, and polyvinyl chloride), cooling fluid (water glycol and others), and region (Asia Pacific, Europe and North America). It covers the competitive landscape and company profiles of the major players in the liquid cooled EV charging cable market ecosystem.

The study also includes an in-depth competitive analysis of the key players in the market, along with their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report:

This report will help market leaders/new entrants in this market with information on the closest approximations of revenue numbers for the overall testing of the liquid cooled EV charging cable ecosystem and its subsegments.

This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies.

This report will also help stakeholders understand the market's pulse and provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

Analysis of key drivers (rising demand for ultrafast and megawatt charging, growing shift to 800 V EV Architecture, need for improved cable design with quick heat dissipation qualities), restraints (high maintenance cost, high installation and service complexity), challenges (regulatory uncertainty with coolant systems), and opportunities (advancements in dielectric coolants and material technology, growing use case for heavy duty truck charging)

Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product launches in the liquid cooled EV charging cable market

Market Development: Comprehensive information about lucrative markets across varied regions

Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the liquid cooled EV charging cable market

Competitive Assessment: In-depth assessment of market ranking, growth strategies, and service offerings of leading players like Phoenix Contact (Germany), HUBER+SUHNER (Switzerland), BRUGG eConnect (Switzerland), Sinbon Electronics Co., Ltd. (Taiwan), and LEONI (Germany), among others, in the liquid cooled EV charging cable market

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

1.3.2 INCLUSIONS & EXCLUSIONS

1.4 YEARS CONSIDERED

1.5 CURRENCY CONSIDERED

1.6 STAKEHOLDERS

2 EXECUTIVE SUMMARY

2.1 MARKET HIGHLIGHTS & KEY INSIGHTS

2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

2.3 DISRUPTIVE TRENDS IN LIQUID COOLED EV CHARGING CABLE MARKET

2.4 HIGH GROWTH SEGMENTS

2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN LIQUID COOLED EV CHARGING CABLE MARKET

3.2 LIQUID COOLED EV CHARGING CABLE MARKET, BY CABLE POWER CAPACITY

3.3 LIQUID COOLED EV CHARGING CABLE MARKET, BY APPLICATION

3.4 LIQUID COOLED EV CHARGING CABLE MARKET, BY CABLE LENGTH

3.5 LIQUID COOLED EV CHARGING CABLE MARKET, BY CABLE DIAMETER

3.6 LIQUID COOLED EV CHARGING CABLE MARKET, BY JACKET MATERIAL

3.7 LIQUID COOLED EV CHARGING CABLE MARKET, BY COOLING FLUID

3.8 LIQUID COOLED EV CHARGING CABLE MARKET, BY REGION

4 MARKET OVERVIEW

4.1 INTRODUCTION

4.2 MARKET DYNAMICS

4.2.1 DRIVERS

4.2.1.1 Rising demand for ultrafast and megawatt charging

4.2.1.2 Growing shift to 800V EV architecture

4.2.1.3 Need for improved cable design with fast heat dissipation qualities

4.2.2 RESTRAINTS

4.2.2.1 High maintenance cost

4.2.2.2 High installation and service complexity

4.2.3 OPPORTUNITIES

4.2.3.1 Advancements in dielectric coolant and material technology

4.2.3.2 Increasing use cases for heavy-duty truck charging

4.2.4 CHALLENGES

4.2.4.1 Regulatory uncertainty with coolant systems

4.3 UNMET NEEDS AND WHITE SPACES

4.3.1 SIMPLIFIED AND LOW-MAINTENANCE COOLANT MANAGEMENT

4.3.2 LACK OF HARMONIZED SAFETY AND CERTIFICATION STANDARDS FOR COOLANTS

4.3.3 COST-OPTIMIZED SOLUTIONS FOR MID-POWER FAST CHARGING (250-350 KW)

4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

4.5 STRATEGIC MOVES BY KEY PLAYERS IN LIQUID COOLED EV CHARGING CABLE MARKET

5 INDUSTRY TRENDS

5.1 PORTER'S FIVE FORCES ANALYSIS

5.1.1 THREAT FROM NEW ENTRANTS

5.1.2 BARGAINING POWER OF SUPPLIERS

5.1.3 BARGAINING POWER OF BUYERS

5.1.4 THREAT FROM SUBSTITUTES

5.1.5 INTENSITY OF COMPETITIVE RIVALRY

5.2 MACROECONOMIC INDICATORS

5.2.1 INTRODUCTION

5.2.2 GDP TRENDS AND FORECAST

5.2.3 TRENDS IN GLOBAL LIQUID COOLED EV CHARGING CABLE INDUSTRY

5.2.4 TRENDS IN GLOBAL AUTOMOTIVE & TRANSPORTATION INDUSTRY

5.3 SUPPLY CHAIN ANALYSIS

5.4 ECOSYSTEM ANALYSIS

5.4.1 RAW MATERIAL AND COMPONENT SUPPLIERS

5.4.2 LIQUID COOLED EV CHARGING CABLE AND CONNECTOR MANUFACTURERS

5.4.3 THERMAL MANAGEMENT AND COOLING TECHNOLOGY PROVIDERS

5.4.4 CHARGING EQUIPMENT OEMS

5.4.5 VEHICLE OEMS

5.4.6 EV CHARGING INFRASTRUCTURE OPERATORS

5.4.7 TESTING, CERTIFICATION, AND STANDARD BODIES

5.5 PRICING ANALYSIS

5.5.1 AVERAGE SELLING PRICE FOR LIQUID COOLED EV CHARGING CABLES, BY KEY PLAYER

5.5.2 AVERAGE SELLING PRICE TREND, BY REGION

5.5.3 INDICATIVE PRICING ANALYSIS, BY CABLE POWER CAPACITY

5.6 TRADE ANALYSIS

5.6.1 IMPORT SCENARIO

5.6.2 EXPORT SCENARIO

5.7 KEY CONFERENCES & EVENTS, 2026-2027

5.8 TRENDS & DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.9 INVESTMENT & FUNDING SCENARIO

5.10 CASE STUDY ANALYSIS

5.10.1 ENABLING ULTRAFAST CHARGING THROUGH LIQUID COOLED CABLE ARCHITECTURE

5.10.2 SCALING HIGH-POWER CHARGING THROUGH DEPLOYMENT OF LIQUID COOLED CABLES

5.10.3 IMPROVING RELIABILITY OF DC FAST CHARGING CABLES THROUGH LIQUID COOLING

5.10.4 DEPLOYING LIQUID COOLED CHARGING CABLES TO SUPPORT RELIABLE HIGH-POWER DC CHARGING

5.10.5 INTEGRATION OF LIQUID COOLED CABLES IN ULTRAFAST DC CHARGING SYSTEMS

5.11 IMPACT OF 2025 US TARIFF

5.11.1 INTRODUCTION

5.11.2 KEY TARIFF RATES

5.11.3 PRICE IMPACT ANALYSIS

5.11.4 IMPACT ON COUNTRY/REGION

5.11.4.1 US

5.11.4.2 Europe

5.11.4.3 Asia Pacific

5.11.5 IMPACT ON END-USE INDUSTRIES

5.12 MNM INSIGHTS INTO KEY PLAYERS

5.13 EV CHARGING POINTS ACROSS REGIONS

5.13.1 PARC GLOBAL EV CHARGING POINTS, 2021-2024 (THOUSAND UNITS)

5.13.2 PARC GLOBAL EV CHARGING POINTS, 2025-2032 (THOUSAND UNITS)

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

6.1 KEY EMERGING TECHNOLOGIES

6.1.1 FLUORINATED DIELECTRICS IN LIQUID COOLED EV CHARGING CABLES