메타텅스텐산 암모늄 시장 : 원료별, 형태별, 등급별, 용도별, 최종 이용 산업별, 지역별 - 세계 예측(-2030년)

Ammonium Metatungstate Market by Raw Material, Form, Grade, Application, End-use Industry, and Region - Global Forecast to 2030

상품코드:1936065

리서치사:MarketsandMarkets

발행일:2026년 02월

페이지 정보:영문 230 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

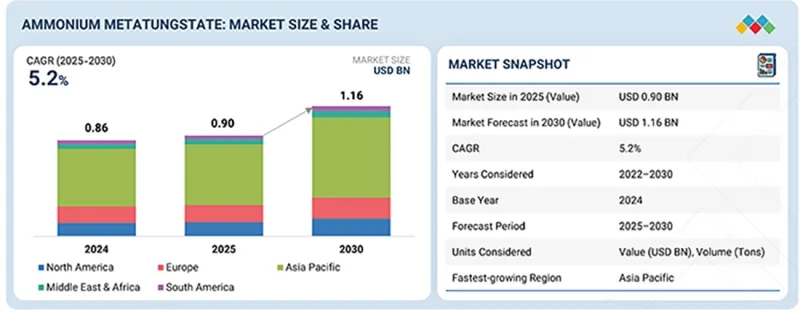

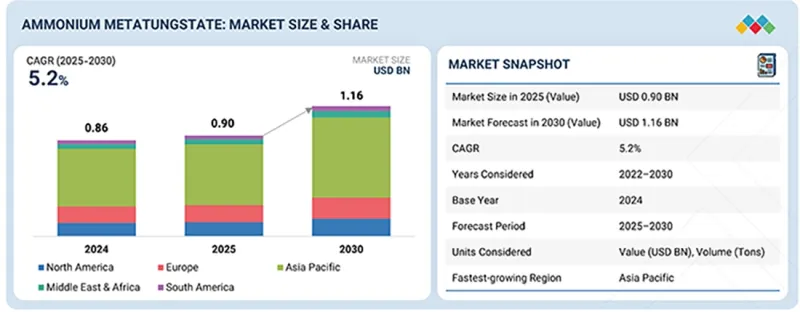

메타텅스텐산 암모늄 시장 규모는 예측 기간 동안 CAGR 5.2%로 성장하여 2025년 9억 달러에서 2030년까지 11억 6,000만 달러에 달할 것으로 전망됩니다.

조사 범위

조사 대상 기간

2022-2030년

기준 연도

2024년

예측 기간

2025-2030년

대상 단위

금액(달러) , 톤

부문

원료, 형태, 등급, 용도, 최종 이용 산업, 지역

대상 지역

유럽, 북미, 아시아태평양, 중동 및 아프리카, 남미

시약용 메타텅스텐산 암모늄(AMT)은 연구, 분석 및 고정밀 산업 공정에서의 사용 확대에 힘입어 예측 기간 동안 가치 기준으로 두 번째로 높은 성장률을 보일 것으로 예상됩니다. 시약 등급의 AMT는 순도와 화학적 안정성이 뛰어나 오염 관리가 중요한 실험실 규모의 합성, 촉매 개발, 첨단 재료 연구에 적합합니다. 재현성과 성능의 신뢰성이 필수적인 학술 및 산업 연구 개발 분야, 전자기기 및 특수 촉매와 같은 틈새 응용 분야에서 그 수요가 특히 증가하고 있습니다. 특정 첨단 기술 분야에서는 고순도 또는 전자 등급 AMT가 주류이지만, 시약 등급 재료는 비용, 가용성 및 품질 사양의 균형 잡힌 균형으로 인해 지속적으로 지지를 확대하고 있으며, 진화하는 AMT 시장 상황에서 기술 등급과 초순수 등급의 중간 선택으로 중요한 위치를 차지하고 있습니다. 중요한 위치를 차지하고 있습니다.

"용도별로는 촉매 분야가 예측 기간 동안 가장 빠른 성장세를 보일 것으로 예상됩니다."

이러한 성장은 청정 연료와 에너지 효율적인 화학 공정으로의 전환이 가속화됨에 따라 뒷받침되고 있습니다. AMT는 수소화 처리, 산화 결합, 선택적 촉매 환원(SCR) 시스템에 사용되는 텅스텐 기반 촉매의 제조에 중요한 전구체 역할을 합니다. 산도, 산화 잠재력, 열 안정성의 독특한 조합으로 촉매 성능을 향상시켜 정제, 석유화학, 환경 응용 분야에서 매우 효과적입니다. 기존의 수소화 분해 및 탈황 용도 외에도 바이오매스 전환, CO2 이용, 수소 생산을 위한 암모니아 분해 등 그린 케미스트리 분야로의 적용이 확대되고 있습니다. 이러한 새로운 지속가능한 기술은 AMT 유래 촉매에 대한 새로운 고부가가치 수요를 창출하고 있습니다. 또한, 정유공장과 화학공장이 더욱 엄격한 배출 기준과 공정 효율 목표를 달성하기 위해 현대화를 추진함에 따라, 텅스텐 촉매 시스템으로의 전환은 이 응용 분야의 성장을 더욱 가속화할 것으로 예상됩니다.

"최종사용자 산업별로는 화학 분야가 예측 기간 동안 가장 빠른 성장을 기록할 것으로 예상됩니다."

첨단 화학 합성 및 촉매 공정에서 텅스텐 기반 중간체의 채택이 증가하고 있습니다. AMT는 고성능 촉매, 특수 텅스텐 화합물, 다양한 다운스트림 제품의 구성요소인 기능성 산화물 제조의 주요 원료로 점점 더 많이 사용되고 있습니다. AMT는 촉매 반응에서 높은 활성과 선택성을 달성하고 폐기물을 줄이고 공정 경제성을 향상시키기 때문에 보다 깨끗하고 에너지 효율적인 화학 생산으로의 전환은 AMT의 수요를 더욱 자극하고 있습니다. 또한, 첨단 코팅제, 고분자 개질제, 환경촉매를 포함한 정밀화학 및 특수 화학제품의 생산 확대는 AMT 활용의 새로운 성장 기회를 창출하고 있습니다. 많은 화학업체들은 지속가능성과 순환경제의 흐름에 따라 AMT를 재생 가능하고 환경 친화적인 중간체로 활용하는 폐쇄형 텅스텐 회수 시스템에도 투자하고 있습니다. 이러한 성능, 다용도성 및 환경 적합성의 조합은 화학 산업을 시장의 주요 촉진요인으로 자리매김하고 있습니다.

"유럽 시장은 예측 기간 동안 두 번째 시장 점유율을 기록할 것으로 예상됩니다."

이러한 성장은 이 지역의 탄탄한 산업 기반, 높은 기술력, 지속가능한 제조에 대한 관심의 증가로 뒷받침되고 있습니다. 특히 독일, 오스트리아, 영국에는 고순도 텅스텐 가공을 위한 인프라를 갖춘 주요 텅스텐 화학 제조업체 및 정련업체가 다수 존재합니다. 유럽의 성숙한 석유화학, 자동차, 항공우주 산업은 엄격한 환경 및 성능 기준에 힘입어 AMT 기반 촉매 및 재료의 주요 소비처가 되었습니다. 저배출 연료로의 전환과 순환 경제 모델로의 전환이 진행됨에 따라 정제업체와 화학업체들은 촉매 시스템과 텅스텐 회수 루프에 AMT를 통합하는 것을 추진하고 있습니다. 또한, 유럽 그린딜(European Green Deal)과 청정에너지 기술에 대한 투자로 뒷받침되는 강력한 R&D 이니셔티브는 텅스텐 촉매 및 전자 재료의 혁신을 촉진하고 있습니다. 이러한 규제 추진, 기술 발전, 산업 성숙도의 조합으로 유럽은 전략적으로 중요하고 안정적인 시장으로 자리매김하고 있으며, 세계 AMT 시장에서 두 번째 지역적 허브로서의 지위를 유지하고 있습니다.

세계의 메타텅스텐산 암모늄 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술·특허 동향, 법·규제 환경, 사례 분석, 시장 규모 추정 및 예측, 각종 부문별·지역별·주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 주요 인사이트

제5장 시장 개요

제6장 메타텅스텐산 암모늄 시장 : 유형별

제7장 메타텅스텐산 암모늄 시장 : 원료별

제8장 메타텅스텐산 암모늄 시장 : 형태별

제9장 메타텅스텐산 암모늄 시장 : 등급별

제10장 메타텅스텐산 암모늄 시장 : 용도별

제11장 메타텅스텐산 암모늄 시장 : 최종 이용 산업별

제12장 메타텅스텐산 암모늄 시장 : 지역별

제13장 경쟁 구도

제14장 기업 개요

제15장 부록

KSM

영문 목차

영문목차

The ammonium metatungstate market is projected to grow from USD 0.90 billion in 2025 to USD 1.16 billion by 2030, at a CAGR of 5.2% during the forecast period.

Scope of the Report

Years Considered for the Study

2022-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million), Volume (Tons)

Segments

Raw Material, Form, Grade, Application, End-use Industry, and Region

Regions covered

Europe, North America, Asia Pacific, the Middle East & Africa, and South America

The reagent grade of ammonium metatungstate (AMT) is expected to be the second-fastest-growing grade in terms of value during the forecast period, driven by its expanding use in research, analytical applications, and high-precision industrial processes. Reagent-grade AMT offers superior purity and chemical consistency, making it suitable for laboratory-scale synthesis, catalyst development, and advanced material research where contamination control is critical. Its demand is rising, particularly in academic and industrial R&D sectors, as well as in niche applications such as electronics and specialty catalysts, where reproducibility and performance reliability are essential. Although high-purity or electronic-grade AMT dominates in certain high-tech segments, reagent-grade material continues to gain traction due to its balanced cost, availability, and quality specifications, positioning it as a key intermediate choice between technical and ultra-high-purity grades in the evolving AMT market landscape.

''In terms of value, catalyst is expected to be the fastest-growing in the overall AMT market during the forecast period.''

This growth is supported by the accelerating global transition toward cleaner fuels and energy-efficient chemical processes. AMT serves as a critical precursor for manufacturing tungsten-based catalysts used in hydroprocessing, oxidative coupling, and selective catalytic reduction (SCR) systems. Its unique combination of acidity, oxidation potential, and thermal stability enhances catalytic performance, making it highly effective in refining, petrochemical, and environmental applications. Beyond traditional hydrocracking and desulfurization uses, the material is increasingly being explored for green chemistry innovations such as biomass conversion, CO2 utilization, and ammonia decomposition for hydrogen production. These emerging sustainable technologies are creating new, high-value demand streams for AMT-derived catalysts. Additionally, as refineries and chemical plants modernize to meet stricter emission norms and process efficiency goals, the shift toward tungsten-based catalyst systems is expected to further accelerate the growth of this application segment.

.

"During the forecast period, the chemical end-use industry is projected to register the fastest growth during the forecast period."

Driven by the rising adoption of tungsten-based intermediates in advanced chemical synthesis and catalytic processes. AMT is increasingly being used as a key ingredient in the manufacture of high-performance catalysts, specialty tungsten compounds, and functional oxides that serve as building blocks for a variety of downstream products. The shift toward cleaner and more energy-efficient chemical production is further stimulating demand, as AMT enables high activity and selectivity in catalytic reactions, reducing waste and improving process economics. Additionally, growth in fine and specialty chemical manufacturing, including advanced coatings, polymer modifiers, and environmental catalysts, is creating new opportunities for AMT utilization. Many chemical producers are also investing in closed-loop tungsten recovery systems, using AMT as a recyclable and environmentally compatible intermediate, aligning with sustainability and circular economy trends. This combination of performance, versatility, and environmental compliance positions the chemical industry as a key growth driver for the global AMT market.

"The AMT market in Europe is projected to register the second-largest market share during the forecast period."

This growth is supported by the region's strong industrial base, advanced technological capabilities, and growing emphasis on sustainable manufacturing. The region hosts several leading tungsten chemical producers and refiners, particularly in Germany, Austria, and the UK, which have well-established infrastructure for high-purity tungsten processing. Europe's mature petrochemical, automotive, and aerospace industries are key consumers of AMT-based catalysts and materials, driven by strict environmental and performance standards. The ongoing transition toward low-emission fuels and the adoption of circular economy models are encouraging refiners and chemical manufacturers to integrate AMT in catalyst systems and tungsten recovery loops. Additionally, robust R&D initiatives, supported by the European Green Deal and investments in clean energy technologies, are fostering innovation in tungsten-based catalysts and electronic materials. This combination of regulatory push, technological advancement, and industrial maturity positions Europe as a strategically important and stable market, maintaining its status as the second-largest regional hub in the global AMT landscape.

This study has been validated through primary interviews with industry experts globally. These primary sources have been divided into the following three categories:

By Company Type: Tier 1 - 60%, Tier 2 - 20%, and Tier 3 - 20%

By Designation: C Level - 33%, Director Level - 33%, and Managers - 34%

By Region: North America - 20%, Europe - 25%, Asia Pacific - 25%, Middle East & Africa - 15%, and South America - 15%

The report provides a comprehensive analysis of company profiles:

Prominent companies in this market include H.C. Starck Tungsten GmbH (Germany), Global Tungsten & Powders (US), Masan High-Tech Materials Corporation (Vietnam), Ganzhou Grand Sea Tungsten Co., Ltd. (China), Ereztech LLC (US), Ganzhou CF Tungsten Co., Ltd (China), United Wolfram (India), ATT Advanced Elemental Materials Co., Ltd. (US), Noah Chemicals (US), and North Metal & Chemical Co. (US).

Research Coverage

This research report categorizes the AMT market by raw material (virgin ore route, secondary/recycled route), form (powder, aqueous solution, crystalline), grade (standard grade, high-purity grade, reagent grade), application (catalysts, pigments, metal finishing, x-ray shielding, analytical chemistry, glass & ceramic production, other applications), end-use industry (chemical, electronics, medical, aerospace & defense, metallurgy, other end-use industries), and region (North America, Europe, Asia Pacific, Middle East & Africa, and South America). The scope of the report includes detailed information about the major factors influencing the growth of the AMT market, such as drivers, restraints, challenges, and opportunities. A thorough examination of the key industry players has been conducted in order to provide insights into their business overview, solutions, and services, key strategies, contracts, partnerships, and agreements. Product launches, mergers and acquisitions, and recent developments in the AMT market are all covered. This report includes a competitive analysis of upcoming startups in the AMT market ecosystem.

Reasons to buy this report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall AMT market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

Analysis of key drivers (regulatory compliance in end-use industries, technological advancement, and performance superiority), restraints (volatility in raw material prices and technical complexity in downstream applications), opportunities (high growth technology sector and circular economy and recycling), and challenges (supply chain vulnerabilities)

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and service launches in the AMT market.

Market Development: Comprehensive information about lucrative markets - the report analyses the AMT market across varied regions.

Market Diversification: Exhaustive information about services, untapped geographies, recent developments, and investments in the AMT market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like H.C. Starck Tungsten GmbH (Germany), Global Tungsten & Powders (US), Masan High-Tech Materials Corporation (Vietnam), Ganzhou Grand Sea Tungsten Co., Ltd. (China), Ereztech LLC (US), Ganzhou CF Tungsten Co., Ltd. (China), United Wolfram (India), ATT Advanced Elemental Materials Co., Ltd. (US), Noah Chemicals (US), and North Metal & Chemical Co. (US).

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 AMMONIUM METATUNGSTATE MARKET SEGMENTATION AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 UNITS CONSIDERED

1.6 STAKEHOLDERS

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 List of key secondary sources

2.1.1.2 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 List of primary interview participants-demand and supply side

2.1.2.3 Key industry insights

2.1.2.4 Breakdown of interviews with experts

2.2 MARKET SIZE ESTIMATION

2.2.1 BOTTOM-UP APPROACH

2.2.2 TOP-DOWN APPROACH

2.3 FORECAST NUMBER CALCULATION

2.4 DATA TRIANGULATION

2.5 FACTOR ANALYSIS

2.6 ASSUMPTIONS

2.7 LIMITATIONS & RISKS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 OPPORTUNITIES FOR PLAYERS IN AMMONIUM METATUNGSTATE MARKET

4.2 AMMONIUM METATUNGSTATE MARKET, BY RAW MATERIAL

4.3 AMMONIUM METATUNGSTATE MARKET, BY FORM

4.4 AMMONIUM METATUNGSTATE MARKET, BY GRADE

4.5 AMMONIUM METATUNGSTATE MARKET, BY APPLICATION

4.6 AMMONIUM METATUNGSTATE MARKET, BY END-USE INDUSTRY

4.7 AMMONIUM METATUNGSTATE MARKET, BY KEY COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Regulatory compliance in end-use industries

5.2.1.2 Technological advancement and performance superiority

5.2.2 RESTRAINTS

5.2.2.1 Volatility in raw material prices

5.2.2.2 Technical complexity in downstream applications

5.2.3 OPPORTUNITIES

5.2.3.1 High-growth technology sectors

5.2.3.2 Circular economy and recycling

5.2.4 CHALLENGES

5.2.4.1 Supply chain vulnerabilities

5.2.4.2 High barriers to new production

5.3 PORTER'S FIVE FORCES ANALYSIS

5.3.1 BARGAINING POWER OF SUPPLIERS

5.3.2 BARGAINING POWER OF BUYERS

5.3.3 THREAT OF NEW ENTRANTS

5.3.4 THREAT OF SUBSTITUTES

5.3.5 INTENSITY OF COMPETITIVE RIVALRY

5.4 MACROECONOMIC INDICATORS

5.4.1 GLOBAL GDP TRENDS

5.5 VALUE CHAIN ANALYSIS

5.5.1 RAW MATERIAL SUPPLIERS

5.5.2 MANUFACTURERS

5.5.3 DISTRIBUTORS

5.5.4 DOWNSTREAM (PRODUCT MANUFACTURING)

5.5.5 END USERS

5.6 ECOSYSTEM ANALYSIS

5.7 TECHNOLOGY ANALYSIS

5.7.1 KEY TECHNOLOGIES

5.7.1.1 Next-generation battery anodes

5.7.1.2 Biomedical and environmental applications

5.7.1.3 Green hydrogen and carbon utilization

5.7.2 ADJACENT TECHNOLOGIES

5.7.2.1 Innovations in tungsten precursor synthesis and recycling

5.7.2.2 Advanced catalyst manufacturing and design

5.7.3 COMPLEMENTARY TECHNOLOGIES

5.7.3.1 Miniaturization in electronics

5.7.3.2 Advanced medical imaging

5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.9 TRADE ANALYSIS

5.9.1 EXPORT SCENARIO

5.9.2 IMPORT SCENARIO

5.10 CASE STUDY ANALYSIS

5.10.1 SUSTAINABLE PRODUCTION OF AMMONIUM METATUNGSTATE VIA REVERSE OSMOSIS

5.10.2 AMMONIUM METATUNGSTATE IN REFORMING CATALYSTS FOR HYDROGEN PRODUCTION

5.10.3 AMT IN CATALYST PREPARATION FOR NOx SCR - RESEARCH APPLICATION

5.11 REGULATORY LANDSCAPE

5.11.1 REGULATIONS

5.11.1.1 Europe

5.11.1.2 Asia Pacific

5.11.1.3 North America

5.11.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.12 KEY STAKEHOLDERS & BUYING CRITERIA

5.12.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.12.2 BUYING CRITERIA

5.13 KEY CONFERENCES AND EVENTS, 2025-2026

5.14 PRICING ANALYSIS

5.14.1 AVERAGE SELLING PRICE TREND, BY REGION

5.14.2 AVERAGE SELLING PRICE TREND, BY APPLICATION

5.15 INVESTMENT AND FUNDING SCENARIO

5.16 PATENT ANALYSIS

5.16.1 APPROACH

5.16.2 DOCUMENT TYPES

5.16.3 PUBLICATION TRENDS, 2014-2024

5.16.4 INSIGHTS

5.16.5 LEGAL STATUS OF PATENTS

5.16.6 JURISDICTION ANALYSIS FROM 2014 TO 2024

5.16.7 TOP COMPANIES/APPLICANTS

5.16.8 TOP 10 PATENT OWNERS (US), 2014-2024

5.17 IMPACT OF 2025 US TARIFF ON AMMONIUM METATUNGSTATE MARKET

5.17.1 INTRODUCTION

5.17.2 KEY TARIFF RATES

5.17.3 PRICE IMPACT ANALYSIS

5.17.4 IMPACT ON KEY COUNTRIES/REGIONS

5.17.4.1 North America

5.17.4.2 Europe

5.17.4.3 Asia Pacific

5.17.5 IMPACT ON END-USE INDUSTRIES

6 AMMONIUM METATUNGSTATE MARKET, BY TYPE

6.1 INTRODUCTION

6.2 PURITY 99%

6.2.1 INDUSTRIAL-GRADE AMT FOR CATALYSTS AND TUNGSTEN POWDERS

6.3 PURITY 98%

6.3.1 AMT FOR CONVENTIONAL INDUSTRIAL APPLICATIONS

6.4 OTHERS

7 AMMONIUM METATUNGSTATE MARKET, BY RAW MATERIAL

7.1 INTRODUCTION

7.2 VIRGIN ORE ROUTE (WO3 FROM PRIMARY ORES)

7.2.1 INDUSTRIAL-GRADE AMT DERIVED FROM PRIMARY TUNGSTEN ORES

7.3 SECONDARY/RECYCLED ROUTE

7.3.1 AMT PRODUCTION VIA TUNGSTEN SCRAP AND CARBIDE RECYCLING

8 AMMONIUM METATUNGSTATE MARKET, BY FORM

8.1 INTRODUCTION

8.2 POWDER

8.2.1 AMT POWDERS TO DRIVE EFFICIENCY IN TUNGSTEN PROCESSING

8.3 AQUEOUS SOLUTION

8.3.1 AQUEOUS SOLUTIONS TO DRIVE GROWTH IN CATALYST INDUSTRY

8.4 CRYSTALLINE

8.4.1 HIGH-PURITY CRYSTALLINE AMT WIDELY USED IN ADVANCED TUNGSTEN APPLICATIONS

9 AMMONIUM METATUNGSTATE MARKET, BY GRADE

9.1 INTRODUCTION

9.2 STANDARD GRADE

9.2.1 COST-OPTIMIZED SOLUTION FOR BULK MANUFACTURING

9.3 HIGH PURITY GRADE

9.3.1 ENABLING ADVANCED APPLICATIONS IN ELECTRONICS AND CATALYSIS

9.4 REAGENT GRADE

9.4.1 SIGNIFICANCE OF REAGENT GRADE AMT IN EARLY-STAGE MATERIAL DEVELOPMENT

10 AMMONIUM METATUNGSTATE MARKET, BY APPLICATION

10.1 INTRODUCTION

10.2 CATALYST

10.2.1 IMPORTANCE IN PETROCHEMICAL AND ENVIRONMENTAL SECTORS

10.3 PIGMENTS

10.3.1 SUPERIOR COLOR RETENTION UNDER EXTREME CONDITIONS

10.4 METAL FINISHING

10.4.1 PROCESS-OPTIMIZED AMT FOR INDUSTRIAL APPLICATIONS

10.5 X-RAY SHIELDING

10.5.1 GROWING DEMAND FOR RADIATION PROTECTION IN HEALTHCARE FACILITIES

10.6 ANALYTICAL CHEMISTRY

10.6.1 ENABLES SENSITIVE DETECTION OF TRACE METALS AND ANIONS

10.7 GLASS & CERAMIC PRODUCTION

10.7.1 IMPROVES THERMAL STABILITY AND HEAT RESISTANCE IN GLASS AND CERAMICS

10.8 OTHER APPLICATIONS

11 AMMONIUM METATUNGSTATE MARKET, BY END-USE INDUSTRY

11.1 INTRODUCTION

11.2 CHEMICAL & PETROCHEMICAL

11.2.1 DEMAND FOR CLEANER FUELS TO DRIVE MARKET

11.3 ELECTRONICS

11.3.1 HIGH-PURITY AMMONIUM METATUNGSTATE ESSENTIAL FOR ELECTRONICS INDUSTRY

11.4 MEDICAL

11.4.1 REGULATORY PRESSURE ON LEAD SHIELDING TO PROVIDE OPPORTUNITY FOR AMMONIUM METATUNGSTATE

11.5 AEROSPACE & DEFENSE

11.5.1 DEMAND FOR AMMONIUM METATUNGSTATE OF HIGH SPECIALIZATION AND QUALITY TO DRIVE MARKET

11.6 METALLURGY

11.6.1 WIDELY USED FOR MAKING SUBSTRATE FOR SEMICONDUCTOR DEVICES

11.7 OTHER END-USE INDUSTRIES

12 AMMONIUM METATUNGSTATE MARKET, BY REGION

12.1 INTRODUCTION

12.2 NORTH AMERICA

12.2.1 US

12.2.1.1 Government support to semiconductor fabrication industry to drive demand

12.2.2 CANADA

12.2.2.1 Oil sands processing and chemical exports are strong drivers for use of ammonium metatungstate

12.2.3 MEXICO

12.2.3.1 Country's transition to trade hub to drive market

12.3 ASIA PACIFIC

12.3.1 CHINA

12.3.1.1 Largest market for ammonium metatungstate

12.3.2 INDIA

12.3.2.1 Growing semiconductor industry through government initiative to drive market

12.3.3 JAPAN

12.3.3.1 Initiatives to restabilize semiconductor industry to drive demand for high-quality ammonium metatungstate

12.3.4 SOUTH KOREA

12.3.4.1 Expansion of electronics industry to directly drive ammonium metatungstate demand

12.3.5 REST OF ASIA PACIFIC

12.4 EUROPE

12.4.1 GERMANY

12.4.1.1 Growth of chemical industry to drive market

12.4.2 FRANCE

12.4.2.1 High quality ammonium metatungstate to drive market

12.4.3 UK

12.4.3.1 Reliance on local sourcing for growing electronics industry to drive market

12.4.4 ITALY

12.4.4.1 Coatings for high purity materials to drive demand for ammonium metatungstate

12.4.5 SPAIN

12.4.5.1 Growing electronic base to support market

12.4.6 REST OF EUROPE

12.5 MIDDLE EAST & AFRICA

12.5.1 GCC COUNTRIES

12.5.1.1 Saudi Arabia

12.5.1.1.1 Vision 2030 to play major role in driving market

12.5.1.2 UAE

12.5.1.2.1 Government's initiative to diversify economy to drive market

12.5.1.3 Rest of GCC

12.5.2 SOUTH AFRICA

12.5.2.1 Ammonium metatungstate demand is directly linked with growing chemical industry

12.5.3 REST OF MIDDLE EAST & AFRICA

12.6 SOUTH AMERICA

12.6.1 BRAZIL

12.6.1.1 Government initiatives to drive market

12.6.2 ARGENTINA

12.6.2.1 Focus on chemical sector to drive market

12.6.3 REST OF SOUTH AMERICA

13 COMPETITIVE LANDSCAPE

13.1 OVERVIEW

13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

13.3 REVENUE ANALYSIS

13.4 MARKET SHARE ANALYSIS

13.4.1 GANZHOU GRAND SEA TUNGSTEN CO., LTD.

13.4.2 XIAMEN TUNGSTEN CO., LTD.

13.4.3 H.C. STARCK TUNGSTEN GMBH

13.4.4 GLOBAL TUNGSTEN & POWDERS

13.4.5 GANZHOU CF TUNGSTEN CO., LTD

13.5 COMPANY VALUATION AND FINANCIAL METRICS

13.6 PRODUCT COMPARISON ANALYSIS

13.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

13.7.1 STARS

13.7.2 EMERGING LEADERS

13.7.3 PERVASIVE PLAYERS

13.7.4 PARTICIPANTS

13.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

13.7.5.1 Company footprint

13.7.5.2 Region footprint

13.7.5.3 Type footprint

13.7.5.4 Raw material footprint

13.7.5.5 Form footprint

13.7.5.6 Grade footprint

13.7.5.7 Application footprint

13.7.5.8 End-use industry footprint

13.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024