Mold Release Agents Market by Type (Water-based, Solvent-based), Application (Die-casting, Rubber Molding, Plastic Molding, Concrete, PU Molding, Wood Composite & Panel Pressing, Composite Molding, Others), & Region - Global Forecast to 2030

상품코드:1931747

리서치사:MarketsandMarkets

발행일:2026년 01월

페이지 정보:영문 243 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

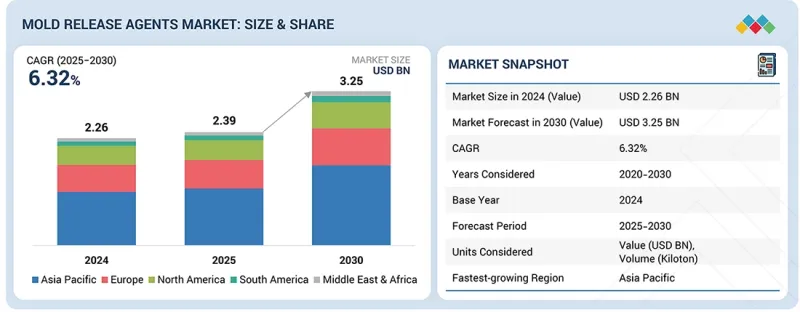

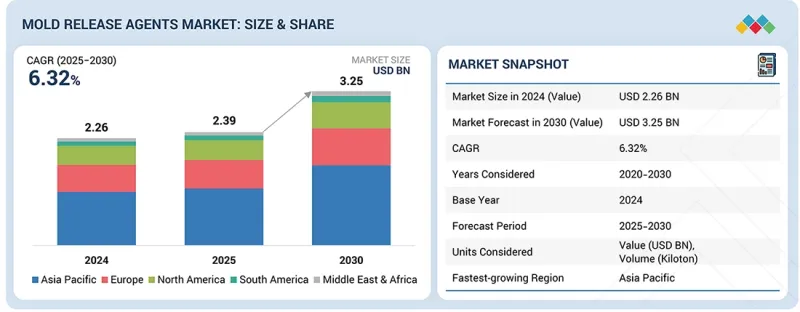

이형제 시장 규모는 2025년 23억 9,000만 달러에서 2030년까지 32억 5,000만 달러로 성장하여 2025년부터 2030년까지 연평균 성장률(CAGR) 6.32%로 예측됩니다.

조사 범위

조사 대상 기간

2020-2030년

기준 연도

2024년

예측 기간

2025-2030년

대상 단위

금액(100만 달러) 및 킬로톤

부문

유형별, 용도별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미

"규제 준수와 제조 효율화에 대한 요구가 이형제 시장 성장을 견인"

환경 안전 및 배출가스 관련 규제가 강화됨에 따라 이형제 시장은 지속적으로 성장하고 있습니다. 각 제조업체들은 이러한 요구사항을 충족시키기 위해 수계 및 저배출형 배합을 단계적으로 채택하고 있습니다. 이러한 전환은 최종사용자 산업에서 생산 효율성 향상, 표면 품질 개선, 금형 내구성 강화에 대한 관심이 높아지는 것과도 일치합니다. 그 결과, 고성능 이형제는 이러한 산업 운영에 필수적인 요소로 자리 잡았습니다.

2024년, PU 성형 부문은 전체 이형제 시장에서 세 번째 점유율을 차지했습니다. 이러한 추세는 예측 기간 동안 지속될 것으로 예상됩니다. 시장의 성장은 자동차 부품, 단열재, 가구, 건축자재 등 다양한 분야에서 폴리우레탄이 광범위하게 사용되고 있기 때문입니다. 또한, 유연성 폼 및 경질 폼의 수요 증가와 생산량 확대는 효과적인 이형제의 필요성을 뒷받침하고 있습니다. 또한, 표면 마감 개선, 사이클 시간 단축, 생산 효율성 향상에 대한 요구는 PU 성형 응용 분야에서 이형제의 수요를 더욱 증가시키고 있습니다.

수성 이형제 부문은 예측 기간 동안 가치 기준으로 가장 빠르게 성장할 것으로 예상됩니다. 이러한 성장은 휘발성유기화합물(VOC) 배출을 줄이기 위한 정부 규제 강화에 의해 촉진되고 있습니다. 환경 보호에 대한 인식이 높아짐에 따라 제조업체들은 환경 친화적일 뿐만 아니라 가공이 용이하고 다재다능한 수성 이형제를 점점 더 많이 채택하고 있습니다. 또한, 배합 기술의 발전으로 이형 성능과 내구성이 더욱 향상되어 솔벤트 기반 제품을 대체할 수 있는 상업적으로 실현 가능한 대안이 되었습니다.

북미는 2024년 기준 세계 3위의 이형제 시장 규모를 자랑했습니다. 자동차, 건설, 고무/플라스틱, 복합재료 산업과 같은 기존 최종사용자 시장이 이 지역의 성장을 주도하고 있습니다. 또한, 이 지역에는 고급 성형 기술 채택률이 높고, 품질과 공정 개선에 중점을 둔 기존 제조 부문이 존재하며, 이는 성장에 기여하고 있습니다. 또한, 환경 및 안전 요인에 대한 엄격한 정부 규제로 인해 첨단 이형제가 더욱 성장하고 있습니다.

본 보고서에서 다룬 주요 기업 프로필에는 Freudenberg Group(독일), Daikin Industries, Ltd.(일본), Henkel AG & Co. KGaA(독일), LANXESS AG(독일), Shin-Etsu Chemical(일본), Dow Inc(미국), Michelman, Inc.(미국), Marbocote Ltd.(영국), McGee Industries, Inc.(미국), Miller-Stephenson, Inc.(미국) 등이 포함됩니다.

조사 범위

이 보고서는 이형제 시장을 유형, 용도, 지역별로 세분화하고 있습니다. 각 지역의 시장 규모 추정치(100만 달러)를 제공하고, 주요 산업 플레이어에 대한 상세한 분석과 함께 각 회사의 사업 개요, 서비스, 이형제 시장과 관련된 주요 전략에 대한 인사이트를 제공합니다.

본 보고서 구매 이유

본 조사 보고서는 산업 분석(업계 동향), 주요 기업의 기업 점유율 분석, 기업 개요 등 다양한 수준의 분석에 초점을 맞추고 있습니다. 이를 종합하여 경쟁 상황, 이형제 시장의 신흥 및 고성장 부문, 고성장 지역, 시장 촉진요인, 억제요인, 성장 기회에 대한 종합적인 견해를 제공합니다.

이 보고서는 다음 사항에 대한 인사이트를 제공합니다:

시장 침투 현황 : 세계 시장에서 주요 기업이 제공하는 이형제에 대한 종합적인 정보

주요 촉진요인 분석:(자동차 및 건설 산업의 급성장, 자동차 및 가구용 수요 증가), 억제요인(용제형 이형제에 대한 엄격한 규제, 금형에 대한 논스틱 코팅 사용 증가), 기회(신흥 경제국의 인프라 개발), 도전 과제(원자재 가격 변동) 등 이형제 시장 성장에 영향을 미치는 요소

제품 개발 및 혁신 : 이형제 시장의 신기술 동향, 연구개발 활동, 제품 및 서비스 출시에 대한 상세 분석

시장 개발 : 지역별로 수익성 높은 신흥 시장에 대한 종합적인 정보 제공

시장 다각화 : 제품, 미개척 지역 및 세계 이형제 시장의 최근 동향에 대한 종합적인 정보를 제공합니다.

경쟁 평가 : 이형제 시장 내 주요 기업의 시장 점유율, 전략, 제품, 생산능력에 대한 상세 분석

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

시장 역학

성장 촉진요인

성장 억제요인

기회

과제

상호 접속된 시장과 분야 횡단적인 기회

티어1/2/3플레이어 전략적 활동

제5장 업계 동향

Porter's Five Forces 분석

거시경제 지표

공급망 분석

생태계 분석

가격 분석

무역 분석

2026년의 주요 회의와 이벤트

고객 비즈니스에 영향을 미치는 동향/혼란

투자와 자금 조달 시나리오

사례 연구 분석

2025년 미국 관세의 영향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신

주요 기술

보완적 기술

기술/제품 로드맵

특허 분석

AI/생성형 AI의 영향

제7장 규제 상황과 지속가능성에 관한 대처

지역 규제와 컴플라이언스

규제기관, 정부기관, 기타 조직

업계 표준

지속가능성에 대한 영향과 규제 정책의 대처

안전 프로토콜

지속가능한 개발

표준화

인증, 라벨, 환경기준

제8장 고객 상황과 구매 행동

의사결정 프로세스

구매 프로세스의 주요 이해관계자와 그 평가 기준

채용 장벽과 내부 과제

응용에서 미충족 수요

제9장 이형제 시장(유형별)

수성

용제형

기타

제10장 이형제 시장(용도별)

다이캐스팅

PU성형

고무 성형

복합 성형

플라스틱 성형

목질 복합재 및 패널 프레스

콘크리트

기타

제11장 이형제 시장(지역별)

아시아태평양

중국

일본

인도

한국

북미

미국

캐나다

멕시코

유럽

독일

프랑스

영국

러시아

이탈리아

스페인

튀르키예

중동 및 아프리카

GCC

남아프리카공화국

남미

브라질

아르헨티나

제12장 경쟁 구도

주요 진출 기업의 전략/강점, 2022-2025년

시장 점유율 분석, 2024년

매출 분석, 2020-2024년

기업 평가 매트릭스 : 주요 진출 기업, 2024년

기업 평가 매트릭스 : 스타트업/중소기업, 2024년

브랜드/제품 비교

기업 평가와 재무 지표

경쟁 시나리오

제13장 기업 개요

주요 진출 기업

FREUDENBERG GROUP

DAIKIN INDUSTRIES, LTD.

HENKEL AG & CO. KGAA

LANXESS AG

SHIN-ETSU CHEMICAL CO., LTD.

DOW INC.

MICHELMAN, INC.

MARBOCOTE LTD.

MCGEE INDUSTRIES, INC.

MILLER-STEPHENSON, INC.

기타 기업

TAG CHEMICALS GMBH

PARKER-HANNIFIN CORPORATION

AGC INC.

AMPACET CORPORATION

POLYTEK DEVELOPMENT CORP.

CHUKYO YUSHI HOLDINGS CO., LTD.

CRESSET CHEMICAL

ILLINOIS TOOL WORKS INC.

CSW INDUSTRIALS, INC.

KAO CORPORATION

MORESCO CORPORATION

PERI SE

SIKA AG

SUMICO LUBRICANT CO., LTD.

MOMENTIVE PERFORMANCE MATERIALS, INC.

제14장 조사 방법

제15장 부록

KSM

영문 목차

영문목차

The mold release agents market is projected to grow from USD 2.39 billion in 2025 to USD 3.25 billion by 2030, at a CAGR of 6.32% between 2025 and 2030.

Scope of the Report

Years Considered for the Study

2020-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million) and Volume (Kiloton)

Segments

Type, Application, and Region

Regions covered

North America, Europe, Asia Pacific, the Middle East & Africa, and South America

"Regulatory compliance and manufacturing efficiency requirements to drive the mold release agents market's growth"

The mold release agents market is growing due to the increasing regulations related to environmental safety and emissions. Manufacturers are progressively adopting water-based and low-emission formulations to comply with these requirements. The shift also aligns with end-use industries' heightened focus on achieving high production efficiency, improved surface quality, and enhanced mold durability. As a result, high-performance mold release agents have become essential for their operations.

"By application, the PU molding segment is projected to account for the third-largest market share during the forecast period."

In 2024, the PU molding segment accounted for the third-largest share of the overall mold release agents market. And this trend is expected to continue during the forecast period. The growth of the market is due to the widespread use of polyurethane in various sectors, including automotive parts, insulation materials, furniture, and construction products. Additionally, the increasing demand for flexible and rigid foams, along with rising production volumes, has sustained the need for effective mold release agents. Moreover, the desire to improve surface finish, reduce cycle times, and enhance production efficiency is further boosting the demand for mold release agents in PU molding applications.

"By type, the water-based mold release agents segment is projected to be the fastest-growing segment during the forecast period."

The water-based mold release agents segment is projected to be the fastest-growing type in terms of value during the forecast period. This growth is driven by stricter government regulations aimed at reducing VOC emissions. As awareness of environmental protection increases, manufacturers are increasingly adopting water-based mold release agents, which are not only environmentally friendly but also easy to process and versatile. Additionally, advancements in formulation technology have further improved their release performance and durability, making them a commercially viable alternative to solvent-based products.

"North America accounted for the third-largest share in the global mold release agents market, in terms of value, in 2024."

North America was the third-largest mold release agents market in 2024. The established end user markets, such as the automotive, construction, rubber & plastic, and composite industries, drive growth in the region. Additionally, the region has a well-established manufacturing sector, with a high adoption of advanced molding technology and a strong emphasis on quality and process improvements, which is also contributing to its growth. Moreover, strict government regulations with respect to the environment and safety factors are favoring advanced mold release agents, which is further propelling growth.

By Company Type: Tier 1 - 55%, Tier 2 - 25%, and Tier 3 - 20%

By Designation: Directors - 50%, Managers - 30%, and Others - 20%

By Region: North America - 40%, Europe - 35%, Asia Pacific - 20%, RoW - 5%

The key players profiled in the report include Freudenberg Group (Germany), Daikin Industries, Ltd. (Japan), Henkel AG & Co. KGaA (Germany), LANXESS AG (Germany), Shin-Etsu Chemical Co., Ltd. (Japan), Dow Inc. (US), Michelman, Inc. (US), Marbocote Ltd. (UK), McGee Industries, Inc. (US), and Miller-Stephenson, Inc. (US).

Study Coverage

This report segments the mold release agents market based on type, application, and region. It provides estimations of value (USD million) for the overall market size across various regions. A detailed analysis of key industry players has also been conducted to provide insights into their business overviews, services, and key strategies associated with the mold release agents market.

Reasons to Buy this Report

This research report is focused on various levels of analysis-industry analysis (industry trends), market share analysis of top players, and company profiles. They together provide an overall view of the competitive landscape; emerging and high-growth segments of the mold release agents market; high-growth regions; and market drivers, restraints, and opportunities.

The report provides insights into the following points:

Market Penetration: Comprehensive information on mold release agents offered by top players in the global market

Analysis of key drivers: (Rapid growth of automotive and construction industries, increasing demand from automotive and furniture applications), restraints (Stringent regulations on solvent-based mold release agents, rising use of non-stick coatings on molds), opportunities (infrastructure development in emerging economies), and challenges (fluctuating raw material prices), influencing the growth of the mold release agents market

Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the mold release agents market

Market Development: Comprehensive information about lucrative emerging markets across regions

Market Diversification: Exhaustive information about products, untapped regions, and recent developments in the global mold release agents market

Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the mold release agents market

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 UNIT CONSIDERED

1.6 STAKEHOLDERS

1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

2.3 DISRUPTIVE TRENDS IN MOLD RELEASE AGENTS MARKET

2.4 HIGH-GROWTH SEGMENTS

2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN MOLD RELEASE AGENTS MARKET

3.2 MOLD RELEASE AGENTS MARKET, BY APPLICATION AND REGION

3.3 MOLD RELEASE AGENTS MARKET, BY TYPE

3.4 MOLD RELEASE AGENTS MARKET, BY COUNTRY

4 MARKET OVERVIEW

4.1 INTRODUCTION

4.2 MARKET DYNAMICS

4.2.1 DRIVERS

4.2.1.1 Rapid growth of automotive and construction industries

4.2.1.2 Increased consumption in high-performance manufacturing applications

4.2.2 RESTRAINTS

4.2.2.1 Stringent regulations on solvent-based mold release agents

4.2.2.2 Extensive use of non-stick coatings on molds

4.2.3 OPPORTUNITIES

4.2.3.1 Infrastructure development in emerging economies

4.2.4 CHALLENGES

4.2.4.1 Fluctuating raw material prices

4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

4.3.1 INTERCONNECTED MARKETS

4.3.2 CROSS-SECTOR OPPORTUNITIES

4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

5.1 PORTER'S FIVE FORCES ANALYSIS

5.1.1 THREAT OF NEW ENTRANTS

5.1.2 THREAT OF SUBSTITUTES

5.1.3 BARGAINING POWER OF SUPPLIERS

5.1.4 BARGAINING POWER OF BUYERS

5.1.5 INTENSITY OF COMPETITIVE RIVALRY

5.2 MACROECONOMIC INDICATORS

5.2.1 INTRODUCTION

5.2.2 GDP TRENDS AND FORECAST

5.2.3 TRENDS IN GLOBAL AUTOMOTIVE INDUSTRY

5.3 SUPPLY CHAIN ANALYSIS

5.3.1 RAW MATERIALS

5.3.2 MANUFACTURING

5.3.3 DISTRIBUTION

5.3.4 APPLICATION

5.4 ECOSYSTEM ANALYSIS

5.5 PRICING ANALYSIS

5.5.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY APPLICATION, 2024

5.5.2 AVERAGE SELLING PRICE TREND, BY REGION, 2022-2025

5.6 TRADE ANALYSIS

5.6.1 IMPORT SCENARIO (HS CODE 340399)

5.6.2 EXPORT SCENARIO (HS CODE 340399)

5.7 KEY CONFERENCES AND EVENTS, 2026

5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.9 INVESTMENT AND FUNDING SCENARIO

5.10 CASE STUDY ANALYSIS

5.10.1 OPTIMIZING AUTOMOTIVE SEATING FOAM PRODUCTION WITH SPRAYIQ AND ADVANCED RELEASE AGENT

5.10.2 REDUCING COSTS AND ENHANCING EFFICIENCY WITH ADVANCED RELEASE AGENTS

5.10.3 TRANSFORMING DENTAL MANUFACTURING WITH RELEASYS ECO-W

5.11 IMPACT OF 2025 US TARIFF

5.11.1 KEY TARIFF RATES

5.11.2 PRICE IMPACT ANALYSIS

5.11.3 IMPACT ON COUNTRY/REGION

5.11.3.1 US

5.11.3.2 Europe

5.11.3.3 Asia Pacific

5.11.4 IMPACT ON APPLICATIONS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, AND INNOVATIONS

6.1 KEY TECHNOLOGIES

6.1.1 TECHNOMELT LOW-PRESSURE MOLDING TECHNOLOGY

6.1.2 FLUORO TECHNOLOGY

6.2 COMPLEMENTARY TECHNOLOGIES

6.2.1 NANOMOLD TECHNOLOGY

6.3 TECHNOLOGY/PRODUCT ROADMAP

6.3.1 SHORT-TERM (2025-2027): COST OPTIMIZATION AND PROCESS CONSISTENCY

6.3.2 MID-TERM (2027-2030): PERFORMANCE ENHANCEMENT AND APPLICATION EXPANSION

6.3.3 LONG-TERM (2030-2035+): SUSTAINABILITY, DIGITALIZATION, AND INTEGRATION

6.4 PATENT ANALYSIS

6.4.1 APPROACH

6.4.2 DOCUMENT TYPES

6.4.3 TOP APPLICANTS

6.4.4 JURISDICTION ANALYSIS

6.5 IMPACT OF AI/GEN AI

6.5.1 TOP USE CASES AND MARKET POTENTIAL

6.5.2 BEST PRACTICES

6.5.3 CASE STUDIES OF AI IMPLEMENTATION

6.5.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

6.5.5 CLIENTS' READINESS TO ADOPT GEN AI

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITATIVES

7.1 REGIONAL REGULATIONS AND COMPLIANCE

7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

7.1.2 INDUSTRY STANDARDS

7.2 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

7.2.1 SAFETY PROTOCOLS

7.2.2 SUSTAINABLE DEVELOPMENT

7.2.3 STANDARDIZATION

7.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

8.1 DECISION-MAKING PROCESS

8.2 KEY STAKEHOLDERS IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

8.2.2 BUYING CRITERIA

8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

8.4 UNMET NEEDS FROM APPLICATIONS

9 MOLD RELEASE AGENTS MARKET, BY TYPE

9.1 INTRODUCTION

9.2 WATER-BASED

9.2.1 EXTENSIVE USE IN DIE CASTING AND CONCRETE PRODUCTS

9.3 SOLVENT-BASED

9.3.1 STRICT GOVERNMENT REGULATIONS IMPEDING LARGE-SCALE ADOPTION

9.4 OTHER TYPES

10 MOLD RELEASE AGENTS MARKET, BY APPLICATION

10.1 INTRODUCTION

10.2 DIE CASTING

10.2.1 HIGH DEMAND FROM AUTOMOTIVE, MARINE, AND AEROSPACE INDUSTRIES

10.3 PU MOLDING

10.3.1 LARGE-SCALE ADOPTION IN INSULATION BACKING FOAMS AND VISCOELASTIC PU PRODUCTS

10.4 RUBBER MOLDING

10.4.1 PREDOMINANCE IN TIRE, GASKET, AND SEAL PRODUCTION

10.5 COMPOSITE MOLDING

10.5.1 RISING NEED FOR CONSISTENT RELEASE PERFORMANCE AND REDUCED CYCLE TIME

10.6 PLASTIC MOLDING

10.6.1 EMPHASIS ON REDUCING CONTAMINATION AND PREVENTING CHEMICAL DEPLETION

10.7 WOOD COMPOSITE & PANEL PRESSING

10.7.1 HEIGHTENED DEMAND FROM CONSTRUCTION INDUSTRY

10.8 CONCRETE

10.8.1 SIGNIFICANCE OF STAMPED CONCRETE IN ARCHITECTURAL APPLICATIONS

10.9 OTHER APPLICATIONS

11 MOLD RELEASE AGENTS MARKET, BY REGION

11.1 INTRODUCTION

11.2 ASIA PACIFIC

11.2.1 CHINA

11.2.1.1 Ongoing industrialization to drive market

11.2.2 JAPAN

11.2.2.1 Robust automotive industry to drive market

11.2.3 INDIA

11.2.3.1 Growing infrastructure development to drive market

11.2.4 SOUTH KOREA

11.2.4.1 Demand from diverse industrial applications to drive market

11.3 NORTH AMERICA

11.3.1 US

11.3.1.1 Extensive utilization in automotive, construction, and aerospace & defense industries to drive market

11.3.2 CANADA

11.3.2.1 Expansion of domestic manufacturing capabilities to drive market

11.3.3 MEXICO

11.3.3.1 Rapid development and shift of key industries from US to drive market

11.4 EUROPE

11.4.1 GERMANY

11.4.1.1 High automotive production volumes to drive market

11.4.2 FRANCE

11.4.2.1 Economic dynamism and robust industrial hubs to drive market

11.4.3 UK

11.4.3.1 Substantial investments in automotive and chemical industries to drive market

11.4.4 RUSSIA

11.4.4.1 Prominence of die casting application to drive market

11.4.5 ITALY

11.4.5.1 Steady growth of manufacturing industry to drive market

11.4.6 SPAIN

11.4.6.1 Significant presence of automotive manufacturers and suppliers to drive market

11.4.7 TURKEY

11.4.7.1 Large-scale manufacturing of building materials to drive market

11.5 MIDDLE EAST & AFRICA

11.5.1 GCC

11.5.1.1 Saudi Arabia

11.5.1.1.1 Strategic initiatives aimed at diversifying economy to drive market

11.5.2 SOUTH AFRICA

11.5.2.1 Increasing demand from construction and automotive industries to drive market

11.6 SOUTH AMERICA

11.6.1 BRAZIL

11.6.1.1 Rising production of commercial and defense aircraft to drive market

11.6.2 ARGENTINA

11.6.2.1 Heightened demand for rubber products to drive market

12 COMPETITIVE LANDSCAPE

12.1 INTRODUCTION

12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

12.3 MARKET SHARE ANALYSIS, 2024

12.4 REVENUE ANALYSIS, 2020-2024

12.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

12.5.1 STARS

12.5.2 EMERGING LEADERS

12.5.3 PERVASIVE PLAYERS

12.5.4 PARTICIPANTS

12.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

12.5.5.1 Company footprint

12.5.5.2 Region footprint

12.5.5.3 Type footprint

12.5.5.4 Application footprint

12.6 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2024