동물 정형외과 시장 : 제품별, 동물 유형별, 용도별, 재료별, 최종사용자별, 지역별 - 세계 예측(-2031년)

Veterinary Orthopedics Market by Product (Orthopedic Implants, Instruments, Consumables), Animal Type (Dog, Cat, Horse, Livestock), Application (TPLO, TTA, Fracture Repair), Material (Metallic, Absorbable), End User, and Region - Global Forecast to 2031

상품코드:1928854

리서치사:MarketsandMarkets

발행일:2026년 01월

페이지 정보:영문 630 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

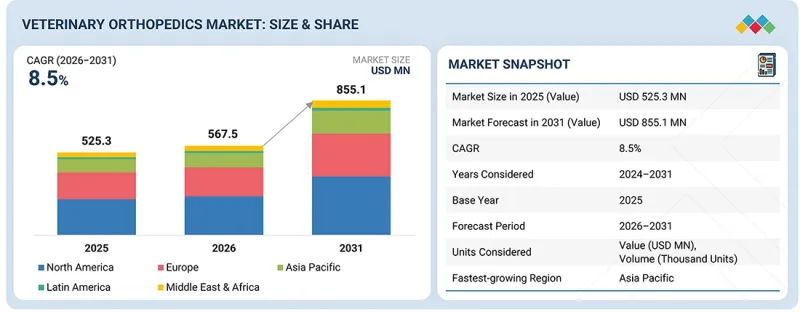

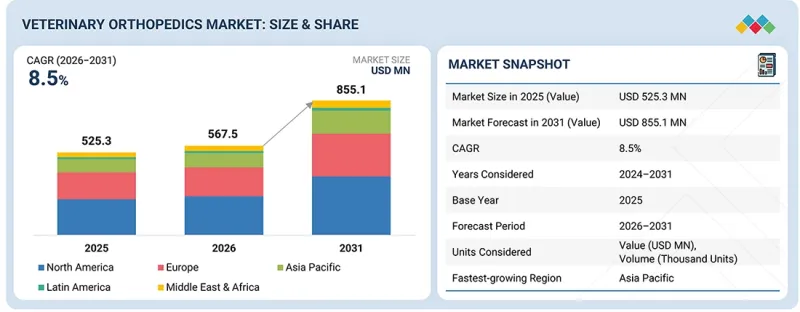

세계의 동물 정형외과 시장 규모는 2026년 5억 7,000만에서 2031년까지 8억 6,000만 달러에 달할 것으로 예측되며, CAGR로 8.5%의 성장이 전망됩니다.

이러한 성장은 동물 정형외과 치료, 외과적 개입, 동물의 운동 기능 회복의 미래를 형성하는 여러 요인에 의해 촉진되고 있습니다.

조사 범위

조사 대상 기간

2024-2031년

기준 연도

2025년

예측 기간

2026-2031년

단위

10억 달러

부문

제품, 용도, 재료, 최종사용자, 지역

대상 지역

북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카

반려동물과 가축의 근골격계 질환, 외상, 퇴행성 관절 질환의 발병률 증가, 반려동물 보호자들의 첨단 정형외과 수술에 대한 선호도 증가가 이 시장의 주요 촉진요인으로 작용할 것으로 보입니다. 수의학이 보다 전문화되고 결과 중심의 진료로 꾸준히 진화하면서 우수한 정형외과용 임플란트, 고정장치, 수술 지향적 수술 솔루션에 대한 수요가 증가하고 있습니다. 동물병원과 전문 진료소에서는 수술의 정확성, 회복 시간, 수술 후 이동성을 향상시킬 수 있는 혁신적인 솔루션이 요구되고 있습니다.

또한, 노화에 따른 정형외과적 질환, 비만 가축의 관절 질환, 외상 관련 사례의 증가로 인해 효과적이고 신뢰할 수 있는 표준화된 정형외과적 수술의 필요성이 증가하고 있습니다. 첨단 고정장치, 관절 안정화 제품, 재건 제품은 이러한 요구에 부응하는 데 중요한 역할을 합니다. 소개환자의 증가와 전문화된 정형외과 진료도 수술 건수 증가에 힘을 보태고 있습니다. 이미징의 발전, 디지털 수술 계획, 수술 후 재활 치료 등 동물 의료 부문의 현대화 추세는 정형외과 분야에서 첨단 솔루션의 채택 확대를 촉진하고 있습니다. 외과 의사의 교육 및 증거에 기반한 모범 사례에 대한 관심이 높아짐에 따라 채용률이 더욱 향상되고 있습니다.

강화된 생체 재료, 특정 환자 동물용 기기, 최소침습 수술, 3D 프린팅 수술 가이드 등의 기술 개발로 인해 동물 정형외과 시장이 발전하고 있습니다. 기기의 품질과 사용 편의성 향상은 예측 기간 동안 동물 정형외과 시장의 성장에 기여할 것으로 보입니다.

"동물 유형별로는 반려동물 부문이 예측 기간 동안 가장 높은 CAGR로 성장할 것으로 예상됩니다."

개와 고양이는 노화와 비만으로 인해 인대파열, 골절, 관절질환 등 정형외과적 질환에 걸리기 쉽기 때문에 이러한 제품에 대한 수요는 항상 존재합니다. 또한, 전문 동물병원에 대한 접근성, 반려동물 보호자들 사이에서 이러한 수술의 결과에 대한 인식이 확산되고, 반려동물 보험 가입률이 점진적으로 증가하고 있는 것도 이러한 성장을 뒷받침하고 있습니다.

"최종사용자별로는 동물병원 및 진료소 부문이 2025년 가장 큰 시장 점유율을 차지했습니다."

2025년 동물병원 및 클리닉 부문이 동물 정형외과 시장을 주도했습니다. 이는 동물의 정형외과 질환의 진단, 수술, 수술 후 후속 치료의 주요 수행 장소이기 때문입니다. 동물병원 및 클리닉에서 치료하는 외상, 인대손상, 퇴행성 관절질환의 수는 여전히 많으며, 정교한 수술장비와 정형외과적 치료능력을 갖춘 시설이 증가하는 추세입니다. 또한, 여러 전문분야를 가진 동물병원의 발전과 소개가 아닌 병원 내 정형외과 진료에 대한 노력은 동물병원 및 동물병원의 이용 증가 요인으로 작용하고 있습니다.

"아시아태평양이 예측 기간 동안 가장 높은 성장률을 보일 것으로 예상됩니다."

아시아태평양은 동물 정형외과 시장에서 가장 높은 CAGR을 보일 가능성이 높습니다. 이는 중국, 인도, 일본, 호주 등의 국가에서 반려동물을 키우는 가구 수가 급증하고 동물 의료비가 지속적으로 증가하고 있기 때문입니다. 정형외과 전문병원과 진료 의뢰 센터의 발달로 수의학 인프라가 개선되면서 진단 검사 및 수술에 대한 접근성이 확대되고 있습니다. 또한, 삶의 질에 있어 운동 기능의 중요성에 대한 인식의 증가, 정형외과 의사의 가용성, 반려동물 보험의 이용 확대 등이 수술의 도입을 촉진하고 있습니다.

세계의 동물 정형외과 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도 등의 정보를 전해드립니다.

목차

제1장 소개

제2장 주요 요약

제3장 중요한 인사이트

동물 정형외과 시장 개요

아시아태평양의 동물 정형외과 시장 : 제품별, 국가별(2025년)

동물 정형외과 시장 : 지역 구성

동물 정형외과 시장 : 지리적 성장 기회

동물 정형외과 시장 : 선진국 vs. 신흥국

제4장 시장 개요

시장 역학

성장 촉진요인

성장 억제요인

기회

과제

미충족 수요와 화이트 스페이스

동물 정형외과 시장의 미충족 수요

화이트 스페이스 기회

상호 접속된 시장과 부문 횡단적인 기회

상호 접속된 시장

부문 횡단적인 기회

Tier 1/2/3 기업의 전략적 활동

제5장 업계 동향

Porter's Five Forces 분석

거시경제 지표

GDP 동향과 예측

세계의 의료 업계 동향

세계의 동물 의료 업계 동향

공급망 분석

밸류체인 분석

생태계 분석

가격 책정 분석

동물 정형외과 제품 평균판매가격 동향 : 주요 기업별(2023-2025년)

동물 정형외과 제품 평균판매가격 동향 : 재료별(2023-2025년)

동물 정형외과 제품 평균판매가격 동향 : 지역별(2023-2025년)

무역 분석

HS 코드 9021의 무역 데이터

HS 코드 9018의 무역 데이터

주요 회의와 이벤트(2026-2027년)

고객 비즈니스에 영향을 미치는 동향/디스럽션

투자와 자금 조달 시나리오

성공 사례와 실세계에 대한 응용

복잡한 개 사지 재건에 활용되는 특정 환축용 3D 프린팅 임플란트

최신 정형외과 임플란트 시스템을 이용한 소동물의 첨단 골절 고정

반려동물에서의 첨단 정형외과 수술 개입의 장기 임상 결과

동물 정형외과 시장에 대한 2025년 미국 관세의 영향

주요 관세율

가격의 영향 분석

국가/지역에 대한 영향

최종 이용 산업에 대한 영향

제6장 기술, 특허, 디지털과 AI 채용에 의한 전략적 파괴

기술 분석

주요 신기술

보완 기술

인접 기술

기술/제품 로드맵

단기(2025-2027년)

중기(2028-2030년)

장기(2030년 이후)

특허 분석

동물 정형외과의 특허 공보 동향

관할구역과 주요 신청자 분석

향후 용도

특정 환축용 정형외과 임플란트 및 수술 가이드

저침습·영상 유도 정형외과 수술

재생의료와 생물학적 제제를 활용한 정형외과 치료

디지털 수술 계획과 AI가 지원하는 의사 결정 지원

통합 재활, 모빌리티 트래킹, 장기적 성과 관리

동물 정형외과 시장에 대한 AI/생성형 AI의 영향

동물 정형외과 생태계의 시장 전망

AI 이용 사례

동물 정형외과 시장에서 AI를 도입하고 있는 주요 기업

제7장 지속가능성과 규제 상황

지역 규제와 컴플라이언스

규제 분석

규제기관, 정부기관, 기타 조직

업계 표준

지속가능성에 대한 대처

동물 정형외과 제품용 재생 재료, 친환경 재료

지속가능성에 대한 영향과 규제 정책의 대처

인증, 라벨, 환경기준

제8장 고객 상황과 구매 행동

주요 이해관계자와 구입 기준

고객 상황과 구매 행동

의사결정 프로세스

채용 장벽과 내부 과제

다양한 최종 이용 산업으로부터의 미충족 수요

시장 수익성

제9장 동물 정형외과 시장 : 제품별

임플란트

기구

소모품

제10장 동물 정형외과 시장 : 재료별

금속

흡수성

제11장 동물 정형외과 시장 : 동물 유형별

반려동물

가축

제12장 동물 정형외과 시장 : 용도별

관절 치환술

상처 고정

특정 수술

제13장 동물 정형외과 시장 : 최종사용자별

동물병원·진료소

전문 정형외과 클리닉

구급 동물병원

학술연구기관

동물 재활 센터

제14장 동물 정형외과 시장 : 지역별

세계의 동물 정형외과 시장 수량 분석(2024-2031년)

북미

북미의 거시경제 전망

북미의 수량 분석 : 제품별(2024-2031년)

북미의 수량 분석 : 재료별(2024-2031년)

미국

캐나다

유럽

유럽의 거시경제 전망

유럽의 수량 분석 : 제품별(2024-2031년)

유럽의 수량 분석 : 재료별(2024-2031년)

독일

영국

프랑스

이탈리아

스페인

네덜란드

기타 유럽

아시아태평양

아시아태평양의 거시경제 전망

아시아태평양의 수량 분석 : 제품별(2024-2031년)

아시아태평양의 수량 분석 : 재료별(2024-2031년)

중국

일본

인도

호주

한국

태국

뉴질랜드

기타 아시아태평양

라틴아메리카

라틴아메리카의 거시경제 전망

라틴아메리카의 수량 분석 : 제품별(2024-2031년)

라틴아메리카의 수량 분석 : 재료별(2024-2031년)

브라질

멕시코

기타 라틴아메리카

중동 및 아프리카

중동 및 아프리카의 거시경제 전망

중동 및 아프리카의 수량 분석 : 제품별(2024-2031년)

중동 및 아프리카의 수량 분석 : 재료별(2024-2031년)

GCC 국가

기타 중동 및 아프리카

제15장 경쟁 구도

개요

주요 진출 기업의 전략/강점

매출 분석(2021-2025년)

시장 점유율 분석(2025년)

미국의 시장 점유율 분석(2025년)

유럽의 시장 점유율 분석(2025년)

주요 시장 기업 순위

기업 평가 매트릭스 : 주요 기업(2025년)

기업 평가 매트릭스 : 스타트업/중소기업(2025년)

브랜드/제품의 비교

주요 기업 연구개발비

기업 평가와 재무 지표

경쟁 시나리오

제16장 기업 개요

주요 기업

MOVORA

SECUROS SURGICAL(CENCORA, INC.)

DEPUY SYNTHES(JOHNSON & JOHNSON)

ARTHREX, INC.

ORTHOMED(UK) LTD.

B. BRAUN SE

VETERINARY INSTRUMENTATION

ANTECH DIAGNOSTICS, INC.

RITA LEIBINGER GMBH & CO. KG

BLUESAO

INTEGRA LIFESCIENCES CORPORATION

INTRAUMA S.P.A

SURGICAL HOLDINGS VETERINARY

PH ORTHCOM

GERVETUSA

기타 기업

NARANG MEDICAL LIMITED

FUSION IMPLANTS

BIO3DTECH

ORTHOMAX MFG. CO. PVT. LTD.

VET ORTHOPEDICS

WELL TRUST(TIANJIN) TECH CO., LTD.

VETERINARYIMPLANTS.COM(VETERINARY DIVISION OF GPC MEDICAL LTD.)

INVICTOS

SAFEX INC.

GSOURCE(ARCH MEDICAL SOLUTIONS)

제17장 조사 방법

제18장 부록

KSM

영문 목차

영문목차

The veterinary orthopedics market is expected to grow from USD 0.57 billion in 2026 to USD 0.86 billion by 2031, at a CAGR of 8.5%. This growth is driven by several key factors shaping the future of veterinary orthopedic care, surgical intervention, and mobility restoration in animals.

Scope of the Report

Years Considered for the Study

2024-2031

Base Year

2025

Forecast Period

2026-2031

Units Considered

Value (USD billion)

Segments

By Product, Application, Material, End User, Region

Regions covered

North America, Europe, Asia Pacific, South America, and the Middle East & Africa

The key factor driving this market is the rising incidence of musculoskeletal disorders, trauma, and degenerative joint diseases in companion and livestock animals, as well as the growing willingness of pet owners to opt for advanced orthopedic procedures. With the steady evolution of veterinary care toward greater specialization and results-oriented care, there is a growing demand for superior orthopedic implants, fixation devices, and procedure-oriented surgical solutions. Veterinary hospitals and specialty practices are seeking innovative solutions to improve surgical accuracy, recovery time, and post-surgical mobility.

In addition, the increasing prevalence of age-related orthopedic diseases, joint diseases in obese patients, and trauma-related cases is increasing the need for effective, reliable, and standardized orthopedic procedures. Advanced fixation devices, joint stabilizing, and reconstructive products are important in meeting this need. Increased referrals and specialized orthopedic practices are also fueling growth in procedures. Current modernization trends in the veterinary health sector, such as advancements in imaging, digital surgical planning, and post-operative rehabilitative care, are also driving increased adoption of advanced solutions in the orthopedic space. A growing emphasis on surgeon education and evidence-based best practices is further improving adoption rates.

Advances in the veterinary orthopedics market, driven by technological developments such as enhanced biomaterials and patient-specific devices, minimally invasive procedures, and 3D-printed surgical guides, are propelling the market forward. Enhancements in the quality and ease of usage of devices will contribute to the growth of the veterinary orthopedics market during the forecasted period.

"By animal type, the companion animals segment is projected to grow at the highest CAGR during the forecast period."

Dogs and cats are more prone to orthopedic disorders, such as ligament tears, fractures, and joint disorders, due to aging or obesity; hence, there is a constant demand for these products. Further, the easy accessibility of specialty animal hospitals, the growing awareness among owners of the outcomes of these procedures, and the gradually increasing adoption rate of pet insurance plans are also supporting this growth.

"By end user, the veterinary hospitals & clinics segment accounted for the largest market share in 2025."

In 2025, the veterinary hospitals & clinics segment dominated the veterinary orthopedics market as they are the primary locations for diagnosis and surgical and post-surgical follow-up treatments for orthopedic disorders in animals. The number of trauma cases, ligament injuries, and degenerative joint disorders treated by veterinary hospitals and clinics remains high, and they are increasingly set up with highly sophisticated surgical facilities and orthopedic capabilities. Moreover, the increased development of multi-specialty veterinary hospitals and the in-house approach to orthopedic care, rather than referral orthopedic care, are responsible for increased use within veterinary hospitals and clinics.

"The Asia Pacific region is expected to witness the highest growth rate during the forecast period."

The Asia Pacific region is likely to report the highest CAGR in the veterinary orthopedics market. This is due to the accelerated growth in the number of pet owners and continued increases in expenditure on animal care in countries such as China, India, Japan, and Australia. The improvement in veterinary infrastructure, with the development of orthopedic specialty hospitals and referral centers, is creating greater access to diagnostic work-ups and surgeries. Further, the growing recognition of the role of mobility in quality of life, along with the availability of orthopedic surgeons and the increased availability of pet insurance, is fueling the uptake of surgical procedures.

Breakdown of supply-side primary interviews:

By Company Type: Tier 1 (60%), Tier 2 (30%), and Tier 3 (10%)

By Designation: C-level Executives (30%), Directors (50%), and Other Designations (20%)

By Region: North America (40%), Europe (25%), Asia Pacific (20%), Latin America (10%), and the Middle East & Africa (5%)

Breakdown of demand-side primary interviews:

By End User: Veterinary Hospitals & Clinics (45%), Specialty Orthopedic Clinics (24%), Emergency Animal Hospitals (14%), Academic & Research Institutes (10%), and Animal Rehabilitation Centers (7%)

By Designation: Veterinarians (47%), Veterinary Hospital Directors & Managers (22%), Veterinary Critical Care Specialists (15%), and Others (16%)

By Region: North America (25%), Europe (24%), Asia Pacific (25%), Latin America (11%), and the Middle East & Africa (15%)

Research Coverage

The market study covers the veterinary orthopedics market in various segments. It aims to estimate the market size and growth potential by product, material, animal type, application, end user, and region. The study also includes an in-depth competitive analysis of the market's key players, along with their company profiles, key observations on their products and business offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report can assist established companies and newer or smaller firms in understanding market trends, enabling them to capture a larger share of the market. Firms that acquire the report can implement one or more of the five strategies outlined below.

This report provides insights into the following points:

Analysis of key drivers (rising companion animal ownership & spending on pet healthcare, higher incidence of orthopedic conditions, and growth in specialty veterinary hospitals & referral networks with advanced surgical capabilities and technology improvements in implants and instruments), restraints (high cost of orthopedic implants, instruments, and advanced surgical procedures and limited availability of trained veterinary orthopedic surgeons), opportunities (geographic expansion into emerging markets and growing adoption of patient-specific implants and 3d-printed guides), and challenges (clinical outcome variability and complication risk and regulatory and quality compliance across regions) influencing the growth of the veterinary orthopedics market.

Product Development/Innovation: Detailed insights on upcoming technologies and product launches in the veterinary orthopedics market.

Market Development: Comprehensive information about lucrative emerging markets. The report analyzes the markets for various types of veterinary orthopedic products across regions.

Market Diversification: Exhaustive information about products, untapped regions, recent developments, and investments in the veterinary orthopedics market.

Competitive Assessment: In-depth assessment of market shares, strategies, products, distribution networks, and manufacturing capabilities of the leading players in the veterinary orthopedics market.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

1.3.2 INCLUSIONS & EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.4 MARKET STAKEHOLDERS

2 EXECUTIVE SUMMARY

2.1 MARKET HIGHLIGHTS & KEY INSIGHTS

2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

2.3 DISRUPTIVE TRENDS IN VETERINARY ORTHOPEDICS MARKET

2.4 HIGH-GROWTH SEGMENTS

2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

3.1 VETERINARY ORTHOPEDICS MARKET OVERVIEW

3.2 ASIA PACIFIC: VETERINARY ORTHOPEDICS MARKET, BY PRODUCT & COUNTRY (2025)