Electronic Hydrofluoric Acid Market by Grade, Type, Application, & Region - Global Forecast to 2030

상품코드:1928850

리서치사:MarketsandMarkets

발행일:2026년 01월

페이지 정보:영문 288 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

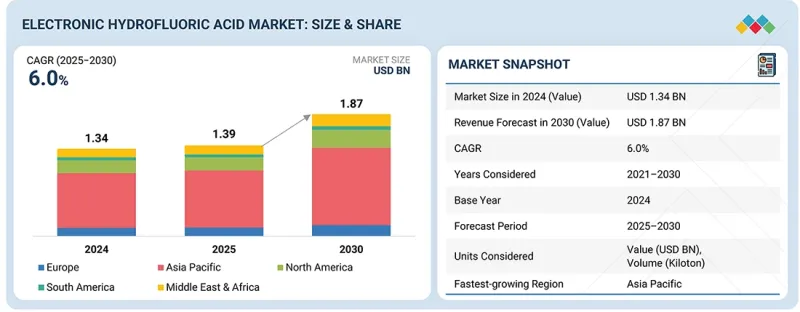

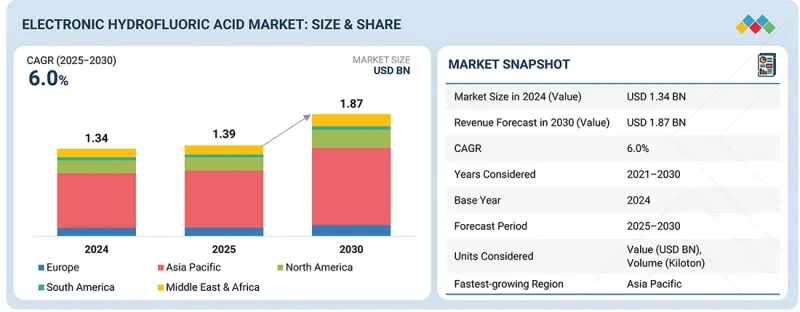

전자 불화 수소산 시장 규모는 2025년 13억 9,000만 달러에서 2030년까지 18억 7,000만 달러로 성장하고, CAGR 6.0%를 나타낼 것으로 예측됩니다.

조사 범위

조사 대상 기간

2021년-2030년

기준 연도

2024년

예측 기간

2025년-2030년

대상 단위

금액(100만 달러), 킬로톤

부문

등급별, 유형별, 용도별, 지역별

대상 지역

북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미

본 시장의 성장은 고순도 불화수소산의 주요 소비 산업인 반도체, 전자기기, 태양광 발전 산업의 지속적인 성장에 의해 주도되고 있습니다. 반도체 생산능력 확장은 계획된 팹 스케줄에 따라 관리되고 있기 때문에 불화수소산 수요는 예측 가능하며, 빠른 성장보다는 안정적인 성장세를 보이고 있습니다.

미세화 기술(7nm, 5nm 이하)로의 지속적인 전환과 고정밀 습식 에칭 공정의 보급은 초순수 불화수소산에 대한 수요를 더욱 강화하고 있습니다. 동시에 불소 공급 제한, 중국의 수출 규제, 엄격한 정제 기준 등 공급 측면의 제약이 시장의 균형을 유지하고 변동성을 억제하고 있습니다. 전반적으로 전자 불화수소산 소비량은 팹 확장 주기, 설비 투자 승인, 장기 공급 계약과 밀접하게 연계되어 있으며, 그 결과 시장은 매년 꾸준히 성장하고 있습니다.

UP-SSS 등급 부문은 전자 불화수소산 시장에서 가장 크고 가장 빠르게 성장하는 분야입니다. UP-SSS 등급 산은 3nm 로직 노드, 차세대 DRAM, 고적층 3D NAND 아키텍처 등 최첨단 반도체 제조의 엄격한 순도 요건을 충족시킬 수 있는 독보적인 능력을 가지고 있습니다. 이러한 첨단 기술 노드에서는 미량의 금속 오염도 심각한 결함, 수율 손실, 장기 신뢰성 문제를 야기할 수 있기 때문에 UP-SSS는 로직 및 메모리 제조의 수많은 불화수소산 기반 에칭 및 세정 공정에서 필수적입니다. TSMC, Samsung, Intel, Intel, SK hynix, Micron 등 주요 반도체 제조업체들은 모든 주요 습식 공정에서 UP-SSS 사용을 표준화하고 있으며, 이로 인해 견고하고 지속적인 수요가 발생하고 있습니다. UP-SSS는 웨이퍼당 소비량이 상대적으로 적고, 저급 불화수소산에 비해 가격 프리미엄이 크며, 세계 생산에서 최첨단 웨이퍼의 점유율이 확대됨에 따라 그 채택이 지속적으로 증가하는 추세에 있습니다.

플루오르스파이트 유래의 전자불화수소산은 불화규산 유래의 전자불화수소산보다 빠른 성장세를 보이고 있습니다. 이는 플루오르스파(CaF2)가 첨단 반도체 제조에서 요구되는 초순도 기준을 확실하게 달성할 수 있는 유일한 원료이기 때문입니다. 천연 형석을 출발 원료로 하여 금속 불순물, 미립자 물질, 규산염을 정밀하게 제어할 수 있어 ppt 수준 또는 ppt 미만의 불순물도 수율과 소자 신뢰성에 영향을 미칠 수 있는 최첨단 로직 칩, DRAM, 3D NAND 제조에 적합합니다. 한편, 인산비료 제조의 제품별 불화규산에서 얻어지는 불화수소산은 금속, 인산염, 실리카 등의 내재적 오염도가 높고, 전자 등급까지 정제하는 데 비용이 많이 들고 기술적으로도 어려움이 있습니다. 이 때문에 주로 산업용, 야금용 및 저급 전자 용도로만 사용됩니다. 2nm급 노드로의 전환, EUV 리소그래피, 고주파 습식 세정 공정 등 반도체 공정이 복잡해짐에 따라 초순수 불화수소산에 대한 수요는 더욱 증가하고 있습니다. 이 초순수 불화수소산은 불소계 제조 공정을 통해서만 안정적인 공급이 가능합니다. 중국, 멕시코, 남아공을 중심으로 한 불소 채굴 및 불화수소산 생산 능력에 대한 세계 투자와 함께 불소 기반 불화수소산 공급 신뢰성이 강화되고 있습니다. 한편, FSA 기반의 불화수소산은 변동이 심한 비료 생산 사이클에 의존하고 있습니다. 그 결과, 플루오르스파 기반 전자 불화수소산에 대한 수요가 FSA 기반 불화수소산을 계속 초과하고 있으며, 이는 첨단 반도체 제조에서 중요한 역할과 우수한 시장 성장 잠재력을 반영하고 있습니다.

반도체 웨이퍼는 첨단 반도체 제조와 노드 미세화의 급속한 확대로 인해 전자 불화수소산 시장에서 가장 빠르게 성장하고 있는 응용 분야입니다. 전자 불화수소산은 웨이퍼 제조의 여러 단계의 산화막 제거, 표면 세정, 이산화 규소 에칭과 같은 중요한 공정에서 웨이퍼 제조에 없어서는 안 될 필수 요소입니다. 더 미세한 공정 노드로의 전환, FinFET 및 게이트 올 어라운드 트랜지스터와 같은 3D 구조, 메모리 디바이스의 적층 수가 증가함에 따라 습식 에칭 및 세정 공정의 빈도와 순도 요구 사항이 크게 증가했습니다. 또한, 특히 아시아태평양의 팹에 대한 강력한 투자로 인해 웨이퍼 가공에서 초순수 전자 불화수소산에 대한 수요가 더욱 가속화되고 있습니다.

아시아태평양은 강력한 산업 확대와 지원적인 정책 프레임워크에 힘입어 전자 불화수소산 시장에서 가장 빠르게 성장하고 있습니다. 이 지역에는 신규 및 기존 반도체 팹, 플랫 패널 디스플레이 공장, 태양광 발전 제조시설이 집적되어 있으며, 전자기기, 재생에너지, 고성능 칩에 대한 세계 수요 증가에 대응하기 위해 규모 확대를 추진하고 있습니다. 역내 각국 정부는 반도체 현지 생산, 재생에너지 도입, 첨단 제조기술에 대한 특혜를 제공하고 있으며, 이는 새로운 제조라인과 첨단 웨이퍼 기술에 대한 투자를 촉진하고 있습니다. 아시아태평양은 현지 불소 채굴 및 불화수소산 생산을 포함한 고도로 통합된 화학 공급망의 혜택을 누리고 있으며, 이는 수입 의존도를 낮추고 공정의 신뢰성을 향상시키고 있습니다. 급속한 도시화, 가전제품의 보급 확대, 재료 및 공정 혁신에 대한 연구개발에 대한 관심이 높아지면서 고순도 불화수소산에 대한 수요를 더욱 촉진하고 있으며, 이 지역은 시장의 주요 성장 동력으로 자리매김하고 있습니다.

Honeywell International Inc.(미국), Solvay(벨기에), LANXESS(독일), Stella Chemifa Corporation(일본), DongYUE GROUP(중국), Soulbrain(한국), JUHUA Technology Inc. JUHUA Technology Inc.(중국), Gulf Flour(UAE), Formosa Daikin Advanced Chemicals(일본), MORITA CHEMICAL INDUSTRIES(일본) 등이 참여하고 있습니다. 전자 불화수소산 시장의 주요 주요 기업들에 대해 조사했으며, 기업 프로파일, 최근 동향, 주요 시장 전략을 포함한 상세한 경쟁 분석을 전해드립니다.

조사 범위

이 보고서는 전자 불화수소산 시장을 유형, 등급, 용도, 지역별로 세분화하고 각 지역의 전체 시장 규모 예측을 제공합니다. 주요 업계 진출기업을 상세하게 분석하여 사업 개요, 제품 및 서비스, 주요 전략, 전자불화수소산 시장과 관련된 사업 확장에 관한 정보를 제공합니다.

본 보고서 구매의 주요 이점

이 보고서는 다양한 수준의 분석, 산업 분석(업계 동향), 주요 기업의 시장 순위 분석, 기업 프로파일에 초점을 맞추고 있으며, 이를 종합하여 경쟁 구도, 전자 불화수소산 시장의 신흥 및 고성장 부문, 고성장 지역, 시장 성장 촉진요인, 저해요인, 기회, 과제에 대한 종합적인 관점을 제공합니다.에 대한 종합적인 견해를 제공합니다.

이 보고서는 다음 사항에 대한 인사이트를 제공합니다.

성장 촉진요인(반도체 및 첨단 전자기기 수요 급증), 억제요인(불화수소산의 극도로 높은 부식성과 건강 위험, 생산자 및 물류 사업자의 OSHA/EPA 준수, 비상 대응, 보험 비용 증가), 기회(반도체 제조 공장은 단납기 및 운송 위험 감소를 우선시함; 반도체 클러스터(미국, 유럽, 인도, 동남아시아) 인근에 설치된 소형 모듈식 불화수소산 정제 유닛은 고부가가치 계약 수주 가능), 과제(ppb 미만의 금속 함량, 미량 유기물 관리, 배치 간 순도 일관성 입증, 고도의 분석 기술, 클린룸 포장, 인증 및 추적성 필요) 추적가능성 필요)

시장 침투: 시장을 선도하는 주요 기업별 전자 불화수소산 시장에 대한 종합적인 정보.

제품 개발 및 혁신 : 시장에서의 향후 기술 동향, 연구개발 활동, 제휴, 계약, 합작투자, 공동연구, 발표, 수상, 사업 확장에 대한 상세한 분석.

시장 개발: 수익성 높은 신흥 시장에 대한 종합적인 정보. 이 보고서는 지역별로 전자불화수소산 시장을 분석했습니다.

시장 용량: 불화수소산 생산 기업의 생산 능력(가능한 경우) 및 향후 불화수소산 시장에서의 생산 능력에 대한 정보를 제공합니다.

경쟁 평가: 전자 불화수소산 시장에서 주요 기업의 시장 점유율, 전략, 제품, 생산 능력에 대한 상세한 평가.

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

시장 역학

성장 촉진요인

성장 억제요인

기회

과제

미충족 요구와 공백

연결된 시장과 분야간 기회

Tier1/2/3참여 기업 전략적 움직임

제5장 업계 동향

Porter의 Five Forces 분석

거시경제 지표

공급망 분석

밸류체인 분석

가격 분석

생태계 분석

고객의 비즈니스에 영향을 미치는 동향/혼란

무역 분석

투자 및 자금조달 시나리오

사례 연구 분석

2025년 미국 관세의 영향-전자 불화 수소산시장

제6장 기술 진보, AI 별 영향, 특허, 혁신, 향후 응용

주요 신기술

보완적 기술

기술/제품 로드맵

특허 분석

향후 응용

AI/생성형 AI가 전자 불화 수소산시장에 미치는 영향

성공 사례와 실세계에의 응용

제7장 지속가능성과 규제 상황

지역 규제와 컴플라이언스

지속가능성 이니셔티브

지속가능성에 대한 영향과 규제 정책 대처

인증, 라벨, 환경기준

제8장 고객 상황과 구매 행동

의사결정 프로세스

구입자 이해관계자와 구입 평가 기준

채택 장벽과 내부 과제

일렉트로닉스 및 반도체 산업 미충족 요구

시장 수익성

제9장 전자 불화 수소산시장(등급별)

EL 등급

업그레이드

UPS

UP-SS

UP-SSS

제10장 전자 불화 수소산시장(유형 유별)

형석 기반

플루오르 규산 기반

제11장 전자 불화 수소산시장(용도별)

반도체 웨이퍼

태양전지

플랫 패널 디스플레이

LED와 화합물 반도체

전자부품

광섬유

MEMS

제12장 전자 불화 수소산시장(지역별)

아시아태평양

중국

일본

인도

한국

기타

북미

미국

캐나다

멕시코

유럽

독일

이탈리아

프랑스

스페인

영국

기타

중동 및 아프리카

GCC 국가

남아프리카공화국

기타

남미

브라질

아르헨티나

기타

제13장 경쟁 구도

주요 시장 진출기업의 전략/강점(2021년-2025년)

시장 점유율 분석, 2024년

매출 분석, 2021년-2025년

제품 비교

기업 평가 매트릭스 : 주요 시장 진출기업, 2024년

기업 평가 매트릭스 : 스타트업/중소기업, 2024년

경쟁 시나리오와 동향

제14장 기업 개요

주요 시장 진출기업

STELLA CHEMIFA CORPORATION

LANXESS

SOLVAY

MORITA CHEMICAL INDUSTRIES CO., LTD.

FORMOSA DAIKIN ADVANCED CHEMICALS CO., LTD.

DONGYUE GROUP

HONEYWELL INTERNATIONAL INC.

NAVIN FLUORINE INTERNATIONAL LIMITED

BASF

GULF FLUOR

기타 기업

ZHEJIANG YONGHE REFRIGERANT CO., LTD.

HALOPOLYMER OJSC

SINOCHEM LANTIAN CO., LTD.

FUJIAN YONGJING TECHNOLOGY CO., LTD.

LIAONING EAST SHINE CHEMICAL TECHNOLOGY CO., LTD.

LUOYANG FENGRUI FLUORINE INDUSTRY CO., LTD.

ZHEJIANG SANMEI CHEMICAL INCORPORATED COMPANY

TANFAC INDUSTRIES LTD.

DERIVADOS DEL FLUOR SAU

ULBA METALLURGICAL PLANT JSC

FUBAO GROUP

FOOSUNG CO., LTD.

제15장 조사 방법

제16장 부록

LSH

영문 목차

영문목차

The electronic hydrofluoric acid market size is projected to grow from USD 1.39 billion in 2025 to USD 1.87 billion by 2030, registering a CAGR of 6.0%.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million), Volume (Kiloton)

Segments

Grade, Type, Application, and Region

Regions covered

North America, Asia Pacific, Europe, Middle East & Africa, and South America

The growth of this market is driven by the sustained expansion of the semiconductor, electronics, and photovoltaic industries, which are the primary consumers of high-purity hydrofluoric acid. Growth is stable rather than rapid because semiconductor capacity expansions are controlled and based on planned fab schedules, ensuring predictable demand for hydrofluoric acid.

The ongoing shift toward smaller technology nodes (7 nm, 5 nm, and below) and high-precision wet-etching processes further reinforces the need for ultra-high-purity hydrofluoric acid. At the same time, supply-side constraints, including limited fluorspar availability, export regulations in China, and strict purification standards, maintain market balance and prevent volatility. Overall, electronic hydrofluoric acid consumption closely follows fab expansion cycles, capital investment approvals, and long-term supply agreements, resulting in steady, year-on-year market growth.

"UP-SSS is the largest grade segment of the electronic hydrofluoric acid market in terms of value."

The UP-SSS grade segment is the largest and fastest-growing segment of the electronic hydrofluoric acid market. UP-SSS grade acid is uniquely capable of meeting the ultra-stringent purity requirements of leading-edge semiconductor manufacturing, including 3 nm logic nodes, next-generation DRAM, and high-stack 3D NAND architectures. At these advanced technology nodes, even trace-level metallic contamination can result in critical defects, yield loss, or long-term reliability issues, making UP-SSS essential for the numerous hydrofluoric acid-based etching and cleaning steps in both logic and memory fabrication. Major semiconductor manufacturers, including TSMC, Samsung, Intel, SK hynix, and Micron, have standardized the use of UP-SSS in all critical wet processes, driving strong and consistent demand. Although the consumption per wafer is relatively low, UP-SSS commands a significant price premium over lower-grade hydrofluoric acid, and its adoption continues to grow in tandem with the increasing share of cutting-edge wafers in global production.

"Fluorite-based is the fastest-growing type segment of the electronic hydrofluoric acid market in terms of value."

Fluorite-based electronic hydrofluoric acid is experiencing faster growth than hydrofluoric acid sourced from fluorosilicic acid because fluorite (CaF2) is the only feedstock that can reliably achieve the ultra-high purity standards demanded by advanced semiconductor manufacturing. Using natural fluorspar as a starting material allows precise control over metallic contaminants, particulates, and silicates, making it suitable for cutting-edge logic chips, DRAM, and 3D NAND fabrication, where even ppt- or sub-ppt-level impurities can impact yield and device reliability. In contrast, hydrofluoric acid obtained from fluorosilicic acid, a by-product of phosphate fertilizer production, has higher inherent contamination levels, including metals, phosphates, and silica, making it costly and technically challenging to purify to electronic standards. This restricts its use primarily to industrial, metallurgical, and lower-end electronic applications. The growing complexity of semiconductor processes, including the shift toward 2 nm-class nodes, EUV lithography, and intensive wet-cleaning sequences, has further amplified the need for ultra-pure hydrofluoric acid, which can be consistently supplied only through fluorite-based production. Coupled with global investments in fluorspar mining and hydrofluoric acid manufacturing capacity, particularly in China, Mexico, and South Africa, this has strengthened the supply reliability of fluorite-based hydrofluoric acid, while FSA-based hydrofluoric acid remains dependent on variable fertilizer production cycles. Consequently, demand for fluorite-based electronic hydrofluoric acid continues to outpace FSA-based hydrofluoric acid, reflecting its critical role in advanced semiconductor fabrication and superior market growth potential.

"Semiconductor wafers are the fastest-growing application segment of the electronic hydrofluoric acid market in terms of value."

Semiconductor wafers represent the fastest-growing application segment for the electronic hydrofluoric acid market due to the rapid expansion of advanced semiconductor manufacturing and node miniaturization. Electronic hydrofluoric acid is indispensable in wafer fabrication for critical processes such as native oxide removal, surface cleaning, and silicon dioxide etching at multiple stages of device production. The transition toward smaller process nodes, 3D architectures such as FinFETs and gate-all-around transistors, and increased layer stacking in memory devices significantly raise the frequency and purity requirements of wet etching and cleaning steps. Additionally, strong investments in fabs, particularly in the Asia Pacific, further accelerate demand for ultra-high-purity electronic hydrofluoric acid in wafer processing.

"Asia Pacific is the fastest-growing electronic hydrofluoric acid market in terms of value."

The Asia Pacific is the fastest-growing electronic hydrofluoric acid market, driven by strong industrial expansion and supportive policy frameworks. The region hosts a concentration of emerging and established semiconductor fabs, flat-panel display plants, and solar PV manufacturing facilities, which are scaling up to meet growing global demand for electronics, renewable energy, and high-performance chips. Governments across the region are offering incentives for local semiconductor production, renewable energy adoption, and advanced manufacturing, which encourages investment in new fabrication lines and advanced wafer technologies. The Asia Pacific region benefits from a well-integrated chemical supply chain, including local fluorspar mining and hydrofluoric acid production, which reduces its dependency on imports and improves process reliability. Rapid urbanization, growing adoption of consumer electronics, and increasing focus on research and development in materials and process innovation further drive demand for high-purity hydrofluoric acid, positioning the region as the leading growth engine in the market.

In-depth interviews were conducted with chief executive officers (CEOs), marketing directors, other innovation and technology directors, and executives from various key organizations operating in the electronic hydrofluoric acid market. Information was gathered from secondary research to determine and verify the market size of several segments.

By Company Type: Tier 1 - 50%, Tier 2 - 30%, and Tier 3 - 20%

By Designation: Managers - 15%, Directors - 20%, and Others - 65%

By Region: North America - 25%, Europe - 15%, Asia Pacific - 45%, Middle East & Africa - 10%, and South America - 5%.

The electronic hydrofluoric acid market comprises Honeywell International Inc. (US), Solvay (Belgium), LANXESS (Germany), Stella Chemifa Corporation (Japan), DONGYUE GROUP (China), Soulbrain Co., Ltd. (South Korea), JUHUA Technology Inc. (China), Gulf Flour (UAE), Formosa Daikin Advanced Chemicals Co., Ltd. (Japan), and MORITA CHEMICAL INDUSTRIES CO., LTD (Japan). The study includes an in-depth competitive analysis of key players in the electronic hydrofluoric acid market, featuring their company profiles, recent developments, and key market strategies.

Research Coverage

This report segments the market for electronic hydrofluoric acid on the basis of type, grade, application, and region, and provides estimations for the overall value of the market across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, products & services, key strategies, and expansions associated with the market for electronic hydrofluoric acid.

Key benefits of buying this report

This research report is focused on various levels of analysis, industry analysis (industry trends), market ranking analysis of top players, and company profiles, which together provide an overall view of the competitive landscape; emerging and high-growth segments of the electronic hydrofluoric acid market; high-growth regions; and market drivers, restraints, opportunities, and challenges.

The report provides insights into the following pointers:

Analysis of drivers (Surging semiconductor and advanced electronics demand), restraints (Hydrofluoric acid's extreme corrosivity and health risk raise OSHA/EPA compliance, emergency response, and insurance costs for producers and logistics providers), opportunities (Fabs prefer shorter lead times and lower transport risk; small modular hydrofluoric acid purification units located near semiconductor clusters (US, Europe, India, & Southeast Asia) can win premium contracts), and challenges (Demonstrating sub-ppb metal levels, trace organic control, and consistent batch-to-batch purity need advanced analytics, cleanroom packaging, and certified traceability).

Market Penetration: Comprehensive information on the electronic hydrofluoric acid market offered by top players in the market.

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, partnerships, agreements, joint ventures, collaborations, announcements, awards, and expansions in the market.

Market Development: Comprehensive information about lucrative emerging markets. The report analyzes the electronic hydrofluoric acid market across regions.

Market Capacity: Production capacities of companies producing electronic hydrofluoric acid are provided wherever available, with upcoming capacities for the electronic hydrofluoric acid market.

Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the electronic hydrofluoric acid market.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.3.4 CURRENCY CONSIDERED

1.3.5 UNIT CONSIDERED

1.4 STAKEHOLDERS

2 EXECUTIVE SUMMARY

2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

2.2 KEY MARKET PARTICIPANTS: INSIGHTS AND STRATEGIC DEVELOPMENTS

2.3 DISRUPTIVE TRENDS SHAPING THE MARKET

2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ELECTRONIC HYDROFLUORIC ACID MARKET

3.2 ELECTRONIC HYDROFLUORIC ACID MARKET, BY TYPE AND REGION

3.3 ELECTRONIC HYDROFLUORIC ACID MARKET, BY GRADE

3.4 ELECTRONIC HYDROFLUORIC ACID MARKET, BY APPLICATION

3.5 ELECTRONIC HYDROFLUORIC ACID MARKET, BY COUNTRY

4 MARKET OVERVIEW

4.1 INTRODUCTION

4.2 MARKET DYNAMICS

4.2.1 DRIVERS

4.2.1.1 Rising global semiconductor wafer fabrication capacity

4.2.1.2 Expansion of AI, 5G, EV, and high-performance computing applications

4.2.1.3 Growing adoption of 300 mm wafers and higher wafer throughput

4.2.2 RESTRAINTS

4.2.2.1 High production and purification costs associated with ultra-high-purity requirements

4.2.2.2 Growing adoption of alternative processes such as vapor HF and dry plasma etching

4.2.3 OPPORTUNITIES

4.2.3.1 Increasing adoption of advanced device architectures such as FinFETs and gate-all-around (GAA) transistors

4.2.3.2 Growth of compound semiconductors (SiC, GaN) and MEMS devices

4.2.4 CHALLENGES

4.2.4.1 Maintaining consistent ppt-ppb level impurity control across large production volumes

4.2.4.2 Meeting stringent environmental, safety, and compliance standards without disrupting fab operations

4.3 UNMET NEEDS AND WHITE SPACES

4.3.1 UNMET NEEDS IN ELECTRONIC HYDROFLUORIC ACID MARKET

4.3.2 WHITE SPACE OPPORTUNITIES

4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

4.4.1 INTERCONNECTED MARKETS

4.4.2 CROSS-SECTOR OPPORTUNITIES

4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

4.5.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

5.1 PORTER'S FIVE FORCES ANALYSIS

5.1.1 THREAT OF NEW ENTRANTS

5.1.2 THREAT OF SUBSTITUTES

5.1.3 BARGAINING POWER OF SUPPLIERS

5.1.4 BARGAINING POWER OF BUYERS

5.1.5 INTENSITY OF COMPETITIVE RIVALRY

5.2 MACROECONOMICS INDICATORS

5.2.1 INTRODUCTION

5.2.2 GDP TRENDS AND FORECAST

5.2.3 TRENDS IN GLOBAL ELECTRONICS INDUSTRY

5.3 SUPPLY CHAIN ANALYSIS

5.4 VALUE CHAIN ANALYSIS

5.5 PRICING ANALYSIS

5.5.1 AVERAGE SELLING PRICE OF ELECTRONIC HYDROFLUORIC ACID, BY TYPE, 2024

5.5.2 AVERAGE SELLING PRICE OF ELECTRONIC HYDROFLUORIC ACID OF KEY PLAYERS, BY TYPE, 2024

5.5.3 AVERAGE SELLING PRICE TREND, BY REGION

5.6 ECOSYSTEM ANALYSIS

5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.8 TRADE ANALYSIS

5.8.1 EXPORT SCENARIO (HS CODE 281111)

5.8.2 IMPORT SCENARIO (HS CODE 281111)

5.9 INVESTMENT AND FUNDING SCENARIO

5.10 CASE STUDY ANALYSIS

5.10.1 ULTRA-HIGH-PURITY EHF ENABLING YIELD IMPROVEMENT IN ADVANCED LOGIC SEMICONDUCTORS

5.10.2 BUFFERED ELECTRONIC HYDROFLUORIC ACID INNOVATION FOR HIGH-ASPECT-RATIO 3D NAND MEMORY APPLICATIONS

5.10.3 APPLICATION-SPECIFIC ELECTRONIC HYDROFLUORIC ACID DEVELOPMENT FOR SIC AND GAN POWER SEMICONDUCTORS

5.11 IMPACT OF 2025 US TARIFF - ELECTRONIC HYDROFLUORIC ACID MARKET

5.11.1 INTRODUCTION

5.11.2 KEY TARIFF RATES

5.11.3 PRICE IMPACT ANALYSIS

5.11.4 IMPACT ON COUNTRIES/REGIONS

5.11.4.1 North America

5.11.4.2 Europe

5.11.4.3 Asia Pacific

5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

6.1 KEY EMERGING TECHNOLOGIES

6.1.1 ULTRA HIGH PURITY HYDROFLUORIC ACID PRODUCTION AND ADVANCED PURIFICATION TECHNIQUES

6.1.2 DILUTE HYDROFLUORIC ACID AND CONTROLLED ETCHING SYSTEMS

6.1.3 CIRCULAR HYDROFLUORIC ACID MANAGEMENT AND CLOSED-LOOP RECYCLING

6.1.4 VAPOR PHASE AND DRY ETCHING ALTERNATIVES

6.2 COMPLEMENTARY TECHNOLOGIES

6.2.1 ADVANCED HYDROFLUORIC ACID HANDLING MATERIALS AND EQUIPMENT

6.2.2 METAL-ASSISTED AND ENHANCED ETCHING METHODS

6.3 TECHNOLOGY/PRODUCT ROADMAP

6.3.1 HISTORICAL FOUNDATION AND CURRENT STATE

6.3.2 ULTRA-HIGH PURITY ADVANCEMENT (UP-SS AND UP-SSS GRADES)

6.3.3 ADVANCED PURIFICATION AND PROCESS CONTROL TECHNOLOGIES

6.3.4 CONTAMINATION-FREE PACKAGING AND DELIVERY SYSTEMS

6.3.5 LOCALIZATION AND FAB-ADJACENT MANUFACTURING TECHNOLOGIES

6.3.6 SUSTAINABILITY, SAFETY, AND REGULATORY-DRIVEN INNOVATION

6.4 PATENT ANALYSIS

6.4.1 METHODOLOGY

6.4.2 PATENTS GRANTED WORLDWIDE, 2015-2024

6.4.3 PATENT PUBLICATION TRENDS

6.4.4 INSIGHTS

6.4.5 LEGAL STATUS OF PATENTS

6.4.6 JURISDICTION ANALYSIS

6.4.7 TOP APPLICANTS

6.4.8 LIST OF MAJOR PATENTS

6.5 FUTURE APPLICATIONS

6.5.1 AI-DRIVEN AUTONOMOUS CHEMICAL DELIVERY & PURIFICATION SYSTEMS

6.5.2 ASEPTIC/ULTRA-LOW-OXYGEN HERMETIC PURIFICATION & DELIVERY SYSTEMS

6.5.3 RESOURCE-RECOVERY & REGENERATION SYSTEMS FOR WASTE VALORISATION & CIRCULAR CHEMICAL PLANTS

6.6 IMPACT OF AI/GEN AI ON ELECTRONIC HYDROFLUORIC ACID MARKET

6.6.1 TOP USE CASES AND MARKET POTENTIAL

6.6.2 BEST PRACTICES IN ELECTRONIC HYDROFLUORIC ACID MANUFACTURING

6.6.3 CASE STUDIES OF AI IMPLEMENTATION IN ELECTRONIC HYDROFLUORIC ACID MARKET

6.6.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

6.6.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN ELECTRONIC HYDROFLUORIC ACID MARKET

6.7 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

6.7.1 SOLVAY: ULTRA-HIGH-PURITY ELECTRONIC HYDROFLUORIC ACID FOR ADVANCED SEMICONDUCTOR MANUFACTURING

6.7.2 STELLA CHEMIFA CORPORATION: PROCESS-INTEGRATED ELECTRONIC HYDROFLUORIC ACID SOLUTIONS FOR LOGIC, MEMORY, AND DISPLAY FABS

6.7.3 HONEYWELL INTERNATIONAL INC.: DIGITALLY ENABLED, HIGH-PURITY ELECTRONIC CHEMICALS FOR RESILIENT SEMICONDUCTOR SUPPLY CHAINS

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

7.1 REGIONAL REGULATIONS AND COMPLIANCE

7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

7.1.2 REGULATIONS RELATED TO ELECTRONIC HYDROFLUORIC ACID

7.1.3 INDUSTRY STANDARDS

7.2 SUSTAINABILITY INITIATIVES

7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF ELECTRONIC HYDROFLUORIC ACID

7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

8.1 DECISION-MAKING PROCESS

8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

8.2.2 BUYING CRITERIA

8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

8.4 UNMET NEEDS IN ELECTRONICS AND SEMICONDUCTOR INDUSTRY

8.5 MARKET PROFITIBILITY

8.5.1 PREMIUM PRICING DRIVEN BY ULTRA-HIGH PURITY REQUIREMENTS

8.5.2 HIGH SWITCHING COSTS AND LONG-TERM CUSTOMER LOCK-IN

8.5.3 ECONOMIES OF SCALE AND CAPITAL INTENSITY ADVANTAGES

8.5.4 STRONG DEMAND VISIBILITY FROM SEMICONDUCTOR CAPACITY EXPANSION

8.5.5 VALUE-ADDED SERVICES AND MARGIN EXPANSION OPPORTUNITIES

9 ELECTRONIC HYDROFLUORIC ACID MARKET, BY GRADE

9.1 INTRODUCTION

9.2 EL GRADE

9.2.1 COST-EFFICIENT PROCESSING IN ESTABLISHED SEMICONDUCTOR AND ELECTRONIC APPLICATIONS TO DRIVE DEMAND

9.3 UP GRADE

9.3.1 GROWING SEMICONDUCTOR FABRICATION AND PROCESS UPGRADES FUELING CONSUMPTION

9.4 UP-S

9.4.1 MINIATURIZATION AND COMPLEX DEVICE ARCHITECTURES PROPEL MARKET GROWTH

9.5 UP-SS

9.5.1 GROWTH IN ADVANCED LOGIC, MEMORY, AND DISPLAY TECHNOLOGIES TO DRIVE CONSUMPTION

9.6 UP-SSS

9.6.1 DEMAND IN NEXT-GENERATION 3D SEMICONDUCTOR AND FLEXIBLE DISPLAYS TO DRIVE MARKET

10 ELECTRONIC HYDROFLUORIC ACID MARKET, BY TYPE

10.1 INTRODUCTION

10.2 FLUORITE-BASED

10.2.1 EFFICIENT PRODUCTION AND CHEMICAL STABILITY FUELING FLUORITE-BASED HF APPLICATIONS IN ELECTRONICS

10.3 FLUOROSILICIC ACID-BASED

10.3.1 LOWER RAW MATERIAL DEPENDENCY AND RELIABLE CHEMISTRY TO PROPEL DEMAND

11 ELECTRONIC HYDROFLUORIC ACID MARKET, BY APPLICATION

11.1 INTRODUCTION

11.2 SEMICONDUCTOR WAFERS

11.2.1 NEED FOR ULTRA-PRECISE OXIDE ETCHING AND SURFACE CLEANING TO DRIVE DEMAND